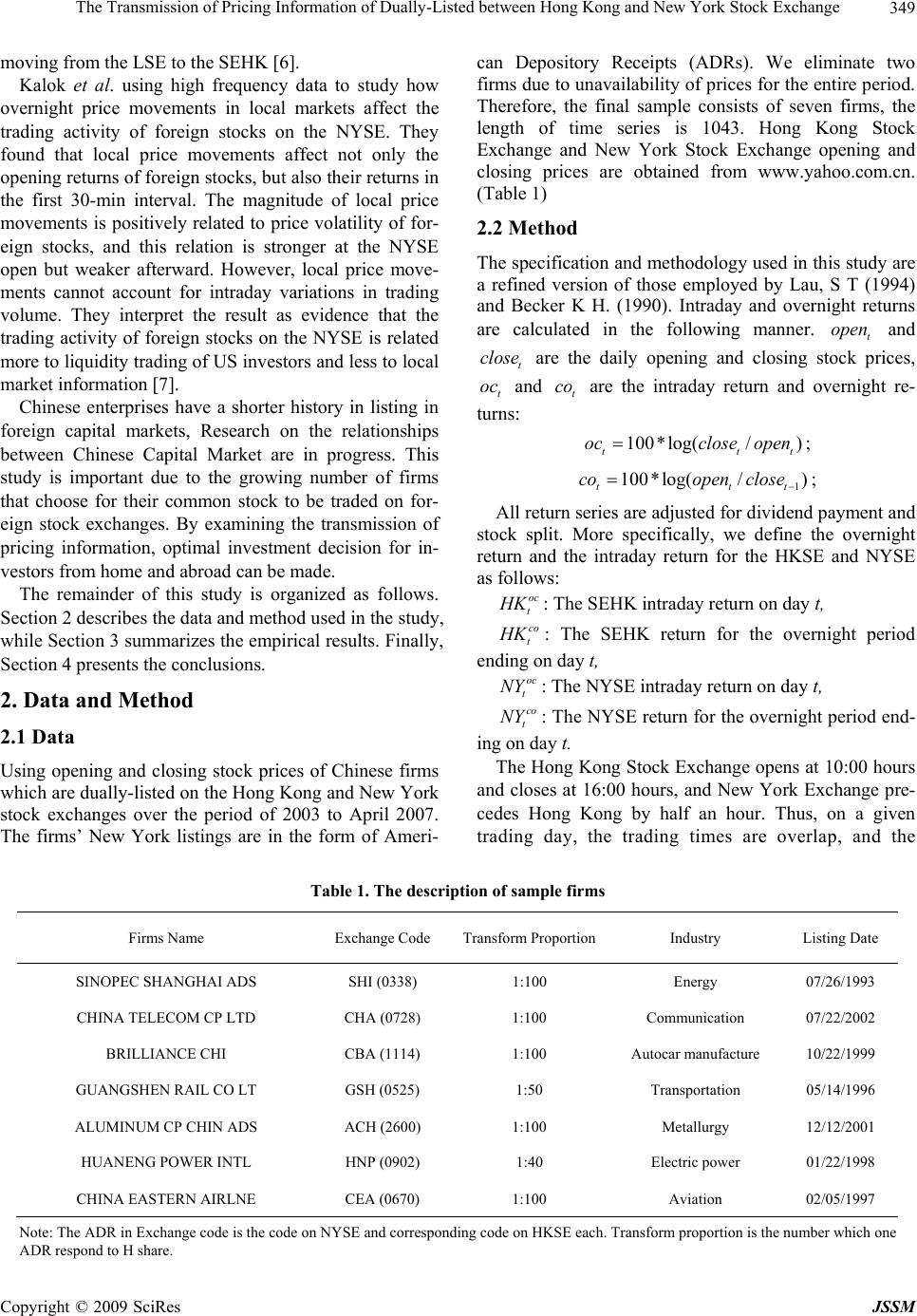

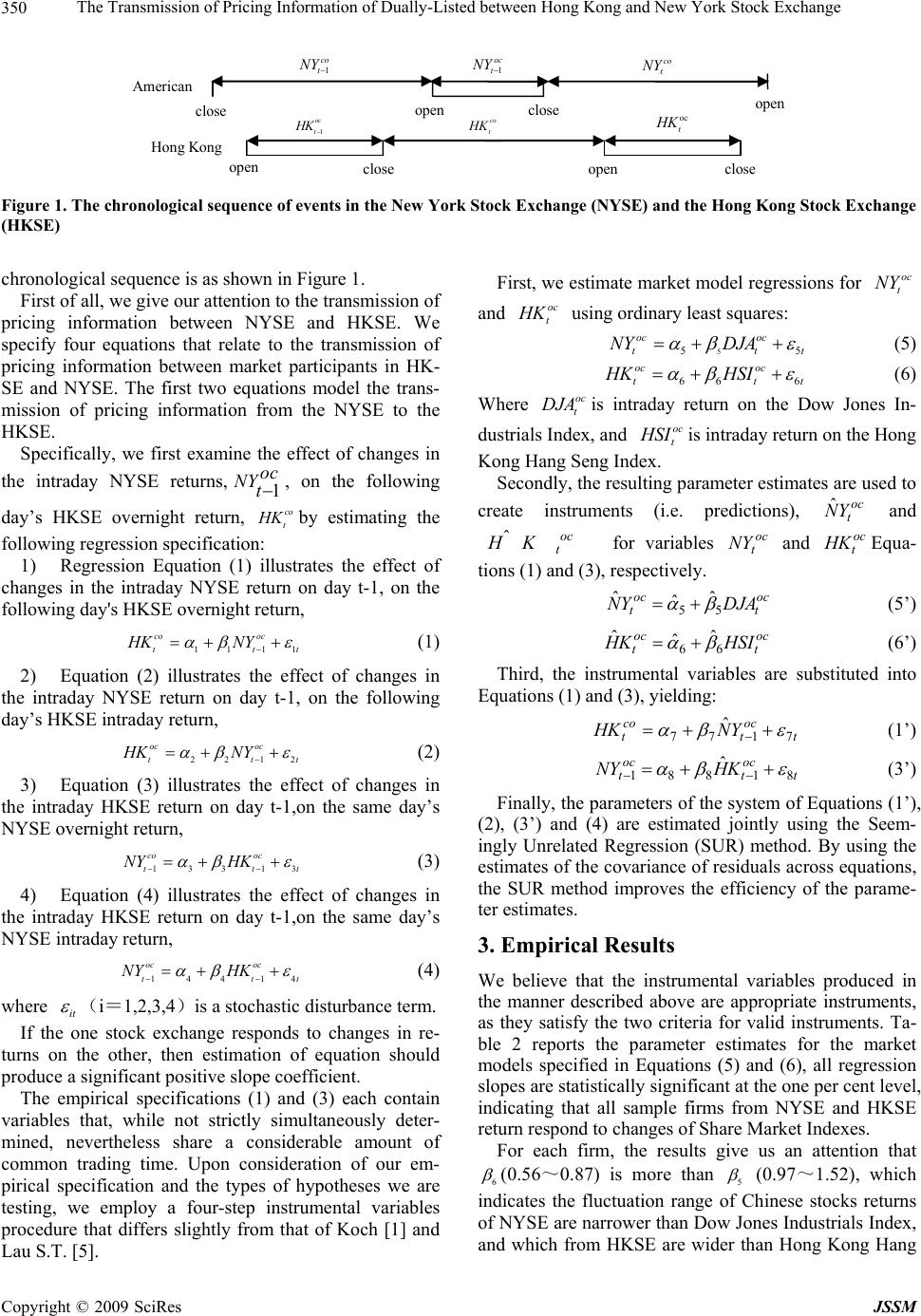

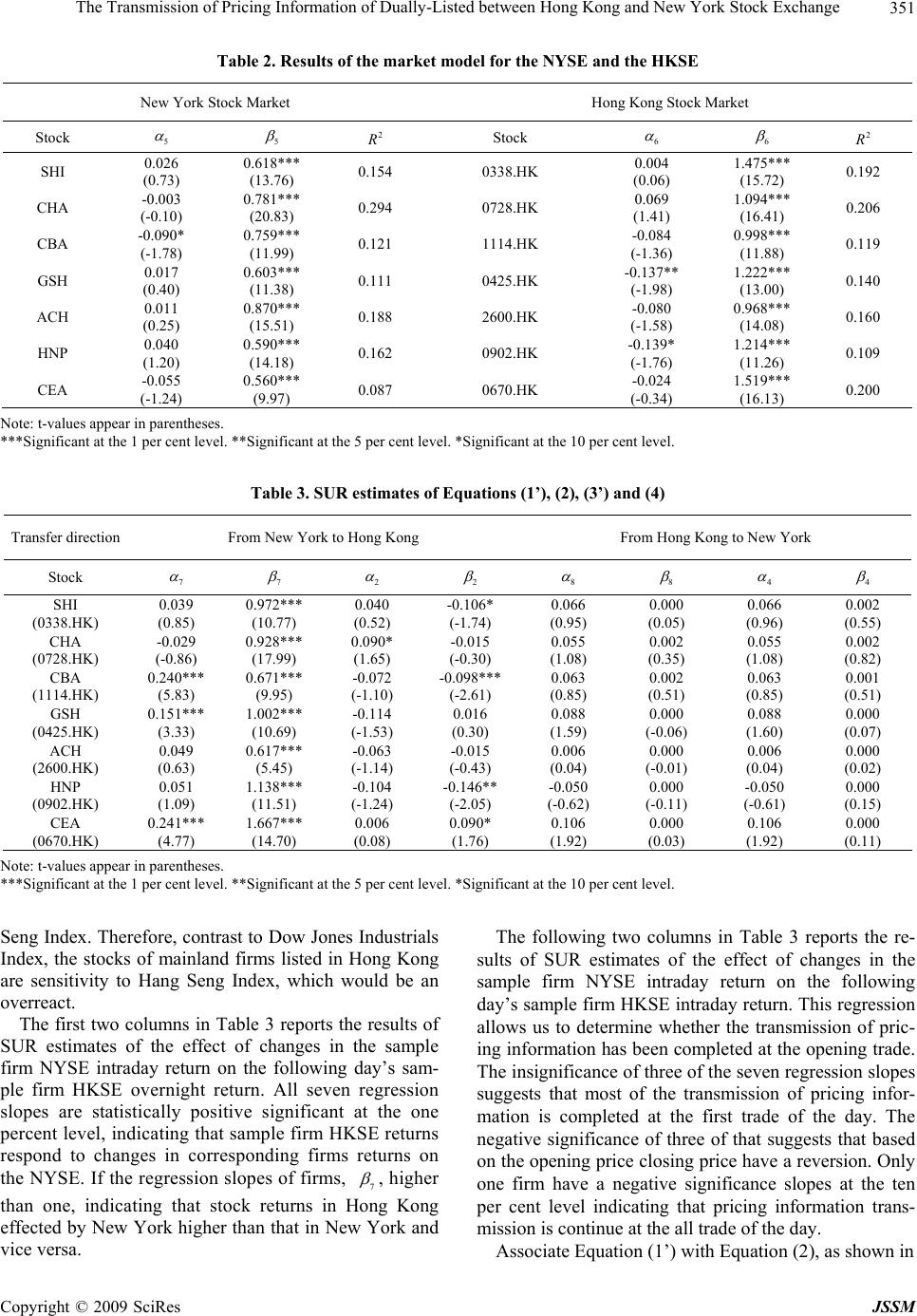

J. Service Science & Management, 2009, 2: 348-352

doi:10.4236/jssm.2009.24041 Published Online December 2009 (www.SciRP.org/journal/jssm)

Copyright © 2009 SciRes JSSM

The Transmission of Pricing Information of

Dually-Listed between Hong Kong and New

York Stock Exchange

Shuangfei LI, Shou CHEN

School of Business Adiministration, Hunan University, Changsha, China

Email: lsfhnu@163.com

Received July 31, 2009; revised September 5, 2009; accepted October 29, 2009.

ABSTRACT

The study investigates the transmission of pricing information between Hong Kong Stock Exchange and New York Stock

Exchange. Using the opening and closing stock prices of these two markets from Jan. 2003 to Apr. 2007 with the

method of Seemingly Unrelated Regression, we draw the conclusions that: 1) intraday returns of Chinese dually-listed

stocks is influenced more obviously by Hang Seng Index than Dow-Jones Average; 2) transmission of pricing informa-

tion is only from New York to Hong Kong; 3) intraday returns of stocks from New York Stock Exchange has a remark-

able influence on that of the next day in Hongkong market, but the stocks price of Hong Kong Stock Exchange has no

relation with which of New York Stock Exchange.

Keywords: Information Tra n smi ssi o n, D ually-List ed, St o ck Price

1. Introduction

In recent years, there have been quite a number of Chi-

nese companies listed in foreign capital markets. Ac-

cording to the China Securities Regulatory’s Statistics,

up to early 2006, there are a total of 120 Chinese compa-

nies listed in foreign capital markets. The market value

of China's A-Shares reaches 9 trillion RMB, while the

market value of overseas listed enterprises reaches 11

trillion RMB. At the mean time, Along with China's fi-

nancial industry is opened to external and to deepen fi-

nance reformation, more and more people begin to pay

attention to the relationships between Chinese market

and overseas securities market. The interdependence of

international equity markets has been examined exten-

sively.

The interdependence of international equity markets

has been examined extensively. Using stock market in-

dices, Koch and Koch examined relationships between

daily closing values of eight national stock indices for the

years 1972, 1980 and 1987.Their result suggested that

international stock market has grown an more interdep-

endent over time, and increased equity market interdep-

endence has been concentrated primarily between mark-

ets in neighboring countries and between markets whose

trading hours overlap [1].

Using multivariate GARCH models, Zhao L. and

Wang Y. point out there is anasymmetry in pred ictability

of the volatility of A share verses B share. Before the

openness to domestic inverstors of B share in Feb. 2001,

the volatility of B share and A share are relatively inde-

pendent. After that, there is a prominent volatility spill-

over effect from A share to B share [2].

However, using the dually-listed stock prices will de-

scribe transmission of pricing information better than

using the indices [3–4]. Using the daily opening and

closing stock prices of seven Japanese corporations that

are dually listed on the New York Stock Exchange

(NYSE) and the Tokyo Stock Exchange (TSE), Lau and

Diltz conclude that market imperfections th at may inhibit

information transfer between TSE and NYSE stock re-

turns are not readily apparent and that international list-

ings do not give rise to arbitrage opportun ities [5].

Bae investigates the transfer of pricing information

between the Hong Kong Stock Exchange (HKSE) and

the London Stock Exchang e (LSE). They find that HKSE

overnight returns respond significantly to changes in LSE

intraday returns, but the transmission pro cess is not com-

pleted at the opening of the SEHK; LSE overnight re-

turns respond significantly to changes in HKSE intraday

returns, but the transmission process is not completed at

the opening of the LSE, either; the impact is stronger