Journal of Financial Risk Management

Vol.04 No.03(2015), Article ID:60111,22 pages

10.4236/jfrm.2015.43018

Granular and Star-Shaped Price Systems

Erio Castagnoli1, Marzia De Donno2, Gino Favero2, Paola Modesti2*

1Accademia Nazionale Virgiliana and Università Bocconi, Mantova and Milan, Italy

2Università degli Studi di Parma Dipartimento di Economia, Parma, Italy

Email: *paola.modesti@unipr.it

Copyright © 2015 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 17 July 2015; accepted 27 September 2015; published 30 September 2015

ABSTRACT

Linear price systems, typically used to model “perfect” markets, are widely known not to accommodate most of the typical frictions featured in “actual” ones. Since some years, “proportional” frictions (taxes, bid-ask spreads, and so on) are modeled by means of sublinear price functionals, which proved to give a more “realistic” description. In this paper, we want to introduce two more classes of functionals, not yet widely used in Mathematical Finance, which provide a further improvement and an even closer adherence to actual markets, namely the class of granular functionals, obtained when the unit prices of traded assets are increasing w.r.t. the traded amount; and the class of star-shaped functionals, obtained when the average unit prices of traded assets are increasing w.r.t. the traded amount. A characterisation of such functionals, together with their relationships with arbitrages and other (more significant) market inefficiencies, is explored.

Keywords:

Arbitrage, Asset Pricing, Super-Hedging, Granularity, Star-Shaped Prices

1. Introduction

One of the first and biggest concerns of Mathematical Finance is to study the prices of a suitable set of risky financial assets of any type, including stocks, indexed bonds, variable rate deposits, derivative securities, and so on. Usually, financial assets are modeled as random variables on some state sets, which are supposed to be the same for every asset in the considered market.

In earlier models, such as the one leading to the celebrated Black, Scholes, and Merton formula for option pricing ( Black & Scholes, 1973 ; Merton, 1973 ), the market is supposed to be a perfect one; in particular, no frictions are featured and no bid-ask spreads or commissions affect prices. Consequently, as it is clearly shown, for instance, in Dothan (1990) , Pliska (1997) , and Björk (1999) , asset prices turn out to be linear with respect to assets themselves, in the sense that the price of the sum of two positions exactly equals the sum of the two separated prices. In such a setting, a central result is found, called the Fundamental Theorem of Asset Pricing, of which dozens of variants are featured in the literature (besides the cited books see, for instance, Delbaen & Schachermayer, 1994 , for quite a general version), which essentially is a representation theorem: roughly speaking, the market prices do not allow for arbitrages (i.e., free gains without risks) if and only if there exist a probability measure called the risk neutral probability―and a discount factor such that prices themselves are (discounted) expected values of the future asset values.

The perfect market model, however, quickly proves to be unfit to provide a good description of realistic markets. For instance, it may be impossible to obtain the exact replication of a given pay-off, and therefore no linear price can be given for it. In such a case, as investigated by Davis & Clark (1994) , the investor may naturally aim at super-hedging it, i.e., at getting at least as much as needed (possibly more) at the minimum possible price. There are also cases when, due to market frictions, a dynamical strategy that exactly replicates the given pay-off may turn out to be more expensive than a super-hedging one: see, e.g., Hodges & Neuberger (1989) . El Karoui & Quenez (1995), Jouini & Kallal (1995), Jouini (1997), and Cvitanić et al. (1999) among others, had investigated such a setting and found a representation theorem: in any case, super-hedging prices turn out to be the maximum of a family of linear prices, which, for instance, Cvitanić et al. (1999) interpreted as prices in “shadow markets”. Moreover, Pham (2000) studied the properties of super-hedging price functionals to find them sublinear: additivity was replaced by subadditivity, meaning that the price of the sum of two positions might be cheaper than the sum of the two separated prices. Since sublinearity entails positive homogeneity besides subadditivity, it turns out to be perfectly fit to describe markets affected by proportional transaction costs (such as taxes or percentage commissions): see, e.g., Pham, Touzi, & Touzi (1999) . Furthermore, sublinearity turned out to be interesting for risk management purposes as well, being the foundational point for the celebrated paper by Artzner et al. (1999) on coherent risk measures.

A class of risk measures more general than the sublinear (i.e., coherent) ones of Artzner et al. (1999) is proposed by Föllmer & Schied (2002) , who replace sublinearity with the weaker convexity1. Inspired by their work, we started wondering whether convex price functions may sensibly be adapted to financial markets: we realized that this was naturally the case, for instance, if unit asset prices are supposed to increase with respect to the traded amount. A representation result can be found, stating that convex price functionals are the upper envelope of a family of affine prices, which admit an interpretation similar to the “shadow markets” of Cvitanić et al. (1999) .

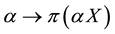

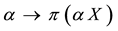

Another, further generalisation, may require average unit asset prices to be increasing, instead of “marginal” ones. This may be the case, for instance, when an agent can choose to buy an asset on several different markets, featuring different increasing unit prices: of course, the purchase will be conducted in such a way that the overall price (or, which is the same, the average unit price) is as low as possible. This leads to a totally new class of price functions, which we name star-shaped because their epigraph turns out to be a star-shaped set with respect to the origin, in the sense of Stewart & Tall (1983) . A representation result can be given for this class of functionals as well, with an interesting economical interpretation.

In the remaining part of this section, the notation used throughout the entire paper is stated, and the current state of the literature about linear and sublinear prices is briefly summarized. Although in different notation, everything exposed here can be found, for instance, in Dothan (1990) , Pliska (1997) , and Björk (1999) for the linear setting, and in Jouini & Kallal (1995) and Koehl & Pham (2000) for the sublinear case. Some examples, in a simple discrete setting, are also given, in order to allow the reader for familiarising with the phenomena under study. Remarkably, we emphasise that, as soon as the price functional is no longer linear, market efficiency is no longer guaranteed by absence of arbitrages only, and that another class of inefficiencies, namely the convenient super-hedgings (roughly speaking, the opportunity to get a better pay-off at a lower price), have to be taken into account.

Section 2 is dedicated to introducing and examining the convex case. After observing that convex functions naturally pop out when pricing by super-hedging by means of assets whose unit price is increasing, we give a generalisation of the Fundamental Theorem of Asset Pricing, and give an interpretation of the representation in terms of market efficiency. It turns out that the market is fully efficient, i.e., that no convenient super-hedging is possible, if all of the “shadow markets” are efficient, whereas absence of arbitrage is guaranteed by a local, less restrictive property.

Star-shaped prices are analysed in Section 3. We show that such functionals are the result of pricing by super- hedging by means of assets whose average price is increasing, and show that such a requirement is actually a proper generalisation of the previous, convex case. We also introduce a new pricing technique, which we may call “super-hedging by chunks” and that mathematically corresponds to the inf-convolution of the price functionals of the “shadow markets”. We show that convexity and star-shape are in some sense “stable” under super-hedging, either in the classical sense or in the “by chunks” one, and analyse the representation of star-shaped functionals in terms of market efficiency.

Finally, Section 4 is dedicated to summarising and comparing the main properties and the efficiency conditions of the four analysed market types and Section 5 features some concluding remarks.

1.1. Notation

A state space

is supposed to be given, and the market

is supposed to be given, and the market

is a set of (real valued) random variables2

is a set of (real valued) random variables2 : every

: every

is identified with an asset, in the sense that the (random) value attained by X corresponds to the pay-off (or the market value) of the considered asset at a suitable maturity. We are supposing that the uncertainty is resolved in a single time period: in other words, the models we encompass are of a static, not dynamic, type. We write

is identified with an asset, in the sense that the (random) value attained by X corresponds to the pay-off (or the market value) of the considered asset at a suitable maturity. We are supposing that the uncertainty is resolved in a single time period: in other words, the models we encompass are of a static, not dynamic, type. We write

(respectively,

(respectively, ) to intend that

) to intend that

(respectively,

(respectively, ) for every

) for every , where

, where

indicates the usual weak inequality between real numbers.

indicates the usual weak inequality between real numbers.

We shall suppose one of the classical “perfect market hypotheses” to hold, requiring every asset

to be infinitely available (there is no “maximum tradable amount”) and divisible (it is possible to buy any fraction of it); furthermore, short sales are allowed. This translates into the fact that, for every

to be infinitely available (there is no “maximum tradable amount”) and divisible (it is possible to buy any fraction of it); furthermore, short sales are allowed. This translates into the fact that, for every

and every

and every , the investor can hold the position

, the investor can hold the position

(where

(where

indicates short sale of

indicates short sale of

units of X). Of course, several assets

units of X). Of course, several assets

can be simultaneously traded, by buying

can be simultaneously traded, by buying

units of each (with

units of each (with

indicating short sale); this corresponds to holding a portfolio of those n assets, whose “final” pay-off plainly turns out to be

indicating short sale); this corresponds to holding a portfolio of those n assets, whose “final” pay-off plainly turns out to be . Mathematically speaking, this corresponds to

. Mathematically speaking, this corresponds to

being a linear space.

being a linear space.

Giving a price to every traded asset

simply amounts to defining a (price) functional

simply amounts to defining a (price) functional . The functional

. The functional

is said to allow for:

is said to allow for:

• An arbitrage (see, e.g.,

Björk, 1999

and

Pliska, 1997

) if there exist a

in

in

such that

such that

(which means that it is possible to obtain an immediate gain, corresponding to the negative price, without any risk, i.e., with the certainty not to lose any money at the maturity);

(which means that it is possible to obtain an immediate gain, corresponding to the negative price, without any risk, i.e., with the certainty not to lose any money at the maturity);

• A convenient super-hedging (quite a recent concept: see, e.g.,

Castagnoli et al., 2009

and

Castagnoli et al., 2011

, but also, for instance,

Hodges & Neuberger (1989)

, who observe the phenomenon although without specifically titling it) if there exist

such that

such that

and

and

(which means that it is possible to obtain a “higher” pay-off at a “lower” price).

(which means that it is possible to obtain a “higher” pay-off at a “lower” price).

Of course, the basic laws of supply and demand imply that neither of the above opportunities, which we shall jointly refer to as inefficiencies, should hold in a market: in both cases, the demand pressure on X would quickly lead its price

to increase until becoming either positive (in the first case) or greater than

to increase until becoming either positive (in the first case) or greater than

(in the second case; furthermore, lack of demand on Y would lead its price

(in the second case; furthermore, lack of demand on Y would lead its price

to decrease as well). Note that:

to decrease as well). Note that:

•

does not allow for arbitrages if and only if

does not allow for arbitrages if and only if

whenever

whenever , that is, if

, that is, if

is (or may be called) positive;

is (or may be called) positive;

•

does not allow for convenient super-hedgings if and only if

does not allow for convenient super-hedgings if and only if

whenever

whenever , that is, if

, that is, if

is (or may be called) increasing.

is (or may be called) increasing.

Generally speaking, absence of arbitrages has the nature of a local property, because it only involves the behaviour of the price functional

with respect to the null pay-off, whereas absence of convenient super-hedgings is a global property, because it is required to hold for every pair

with respect to the null pay-off, whereas absence of convenient super-hedgings is a global property, because it is required to hold for every pair .

.

It is noteworthy as well that there are no general links between positivity and monotonicity. Take for instance, : the functional

: the functional

is (of course) positive but not increasing (because, taken a

is (of course) positive but not increasing (because, taken a

in

in , it is

, it is

and

and ), whereas, taken a

), whereas, taken a

in

in , the functional

, the functional

is increasing but

is increasing but

not positive (because , although

, although ).

).

Note also that, for every , the price functional

, the price functional

induces a function

induces a function

defined by

defined by , which in a natural way can be called the supply and demand function for X.

, which in a natural way can be called the supply and demand function for X.

Remark 1. We purposefully decided to avoid measurability issues: in particular, we never mentioned the ( -)algebra

-)algebra

on

on

where the probability P is properly defined (and with respect to which all the

where the probability P is properly defined (and with respect to which all the

have to be measurable). This is only possible because of our choice of dealing with single period models: in order to introduce a dependence from time, actually, it is unavoidable to follow the well-known approach of defining a filtration

have to be measurable). This is only possible because of our choice of dealing with single period models: in order to introduce a dependence from time, actually, it is unavoidable to follow the well-known approach of defining a filtration

of (

of ( -)algebrae contained in

-)algebrae contained in

and to suppose that, at every time

and to suppose that, at every time , the value (price) of a random variable

, the value (price) of a random variable

is given by its conditional expected value

is given by its conditional expected value , possibly discounted in a suitable way.

, possibly discounted in a suitable way.

In the same way, the price functional

should be taken to be measurable with respect to the (

should be taken to be measurable with respect to the ( -)algebra

-)algebra

(and the Borel

(and the Borel

-algebra

-algebra

on

on ). As a matter of fact, the most general setting for this situation is to take an arbitrary (real) linear space

). As a matter of fact, the most general setting for this situation is to take an arbitrary (real) linear space

and to consider as possible price functionals all of the elements of a subspace

and to consider as possible price functionals all of the elements of a subspace

of the algebraic dual of

of the algebraic dual of . Moreover, by considering on

. Moreover, by considering on

the weak topology (i.e., the minimal one that makes continuous all of the

the weak topology (i.e., the minimal one that makes continuous all of the ),

),

turns out to be the topological dual of

turns out to be the topological dual of , so that our setting can be included in the topological duality among linear spaces, a typical topic in Functional Analysis. Some more details can be found in

Castagnoli et al. (in print)

and references therein.

, so that our setting can be included in the topological duality among linear spaces, a typical topic in Functional Analysis. Some more details can be found in

Castagnoli et al. (in print)

and references therein.

Remark 2. The arbitrage and convenient super-hedging opportunities defined above are often called strong in the literature, and their weak counterparts are defined as follows. Write

to indicate that

to indicate that

and

and

(that is, there exists at least an

(that is, there exists at least an

such that

such that ). In such a case, the functional

). In such a case, the functional

is said to allow for:

is said to allow for:

• A weak arbitrage (or an arbitrage of the second kind) if there exists a

in

in

such that

such that

(the case

(the case

is allowed, possibly cancelling the immediate gain, but in some states a gain at the maturity will be obtained);

is allowed, possibly cancelling the immediate gain, but in some states a gain at the maturity will be obtained);

• A weak convenient super-hedging (or a convenient super-hedging of the second kind) if there exist

such that

such that

and

and

(the prices may coincide, but in some states X will pay off strictly better than

(the prices may coincide, but in some states X will pay off strictly better than ).

).

It is straightforward that:

•

does not allow for weak arbitrages if and only if

does not allow for weak arbitrages if and only if

whenever

whenever : that is, if and only if

: that is, if and only if

is strictly positive;

is strictly positive;

•

does not allow for weak convenient super-hedgings if and only if

does not allow for weak convenient super-hedgings if and only if

whenever

whenever : that is, if and only if

: that is, if and only if

is strictly increasing.

is strictly increasing.

As a matter of fact, when the assets

are not discrete random variables, the above definitions turn out to be impossible to deal with (they would imply, for instance, that for every

are not discrete random variables, the above definitions turn out to be impossible to deal with (they would imply, for instance, that for every

the “Dirac function”

the “Dirac function”

gets a positive price

gets a positive price , which is plainly meaningless). It is then customary to take into consideration an a-priori probability P on

, which is plainly meaningless). It is then customary to take into consideration an a-priori probability P on , and to define

, and to define

when

when

and

and . In such a case, all of the “inequalities” between random variables are of course to be intended in the “P-almost everywhere” sense.

. In such a case, all of the “inequalities” between random variables are of course to be intended in the “P-almost everywhere” sense.

We decided not to take into consideration the weak arbitrages, both for the sake of simplicity and because we want to emphasize that there is no actual need for the a priori probability P to be given. It is nevertheless proper to cite this cases, both for compatibility with the existing literature and to remark that asking for weaker and weaker inefficiencies to be removed from the market translates into stronger and stronger regularity properties for the price functional .

.

It is also noteworthy that, in order to define weak inefficiencies and to intend the inequalities “almost everywhere”, instead of an a priori probability P, any a priori measure

equivalent to P could be considered on

equivalent to P could be considered on : it would actually be exactly the same to define

: it would actually be exactly the same to define

whenever

whenever

and

and , i.e., when the set where

, i.e., when the set where

has a positive measure instead of a positive probability. Briefly said, the normalisation property of the a priori measure is completely unnecessary.

has a positive measure instead of a positive probability. Briefly said, the normalisation property of the a priori measure is completely unnecessary.

1.2. Perfect Markets: The Linear Case

Besides the infinite availability and divisibility hypotheses cited above, the classical models based on “perfect markets” (see the already cited Björk, 1999 , Pliska, 1997 , and Dothan, 1990 ) ask for three more requirements. First of all, all market agents are fully rational and they aim at maximising their profit; furthermore, all agents are equally informed, without “informational asymmetries”. Secondly, the agents are price takers: they have no possibility to negotiate the prices they see on the markets. Finally, in the market there are no taxes, no bid-ask spreads, no commissions: in a word, there are no frictions.

All of these hypotheses together could be simply summarised in a single property: a market is called perfect if the price functional

is linear. Recall that the linearity of

is linear. Recall that the linearity of

means that

means that

for every

for every

and every

and every ; equivalently,

; equivalently,

is additive (

is additive ( for every

for every ) and homogeneous (

) and homogeneous ( for every

for every

and every

and every ). Note that this translates into the fact that the unit price for every asset

). Note that this translates into the fact that the unit price for every asset

does not depend on the traded amount: buying (or short selling) a units of X exactly costs (or yields)

does not depend on the traded amount: buying (or short selling) a units of X exactly costs (or yields)

times the unit price of X. In other words, the supply and demand function

times the unit price of X. In other words, the supply and demand function

is a linear function for every

is a linear function for every : for every

: for every ,

, .

.

Every linear functional on a linear space attains null value at the “origin” (i.e., at the null vector): as an immediate consequence, an increasing linear functional turns out to be positive as well. Shortly said, for linear functionals, (increasing) monotonicity implies positivity. In the case of linear functionals, moreover, the converse is also true:

is equivalent to

is equivalent to , and the fact that

, and the fact that

immediately yields that a positive linear functional is increasing as well. In other words, positivity and monotonicity are equivalent in the linear setting: therefore, in the classical literature about perfect markets, convenient super-hedgings have never been specifically recognised as market inefficiencies, because a price functional allows for convenient super-hedgings if and only if it allows for arbitrages.

immediately yields that a positive linear functional is increasing as well. In other words, positivity and monotonicity are equivalent in the linear setting: therefore, in the classical literature about perfect markets, convenient super-hedgings have never been specifically recognised as market inefficiencies, because a price functional allows for convenient super-hedgings if and only if it allows for arbitrages.

A classical duality result states that, given a linear space

of real valued functions defined on the same set

of real valued functions defined on the same set , a functional

, a functional

is linear if and only if there exist a (signed) measure

is linear if and only if there exist a (signed) measure

on

on

such that

such that

(Lebesgue integrals). Usually, it is said that

can be represented as the Lebesgue integral with respect to a suitable measure

can be represented as the Lebesgue integral with respect to a suitable measure

defined on

defined on ; we remark that the measure

; we remark that the measure

may be “signed”, i.e., that it may attain negative values. The Fundamental Theorem of Asset Pricing, translated into our setting, states that the price functional

may be “signed”, i.e., that it may attain negative values. The Fundamental Theorem of Asset Pricing, translated into our setting, states that the price functional

allows for no arbitrages if and only if it is represented by a “proper” positive measure

allows for no arbitrages if and only if it is represented by a “proper” positive measure .

.

If the “constant” (degenerate) random variables

belong to

belong to

(or, equivalently, if the monetary unit

(or, equivalently, if the monetary unit

belongs to

belongs to ), then the price of

), then the price of

amounts to

amounts to : in other words, the “norma-

: in other words, the “norma-

lisation factor”

has the financial meaning of the discount factor for the considered time period. Note also that the measure

has the financial meaning of the discount factor for the considered time period. Note also that the measure

turns out to be a probability on

turns out to be a probability on : this way, the above representation of the price functional becomes

: this way, the above representation of the price functional becomes

(1)

(1)

which is classically told by stating that, if no arbitrages are allowed, the current prices of financial assets are the discounted expected values of their final random pay-off. In such a case,

is called a risk-neutral probability (or, in the dynamical case, a martingale measure).

is called a risk-neutral probability (or, in the dynamical case, a martingale measure).

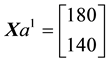

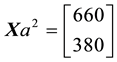

Example 1. Take into consideration the state space : since

: since

is finite, every random variable

is finite, every random variable

can be identified with the vector

can be identified with the vector : therefore, we shall simply write

: therefore, we shall simply write . Suppose that two assets are exchanged on the market:

. Suppose that two assets are exchanged on the market: , at price 4, and

, at price 4, and , at price 5.

, at price 5.

The decision to hold a portfolio obtained by buying (or short selling)

units of

units of

and

and

units of

units of

can be identified with the vector

can be identified with the vector : it leads to the pay-off

: it leads to the pay-off

and costs

and costs . Note that every pay-off

. Note that every pay-off

can be obtained by means of a suitable (and unique) portfolio: in other

can be obtained by means of a suitable (and unique) portfolio: in other

words,

, where it is intended that the price of every

, where it is intended that the price of every

is defined as the price of the portfolio a yielding the pay-off X.

is defined as the price of the portfolio a yielding the pay-off X.

We can simplify the notation by defining the pay-off matrix : this way, the portfolio

: this way, the portfolio

simply leads to the pay-off

simply leads to the pay-off

(usual matrix product). If we further define the price vector

(usual matrix product). If we further define the price vector , it is clear that the price of the portfolio a is

, it is clear that the price of the portfolio a is .

.

Note that every linear functional

simply amounts to the vector (“inner”) product by a vector

simply amounts to the vector (“inner”) product by a vector , with

, with

and

and : indeed,

: indeed, .

.

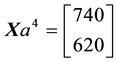

Let us now represent the price functional . As we already mentioned, for every

. As we already mentioned, for every

it has to be

it has to be , with a such that

, with a such that . Suppose now that

. Suppose now that

is a vector such that

is a vector such that :3 it is immediate

:3 it is immediate

that , and therefore that

, and therefore that

represents

represents . Since the linear system

. Since the linear system

has

has

the unique solution , such a vector turns out to be the representation of the linear price functional

, such a vector turns out to be the representation of the linear price functional

induced by the market prices.

induced by the market prices.

It is immediate to realise that, since both components of

are positive, the functional

are positive, the functional

is (positive, and therefore) monotonically increasing. This shows that no arbitrages are allowed in the market. Note also that the

is (positive, and therefore) monotonically increasing. This shows that no arbitrages are allowed in the market. Note also that the

discount factor is , and that the vector

, and that the vector

corresponds to a probability Q on

corresponds to a probability Q on , assigning

, assigning ,

, . Furthermore, for every

. Furthermore, for every ,

, .

.

Just for the sake of completeness, suppose that the price of

be 8 instead of 4. In this case, the unique so-

be 8 instead of 4. In this case, the unique so-

lution of the system

would be

would be

the presence of a non-positive component implies that

the presence of a non-positive component implies that

is not positive and that indicates the possibility of arbitrages. Indeed, the pay-off

is not positive and that indicates the possibility of arbitrages. Indeed, the pay-off

is obtained with the portfolio

is obtained with the portfolio

at the price

at the price .

.

1.3. Proportional Frictions: The Sublinear Case

A natural generalisation of the linear model is to suppose that some frictions affect the market, in order to accommodate, for instance, taxes or commissions. By supposing such frictions to be proportional to the traded amount, it is possible to maintain “half” of the homogeneity property of the price functional: namely,

turns out to be positively homogeneous, meaning that

turns out to be positively homogeneous, meaning that

for every

for every

and every

and every

(no longer for every

(no longer for every ).

).

It is clear that such a price functional can no longer be expected to be additive: for instance, an agent buying both

and

and

will pay the taxes and commissions on both of them, and thus will end up paying a positive price for the null pay-off: in symbols,

will pay the taxes and commissions on both of them, and thus will end up paying a positive price for the null pay-off: in symbols, . Nevertheless, since the agents are still supposed to be rational, it is reasonable to suppose that

. Nevertheless, since the agents are still supposed to be rational, it is reasonable to suppose that

is subadditive, i.e., that

is subadditive, i.e., that

(if the price of a joint position were greater than the sum of the two composing ones, every rational agent would separately buy the two components).

(if the price of a joint position were greater than the sum of the two composing ones, every rational agent would separately buy the two components).

If , generally speaking, the bid price induced by a pricing functional is

, generally speaking, the bid price induced by a pricing functional is . If

. If

is (sublinear, and therefore) subadditive, recalling that

is (sublinear, and therefore) subadditive, recalling that , we get

, we get , where we write

, where we write

to underline that those expressed by

to underline that those expressed by

actually are ask prices. Roughly speaking, then, sublinear functionals model the case when the ask and the bid price may differ (due to taxes, commissions, or general bid-ask spreads), yet the unit price does not depend on the traded amount. The supply and demand function induced by a sublinear

actually are ask prices. Roughly speaking, then, sublinear functionals model the case when the ask and the bid price may differ (due to taxes, commissions, or general bid-ask spreads), yet the unit price does not depend on the traded amount. The supply and demand function induced by a sublinear

for a given

for a given

takes the form

takes the form

.

.

Every sublinear functional attains null value at the origin: therefore, every increasing sublinear functional is positive as well. The converse is not true, as already mentioned: the norm functional is positive, but not increasing. As a consequence, there may be sublinear price functionals that allow for convenient super-hedgings although not allowing for arbitrages. It is noteworthy, nevertheless, that

turns out to be increasing every time that it is “negative”, i.e., when

turns out to be increasing every time that it is “negative”, i.e., when

for every

for every : in such a case, indeed, whenever

: in such a case, indeed, whenever

we get

we get . Recalling that the bid price of the pay-off X is naturally defined as

. Recalling that the bid price of the pay-off X is naturally defined as , the “negativity” condition translates into

, the “negativity” condition translates into

for every

for every : in other words, absence of arbitrages is guaranteed by the positivity of ask prices of the positive pay-offs, whereas absence of convenient super-hedgings is ensured by the positivity of bid prices of the same positive pay-offs.

: in other words, absence of arbitrages is guaranteed by the positivity of ask prices of the positive pay-offs, whereas absence of convenient super-hedgings is ensured by the positivity of bid prices of the same positive pay-offs.

As an immediate consequence of the classical Hahn-Banach Theorem, a sublinear functional

can be represented as the pointwise maximum of the linear functionals that it “dominates”. In greater detail: if

can be represented as the pointwise maximum of the linear functionals that it “dominates”. In greater detail: if

is a sublinear functional, then the set

is a sublinear functional, then the set

is not empty and

is not empty and . Moreover, if

. Moreover, if

is not allowed to take infinite values, L turns out to be convex and compact, so that the “sup “can be replaced by a “max”. It is possible to show (see

Pliska, 1997

and

Castagnoli et al., 2009

) that:

is not allowed to take infinite values, L turns out to be convex and compact, so that the “sup “can be replaced by a “max”. It is possible to show (see

Pliska, 1997

and

Castagnoli et al., 2009

) that:

•

is positive if and only if there exists (at least) a positive

is positive if and only if there exists (at least) a positive ;

;

•

is increasing if and only if every

is increasing if and only if every

is positive.

is positive.

From a mathematical point of view, L is the subdifferential of

at 0 (see, e.g.,

Rockafellar, 1970

).

at 0 (see, e.g.,

Rockafellar, 1970

).

According to such a characterisation, if

does not allow for convenient super-hedgings (and, therefore, not even for arbitrages), every

does not allow for convenient super-hedgings (and, therefore, not even for arbitrages), every

can be represented as the expected value with respect to a suitable measure

can be represented as the expected value with respect to a suitable measure , discounted by a suitable factor

, discounted by a suitable factor :

:

In other words, an efficient sublinear functional acts “as if” a whole set L of “plausible” scenarios

are involved, each corresponding to (a linear price functional, i.e., to) a probability measure

are involved, each corresponding to (a linear price functional, i.e., to) a probability measure

and a discount factor

and a discount factor : the price assigned to every random variable amounts to the “worst case” discounted expected value, i.e., to the linear functional assigning the highest price to X. It is noteworthy to mention that such a representation was already conjectured by

de Finetti & Obry (1933)

.

: the price assigned to every random variable amounts to the “worst case” discounted expected value, i.e., to the linear functional assigning the highest price to X. It is noteworthy to mention that such a representation was already conjectured by

de Finetti & Obry (1933)

.

One final consideration is in order. A rational investor who aims at obtaining the pay-off

(which need not belong to

(which need not belong to ) is naturally led to look for the best (super)hedge of Z, i.e., to buy the cheapest traded asset

) is naturally led to look for the best (super)hedge of Z, i.e., to buy the cheapest traded asset

that dominates Z

(El Karoui & Quenez, 1995)

. This way, (a better pay-off than) Z can be obtained at the price

that dominates Z

(El Karoui & Quenez, 1995)

. This way, (a better pay-off than) Z can be obtained at the price

called the cheapest super-hedging price of Z. It is quite clear that, if

does not allow for convenient super-hedgings,

does not allow for convenient super-hedgings,

for every

for every ; on the other hand, it is immediate to realise that, if

; on the other hand, it is immediate to realise that, if

allows for convenient super-hedgings, then

allows for convenient super-hedgings, then . It is indeed possible to show that

. It is indeed possible to show that

is sublinear as soon as

is sublinear as soon as

is and that, if

is and that, if , then

, then

with

with .

.

Roughly speaking,

turns out to be the highest sublinear functional, among those dominated by

turns out to be the highest sublinear functional, among those dominated by , that does not allow for (arbitrages or) convenient super-hedgings.

, that does not allow for (arbitrages or) convenient super-hedgings.

Example 2. Consider the same two assets of Example 1, with pay-off matrix , but suppose now

, but suppose now

that two price vectors are given, namely that of the ask prices

and of the bid prices

and of the bid prices

(of course

(of course ). The price of every

). The price of every

is found as its cheapest super-hedging price:

is found as its cheapest super-hedging price:

(where

(where

and

and

denote the positive and negative part of

respectively). A standard linear programming duality argument4 allows to conclude that the price

respectively). A standard linear programming duality argument4 allows to conclude that the price

dominates the linear functional induced by the vector

dominates the linear functional induced by the vector

if and only if

if and only if , which amounts to finding all the js such that

, which amounts to finding all the js such that , with

, with .

.

The solutions of the given parametric linear system is the set : it is immediate to check that it is a convex and compact subset of

: it is immediate to check that it is a convex and compact subset of . Since L contains positive vectors only, we can conclude that

. Since L contains positive vectors only, we can conclude that

allows for no convenient super-hedgings (and, therefore, for no arbitrages).

allows for no convenient super-hedgings (and, therefore, for no arbitrages).

It is possible to build examples when the functional

induced by the listed assets allows for arbitrages and for convenient super-hedgings, or for convenient super-hedgings only. For the sake of brevity, we invite the interested reader to see

Castagnoli et al. (2009)

.5

induced by the listed assets allows for arbitrages and for convenient super-hedgings, or for convenient super-hedgings only. For the sake of brevity, we invite the interested reader to see

Castagnoli et al. (2009)

.5

2. Increasing Unit Prices

The Granular (Convex) Case

Although sublinear prices can indeed capture several features of prices in the “real world”, they still feature unit prices which do not depend on the traded amount. Who trades on actual markets, instead, knows well that unit prices tend to increase with respect to the amount bought, and to decrease with respect to the amount sold. Suppose, for instance, that we are set to buy 1000 units of some asset. Having a look at the offer prices, we see that someone is selling up to 100 units at 3?each, someone else up to 500 units at 3.1?each, someone else up to 600 units at 3.2?each, and so on. This way, we are facing increasing unit prices, and to buy all of the 1000 units we have to pay : it is immediate to realise that, generally speaking, total price needed to buy

: it is immediate to realise that, generally speaking, total price needed to buy

units of an asset turns out to be a(n increasing and) convex function of

units of an asset turns out to be a(n increasing and) convex function of

(and piecewise affine, in our example, but this is not necessary: the price is a convex function of the traded amount every time that the marginal price is increasing, which is the standard hypothesis of the classical law of supply and demand). We want to show that a natural way to model such a situation is to take into consideration a convex price functional

(and piecewise affine, in our example, but this is not necessary: the price is a convex function of the traded amount every time that the marginal price is increasing, which is the standard hypothesis of the classical law of supply and demand). We want to show that a natural way to model such a situation is to take into consideration a convex price functional

(which is of course a generalisation of the sublinear case, because every sublinear functional is convex as well): in order to do so, let us see how a convex price functional comes out in a very natural way.

(which is of course a generalisation of the sublinear case, because every sublinear functional is convex as well): in order to do so, let us see how a convex price functional comes out in a very natural way.

Suppose that, in an exchange list under consideration, the assets

are included, such that, for every

are included, such that, for every , the supply and demand function

, the supply and demand function

is increasing and convex. Of course, the set

is increasing and convex. Of course, the set

of all attainable pay-offs is the linear space spanned by the traded assets:

of all attainable pay-offs is the linear space spanned by the traded assets: . The only reasonable way of assigning a price to every

. The only reasonable way of assigning a price to every

is to use the super-hedging technique seen at the end of the previous section:

is to use the super-hedging technique seen at the end of the previous section:

It is immediate to show that such functional

is increasing5; since

is increasing5; since , the monotonicity of

, the monotonicity of

implies its positivity, which, from the financial point of view, means that the “cheapest super-hedging” price functional

implies its positivity, which, from the financial point of view, means that the “cheapest super-hedging” price functional

does not allow neither for arbitrages nor for convenient super-hedgings. It is also possible, although a little technical, to show that

does not allow neither for arbitrages nor for convenient super-hedgings. It is also possible, although a little technical, to show that

is convex, i.e., that

is convex, i.e., that

for every

for every

and every

and every

6: the convexity of the single supply and demand functions “propagates” to the entire pricing functional.

6: the convexity of the single supply and demand functions “propagates” to the entire pricing functional.

Fenchel’s Theorem ensures that a convex functional

can be represented as the pointwise maximum of the affine functionals that it dominates, where an affine functional is the translation of a linear functional:

can be represented as the pointwise maximum of the affine functionals that it dominates, where an affine functional is the translation of a linear functional:

is affine if there exist

is affine if there exist

linear and

linear and

such that

such that . In greater detail:

. In greater detail:

Proposition 1 (Fenchel’s Theorem). Let

be convex. Then the set

be convex. Then the set

is non-empty, closed and convex and such that

is non-empty, closed and convex and such that

for every

for every .

.

Since every

can be written as

can be written as

with

with

linear and

linear and , and since every linear functional can be represented as in (1), the convex functional

, and since every linear functional can be represented as in (1), the convex functional

can be represented as

can be represented as

(2)

(2)

Note that

implies that all of the constants

implies that all of the constants

are

are , and that at least one of them is null,

, and that at least one of them is null,

because .

.

Example 3. Take into consideration the same two assets of Examples 1 and 2, with pay-off matrix,

, and suppose that they are exchanged on the market as follows:

, and suppose that they are exchanged on the market as follows:

•

has unit price 4 for (short) sales or purchases up to 10 units, 4.2 for purchases up to 50 units and 4.4 beyond 50 units;

has unit price 4 for (short) sales or purchases up to 10 units, 4.2 for purchases up to 50 units and 4.4 beyond 50 units;

•

has unit price 5 up to 20 units, 5.5 up to 80 units and 6 beyond 80 units.

has unit price 5 up to 20 units, 5.5 up to 80 units and 6 beyond 80 units.

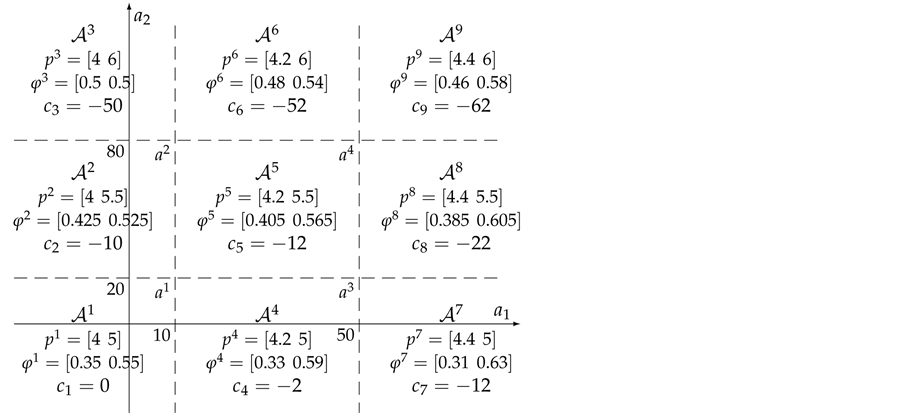

Such prices split the portfolio space into nine regions, identified by four vertices (see Figure 1).

Let , and consider the portfolio

, and consider the portfolio . Of course,

. Of course, ; therefore,

; therefore, .Since

.Since

is defined as the cheapest (super)hedge of W,

is defined as the cheapest (super)hedge of W, . On the other hand, the fact that all of the functions

. On the other hand, the fact that all of the functions

are convex w.r.t.

are convex w.r.t.

implies that

implies that . By transitivity,

. By transitivity,

, i.e. ,

, i.e. ,

is convex.Note that this implies that the inequalities (3) hold for every

is convex.Note that this implies that the inequalities (3) hold for every , not just for the listed assets.•

, not just for the listed assets.• , which yields the pay-off

, which yields the pay-off

and costs

and costs ;•

;• , which yields the pay-off

, which yields the pay-off

and costs

and costs

(recall thefirst 20 units of

(recall thefirst 20 units of

are bought at the cheaper price 5, and only the 60 subsequent units are bought at the higher price 5.5;•

are bought at the cheaper price 5, and only the 60 subsequent units are bought at the higher price 5.5;• , which yields the pay-off

, which yields the pay-off

and costs

and costs ;•

;• , which yields the pay-off

, which yields the pay-off

and costs

and costs .Inside each region, the unit prices

.Inside each region, the unit prices

remain constant (shown in Figure 1 as well), and therefore the price functional

remain constant (shown in Figure 1 as well), and therefore the price functional

is affine: we may write

is affine: we may write ,

, .In greater detail: there have to be nine vectors

.In greater detail: there have to be nine vectors

and nine (non positive) constants

and nine (non positive) constants

Figure 1. The portfolio space in Example 3.

such that, if

such that, if

with

with

, then

, then . Every vector

. Every vector

identifies a discount factor

identifies a discount factor

and a risk-neutral probability

and a risk-neutral probability , and therefore this model

, and therefore this model

identifies at least nine risk-neutral measures; however, as already pointed out, the risk-neutral measures turn out not to be as important as the properties of the price functional in order to investigate market efficiency.

Note that, if both X and

belong to the same region

belong to the same region , then

, then : it is then straightforward to realise that, for every

: it is then straightforward to realise that, for every , the vector

, the vector

is easily determined by solving the usual linear system

is easily determined by solving the usual linear system . The constants

. The constants ,

,

, are calculated as the amount “saved” by buying the “first” units at a price smaller than

, are calculated as the amount “saved” by buying the “first” units at a price smaller than :

:

• In , the effective prices are the lowest ones: therefore,

, the effective prices are the lowest ones: therefore,

(we could argue the same conclusion from the fact that

(we could argue the same conclusion from the fact that );

);

• In , the price of

, the price of

is 5.5, but the first 20 units are bought at the price

is 5.5, but the first 20 units are bought at the price , thus “saving”

, thus “saving”

: therefore,

: therefore,

(as a double check, consider for instance that the portfolio

(as a double check, consider for instance that the portfolio

yields the pay-off

yields the pay-off

and costs

and costs , and

, and

pre-

pre-

cisely yields );

);

• In , the price of

, the price of

is 6, but the first 20 units are bought at

is 6, but the first 20 units are bought at

less and the subsequent (

less and the subsequent ( ) 60 at

) 60 at

less, for a total “saving” of

less, for a total “saving” of : therefore,

: therefore,

(note that such a saving can also be calculated as the one achieved in the “previous” region

(note that such a saving can also be calculated as the one achieved in the “previous” region , i.e.,

, i.e.,

, plus the additional saving of 0.5 on all of the first 80 units:

, plus the additional saving of 0.5 on all of the first 80 units: );

);

• In , the price of

, the price of

is 4.2, but the first 10 units are bought at

is 4.2, but the first 10 units are bought at

less, thus “saving”

less, thus “saving” : therefore,

: therefore, ;

;

• In , both the first 10 units of

, both the first 10 units of

and the first 20 units of

and the first 20 units of

are bought at a lower price: the savings of

are bought at a lower price: the savings of

and

and

add up, and therefore

add up, and therefore ;

;

• In , the savings of

, the savings of

and

and

add up, and therefore

add up, and therefore ;

;

• In , the first 10 units of

, the first 10 units of

cost

cost

less than the “full” price, and the subsequent (

less than the “full” price, and the subsequent ( ) 40 cost

) 40 cost

less: the total saving is

less: the total saving is : therefore,

: therefore, ;

;

• In , the savings of

, the savings of

and

and

add up, and therefore

add up, and therefore ;

;

• Finally, .

.

Now, the price of every pay-off

can be calculated as

can be calculated as . For instance, for

. For instance, for

we get:

we get:

(the maximum price is emphasised). Note that, indeed, X is yielded by the portfolio , and the price of a is

, and the price of a is .

.

As already mentioned, the price functional

is convex. We want nevertheless to strike out that, generally

is convex. We want nevertheless to strike out that, generally

speaking, it is neither sub- nor superadditive: for instance, consider again the pay-off . It is possible to check that

. It is possible to check that

and

and , and therefore

, and therefore

. On the other hand, it is also

. On the other hand, it is also , and therefore

, and therefore . We want to point out that this second inequality

. We want to point out that this second inequality

does not correspond to a convenient super-hedging: indeed, it is not possible to buy simultaneously two portfo-

lios yielding the claim

because, when doubling the position, the unit prices of the traded assets increase.

because, when doubling the position, the unit prices of the traded assets increase.

It is still possible to show that, if

does not take infinite values, the set

does not take infinite values, the set

is compact and

is compact and

convex. Mathematically speaking, the set

is the union of the sub differentials of

is the union of the sub differentials of

at all points

at all points ; note that, if

; note that, if

is sublinear, then

is sublinear, then .

.

In perfect analogy to what happens for sublinear functionals,

is increasing if and only if every

is increasing if and only if every

is positive. The natural technique of pricing any pay-off Z (either belonging to

is positive. The natural technique of pricing any pay-off Z (either belonging to

or not) by super-hedging, as seen in Section 1.3, can still be applied, even in the case when

or not) by super-hedging, as seen in Section 1.3, can still be applied, even in the case when

allows for convenient super-hedgings, and it can be shown that the cheapest super-hedging price

allows for convenient super-hedgings, and it can be shown that the cheapest super-hedging price

is a convex functional if the “original”

is a convex functional if the “original”

is. Furthermore, the set

is. Furthermore, the set

corresponding to the set

corresponding to the set

identified by

identified by

turns out to be precisely the set

turns out to be precisely the set .

.

Example 4. On

consider the two assets:

consider the two assets:

• , at the unit price of 4.5, which increases at 4.7 for purchases of more than 10 units;

, at the unit price of 4.5, which increases at 4.7 for purchases of more than 10 units;

• , traded at 3.4 per unit, which increases at 3.7 for purchases of more than 20 units.

, traded at 3.4 per unit, which increases at 3.7 for purchases of more than 20 units.

This way, . The prices split the portfolio space into four regions

. The prices split the portfolio space into four regions , corresponding to the four “quadrants” identified by the portfolio

, corresponding to the four “quadrants” identified by the portfolio

(see Table 1); note that the portfolio

(see Table 1); note that the portfolio

yields the pay-off

yields the pay-off

and costs

and costs . The vectors

. The vectors

and the constants

and the constants , calculated as in

, calculated as in

Table 1. The four regions of the portfolio space in Example 4.

previous Example 3, are also shown.

There are positive vectors in

(such as

(such as , for instance); yet, the negative components of

, for instance); yet, the negative components of

and

and

indicate the possibility of a convenient super-hedging. It is quite clear that such possibilities apply to all of the portfolios belonging to the regions

indicate the possibility of a convenient super-hedging. It is quite clear that such possibilities apply to all of the portfolios belonging to the regions

and

and .

.

Consider, for instance, the portfolio , whose pay-off is

, whose pay-off is

and whose price is

and whose price is . It is immediate to check that the pay-off

. It is immediate to check that the pay-off

can be super-hedged by means of the portfolio

can be super-hedged by means of the portfolio , whose pay-off is

, whose pay-off is

and whose price is

and whose price is : a convenient super-hedging is found, and the cheapest super-hedging price functional

: a convenient super-hedging is found, and the cheapest super-hedging price functional

will be such that

will be such that

(indeed, it can be shown that the equality holds).

(indeed, it can be shown that the equality holds).

Analogously, the portfolio

yields the pay-off

yields the pay-off

at the price

at the price , but a convenient super-hedging is given by

, but a convenient super-hedging is given by , whose pay-off is

, whose pay-off is

and whose price is

and whose price is . Therefore,

. Therefore,

(and, as before, the equality holds, indeed).

(and, as before, the equality holds, indeed).

It is possible to prove7 that the “adjusted” functional , calculated after exploiting all of the convenient super-hedgings, is calculated as the maximum of six affine functionals as shown in Table 2. Notably enough, the convex set

, calculated after exploiting all of the convenient super-hedgings, is calculated as the maximum of six affine functionals as shown in Table 2. Notably enough, the convex set

identified by the six vectors

identified by the six vectors

exactly amounts to the subset of the positive vectors contained in the “original” set

exactly amounts to the subset of the positive vectors contained in the “original” set

(see Figure 2). Note also that not all of the vectors

(see Figure 2). Note also that not all of the vectors ,

,

, induce risk neutral measures, because some of them have negative components; however, each of the six “vertices” of the “restricted” set

, induce risk neutral measures, because some of them have negative components; however, each of the six “vertices” of the “restricted” set

can again be seen as the product of a risk neutral measure and a discount factor (for instance,

can again be seen as the product of a risk neutral measure and a discount factor (for instance,

corresponds to the degenerate probability

corresponds to the degenerate probability

such that

such that

and to the discount fac-

and to the discount fac-

Figure 2. The sets

(thin line) and

(thin line) and

(thick line) in Example 4.

(thick line) in Example 4.

Table 2. The four regions of the portfolio space in Example 4 after taking advantage of the convenient super-hedging opportunities.

tor ). Nevertheless, we remark that such elements are not as important as the js themselves to investigate market efficiency.

). Nevertheless, we remark that such elements are not as important as the js themselves to investigate market efficiency.

When it comes to positivity, things get a little more complicated: indeed, the fact that

contains no positive functionals at all is still sufficient, but no longer necessary, in order to allow for arbitrages. Consider the following (and quite minimal) example.

contains no positive functionals at all is still sufficient, but no longer necessary, in order to allow for arbitrages. Consider the following (and quite minimal) example.

Example 5. Again on , suppose that the asset

, suppose that the asset

is sold at the unit price 0.4 regardless of the amount, and that

is sold at the unit price 0.4 regardless of the amount, and that

is sold at unit price

is sold at unit price

up to 5 units, and 0.5 for more than 5 units. The portfolio space is trivially split into two regions (and in each of them, since

up to 5 units, and 0.5 for more than 5 units. The portfolio space is trivially split into two regions (and in each of them, since , it is trivially

, it is trivially ):

):

It is clear that arbitrages are possible, because buying

with

with

has a negative price for every

has a negative price for every

. Nevertheless, the set

. Nevertheless, the set

contains the positive vector

contains the positive vector .

.

It is still possible to define the cheapest super-hedging price functional : it turns out that it simply amounts

: it turns out that it simply amounts

to replace, in the region ,

,

and

and

with

with

and

and . As a consequence, it is no longer

. As a consequence, it is no longer : indeed,

: indeed,

, which precisely indicates the possibility to get a free gain of 3 without risk. It is

, which precisely indicates the possibility to get a free gain of 3 without risk. It is

also worth pointing out that such an arbitrage is just “local” in the spirit of Castagnoli et al. (2011) , in the sense that there is an upper bound to the gains that can be obtained by means of arbitrages.

The point is that, as already mentioned, an arbitrage is nothing but a convenient super-hedging of the null vector. In the sublinear case, positive homogeneity ensures that such a convenient super-hedging (meaning both its positive pay-off and its negative price) can be multiplied by an arbitrary positive constant and still remain an arbitrage: this way, if arbitrages are possible, the region of the arbitrage portfolios is always unbounded. In the “granular” convex case, instead, positive homogeneity no longer holds, and therefore arbitrages may be confined to a bounded region, as it happens in Example 5.

As a matter of fact, it is possible to show that a linear functional

matters in determining whether

matters in determining whether

allows for arbitrages or not only if

allows for arbitrages or not only if

is relative to a “region” of the portfolio space that contains the null pay-off: we call

is relative to a “region” of the portfolio space that contains the null pay-off: we call

such a subset of

such a subset of

8. In other terms, while

8. In other terms, while

is the union of all subdifferentials of

is the union of all subdifferentials of , we are here only interested in the subdifferential

, we are here only interested in the subdifferential

of

of

at the origin. Briefly, a convex functional

at the origin. Briefly, a convex functional

is positive if and only if there exists a positive

is positive if and only if there exists a positive .

.

For sublinear functionals, it can be proven that the subdifferential at each point is by necessity a subset of the subdifferential at 0, or, in other words that . This, besides the “unbounded” nature of arbitrages in sublinear markets, provides a further argument in favour of the fact that, unlike what happens for convex markets, in sublinear markets absence of arbitrages and absence of convenient super-hedgings are properties of the same set L.

. This, besides the “unbounded” nature of arbitrages in sublinear markets, provides a further argument in favour of the fact that, unlike what happens for convex markets, in sublinear markets absence of arbitrages and absence of convenient super-hedgings are properties of the same set L.

The results of this section can be summarized and formalized in the following

Theorem 1. Let

be a linear space of financial assets, and

be a linear space of financial assets, and

be a convex pricing functional such that

be a convex pricing functional such that . Define

. Define

and, for every

and, for every , call

, call

and

and , so that

, so that . Let

. Let

and

and . Then:

. Then:

1. L is non-empty, closed and convex;

2. for every ,

, ;

;

3. for every ,

,

and

and

is linear; furthermore, there exists

is linear; furthermore, there exists

such that

such that ;

;

4.

and

and

are non-empty, closed and convex, and

are non-empty, closed and convex, and ;

;

5.

is increasing if and only if every

is increasing if and only if every

is positive;

is positive;

6.

is positive if and only if there exists a positive

is positive if and only if there exists a positive .

.

3. Increasing Average Prices

The Star-Shaped Case

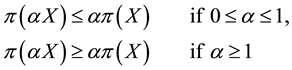

Suppose that

is such that the supply and demand function

is such that the supply and demand function

is convex. If, as it is natural to suppose,

is convex. If, as it is natural to suppose,

, then it turns out that

, then it turns out that

(3)

(3)

the first inequality comes from the convexity property, because (being ) it is

) it is ; it is furthermore possible to see that the two inequalities are equivalent to each other9.

; it is furthermore possible to see that the two inequalities are equivalent to each other9.

A possible reason why inequalities (3) are sensible in ordinary markets can be seen as follows. Take

such that

such that , so that

, so that . The first of the two inequalities (3) above is equivalent to

. The first of the two inequalities (3) above is equivalent to

in other words, the supply and demand function of an

satisfies (3) if and only if the average unit price of X is increasing with respect to the traded amount. This is why we deem reasonable such a property: indeed, when aiming at purchasing some quantity of something, it is rational to buy it at the lowest possible overall price, which of course coincides with the lowest average unit price.

satisfies (3) if and only if the average unit price of X is increasing with respect to the traded amount. This is why we deem reasonable such a property: indeed, when aiming at purchasing some quantity of something, it is rational to buy it at the lowest possible overall price, which of course coincides with the lowest average unit price.

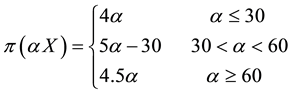

Suppose, for instance, that three agents sell the same asset X on the market. The first one sells it at 4 per unit, but can only provide up to 30 units. The second one sells it at 5 per unit (for any amount). The third one sells it at 4.5 per unit, but only for a minimum order of 50 units. It is clear that the best price that can be obtained to buy

units of X are:

units of X are:

for instance, to buy 50 units of X, the unit price of 4.5 may be obtained, but it is less expensive to buy 30 units from the first agent and 20 from the second, at a total price of

instead of

instead of . Note that the average price obtained with the “separate” purchase is

. Note that the average price obtained with the “separate” purchase is .

.

We shall call star-shaped a supply and demand function

that satisfies inequalities (3) and, in general, any function

that satisfies inequalities (3) and, in general, any function , with

, with

any real linear space, that does the same. Note the difference with “granular” pricing functionals, which feature an increasing marginal price with respect to the traded amount: of course every convex function is star-shaped as well, but the converse need not be true.

any real linear space, that does the same. Note the difference with “granular” pricing functionals, which feature an increasing marginal price with respect to the traded amount: of course every convex function is star-shaped as well, but the converse need not be true.

Example 6. The function

defined as

defined as

is star shaped, because ( and) its “average value”

and) its “average value”

is increasing. Nevertheless, f is not convex (and not even continuous).

is increasing. Nevertheless, f is not convex (and not even continuous).

A geometrical interpretation of the star-shaped property is easily deduced from the monotonicity of average prices. Recall that, given any real linear space , a function

, a function

is convex if and only if, whenever two points

is convex if and only if, whenever two points

are given “above” the “graph” of f, i.e., such that

are given “above” the “graph” of f, i.e., such that

, then the entire segment adjoining

, then the entire segment adjoining

and

and

remains “above” the graph of f (which translates into

remains “above” the graph of f (which translates into

for every

for every ). The property that average prices are increasing for star-shaped functions translates into the fact that whenever

). The property that average prices are increasing for star-shaped functions translates into the fact that whenever

is given “above” the “graph” of f, i.e., such that

is given “above” the “graph” of f, i.e., such that , then the entire segment adjoining

, then the entire segment adjoining

and

and

remains “above” the graph of f (which translates into

remains “above” the graph of f (which translates into

for every

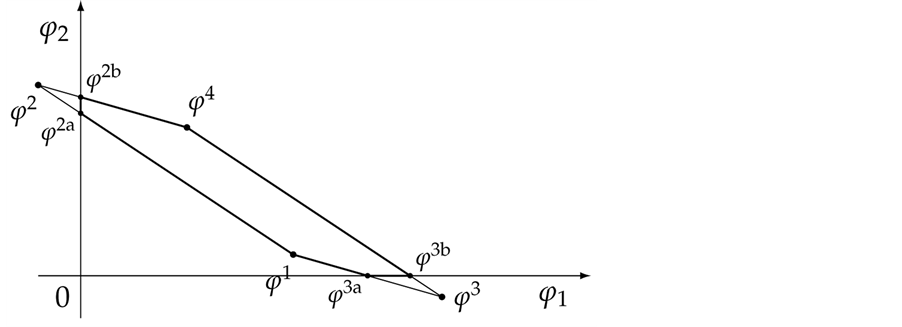

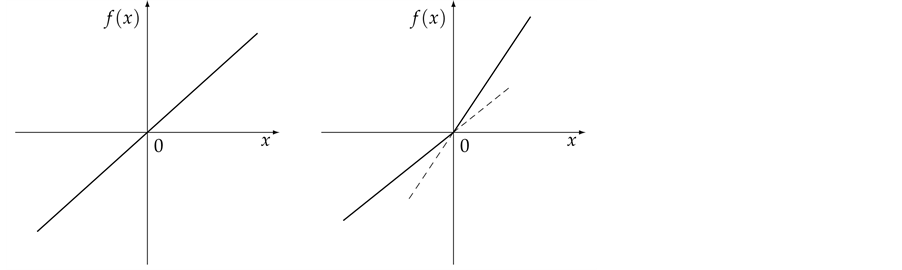

for every ). In Figure 3 the typical appearance of the four functions examined in this paper is depicted for functions

). In Figure 3 the typical appearance of the four functions examined in this paper is depicted for functions .

.

(a) (b)

(a) (b) (c) (d)

(c) (d)

Figure 3. Typical graphs of (a) a linear function; (b) a sublinear (and not linear) function; (c) a convex (and not sublinear) function and (d) a star-shaped (and neither convex nor continuous) function.

Suppose that, in an exchange list under consideration, the assets

are included, such that, for every

are included, such that, for every , the supply and demand function

, the supply and demand function

is increasing and star-shaped. Once again, we define on the set

is increasing and star-shaped. Once again, we define on the set

of all attainable pay-offs a price functional

of all attainable pay-offs a price functional

by super-hedging:

by super-hedging:

As usual, such a functional immediately turns out to be increasing (and therefore positive, because ); moreover, it can be proved that

); moreover, it can be proved that

is star shaped as well, i.e., that inequalities (3) hold for every

is star shaped as well, i.e., that inequalities (3) hold for every . So to say, the star-shape of the single supply and demand functions “propagates” by super-hedging.

. So to say, the star-shape of the single supply and demand functions “propagates” by super-hedging.

An adaptation of a result by

Chateauneuf & Aouani (2008)

, still unpublished (see

Castagnoli et al., 2009

), shows that a star-shaped functional

can be represented as the pointwise minimum of the convex functions that dominate it. In detail:

can be represented as the pointwise minimum of the convex functions that dominate it. In detail:

Proposition 2. Let

be a star-shaped functional. Then the set

be a star-shaped functional. Then the set

is closed and convex, and

is closed and convex, and

for every

for every .

.

It is indeed possible to prove that only the convex functionals

such that

such that

can be taken into consideration, i.e., that if

can be taken into consideration, i.e., that if , then (

, then ( is closed and convex as well and)

is closed and convex as well and)

as well. By applying Proposition 1, we can write each

as well. By applying Proposition 1, we can write each

as in (2), and therefore represent the star-shaped functional

as in (2), and therefore represent the star-shaped functional

as

as

(4)

(4)

To give an economical interpretation of such a representation, think that several agents are available to sell X on the market. Each agent, corresponding to a , assigns a convex price to X (i.e., has an increasing marginal price), and we are free to choose the agent we want to buy the asset X from (i.e., the cheapest one).

, assigns a convex price to X (i.e., has an increasing marginal price), and we are free to choose the agent we want to buy the asset X from (i.e., the cheapest one).

It is worth mentioning that the class of star-shaped functionals is closed under pointwise sup and inf, even for an infinite family of functionals; more explicitly, if

is any real linear space and

is any real linear space and

is a family of star-shaped functionals such that

is a family of star-shaped functionals such that , then

, then

and

and .

.

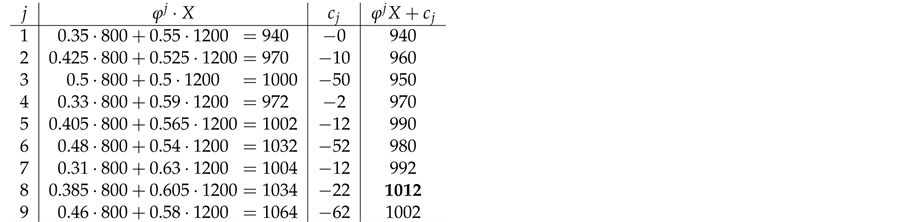

Example 7. Take into consideration the same two assets of Examples 1, 2, and 3, with pay-off matrix

We suppose that the investor can call her/his demands on three different markets, each run by a (representative) agent with her/his own convex price system: this way, three convex price functionals

We suppose that the investor can call her/his demands on three different markets, each run by a (representative) agent with her/his own convex price system: this way, three convex price functionals ,

,

and

and

are given. Suppose that the first one is the same of Example 2, with nine portfolio region as follows:

are given. Suppose that the first one is the same of Example 2, with nine portfolio region as follows:

The second agents gives the granular price functional

identified by10

identified by10

The third agent simply gives a linear price: ,

, .

.

Let us take into consideration some random variables: the details of the calculations (which amount to see in which region the price of the given pay-offs is maximum) are left to the reader.

• For , it is

, it is ,

,

, and

, and : therefore,

: therefore,

is bought from the second agent and

is bought from the second agent and .

.

• For , it is

, it is ,

,

, and

, and : therefore,

: therefore,

is bought from the first agent and

is bought from the first agent and .

.

• For , it is

, it is ,

,

and

and : therefore,

: therefore,

is bought from the third agent and

is bought from the third agent and .

.

It is then clear that each of the three price systems has a chance to prove the cheapest one and, therefore, that it is effective in determining

as the pointwise minimum of

as the pointwise minimum of ,

,

, and

, and . This can happen even for a

. This can happen even for a

single asset: for instance, the three demand functions

for

for

in the three mar-

in the three mar-

kets turn out to be:

and . It is straightforward (but very laboured) to see that

. It is straightforward (but very laboured) to see that

note that the marginal price is not increasing (for instance, around , it decreases from 15.925 to

, it decreases from 15.925 to

15.075), whereas the average one is.

It is still true that the star-shaped price functional

does not allow for convenient super-hedgings if and only if it is increasing.