Modern Economy

Vol.07 No.12(2016), Article ID:72081,20 pages

10.4236/me.2016.712134

Informal Sector Tax Compliance Issues and the Causality Nexus between Taxation and Economic Growth: Empirical Evidence from Ghana

Bismark Ameyaw1*, Amos Oppong1, Lucille Aba Abruquah1, Eric Ashalley2

1School of Management and Economics, University of Electronic Science and Technology of China, Chengdu, China

2Institute of Fundamental and Frontier Sciences, University of Electronic Science and Technology of China, Chengdu, China

Copyright © 2016 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/

Received: October 2, 2016; Accepted: November 14, 2016; Published: November 17, 2016

ABSTRACT

Revenues generated from taxes constitute a major source of income for governments. However, the epic display of tax evasion by individuals and firms in most countries has induced researches on the factors accounting for tax evasion in developing countries. Therefore, this study is conducted to investigate the determinants of the informal sector compliance issues and the causality nexus between tax evasion and Gross Domestic Product (GDP). This research solely adopts the theory of planned behavior in analyzing tax compliance issues. The research work is divided into two parts. In analyzing the informal sector compliance issues, questionnaires were submitted to 600 respondents comprising informal sector taxpayers in all the ten regions in Ghana. Regression analysis was employed in our study to depict the results of the informal sector compliance issues. The result revealed that attitudes, subjective norm and perceived behavioral control are the main determinants of the informal sector compliance issues. The second part of this research examined the causality between taxes and GDP in Ghana’s economy over the period of 1980-2015. The data were analyzed by employing the Augmented Dickey Fuller Unit Root test, the variables were found to be integrated of the order one and the Johansen test showed the presence of co-integration between the variables. The Granger causality test for the study indicated a unidirectional causality from taxation to GDP. Therefore, the study recommends that efforts should be geared towards the improvement of tax systems in order to augment the GDP of the country.

Keywords:

Taxation, GDP, Granger Causality, Theory of Planned Behavior

1. Introduction

Taxpayers’ ethical values play an important role in the compliance decision of individual taxpayers [1] . It is therefore asserted that individuals possessing sturdier ethical beliefs seem to have auspicious compliance attitude with the reason being that such individuals see compliance as either a responsibility or obligation that must be honored with respect [1] . In consonance with [1] , [2] argued that there exists a direct effect running from ethical value to the compliance decision of an individual. Ethical beliefs are the most important factors to consider in improving compliance decisions of individuals comprising the informal sector [3] . Tax compliance is deemed higher when there exists a sturdier belief that tax evasion is unethical [4] .

Compliance issues are different from both the country and the individual at stake [5] . Issues of compliance may take the form of taxpayers’ perception on tax system [6] , taxpayers’ understanding of tax laws [7] , punishments such as penalties [8] , the cost incurred in complying to taxes [9] and perceived behavioral control [10] . Discussions on tax compliance issues and decisions should measure attitudes and prevailing social norms citizens perceive when honoring their tax duties [6] . [11] argued that compliance to taxes corresponds an increment in audit and income rates thereby causing a reduction in tax rates. Tax compliance among citizens may surge when citizens benefit from their tax payments whiles the reduction or surge in tax fines seems to have few effects on compliance decisions of taxpayers [11] . The traditional approaches in solving tax compliance issues among taxpayers propose policies oriented to punishment such as penalty rate [11] . However, those traditional approaches failed to completely give an in-depth insight into compliance behaviors because much emphasis was placed on economic factors ignoring psychological approaches to tax noncompliance [12] . Irrespective of the economic models and psychological models, certain scholars suggest that noncompliance decision is affected by factors outside the basic model in ways not actually captured by those compliance theories [13] .

The causality nexus between tax evasion and GDP seems not to reach a general conclusion due to numerous results obtained by scholars. A study conducted by [14] concluded that there exists a unidirectional causality between tax evasion and GDP whereas studies conducted by [15] [16] also asserted that there exists a bidirectional causality between tax evasion and GDP.

Many traders travel several miles to trade in Accra. Based on that, more businesses are springing up in Accra (Ghana’s capital) due to its industrious nature. More business owners are registering their businesses in order to file their tax returns and vice versa. The rise in businesses issues of tax compliance has remained a challenge in this assembly and as such, it is prudent to investigate into taxpayers’ compliance issues in this assembly and the causality nexus between tax evasion and GDP in Ghana as a whole.

2. Review of Literature

Most governments struggle in achieving laid down long and short term developmental goals due to tax non-compliance. Across the world taxes are deemed as the most expedient means through which government fund their projects and expenses. The evasion of taxes has attracted huge concerns from policy makers and international bodies because it impends the capacity of government in raising revenue to fund government expenditures [2] . Tax evasion poses much threat to emerging and developing countries due to their vulnerability in economic stability [17] . Revenues generated by governments to fund its expenditure hinges on solely on taxpayers’ willingness to comply with tax laws [18] . Empirical findings on tax compliance issues in developed countries from [19] [20] cannot be applied to developing and emerging countries due to the differences in socio-political and demographic compositions thereby calling for more pragmatic approach in analyzing compliance behaviors of taxpayers’ in these countries [21] . The neoclassical approach in modelling tax evasion accentuates tax rate, magnitude of fines, level of income and audit probability as the core methods in curbing noncompliance issues but such an approach has been heavily criticized by [22] based on the fact that the neoclassical approach heavily relies on economic approach ignoring the psychological approach in curbing these challenges [22] . This challenge ushered in new approaches in analyzing compliance behaviors of taxpayers [23] . In consonance with [23] , [12] postulated non-compliance factors such as taxpayers’ attitude, taxpayers’ perception on tax fairness, and other demographic factors as the main determinants of tax compliance. [24] asserted that taxpayers perceived fairness in tax systems encourages tax non-compliance.

Issues pertinent to tax compliance cost has induced researches identifying plentiful factors affecting taxpayers’ compliance behaviors [25] . In explaining compliance behaviors two theories comes to play-economic based theory which underscore incentives, and the psychological-based theories which emphasize attitude [26] . Key players in analyzing compliance behaviors may include attitudinal traits, economic, structural and demographic factors. In dealing with compliance issues, it is invaluable to take into consideration individual’s verdict to comply with tax laws. The economic factors postulate on the premise that taxpayers’ will respond to sanctions on tax non-compliance [27] .

2.1. Tax Compliance Economic Factors

In explaining the economic factors of tax compliance, tax rate, actual income level, tax audit, tax benefits, fines-penalties and audit probabilities are considered important.

Tax Rate: Tax rate compliance decision has induced mixed results. Some pioneering authors [8] [14] argue that the increment in tax rates would automatically increase compliance to taxes whereas [28] possesses a contrary view. [28] postulated that the surge in marginal tax rate has absolutely zero effect on tax evasion and compliance behaviors. In other views, the persistent evasion of taxes by individuals rather increases tax rates. Based on the above review, there exists a contradictory empirical outcome on the upshot of tax rates on the level of tax compliance. Empirical evidence on the comparisons between the effects of tax rates on the level of tax compliance in different country should be considered negligible if the tax systems in these two countries are considered different [29] . It is difficult to flout the contributions of tax rate and income effects on tax compliance level in experimental research. In field research, opportunities for tax evasion and source of income interact with tax rates thereby posing an adverse effect on compliance decisions of taxpayers [5] .

Actual Income Level: In discussing the actual income level, we discussed the level of income for the self-employed, employed taxpayers, income earned through effortless job and hard work earned income. In general, the employed tends to have a lower effort not to comply to taxes than the self-employed. In most countries, the employed taxpayers experience tax deductions from their salary packages before they received their salary. On the contrary, the self-employed files their tax returns themselves thereby offering them a great opportunity to underreport their income levels in order to evade taxes. An empirical evidence shows that there is a greater percentage of tax compliance on taxpayers’ income earned through effortless work [5] . On the contrary, taxpayers are more reluctant to lose their hard work earned income to tax officials [5] .

Tax Audit: Intensifying audit systems and structures deters tax officials [8] . However, it is explicit that tax audit breeds administration cost. Intensifying audit systems also generates adverse effects on other administrative functions such as tax collection [29] . It is complex to measure the level of tax audit intensification because audit systems have no general process and procedures. The number of taxpayers for audit processes is also difficult to measure in most developing countries. Tax records and tax registration of businesses is still a challenge which hasn’t been solved. With respect to this challenge, tax authorities audit those few registered businesses leaving the unregistered businesses. Due to this, most business owners in the developing countries do not comply with taxes due to tax system slacks.

Tax Benefits: The institution of tax benefits has a mixed effect on tax compliance. First, if tax benefits are given to certain individuals or entities, it may encourage tax compliance because the amount of taxes to be paid may be lower than expected. However, the problem arises when most entities converts their organizations to different forms just to enjoy tax benefit. This problem breeds non-compliance behaviors thus posing an effect on the annual tax revenues generated.

Fines and Penalties: In a popular assertion, the upsurge in fines deters taxpayers away from the non-compliance to taxes. However, if fines are set too high, taxpayers would possibly and legally find the loopholes in tax systems to circumvent the payment of taxes. Moreover, the institution of flat fines does not serve as a deterrence measure. For example, linking flat fine structure to the relative income level of citizens seems fair. The middle and high income earners would not be directly affected by fines as compared to a low income earner. Therefore, the effectiveness of fines in deterring taxpayers into complying with taxes should be linked with their actual level of income to ensure effectiveness. Additionally, penalty rates are different depending on the kind of evasion and evasion behaviors. For example, there exist different penalty rates and sentences for under-reporting, non-filing etc. Unintentional non-compliance attracts lower penalties as compared to the intentional non-compliance [29] .

Audit Probabilities: Several authors [28] [30] have predicted the impact of audit probabilities on tax compliance as feeble. Threatening taxpayers with audit probabilities somehow encourages compliance by the low and middle level income earners whiles the high level income earners are left out [30] . Subjective and objective audit probabilities are invaluable in explaining compliance issues. Subjective audit probability has more effect on compliance than the objective audit probability [28] . Taxpayers ultimately weigh the successful evasion gains to the consequence attached to detection and punishment. This opportunity cost motivates taxpayers into priory auditing their books beforehand. Taxpayers mostly fear that an increase in the probability of detection connotes huge income declaration [8] . Rightfully, the subjective probability of being audited serves to have a greater impact on compliance decisions since the decision lies solely with tax authorities. Therefore, an imprecise information about auditing a particular entity renders panic to such entities to comply with taxes than setting actual date for audit.

2.2. Reforms on Tax Compliance in Ghana

Compliance to taxes in Ghana has engrossed numerous reforms in Ghanaian tax systems. In 2011, the introduction of e-government project aimed at electronically link tax payments of registered businesses to both the GRA and the Registrar Generals Department (RGD) to track tax payment processes and procedures [28] . In an effort to improve tax systems in Ghana, the Internal Revenue Service (IRS), the Customs Exercise and Preventive Service (CEPS), the Value Added Tax Service (VAT) and the Revenue Agency Governing Body (RAGB) amalgamated in 2009 in accordance with the Ghana Revenue Authority (GRA) Act 791 in order to come out with strategies to ensure tax compliance. The core basis of the amalgamation of these independent bodies into the GRA was to integrate the management of domestic tax and customs, modernize domestic tax and customs operations through accurate and appropriate review processes and procedures and to integrate VAT and IRS into domestic tax and functional lines [28] . The Large Taxpayer Unit (LTU) was also established in 2004 for the integration of tax administration duties as well as serving as one stop shop operation for taxpayers. The taxpayer identification number was instituted to augment tax collection and payment effectiveness in 2002. The formulation of revenue policies, tax reforms management and supervisory service to CEPS and IRS called for the formulation of the National Revenue Secretariat (NRS) in 1986. In curbing the slack fiscal adjustment program designed in 1983 in reinstating Ghana’s tax base, the administrative reform of 1985 was introduced to enhance tax administration efficiency [28] . Also, the slack fiscal adjustment programme called for the invention of VAT to curtail vicissitudes in reference to the conduct of economic agents [31] .

Irrespective of taxpayers’ perception about fairness in tax systems and tax administration, the complex nature of the Ghanaian tax systems and laws affect compliance behaviors. The amendment of the Internal Revenue Act 2000 of Ghana (Act 592) states in section 1 that that “a person who has a chargeable income shall pay subject to this Act, for each year of assessment income tax as calculated in accordance with this Act”. This Act therefore imposes responsibility on citizens to comply to taxes but taxpayers’ compliance on tax authorities view seems to be a challenge [21] . [32] argued tax compliance decisions depends on lack of understanding of tax systems, apathy towards government and improper book keeping. The complexity of tax systems and laws is seen as a probable reason for tax non-compliance [33] . In line with this [34] argued that tax systems should be simple and clear in order to breed total understanding from taxpayers. It is important to note that taxpayers’ demand accountability from revenues mobilized from taxpayers’ by the state [32] . Lack of meaning accountability by the state may cause slack in compliance decisions of taxpayers. Citizens complying to tax payments should ginger governments to provide expenditure records of the usage of tax revenues [35] .

3. Materials and Methods

3.1. The Allingham and Sandmo (A-S) Model

The Allingham and Sandmo Model stresses the benefits of successful evasion against the risk involved in detection and punishment. The focal view of A-S model is that individuals comply to taxes due to the panic involved in detection. In explaining this focal view, it is assumed that an individual receives a fixed income (I) and must decide how much of this income to report and underreport to tax authorities. The amount of Income declared (D) attracts tax rate (T) whiles no taxes are paid on underreported income. In a situation where an individual underreport income, the individual may be audited with a fixed probability (P). All underreported income will be retrieved and a fine rate (F) on each income that was supposed to be paid but wasn’t paid. Individuals investigated for underreporting of income are worse off because such a decision leads to fine rates whereas individuals who isn’t audited for underreporting seems better off. With the A-S model, taxpayers have two decisions to make. Taxpayers may opt to declare their true income or may underreport their income. The model therefore suggest that declared income hinges on I, P, F and T. Therefore, D = f (I, P, F, T).

Furthermore, it is important to note income attracts expenditure back to the government. Therefore, compliance to taxes may directly depend on the benefit taxpayers derives from tax payments on public goods funded. Government expenditure is denoted (G) and this causes the initial model to be D = f (I, P, F, T, G).

The A-S model has attracted numerous criticisms because it fails to focus on other germane noneconomic aspects (Table 1). Such criticisms have gingered research into making extensions to the A-S model and the adoption of non-economic models. This research focuses on the Theory of Planned behavior in coming out with our research hypothesis.

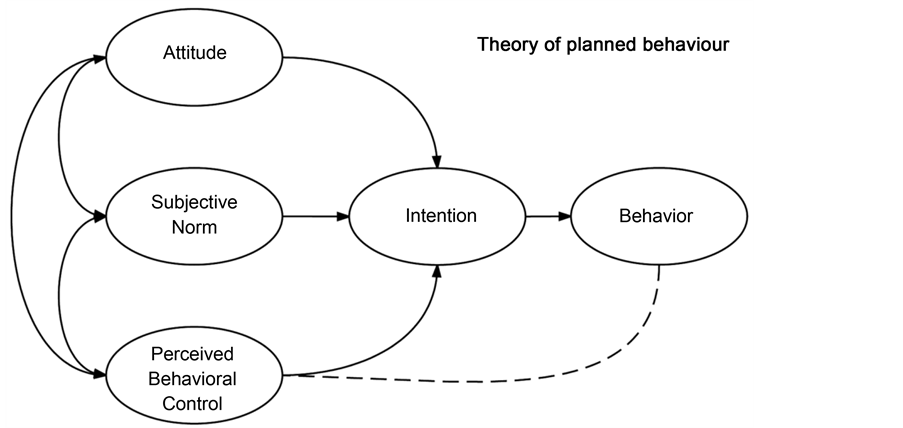

3.2. Theory of Planned Behavior

The Theory of Planned Behavior (TPB) came out as an extension to the Theory of

Table 1. Prediction of the A-S model on tax compliance.

Data source: Authors prediction on A-S model.

Reasoned Action (TRA). The core emphasis on the TRA was based on voluntary behavior. It was realized that the behavior seems not voluntary and under control. This led to the inclusion of perceived behavioral control. Such an inclusion led to the TPB. TPB predicts that behavior can be deliberate and planned. The TPB asserts that an individual intention of coming out with a behavior is the best predictor of whether or not such a behavior will actually be performed. The best predictor of a behavior is the behavior a person actually shows. The TPB posits that human action is guided by Attitude toward the specific behavior, the normative belief expectations and perceived behavioral control.

According to the TPB, attitude is a function of behavioral belief. The belief links the behavior to an outcome. The linkage of behavioral attributes to actual behaviors can be valued positively or negatively and that it is possible to acquire and attitude towards a behavior. The favoring of behaviors individuals has strong emotional ties which have desirable consequences as opposed to the forming of unfavorable attitude leading to undesirable consequence. Basically, behavioral belief and the importance of belief serves as a yardstick for measuring attitudes.

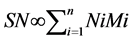

Subjective norms focus on the expectations that referent individuals approve or disapprove a specific behavior. In measuring subjective norms, the strength of each normative belief is multiplied with an individual motivation to complying with a specific behavior from a particular referent. Subjective norms are proportional to the sum of resulting product obtained. Therefore, subjective norm is a function of motivation and normative belief.

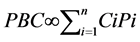

Perceived behavioral control is also determined by control beliefs determined by the presence or absence of opportunities and requisite resources. These control beliefs may be influenced by experiences of friends, second hand information about such a behavior and other factors that maximizes or minimizes the difficulty in performing the behavior in question. The possession of adequate resources and opportunities and the fewer obstacles individuals anticipated connotes the greater their perceived control over the behavior. Perceived behavioral control is a function of control belief and perceived power.

Theory of Planned Behaviour

In psychology, theory of planned behavior (TPB) is a theory that associates beliefs with behaviors. TPB is a theory that gives an in-depth knowledge about human behaviors. TPB asserts that attitudes, subjective norms and perceive behavioral control shapes individuals’ behaviors and behavioral intentions.

3.3. Research Hypothesis

3.3.1. Hypothesis 1: Taxpayers Attitude Positively Influence on Intention to Comply

Attitudes towards an action or event may be satisfactory or unsatisfactory. According to [28] , taxpayers with satisfactory attitudes towards the evasion of taxes are less compliant as compared to taxpayers with unsatisfactory attitude towards tax evasion. An empirical result from [1] postulates that persons with sturdier and favorable attitude may depict positive compliance intention because they will see tax compliance systems as a responsibility that must be honored at all cost [36] . Widely accepted empirical evidence asserts that ethical value may affect a person’s tax compliance intention [2] . Taxpayers who regard tax evasion as unethical are predicted to comply to taxes more that taxpayers who regard tax evasion as ethical [37] .

Attitudes towards tax compliance may stem from numerous factors. However, this research work will consider taxpayers’ perception on tax system fairness and their risk preference as the main attitudinal determinants that influences tax compliance intention. Unfairness in tax systems will motivate taxpayers to engross themselves in noncompliant intentions [38] . [25] reported a significant negative relationship fairness in tax systems and tax evasion. It is reported that, taxpayers have less satisfactory attitude towards tax systems as a result of low compliance levels [39] . [26] revealed that there exists a significant positive relationship between tax system fairness and intention to comply. Risk preference is seen as a distinctive feature of an individual that influences an individual’s attitude [40] . It is widely asserted that taxpayers’ attitudes to risk cannot be underestimated in compliance intentions [41] [42] . Individual taxpayers’ decisions may be influenced by their attitudes towards risk [43] . There exist inconsistencies in the taxpayers’ decision due to uncertainties of what might occur tomorrow therefore it cannot be always conclude that attitudes have a strong positive effect on intention to comply because individuals or taxpayers’ risk preference varies according to the situation at hand or the challenges individuals faces [44] .

3.3.2. Hypothesis 2: Taxpayers Subjective Norms Have Positive Effect on Intention to Comply

Subjective norms are expectations important individuals believe or expect a taxpayer to act. Subjective norms are basically the perceived social pressure to engage or not to engage in a specific behavior. In evaluating the course of an action, subjective norm may be the first norm to be considered. Subjective norms assist taxpayers’ in determining whether compliance to tax laws may lead to approval or disapproval by taxpayers’ closest groups. The relationship between subjective norms and tax compliance is deemed complex prompting [45] to argue that concurring behavior should be elicit by social norms when taxpayers’ finds within a group to which such norms are ascribed. The importance of subjective norms is postulated by the theory of planned behavior thus subjective norms have played crucial part in analyzing compliance behaviors. Empirical evidence from [46] [47] concluded that there exists a significant positive relationship between subjective norms and tax compliance intentions. Understanding subjective norms calls for in-depth knowledge about the number of persons or referent groups around the taxpayer who supports tax compliance, the surge in the needed support of other taxes on tax compliance and the higher the intention to comply [48] . It is important to note that the negative attitude towards tax compliance by people surrounding the taxpayer will have a corresponding effect of tax noncompliant by the taxpayer [49] . Empirical evidence from [50] [51] [52] proves that subjective norms have positive effect on compliance intentions.

3.3.3. Hypothesis 3: Perceived Behavioral Control Have a Positive Effect on Intention to Comply

Perceive behavioral control is seen as an important determinant for the exhibition of an actual behavior [48] . Numerous researches and empirical evidence has predicted perceive behavioral control not to have an accepted standard measure [53] . Perceive behavioral control can also be denoted as “perceive confidence”, “perceive difficulty”, and “perceive control”. Perceive behavioral control is mostly allied to a specific behavior only if such perceive control is in consonance with the actual or intended control a person has over his behavior [53] . Empirical evidence from [54] [55] indicates that perceived behavioral control positively influences behavioral intention. With reference to taxation [47] argued that there is a positive correlation between perceive behavioral control and intention to comply. An in-depth analysis of perceive behavioral control in the ethical field also concluded a positive relationship between perceive behavioral control and intention to comply [55] .

Difficulty in explaining perceived behavioral control has been brought to limelight by various researchers. Understanding an individual perceive behavioral control has been a challenge thus calling for various approaches in explaining this concept due to its subjective nature. Due to the subjective nature of perceive behavioral control, new variables like moral ethics and obligation have been fused into this concept in order to come out with accurate conclusions about an individual perceived behavioral control [26] [47] . Perceived behavioral control has also prompted researchers into culminating various external approaches such as resource availability and internal approaches such as skill, ability and confidence into its analysis [56] .

3.3.4. Hypothesis 4: Intention to Comply Has a Positive Effect on Tax Compliance Behavior

Intention to comply is basically defined as a determination or a concerted effort to mobilize an action in order to undertake or implement a behavior. Empirical evidence from [57] indicates that intention to comply has a positive effect on tax compliance behavior. Likewise, empirical evidence from [58] proved that intention to comply has a significant positive effect on tax compliance behaviors. Empirical evidence from Indonesia indicated that intention to comply momentously influence compliance behaviors pertaining with taxes [52] [59] . Additionally, [26] also asserted that intention to comply positively influences tax compliance behaviors.

3.3.5. Hypothesis 5: Taxation Granger Causes GDP and Vice Versa

The impact of taxes on GDP has attracted numerous researches worldwide. A study by [60] concluded that income taxes of corporations significantly influence GDP. An empirical evidence from [61] revealed 0.2% - 0.3% difference in rates of growth with reference to key tax reform thus predicting that such effect may negatively affect individuals’ standard of living. Conclusion drawn by [62] reveal that shares in property and personal taxes positively impacted GDP whiles shares in goods and services taxes negatively affected GDP hence prompting the argument that GDP has an influential effect on tax mix. Empirical analysis from [63] postulated that GDP has a significant on tax. Taxation is also seen as a fiscal policy instrument used to stimulate the growth of an economy [64] . With reference to causality, [65] concluded that Petroleum Profit Tax (PPT), Companies Income Tax (CIT) and Customs and Excise Duties (CED) grange causes GDP.

3.4. Research Design and Data Collection

In analyzing the variables pertaining to the theory of planned behavior, this research study espoused qualitative and quantitative research approach. In ensuring precision, objectivity and result accuracy, logical reasoning is applied to reflect respondents’ responses. Qualitative data was obtained through taped interviews and field notes. A 5 point Likert scale ranging from Completely disagree to Completely agree with neutral scores amidst the two scores was also used in analyzing the quantitative data. Completely disagree, Disagree, Neutral, Agree and Completely Agree is denoted by 1, 2, 3, 4, and 5 respectively. Primary data was obtained using questionnaires containing individual judgement of the variables examined. The questionnaires consisted of two sections with the first section consisting of biographic information and the second section comprising Likert scale items. The survey was conducted comprising 600 petty traders and medium scale owners from the ten regions of Ghana with 60 respondents from each region. Respondents included market women, beauticians, artisans, sole proprietorship businesses. Microsoft excel and Statistical Package for the Social Sciences (SPSS) was employed to analyzed respondents’ quantitative data. Questioners retrieved from respondents were analyzed using descriptive statistics, factor analysis and regression analysis. Reliability and validity test was undertaken to obtain the strength of each construct.

In analyzing the causality nexus of taxation and GDP, time series data sourced from Ghana Statistical Service (GSS), Bank of Ghana (BoG) daily and annual bulletin and Internal Monetary Fund (IMF) annual reports. The data comprises Taxation (Tax on Petroleum (TOP), Company Income Tax (CIT), Custom and Excise Duties (CED), Personal Income Tax (PIT) and Petroleum Profit Tax (PPT)) and GDP for the period of 1980-2015. This study uses the granger causality test to examine the direction of causality between tax and GDP. Econometric test like the Augmented Dickey Fuller unit root test, co-integration test and the vector error correction model were employed in this research to ascertain the variables long run relationship and data stationarity. The econometric views were used in carrying out this analysis.

4. Research Analysis Presentation and Discussion

4.1. Primary Source Data Presentation

Out of the 600 questionnaires submitted, 541 constituting 90.16% was retrieved. The 541 cases constituted 321 (59.3%) females and 220 (40.6) males. On the score of age, 311 (57.4%) was within the age range of 30 and below, 124 (22.9%) fell into the age range of 31 to 45 whiles 106 (19.6%) also fell within the age range of 46 and above. The count of occupation constituted 281 (51.9%) petty traders, 99 (18.3%) beauticians, 60 (11.1%) artisans and 101 (18.6%) sole proprietorship business owners. 60 questioners were submitted to respondents of each regional capitals of Ghana with 54 (90%) retrieved from Accra (Greater Accra Region), 56 (93.3%) from Koforidua (Eastern Region), 55 (91.6%) from Takoradi (Western Region), 48 (80%) from Kumasi (Ashanti Region), 57 (95%) from Cape Coast (Central Region), 52 (86.6%) from Ho (Volta Region), 53 (88.3%) from Sunyani (BrongAhafo Region), 56 (93.3%) from Tamale (Northern Region), 55 (91.6%) from both Bolgatanga (Upper East Region) and Wa (Upper West Region).

Table 2 depicts an average respondent’s answer to questionnaires on attitudes, perceived behavioral control, intention to comply and compliance behavior more than 4 indicating that respondents agree to each of the questions posed under each of the

Table 2. Summary statistics of variables.

Data source: Authors field survey.

variables. Of all the constructs, only subjective norm had an average value less than 4 suggesting that respondents nearly agreed that subjective norms have a positive impact on compliance behavior.

Table 3 represents validity (discriminant validity and convergent validity) and reliability scores of the variables. Discriminant validity asserts that the correlation of different construct indicators shouldn’t be highly correlated. The value of the cross loadings depicts a high value construct for each indicator thus revealing that the instruments used in this research work is valid. Also, convergent validity asserts that the indicator can’t be removed or deleted if the loading variables are between 0.50 and 0.70. It can be seen the Communality and the Average Variance Extracted (AVE) is also greater than 0.50. The constructs depict the outer loading factor value greater than 0.70 whereas communality and AVE is also greater than 0.50.

Reliability test focuses on the consistency and accuracy of a measuring device or tool. By using all construct, the value of the reliability composite value and Cronbach alpha is greater than 0.70 and 0.60 respectively thereby proving the reliability of the instruments used in this research.

With reference to the first hypothesis, the results depicted a t statistical value of 5.5443 > 1.645 hence it can be concluded that taxpayers’ attitude positively influence intention to comply (Table 4). Also, the coefficient value of 0.46789 suggests that a positive influence from attitude to intention to comply. The result of this study is in consonance with earlier researches done by [24] [38] [66] [67] . [66] argued in various sections in his research work that taxpayers’ attitudes and perception about fairness in tax systems has a strong positive influence on a taxpayer intention to comply to various forms of taxes. Likewise, [67] postulated that unfairness in tax systems brings about negative attitudinal effects on intention to comply with taxes. The empirical evidence derived from this study implies that taxpayers with favorable attitudes towards taxes will highly comply to taxes rather than taxpayers with unfavorable attitudes towards taxes.

The second hypothesis showed a t statistical value of 5.1321 > 1.645 and the 0.48675 coefficient value implies that taxpayers’ subjective norms have a positive impact on intention to comply hence H2 is supported. It can also be concluded from the analysis

Table 3. Validity and reliability test.

Data source: Authors field survey.

Table 4. Hypothesis testing and discussions.

AT: Attitude, SN: Subjective Norm, PBC: Perceived Behavioral Control, IC: Intention to Comply, TCB: Tax Compliance Behavior. Data source: Authors field survey.

that higher tax compliance subjective norms connote higher intention to comply. The empirical evidence is consistent with researches from [47] [51] and [52] with all these authors suggesting that subjective norm positively impact intention to comply. Hence, it can also be asserted that taxpayers with higher perception of subjective norm will comply with their tax obligations than taxpayers possessing low perception on subjective norms. Thus, it can be concluded that subjective norm is a determinant of compliance intentions.

Hypothesis three stated that perceived behavioral control have a positive effect on intention to comply. Results testing showed a t statistical value of 7.8691 > 1.645. Therefore, it can be concluded that H3 is supported. 0.49144 coefficient value indicates that perceived behavioral control has a positive effect on intention to comply. Also, it can be concluded that favorable perceived behavioral control towards tax compliance predicts higher compliance intentions. The result obtained from the third hypothesis is consistent with earlier researches from [47] [54] [55] depicting that perceive behavioral control has a positive influence on intention to comply.

The empirical evidence derived from the fourth hypothesis shows that H4 is supported because the t statistics value of 12.2137 > 1.645. The coefficient value of 0.4215 indicates that intention to comply has a positive effect on tax compliance behavior. It can further be concluded that higher compliance intentions connote higher tax compliance behavior. The empirical evidence obtained from the fourth hypothesis is consistent with researches from [26] [48] [52] [59] because these researchers also proved that intention to comply has a positive effect on tax compliance behaviors. Therefore, it can be further concluded that intention to comply is a determinant of tax compliance behavior.

4.2. Secondary Source Data Presentation (Causality between Taxation and GDP)

Table 5 depicts Breusch-Godfrey Serial Correlation LM test in testing the existence of autocorrelation. The p-value figure of 0.283614 proves the non-existence of autocorrelation because the p-value is greater than the critical value of 0.05 (5%).

Empirical evidence derived from the White Heteroscedasticity test from Table 5 above shows that there is no evidence of heteroscedasticity because the p-value figures of 0.312678 and 0.301437 is greater than the critical value of 0.05 (5%) (Table 6).

The Ramsey RESET test in Table 7 above proves that there is no non-linearity in the regression model thus concluding that the model is appropriate since the p-value figure of 0.194579 is greater than the critical value of 0.05 (5%).

The Augmented Dickey-Fuller test (Table 8) submits that all the taxation variables are stationary at the first differencing (1(1)) except the Tax on Petroleum which became stationary at level (1(0)). The results further prove that all variables were significant at 1% and 5%.

The empirical results (Table 9) from the Johansen Co-integration test show that the likelihood ratios are greater than the 5% critical value. Thus, it can be concluded that there exists a long run equilibrium relationship between GDP and the taxation variables used in this research.

The Pairwise Granger Causality Test from Table 10 above depicts the causality nexus between taxation and economic growth (GDP) of a country. The results depict that all the taxation variables under consideration granger causes GDP hence implying that

Table 5. Breusch-Godfrey serial correlation LM test.

Table 6. White heteroscedasticity test.

Table 7. Ramsey reset test.

Table 8. Augmented dickey-fuller test.

GDP: Gross Domestic Project, TOP: Tax on Petroleum, CIT: Company Income Tax, CED: Customs Excise Duties, PIT: Personal Income Tax and PPT: Petroleum Profit Tax.

Table 9. Johansen cointegration test (Lags interval: 1 to 1).

taxation strongly impacts the economic growth of Ghana. The findings of the causality nexus between taxation and GDP are consistent with [60] [61] [62] [63] in which all these authors concluded that taxation has a substantial impact on GDP.

5. Conclusions and Recommendations

This study is purposely undertaken to investigate the desire of taxpayers to comply with their tax obligations through attitude on intention to comply, subjective norms on intention to comply, perceived behavioral control on intention to comply, intention to comply and tax compliance behavior and finally, the causality nexus between taxation and economic growth (GDP). Overall, the empirical evidence showed that attitude, subjective norm and perceived behavioral control have a significant positive relationship with intention to comply. Additionally, results from the empirical analysis also depicted that intention to comply has a strong positive influence on tax compliance behaviors. The conclusion drawn from taxation and economic growth (GDP) causality capturing time series data culled from 1980-2015 revealed that there exists a long-run equilibrium relationship between taxation and economic growth (GDP). The granger causality test affirms that the taxation variable Granger causes GDP. Therefore, the government and taxation related stakeholders should ensure fairness in tax systems to encourage

Table 10. Pairwise granger causality test: Lag 2.

tax compliance behaviors. Additionally, tax revenues should be spent on their intended purposes that promote the standard of living of taxpayers and the country’s development as a whole in order to encourage and augment tax compliance behaviors. Furthermore, favorable conditions should be created by policymakers in ensuring that the influential groups around the taxpayer should be in support of tax compliance behaviors. Also, corruption in tax administration should be eradicated to ensure fairness in tax systems and strategies should be adopted to restructure tax systems in general to avoid the evasion of taxes. Finally, the government and tax officials and other taxation related stakeholders should show transparency and accountability in tax revenues expenditures to encourage tax compliance behaviors from taxpayers

6. Limitations and Future Research

The sample size is not very large enough to cover all taxpayers constituting the informal sector across the ten regions of Ghana. Case study and longitudinal approaches would have been appropriate but limited time available and unwillingness of taxpayers in disclosing their identity prompted the usage of the survey approach.

In furtherance, regional comparative analysis in all the ten regions in Ghana would worth exploring as well as comparative analysis between developing, emerging and developed countries on tax compliance behaviors is recommended for future research.

Acknowledgements

I am grateful to Professor Tang Qi and Mr. Eugene Oware Koranteng for giving me support throughout this research work.

Cite this paper

Ameyaw, B., Oppong, A., Abruquah, L.A. and Ashalley, E. (2016) Informal Sector Tax Compliance Issues and the Causality Nexus between Taxation and Economic Growth: Empirical Evidence from Ghana. Modern Economy, 7, 1478-1497. http://dx.doi.org/10.4236/me.2016.712134

References

- 1. Ho, D. and Wong, B. (2008) Issues on Compliance and Ethics in Taxation: What Do We Know? Journal of Financial Crime, 15, 369-382.

http://dx.doi.org/10.1108/13590790810907218 - 2. Chau, G. and Leung, P. (2009) A Critical Review of Fischer Tax Compliance Model: A Research Synthesis. Journal of Accounting and Taxation, 1, 34-40.

- 3. Bobek, D.D. and Hatfield, R.C. (2003) An Investigation of the Theory of Planned Behavior and the Role of Moral Obligation in Tax Compliance. Behavioral Research in Accounting, 15, 13-38.

http://dx.doi.org/10.2308/bria.2003.15.1.13 - 4. Reckers, P.M., Sanders, D.L. and Roark, S.J. (1994) The Influence of Ethical Attitudes on Taxpayer Compliance. National Tax Journal, 47, 825-836.

- 5. Kirchler, E (2007) The Economic Psychology of Tax Behaviour. Cambridge University Press, Cambridge.

http://dx.doi.org/10.1017/CBO9780511628238 - 6. Ambrecht and Association and Ambrecht (1998) Increasing Taxpayers Compliance: A Discussion of the Negligence Penalty. Paper presented to the ways and Means Committee of U.S. House of Representatives, Washington DC. www.taxlawsb.com/ambrecht-law-in-the-news.php

- 7. Plumley, A.H. (1992) The Impact of the IRS on Voluntary Tax Compliance: Preliminary Empirical Results. 95th Annual Conference on Taxation, Orlando, 14-16 November 2002, 116.

- 8. Allingham, M.G. and Sandmo, A. (1972) Income Tax Evasion: A Theoretical Analysis. Journal of Public Economics, 1, 323-338.

http://dx.doi.org/10.1016/0047-2727(72)90010-2 - 9. Slemrod, J. (2007) Cheating Ourselves: The Economics of Tax Evasion. Journal of Economic Perspectives, 21, 25-48.

http://dx.doi.org/10.1257/jep.21.1.25 - 10. Palil, M.R. and Mustapha, A.F. (2011) Tax Audit and Tax Compliance in Asia: A Case Study of Malaysia. European Journal of Social Sciences, 24, 7-32.

- 11. Alm, J., Jackson, B.R. and McKee, M. (1992) Estimating the Determinants of Taxpayer Compliance with Experimental Data. National Tax Journal, 45, 107-114.

- 12. Fischer, C.M., Wartick, M. and Mark, M. (1992) Detection Probability and Taxpayer Compliance: A Review of the Literature. Journal of Accounting Literature, 11, 1-46.

- 13. Alm, J. (1999) Tax Compliance and Tax Administration. In: Bartley, H.W., Ed., Handbook on Taxation, Marcel Deker, New York.

- 14. Alkins, C. (2011) Causality Nexus between Tax Evasion and GDP. Journal of Business Economics, 3, 12-31.

- 15. Mironov, M. (2010) Tax Evasion and Growth: Evidence from Russia. IE Business School.

http://www.mironov.FM - 16. Ambrose, D. (2006) Tax Evasion and GDP in the United States. Journal of National Tax Policy, 6, 1-17.

- 17. GIZ (2010) Addressing Tax Evasion and Avoidance in Developing Countries. Deutsche Gessellschaft fur Internationale Zusammenarbeit (GIZ) GmbH.

- 18. Feldman, N. and Slemrod, J. (2009) War and Taxation: When Does Patriotism Overcome the Free-Rider Impulse? In: Martin, I.W., Mehrotra, A.K. and Prasad, M., Eds., The New Fiscal Sociology: Taxation in Cooperative and Historical Perspectives, Cambridge University Press, Cambridge, 138-154.

http://dx.doi.org/10.1017/CBO9780511627071.009 - 19. Serdan, B., Ahmet, F.C. and Tamer, B. (2011) An Investigation of Tax Compliance Intentions: A Theory of Planned Behavior Approach. European Journal of Economics, Finance and Administrative Sciences, 28, 181-188.

- 20. Aktan, C.C. and Savasan, F. (2009) Tax Morale: Empirical Evidence from Turkey. Annual Meeting of the European Public Choice Society, Izmir, 8-11 April 2010.

- 21. Alabede, O.J., Zainol, A. and Kamil, M.I. (2011) Determinants of Tax Compliance Behaviour: A Proposed Model for Nigeria. International Research Journal of Finance and Economics, 78, 121-136.

- 22. Likhovsk, A. (2010) Is Tax Law Culturally Specific? Lessons from the History of Income Tax law in Mandatory Palestine. Theoretical Inquiries in Law, 11, 725-763.

http://dx.doi.org/10.2202/1565-3404.1257 - 23. Alm, J., Kirkchler, E., Muehlbacher, S., Gangl, K., Hofmann, E., Kogler, C. and Pollai, M. (2011) Rethinking the Research Paradigms for Analyzing Tax Compliance Behavior. The Shadow Economy, Tax Evasion and Money Laundering, Münster, 34.

- 24. Richardson, D. (2006) Determinants of Tax Evasion: A Cross-Country Investigation. Journal of International Accounting, Auditing and Taxation, 15, 150-169.

http://dx.doi.org/10.1016/j.intaccaudtax.2006.08.005 - 25. Christian, A. (2005) The Shirts off Their Backs: How Tax Policies Fleece the Poor. Christian Aid Briefing. www.christianaid.org.uk/images/the_shirts_off_their_backs.pdf

- 26. Trivedi, V.U., Shehata, M. and Mestelman, S. (2005) Attitudes, Incentives, and Tax Compliance. Canadian Tax Journal, 52, 29-61.

- 27. Wallschutzky, I.G. (1984) Possible Causes of Tax Evasion. Journal of Economic Psychology, 5, 371-384.

http://dx.doi.org/10.1016/0167-4870(84)90034-5 - 28. Kirchler, E., Hoelzl, E. and Wahl, I. (2008) Enforced versus Voluntary Tax Compliance: The ‘‘Slippery Slope’’ Framework. Journal of Economic Psychology, 29, 210-225.

http://dx.doi.org/10.1016/j.joep.2007.05.004 - 29. Hyun, J.K. (2005) Tax Compliances in Korea and Japan: Why Are They Different? Policy Research Institute, Ministry of Finance, Japan, 115.

- 30. Slemrod, J., Blumenthal, M. and Christian, C. (2001) Taxpayer Response to an Increased Probability of Audit: Evidence from a Controlled Experiment in Minnesota. Journal of Public Economics, 79, 455-483.

http://dx.doi.org/10.1016/s0047-2727(99)00107-3 - 31. Ameyaw, B., Addai, B., Ashalley, E. and Quaye, I. (2015) The Effects of Personal Income Tax Evasion on Socio-Economic Development in Ghana: A Case Study of the Informal Sector. British Journal of Economics, Management & Trade, 10, 1-14.

http://dx.doi.org/10.9734/BJEMT/2015/19267 - 32. Terkper, S. (2007) Improving Taxpayer Accounting for SMEs and Individuals. Andrew Young School of Policy Studies. Annual Conference on Public Finance Issues: Alternative Methods of Taxing Individuals, Georgia State University, Georgia State, 22-23.

- 33. Jackson, B. and Milliron, V. (1986) Tax Compliance Research: Findings, Problems and Prospects. Journal of Accounting Literature, 5, 125-165.

- 34. Ho, D., Ho, D.C. and Young, A. (2013) A Study of the Impact of Culture on Tax Compliance in China. International Tax Journal, 33-44.

- 35. Thorndike, J.J. (2009) The Unfair Advantage of the Few: The New Deal Origins of “Soak the Rich” Taxation. In: Martin, I.W., Mehrotra, A.K. and Prasad, M., Eds., The New Fiscal Sociology: Taxation in Comparative and Historical Perspectives, Cambridge University Press, Cambridge, 29-47.

http://dx.doi.org/10.1017/cbo9780511627071.003 - 36. Alm, J., McClelland, G.H. and Schulze, W.D. (1992) Why Do People Pay Taxes? Journal of Public Economics, 48, 21-38.

http://dx.doi.org/10.1016/0047-2727(92)90040-M - 37. Manaf, N.A. (2004) Land Tax Administration and Compliance Attitude in Malaysia. Unpublished Doctoral Thesis, University of Nottingham, Nottingham, UK.

- 38. Gilligan, G. and Richardson, G. (2005) Perceptions of Tax Fairness and Tax Compliance in Australia and Hong Kong: A Preliminary Study. Journal of Financial Crime, 12, 331-343.

http://dx.doi.org/10.1108/13590790510624783 - 39. Chan, C.W., Troutman, C.S. and O’Bryan, D. (2000) An Expanded Model of Taxpayer Compliance: Empirical Evidence from USA and Hong Kong. Journal of International Accounting, Auditing and Taxation, 9, 83-103.

http://dx.doi.org/10.1016/S1061-9518(00)00027-6 - 40. Sitkin, S.B. and Pablo, A.L. (1992) Reconceptualizing the Determinants of Risk Behavior. The Academy of Management Review, 17, 9-38.

- 41. Alm, J. and Torgler, B. (2006) Culture Differences and Tax Morale in United States and Europe. Journal of Economic Psychology, 27, 224-246.

http://dx.doi.org/10.1016/j.joep.2005.09.002 - 42. Torgler, B. (2003) Tax Morale: Theory and Analysis of Tax Compliance. Unpublished Doctoral Dissertation, University of Zurich, Zurich, Switzerland.

- 43. Torgler, B. (2007) Tax Compliance and Tax Morale. Edward Elgar Publishing Ltd., Cheltenham.

- 44. Aronson, E., Wilson, T.D. and Akert, R.M. (2010) Social Psychology. 7th Edition, Pearson Prentice Hall, Upper Saddle River.

- 45. Wenzel, M. (2003) Tax Compliance and the Psychology of Justice: Mapping the Field. In: Braithwaite, V., Ed., Taxing Democracy: Understanding Tax Avoidance and Evasion, Ashgate Publishing, Aldershot.

- 46. Bobek, D.D., Roberts, R.W. and Sweeney, J.T. (2007) The Social Norms of Tax Compliance: Evidence from Australia, Singapore, and the United States. Journal of Business Ethics, 74, 49-64.

http://dx.doi.org/10.1007/s10551-006-9219-x - 47. Bobek, D.D. and Hatfield, R.C. (2003) An Investigation of the Theory of Planned Behavior and the Role of Moral Obligation in Tax Compliance. Behavioral Research in Accounting, 15, 13-38.

http://dx.doi.org/10.2308/bria.2003.15.1.13 - 48. Ajzen, I. (1991) The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes, 50, 179-211.

http://dx.doi.org/10.1016/0749-5978(91)90020-T - 49. Basri, Y.M., Surya, R.A.S., Fitriasari, R., Novriyan, R. and Tania, T.S. (2012) Studi Ketidakpatuhan Pajak: Faktor Yang Mempengaruhinya (Kasus pada Wajib pajak Orang Pribadi yang terdaftar di KPP Pratama Tampan Pekanbaru). Paper presented at the Simposium Nasional Akuntansi 15, Universitas Lambung Mangkurat Banjarmasin.

- 50. Cullis, J., Jones, P. and dan Savoia, A. (2012) Social Norms and Tax Compliance: Framing the Decision to Pay Tax. The Journal of Socio-Economics, 41, 159-168.

http://dx.doi.org/10.1016/j.socec.2011.12.003 - 51. Hai, O.T. and dan See, L.M. (2011) Behavioral Intention of Tax Non-Compliance among Sole-Proprietors in Malaysia. International Journal of Business and Social Science, 2, 142-152.

- 52. Mustikasari, E. (2007) Kajian Empiris Tentang Kepatuhan Wajib Pajak Badan di Perusahaan Industri Pengolahan di Surabaya. Simposium Nasional Akuntansi X Makasar.

- 53. Trafimow, D., Sheeran, P., Conner, M. and Finlay, K. (2002) Evidence That Perceived Behavioural Control Is a Multidimensional Construct: Perceived Control and Perceived Difficulty. British Journal of Social Psychology, 41, 101-121.

http://dx.doi.org/10.1348/014466602165081 - 54. Park, H. and Blenkinsopp, J. (2009) Whistleblowing as Planned Behavior—A Survey of South Korean Police Officers. Journal of Business Ethics, 85: 545-556.

http://dx.doi.org/10.1007/s10551-008-9788-y - 55. Kidwell, B. and Jewell, R. (2003) An Examination of Perceived Behavioral Control: Internal and External Influences on Intention. Psychology and Marketing, 20, 625-642.

http://dx.doi.org/10.1002/mar.10089 - 56. Salman, K.R. and Sarjono, B. (2013) Intention and Behavior of Tax Payment Compliance by the Individual Tax Payers Listed in Pratama Tax Office West Sidoarjo Regency. Journal of Economics, Business, and Accountancy, 16, 309-324.

http://dx.doi.org/10.14414/jebav.v16i2.188 - 57. Langham, J.A., Paulsen, N. and Hartel, C.E.J. (2012) Improving Tax Compliance Strategies: Can the Theory of Planned Behavior Predict Business Compliance? eJournal of Tax Research, 10, 364-402.

- 58. Pope, J. and Mohdali, R. (2010) The Role of Religiosity in Tax Morale and Tax Compliance. Australian Tax Forum, 25, 565-596.

- 59. Aini, A.O., Budiman, J. and Wijayanti, P. (2013) Kepatuhan Wajib Pajak Badan Perusahaan Manufaktur di Semarang Dalam Perspektif Tax Professional. Paper Presented at the Proceeding Simposium Nasional Perpajakan 4, Universitas Trunojoyo, Madura.

- 60. Anyanwu, J.C. (1997) Nigerian Public Finance. Joanne Educational Publishers, Onitsha.

- 61. Engen, E. and Skinner, J. (1996) Taxation and Economic Growth. National Tax Journal, 49, 617-642.

http://dx.doi.org/10.3386/w5826 - 62. Tosun, M.S. and Abizadeh, S. (2005) Economic Growth and Tax Components: An Analysis of Tax Changes in OECD. Applied Economics, 37, 2251-2263.

http://dx.doi.org/10.1080/00036840500293813 - 63. Arnold, J.M., Brys, B., Heady, C., Johanson, A., Schwellnus, C. and Vartia, L. (2011) Tax Policy for Economic Recovery and Growth. The Economic Journal, 121, F59-F80.

http://dx.doi.org/10.1111/j.1468-0297.2010.02415.x - 64. Bhartia, H.L. (2009) Public Finance. 13th Edition, Vikas Publishing House PVT Ltd., New Delhi.

- 65. Jhingan, M.L. (2004) Money, Banking, International Trade and Public Finance. 7th Edition, Vrinda Publication (P) Ltd., New Delhi.

- 66. Razak, A.A. and dan Adafula, C.J. (2013) Evaluating Taxpayers’ Attitude and Its Influence on Tax Compliance Decisions in Tamale, Ghana. Journal of Accounting and Taxation, 5, 48-57.

http://dx.doi.org/10.5897/JAT2013.0120 - 67. Kogler, C., Batrancea, L., Nichita, A., Pantya, J., Belianin, A. and dan Kirchler, E. (2013) Trust and Power as Determinants of Tax Compliance: Testing the Assumptions of the Slippery Slope Framework in Austria, Hungary, Romania and Russia. Journal of Economic Psychology, 34, 169-180.

http://dx.doi.org/10.1016/j.joep.2012.09.010