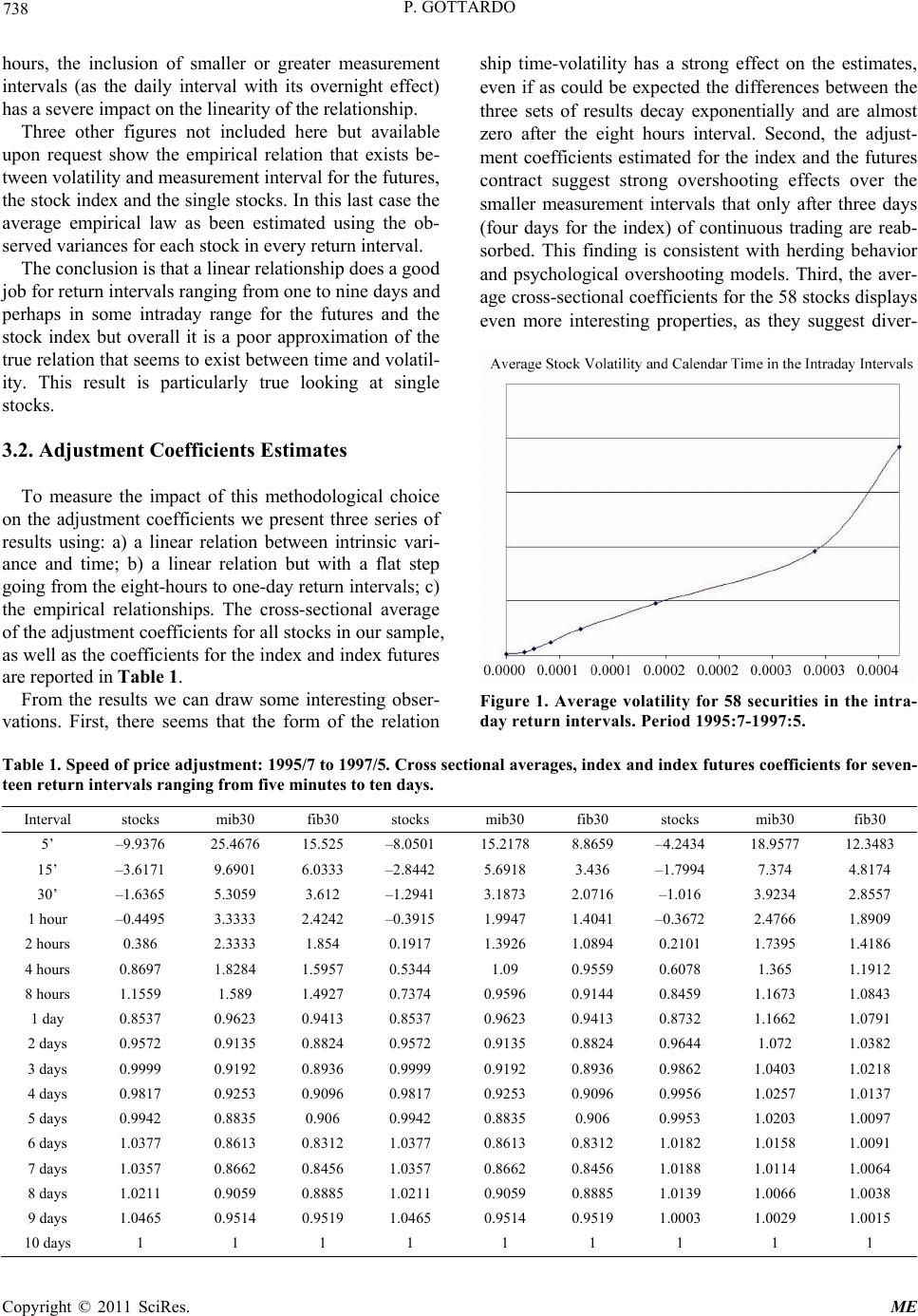

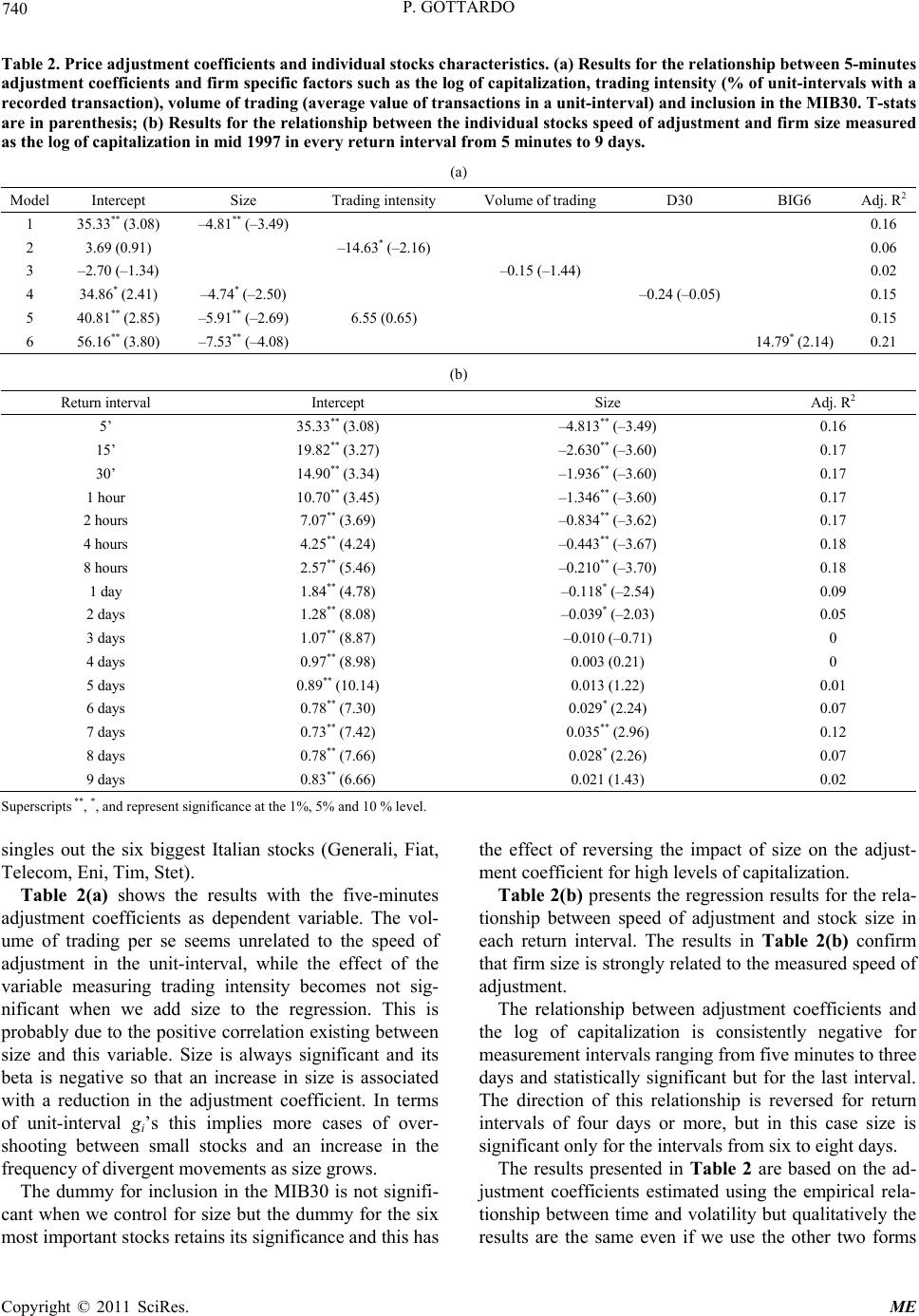

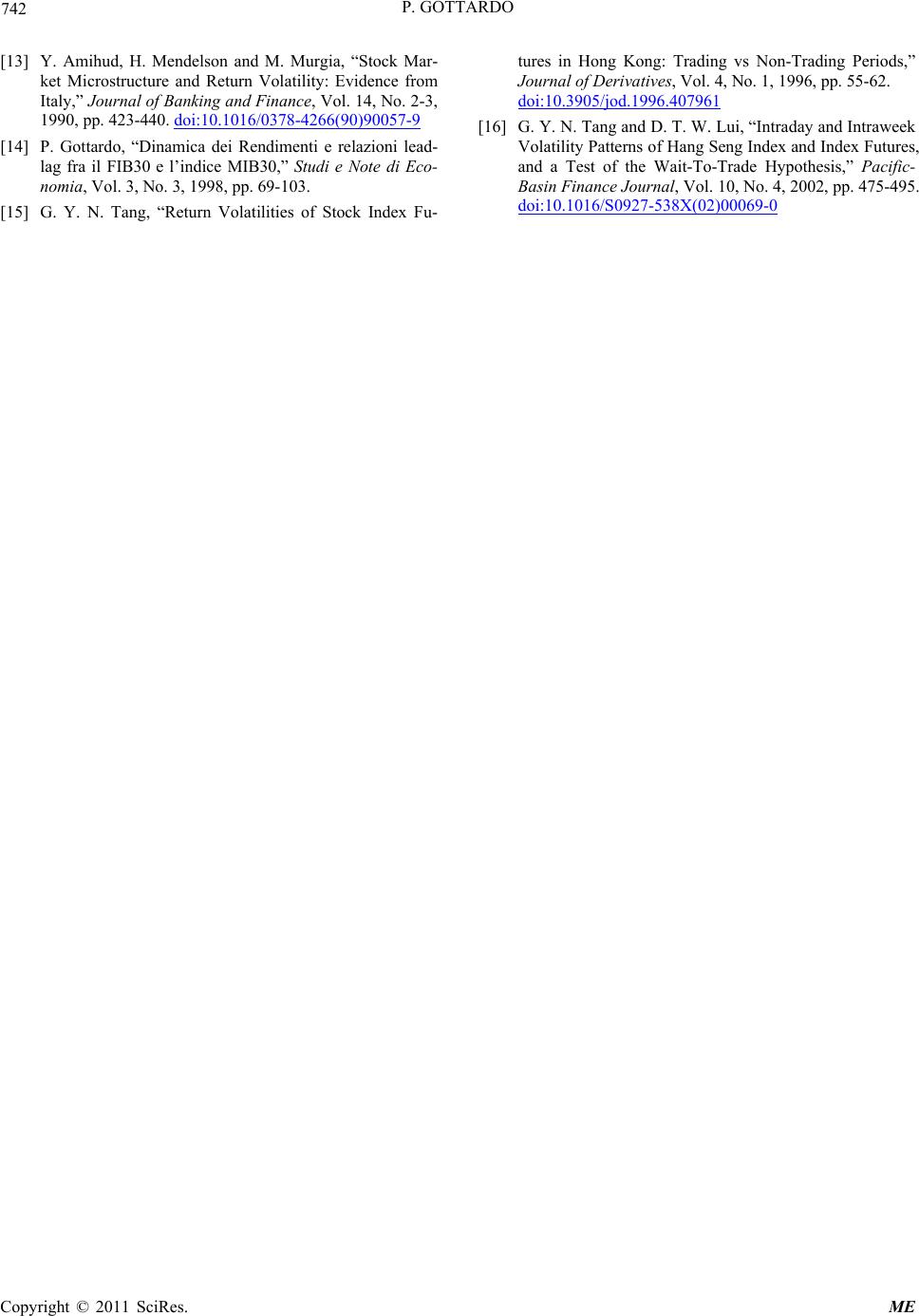

P. GOTTARDO 741

of the relationship.

Overall our results support the proposition that stock

prices adjust slowly to new information but in a different

manner for small and big firms and this is reflected in a

highly significant relation between adjustment coeffi-

cients and stock size. The inclusion in the MIB30 index

does not seem to be a relevant factor but this is the result

of two facts. First, only the biggest stocks are included in

the index, adding size as explanatory variable is likely to

dim any effect related to a dummy controlling for the

participation in the index. Second, among the big firms

the trading is highly concentrated in few stocks and is

not by chance that in Table 2(a) a dummy like BIG6 is

significant even when the MIB30 dummy is added to

model 6 (not shown). These six stocks are the core of

every portfolio whose aim is to replicate the index and

are necessary to implement any strategy requiring trading

in the futures and the unde rl ying m a rk et .

4. Conclusions

The degree of efficiency in the stock and futures markets

can be measured by the speed with which prices adjust to

incorporate new information. This process may be slow

with prices that take time to reflect value changes or very

speedy. It is also possible that in very short intervals or

in the long period prices display patterns that lead away

from equilibrium (at least temporarily) or give rise to

under and ov erreaction phenomen a.

This paper adapts the model developed in Amihud-

Mendelson [8] and Damodaran [9] to consider jointly

intraday and infraday data. The speed of adjustment is

estimated as function of the variances in different return

intervals from five minutes to ten days, as well as the

covariances in the infraday intervals. The approach is

then applied to the Italian index (MIB30) and index fu-

tures (FIB30), and to a sample of the most important

stocks listed in this market.

We show that the assumptions about the form of the

relationship between return volatility and time are critical

for the measured adjustment coefficients, the hypothesis

of linearity cannot be accepted using jointly intraday and

infraday returns as the resulting estimates are grossly

inflated for the smaller measurement intervals. We find

evidence that prices adjust slowly to new information,

three to five days of trading are necessary to complete

the adjustment and this is true for the index futures but

also on average for each individual stock. We also find

evidence that there is no simple intraday adjustment

process, the futures seems to overreact for small return

intervals, while on average the individual stocks diverge

from value for intervals up to two hours and then show a

pattern of lagged adjustment.

There are peculiar regularities in the price adjustment

of single stocks and the firms included in the index un-

derlying the futures behave differently from the others.

The analysis of the relationship between adjustment co-

efficients and firm characteristics confirms that size is

strongly related to the measured speed of adjustment for

most of the measurement intervals

5. References

[1] K. Daniel, D. Hirshleifer and A. Subrahmanyam, “Inves-

tor Psychology and Security Market Under- and Overre-

actions,” Journal of Finance, Vol. 53, No. 6, 1998, pp.

1839-1885. doi:10.1111/0022-1082.00077

[2] E. F. Fama, “Market Efficiency, Long Term Returns and

Behavioral Finance,” Journal of Financial Economics,

Vol. 49, No. 3, 1998, pp. 283-306.

doi:10.1016/S0304-405X(98)00026-9

[3] J. M. Patell and M. A. Wolfson, “The Intraday Speed of

Price Adjustment of Stock Prices to Earnings and Divi-

dend Announcements,” Journal of Financial Economics,

Vol. 13, No. 2, 1984, pp. 223-252.

doi:10.1016/0304-405X(84)90024-2

[4] J. Hasbrouck and T. Ho, “Order Arrival, Quote Behavior

and the Return-Generating Process,” Journal of Finance,

Vol. 42, No. 4, 1987, pp. 1035-1049.

doi:10.2307/2328305

[5] K. Garbade and W. Silber, “Structural Organization of

Secondary Markets: Clearing Frequency, Dealer Activity

and Liquidity Risk,” Journal of Finance, Vol. 34, No. 3,

1979, pp. 577-593. doi:10.2307/2327427

[6] K. Garbade and W. Silber, “Price Movement and Price

Discovery in Futures and Cash Markets,” Review of

Economics and Statistics, Vol. 65, No. 2, 1983, pp. 289-

297. doi:10.2307/1924495

[7] B. Goldman and A. Beja, “Market Prices vs. Equilibrium

Pri ces: Return’s Variance, Serial Correlation, and the Role

of the Specialist,” Journal of Finance, Vol. 34, No. 3,

1979, pp. 595-607. doi:10.2307/2327428

[8] Y. Amihud, and H. Mendelson, “Index and Index-Futures

Returns,” Journal of Accounting, Auditing & Finance,

Vol. 4, No. 2, 1989, pp. 415-431.

[9] A. Damodaran, “A Simple Measure of Price Adjustment

Coefficients,” Journal of Finance, Vol. 48, No. 1, 1993,

pp. 387-400. doi:10.2307/2328896

[10] N. Brisley and M. Theobald, “A Simple Measure of Price

Adjustment Coefficients: A Correction,” Journal of Fi-

nance, Vol. 51, No. 1, 1996, pp. 381-382.

doi:10.2307/2329314

[11] W. F. M. DeBondt and R. H. Thaler, “Does the Stock

Market Overreact?” Journal of Finance, Vol. 40, No. 3,

1985, pp. 793-808. doi:10.2307/2327804

[12] Y. Amihud and H. Mendelson, “Trading Mechanisms and

Stock Returns: An Empirical Investigation,” Journal of

Finance, Vol. 42, No. 3, 1987, pp. 533-553.

doi:10.2307/2328369

Copyright © 2011 SciRes. ME