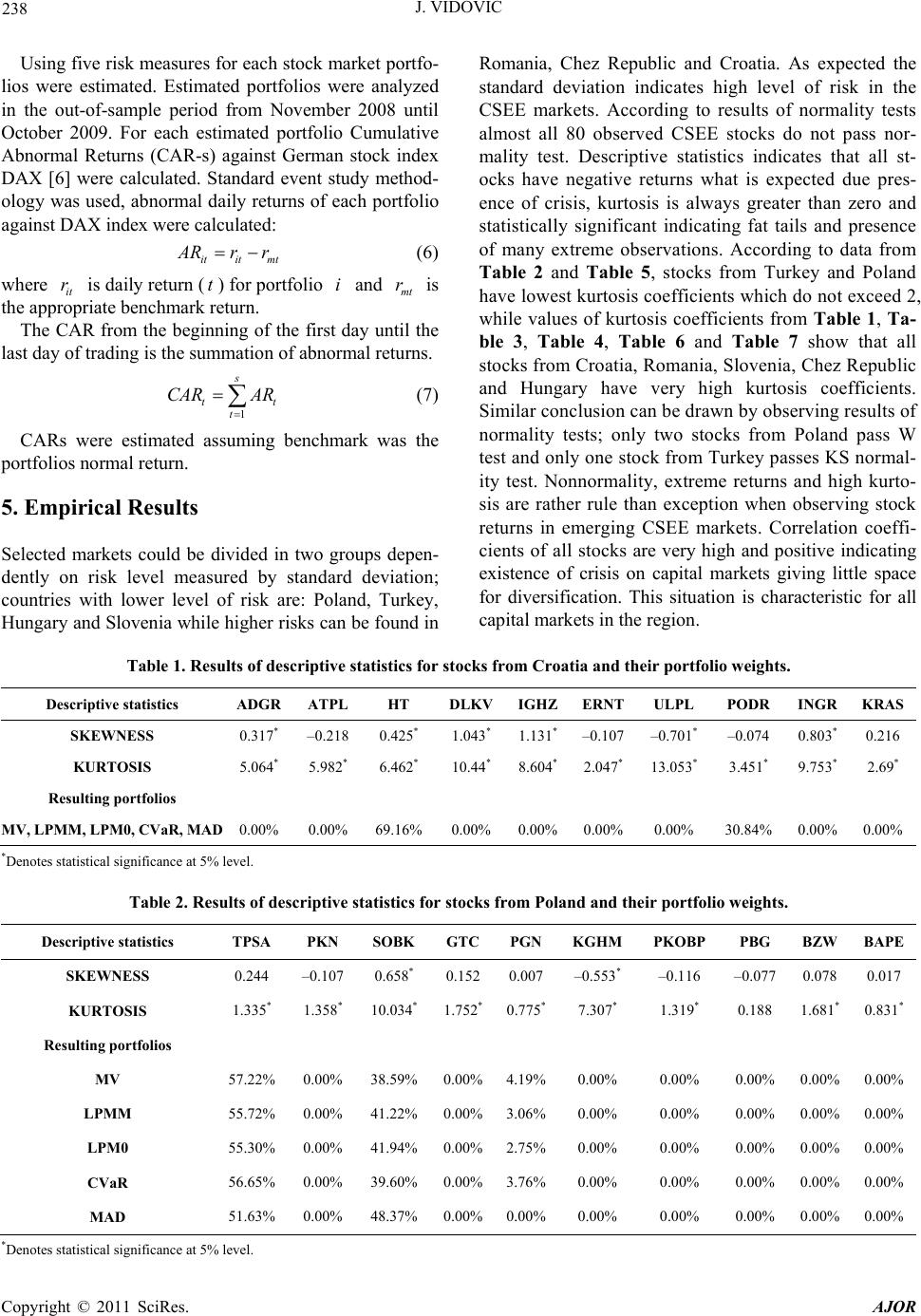

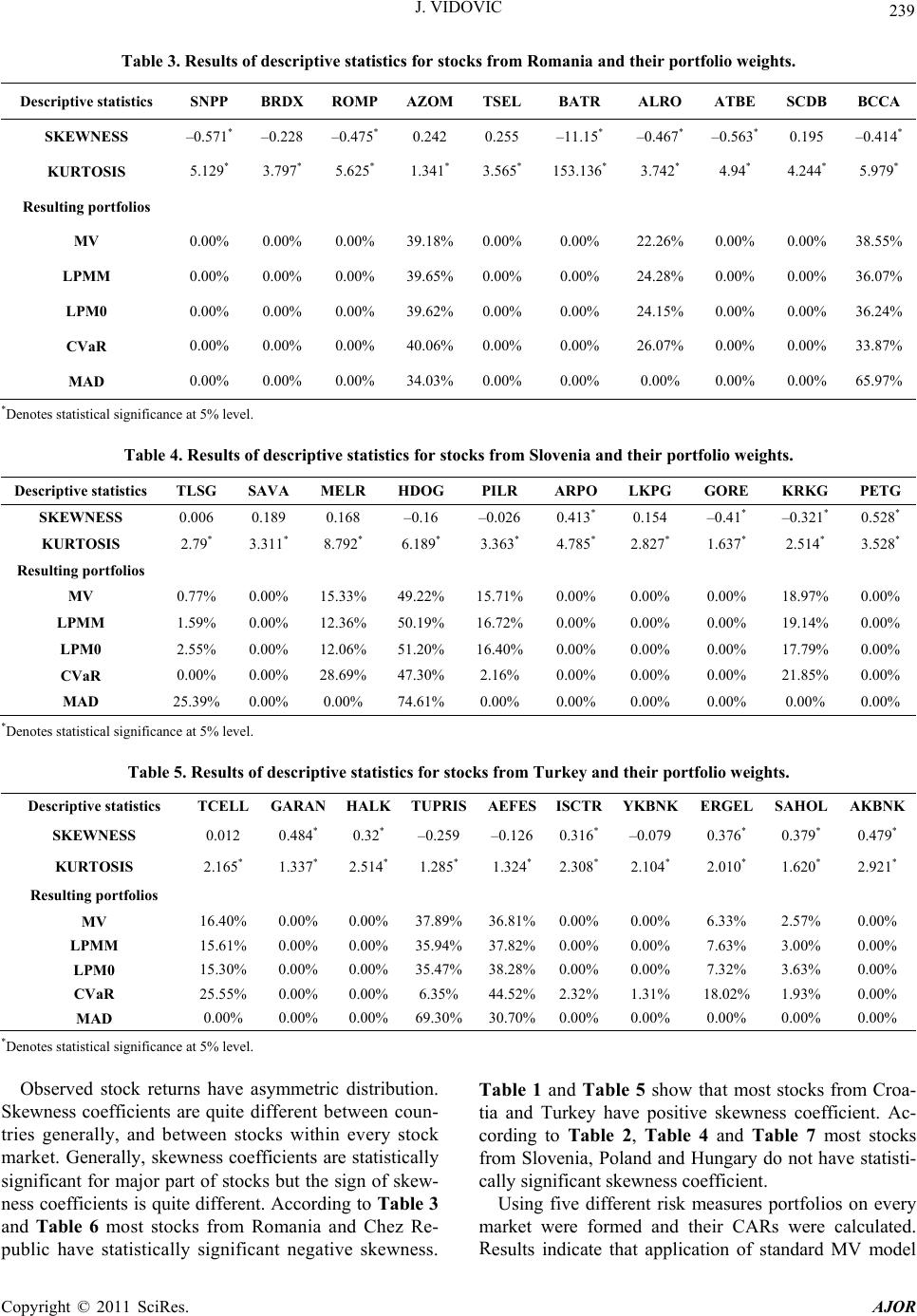

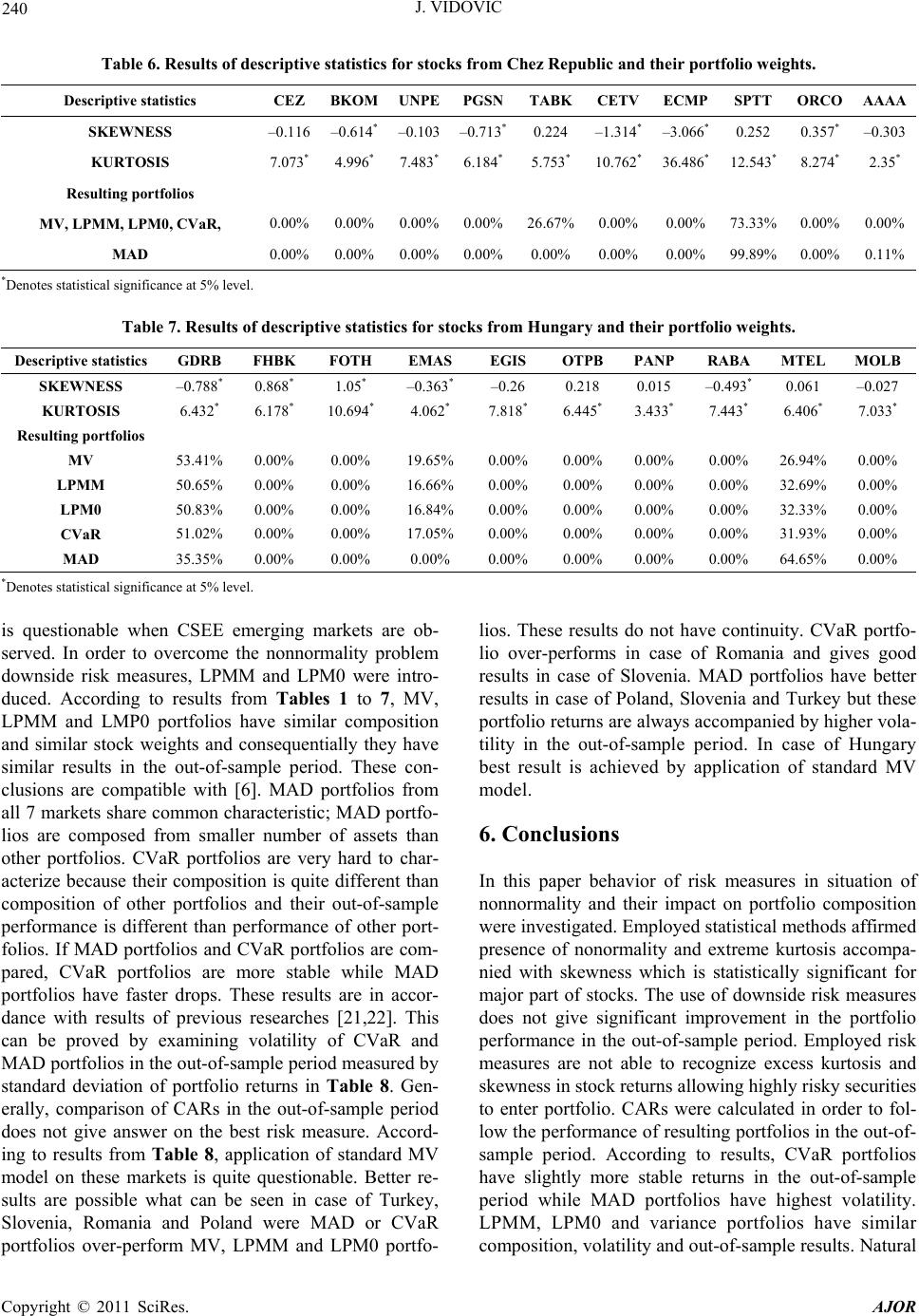

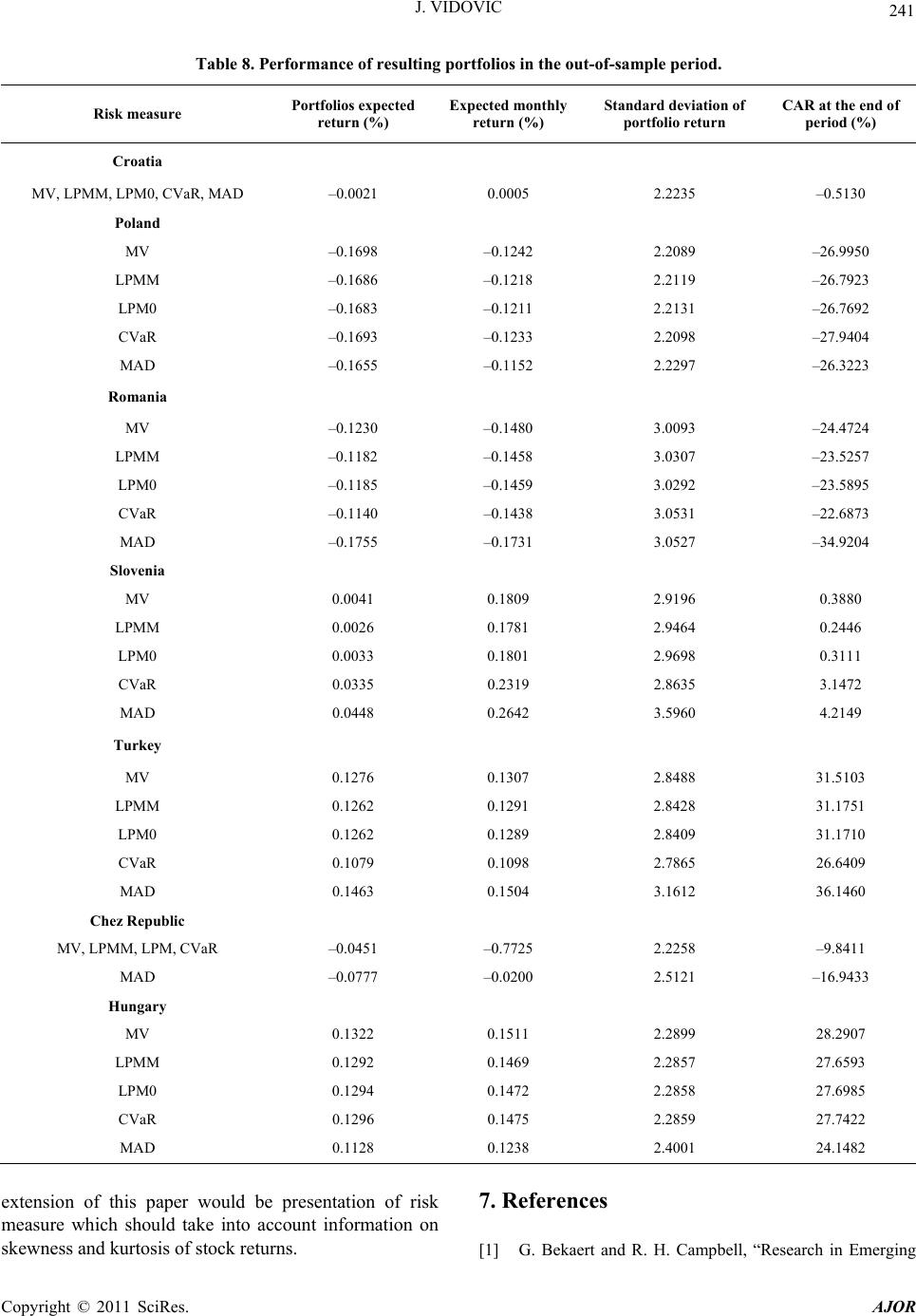

J. VIDOVIC

242

Markets Finance: Looking to the Future,” Emerging Mar-

kets Review, Vol. 3, No. 4, 2002, pp. 429-448.

doi:10.1016/S1566-0141(02)00045-6

[2] G. Bekaert and C. Harvey, “Emerging Markets Finance,”

Journal of Empirical Finance, Vol. 10, No. 1-2, 2003, pp.

3-56. doi:10.1016/S0927-5398(02)00054-3

[3] S. Stevenson, “Emerging Markets, Downside Risk and

the Asset Allocation Decision,” Emerging Markets Re-

view, Vol. 2, No. 1, 2001, pp. 50-66.

doi:10.1016/S1566-0141(00)00019-4

[4] R. Susmel, “Extreme Observations and Diversification in

Latin America Emerging Equity Markets,” Journal of In-

ternational Money and Finance, Vol. 20, No. 7, 2001, pp.

971-986. doi:10.1016/S0261-5606(01)00014-6

[5] J. Vidović and Z. Aljinović, “Research on Stock Returns

in Central and South-East European Transitional Econo-

mies,” Proceedings KOI 10th International Symposium

on Operational Research in Slovenia, Nova Gorica, 23 -

25 September 2009, pp. 237-246.

[6] C. G. Gilmore, G. M. McManus and A. Tezel, “Portfolio

Allocations and the Emerging Equity Markets of Central

Europe,” Journal of Multinational Financial Manage-

ment, Vol. 15, No. 3, 2005, pp. 287-300.

doi:10.1016/j.mulfin.2004.12.001

[7] C. A. J. Middleton, S. G. M. Fifield and D. M. Power,

“Investment in Central and Eastern European Equities,”

Studies in Economics and Finance, Vol. 24, No. 1, 2007,

pp. 13-31. doi:10.1108/10867370710737364

[8] T. Gklezakou and J. Mylonakis, “Interdependence of the

Developing Stock Markets, before and during the Eco-

nomic Crisis: The Case of South Europe,” Journal of

Money, Investment and Banking, Vol. 11, 2009, pp. 70-

78.

[9] J. Bley, “European Stock Market Integration: Fact or

Fiction?” Journal of International Financial Markets, In-

stitutions and Money, Vol. 19, No. 5, 2009, pp. 759-776.

[10] H. M. Markowitz, “Portfolio Selection: Efficient Diversi-

fication of Investments,” John Wiley & Sons, New York,

1959.

[11] P. C. Fishburn, “Mean-Risk Analysis with Risk Associ-

ated with Below-Target Returns,” American Economic

Review, Vol. 67, No. 2, 1977, pp. 116-126.

[12] V. S. Bawa and E. B. Lindenberg, “Capital Market Equi-

librium in a Mean-Lower Partial Moments Framework,”

Journal of Financial Economics, Vol. 5, No. 2, 1977, pp.

198-200. doi:10.1016/0304-405X(77)90017-4

[13] H. Konno and H. Yamazaki, “Mean-Absolute Deviation

Portfolio Optimization Model and Its Application to To-

kyo Stock Market,” Management Science, Vol. 37, No. 5,

1991, pp. 519-531. doi:10.1287/mnsc.37.5.519

[14] S. Uryasev, “Conditional Value-at-Risk (CVaR): Algo-

rithms and Applications,” Working Paper, University of

Florida, 2002. http://www.ise.ufl.edu/uryasev

[15] A. Alexandre, M. Houkari and J.-P. Laurent, “Spectral

Risk Measures and Portfolio Selection,” Journal of Bank-

ing and Finance, Vol. 32, No. 9, 2008, pp. 1870-1882.

doi:10.1016/j.jbankfin.2007.12.032

[16] C. Acerbi and D. Tasche, “On the Coherence of Expected

Shortfall,” Journal of Banking and Finance, Vol. 26, No.

7, 2002, pp. 1487-1503.

doi:10.1016/S0378-4266(02)00283-2

[17] R. T. Rockafellar and S. Uraysev, “Optimization of Con-

ditional Value-at-Risk,” Journal of Risk, Vol. 2, No. 3,

2000, pp. 21-41.

[18] G. Y. N. Tang, “How Efficient Is Naive Portfolio Diver-

sification? An Educational Note,” Omega—The Interna-

tional Journal of Management Science, Vol. 32, No. 2,

2004, pp. 155-160.

[19] L. R. Irala and P. Patil, “Portfolio Size and Diversifica-

tion,” SMCS Journal of Indian Management, Vol. 4, No.

1, 2007, pp. 1-6.

[20] S. S. Shapiro, M. B. Wilk and H. J. Chen, “A Compara-

tive Study of Various Tests of Normality,” Journal of the

American Statistical Association, Vol. 63, No. 324, 1968,

pp. 1343-1372. doi:10.2307/2285889

[21] Y. Simaan, “Estimation Risk in Portfolio Selection: The

Mean Variance Model versus the Mean Absolute Devia-

tion Model,” Management Science, Vol. 43, No. 10, 1997,

pp. 1437-1446. doi:10.1287/mnsc.43.10.1437

[22] E. Angelelli, R. Mansini and G. M. Speranza, “A Com-

parison of MAD and CVaR Model with Real Features,”

Journal of Banking & Finance, Vol. 32, No. 7, 2008, pp.

1188-1197. doi:10.1016/j.jbankfin.2006.07.015

Copyright © 2011 SciRes. AJOR