C. F. LING ET AL.

Copyright © 2011 SciRes. JMF

118

that the superior performance of growth stocks in the late

1990s was mainly due to investors’ rosy expectation about

the future growth of technology co mpanies, rather than a

change in fundamentals. For this to be true, there should

have then been a subsequent price adjustment for both

value and growth stocks to reflect their earnings growth.

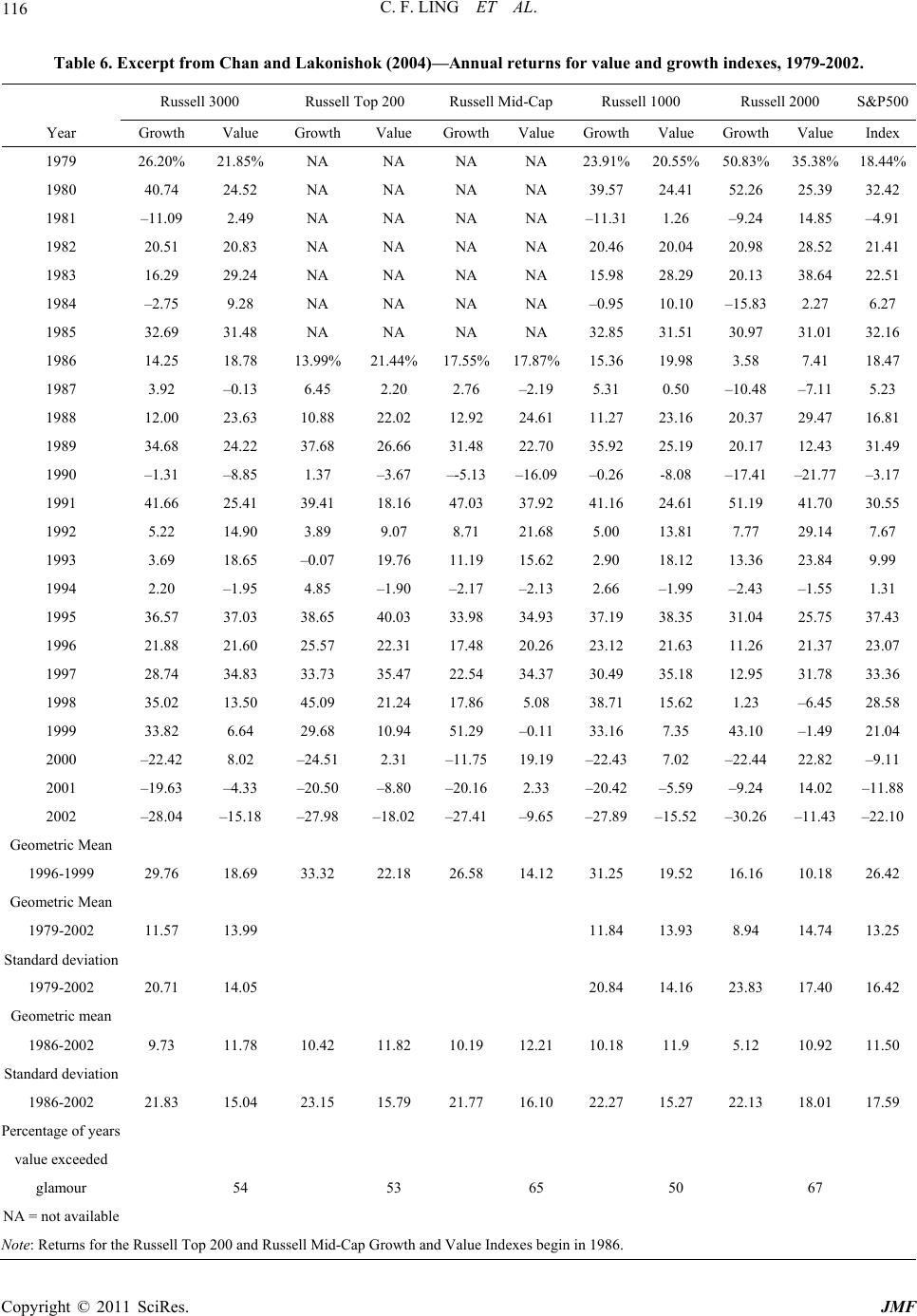

Indeed, in Table 6 we can see that in 2000, the Russell

Top 200 Growth Index fell by 24.51%, followed by a

decline of 20.5% the next year. On the other hand, the

Russell 2000 Value Index rose by 22.82% and 14.02%,

respectively. This indicates that investors finally realized

that those “growth” companies had fallen short of their

expec tations, and a pr ice adjustmen t occurred as a result.

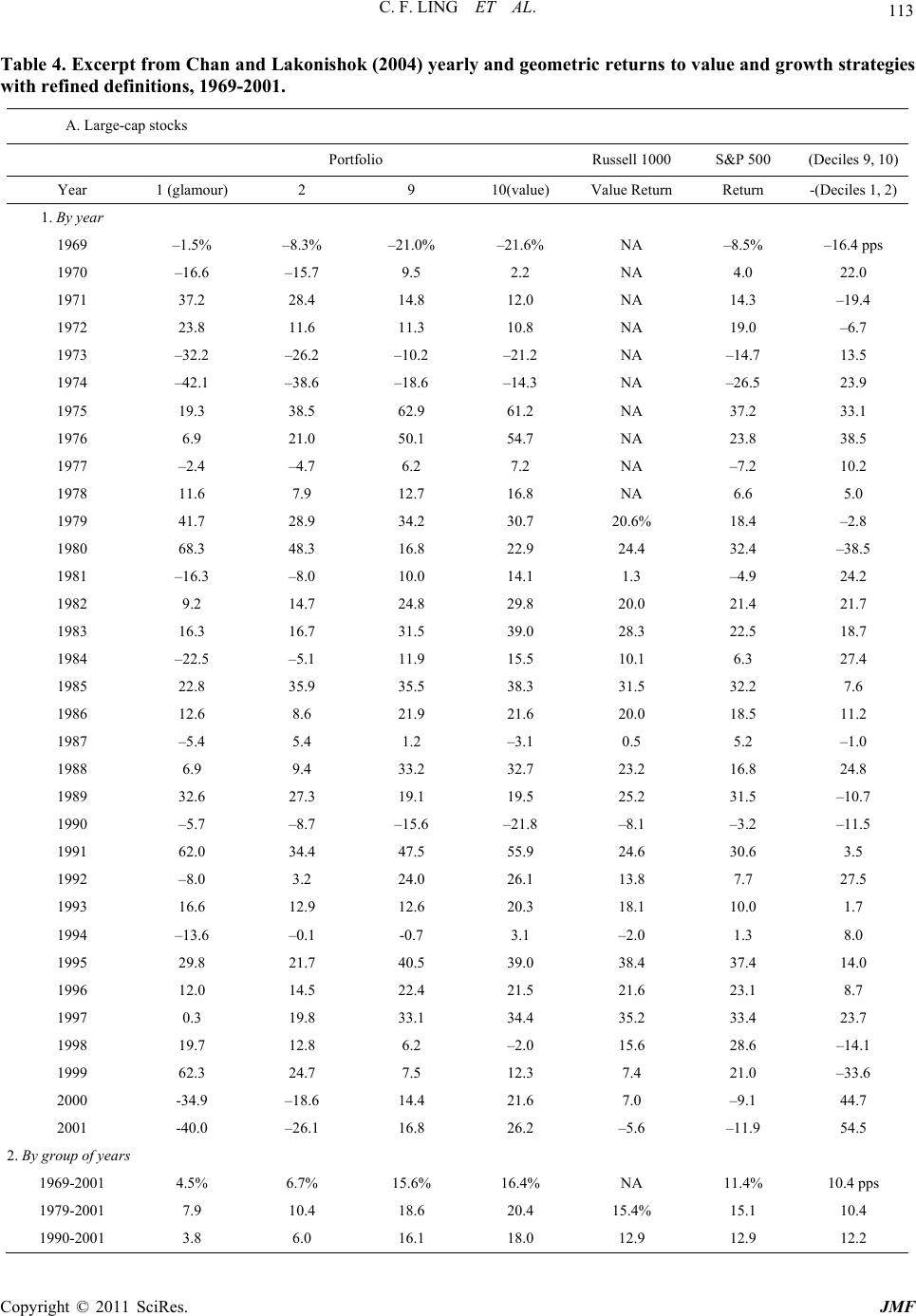

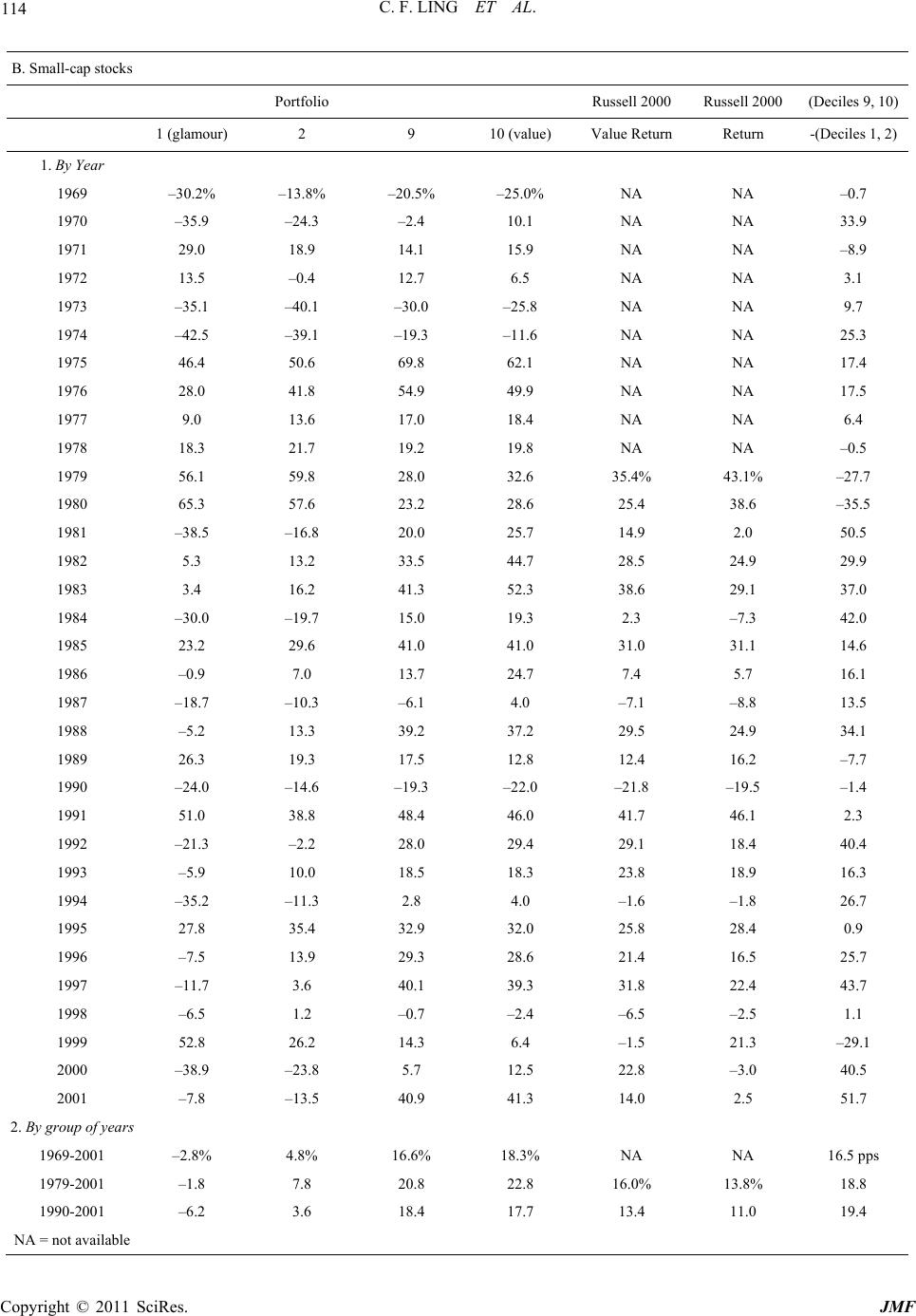

Looking at the overall record, from 1979 to 2002, the geo-

metric return of value stocks still outperformed growth

stocks. From Table 6, it was 13.99% vs. 11 .57% for large-

cap stocks, and 14.74% vs. 8.94% for small-cap stocks.

There were some discrepancies in the Russell index,

however, as it did not represent extreme bets on growth

or value since only two portfolios were formed (instead

of 10). Further, the underlying stocks were value weighted

and rely on only two indicators (BV/MV and analysts’

long-term growth forecasts). To address this concern,

Chan and Lakonishok [8] performed another analysis by

sorting stocks using a composite indicator and placing

them in 10 deciles with each stocks equally weighted in

each portfolio. The results are shown in Table 4. From

1996-2001, we can see that for large-cap stocks (Panel

A), the value portfolio only fell behind the growth port-

folio in 1998 and 1999, and cau ght up again in 2000 and

2001. As a result, the geometric return for value stocks

from 1990-2001 is 16.1%, compared to 3.8% for growth

stocks. For small cap stocks, the spread is even more sig-

nificant: 18.4% for value compared to –6.2% for growth.

3. Conclusions

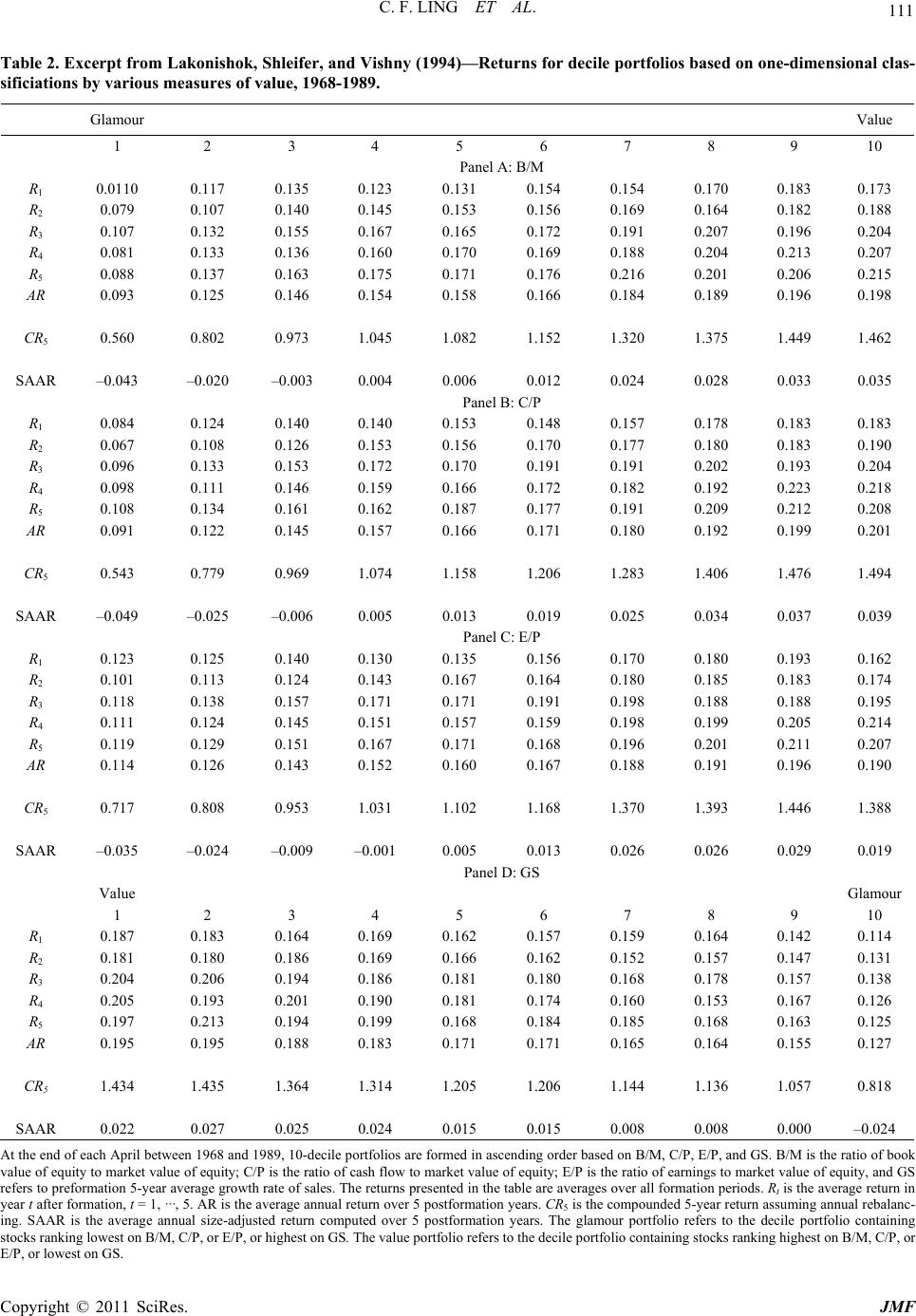

Various studies provided evidence that value stocks could

generate superior return than growth stocks. This spread

is often more significant in the small-cap stocks than in

the large-cap stocks, indicating that part of the spread must

be attributed to size of the companies. In addition, the

studies showed that systematic risk cannot not be accounted

for the spread as both glamour and value portfolios have

similar beta.

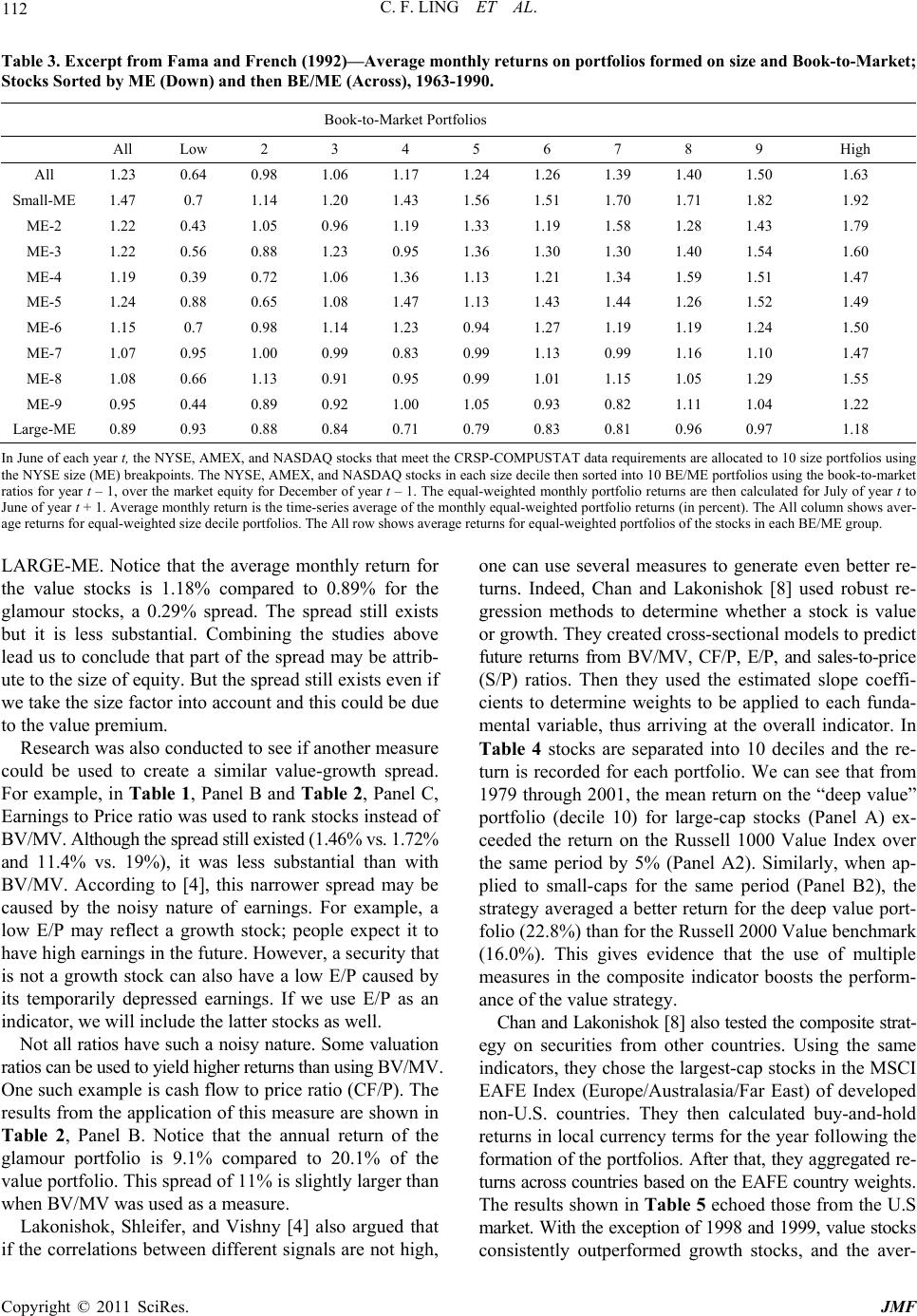

Further studies showed that even we took the compa-

nies’ size into account, the spread still existed. This leads

to the assertion there is a value premium that con tributes

to the spread. The reasons of the existence of value pre-

mium will be explored later. But in a vague sense, some

scholars argued that this could be caused by extrapola-

tion bias: people incorrectly use past data to predict fu-

ture performance of a company.

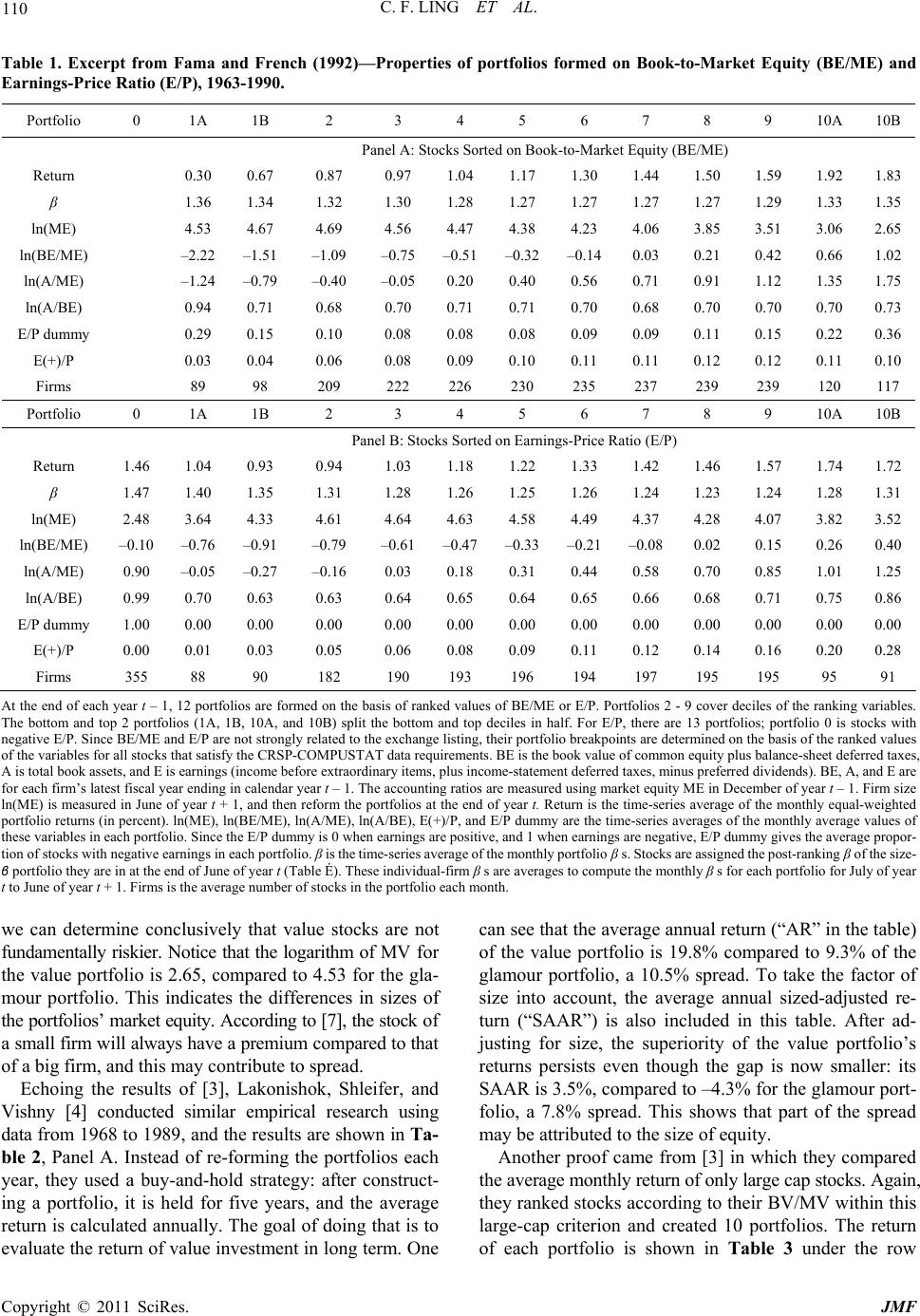

In addition, a number of different indicators could be

used to yield value premium. And a combination of such

indicators could often yield a higher return than using

just a single indicator.

On the other hand, the persisting superior return of

growth stocks in late 1990s seemed to invalidate the claim

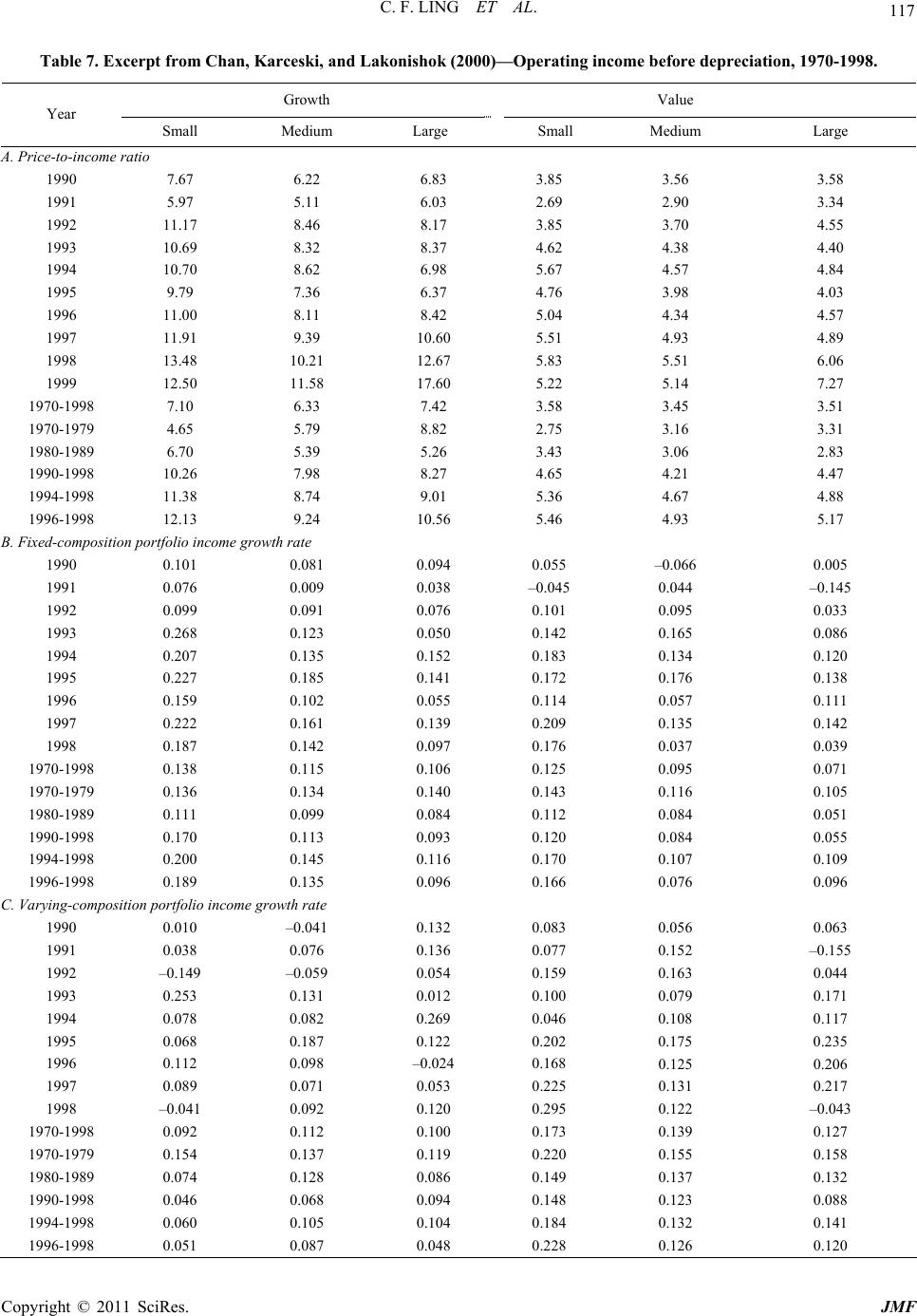

of value premium. However, further study showed that

those “growth” companies didn’t realize any stronger

subsequent earnings growth than value companies even

though their P/I ratio continued to be high. There was

also a rigorous price adjustment in late 2000 and 2001,

with value stocks skyrocketing and growth stocks plum-

meting. Combining these two pieces of evidence, some

scholars argued that the value premium did not disappear.

Instead, it just took longer for the price reversion to oc-

cur as market persisted to have rosy expectation to tech-

nology companies.

4. References

[1] B. Graham and D. Dodd, “Security Analysis,” 6th Edition,

Graw-Hill, New York City, 2009, pp. 61-70.

[2] S. Basu, “Investment Performance of Common Stocks in

Relation to Their Price-Earnings Ratios: A Test of the Ef-

ficient Market Hypothesis,” Journal of Finance, Vol. 32,

No. 3, 1977, pp. 255-274. doi:10.2307/2326304

[3] E. F. Fama and K. R. French, “The Cross-Section of Ex-

pected Stock Returns,” Journal of Finance, Vol. 47, No.

2, 1992, pp. 427-465. doi:10.2307/2329112

[4] J. Lakonishok, A. Shleifer and R. W. Vishny, “Contrarian

Investment, Extrapolation, and Risk,” Journal of Finance,

Vol. 49, No. 5, 1994, pp. 1541-1578.

doi:10.2307/2329262

[5] L. K. C. Chan, Y. Hamao, and J. Lakonishok, “Funda-

mentals of Stock Return in Japan,” Journal of Finance,

Vol. 46, No. 5, 1991, pp. 1739-1764.

doi:10.2307/2328571

[6] E. F. Fama and K. R. French. “Value versus Growth: The

International Evidence,” Journal of Finance, Vol. 53, No.

6, 1998, pp. 1975-1999. doi:10.1111/0022-1082.00080

[7] R. W. Banz, “The Relationship between Return and

Market Value of Common Stock,” Journal of Financial

Economics, Vol. 9, No. 1, 1981, pp. 3-18.

doi:10.1016/0304-405X(81)90018-0

[8] L. K. C. Chan and J. Lakonishok, “Value and Growth

Investing: Review and Update,” Financial Analyst Jour-

nal, Vol. 60, No. 1, 2004, pp. 71-86.

doi:10.2469/faj.v60.n1.2593

[9] C. Asness, “The Interaction of Value and Momentum

Strategies,” Financial Analysts Journal, Vol. 53, No. 2

1997, pp. 29-36. doi:10.2469/faj.v53.n2.2069

[10] D. Kent and S. Titman, “Market Efficiency in an Irra-

tional World,” Financial Analysts Journal, Vol. 55, No. 6

1999, pp. 28-40. doi:10.2469/faj.v55.n6.2312