Journal of Service Science and Management, 2011, 4, 380-390 doi:10.4236/jssm.2011.43044 Published Online September 2011 (http://www.SciRP.org/journal/nm) Copyright © 2011 SciRes. JSSM What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? Jun-Yi Shen1, Xiang-Dong Qin2 1Faculty of International Studies, Hiroshima City University, Hiroshima, Japan; 2School of Economics, Antai College of Economics and Management, Shanghai Jiao Tong University, Shanghai, China. Email: shen@intl.hiroshima-cu.ac.jp, xdqin@sjtu.edu.cn Received May 4th, 2011; revised July 6th, 2011; accepted July 16th, 2011. ABSTRACT Understanding why firms choose to implement voluntary environmental schemes in a large polluted coun try like China is important for both environmental economists and policy makers. In this paper, we utilize unique plant-level survey data of 270 Chinese firms in manufacturing industry to id entify the key determinants of their decisions on certifying IS O 14001 environmental management standard and the Chinese Environmental Label. The empirical results exhibit that while there are a number of factors (e.g., ownership, firm size, target market, and the number of rivals) having similar effects on the certification decisions between the two examined programs, the unique factors that only affect the deci- sion of certifying one program (i.e., ISO 140 01 or the Chinese Environmental Label) are also observed. Keywords: Voluntary Environmental Scheme, ISO 14001, Eco-Label, Chinese Firm 1. Introduction In the past decade, the trend towards promoting volun- tary action and pollution prevention as opposed to man- datory (command-and-control) environmental regulations that prescribe quantity limits on pollutants had increased as more governments worldwide faced and continue to face limited environmental enforcement budgets [1]. The emerging voluntary approach to pollution abatement be- comes more and more popular in recent years. This is because of a growing number of business-initiated ac- tions to change corporate culture and management prac- tices through the introduction of environmental label or eco-label programs and international environmental ma- nagement system certification programs such as the In- ternational Standards Organization (ISO) programs [2]. Eco-labels have been used for over twenty years to pro- vide consumers with information about a product which is characterized by improved environmental performance and efficiency compared with similar products without those labels. The main purpose of promoting eco-label programs is to avoid the possible asymmetric information problem between producers and consumers, because some environmentally friendly products normally have unobservable characteristics [3]. In comparison to eco- label programs, ISO programs concern the way a firm goes about its production, and notdirectly the results of this production. In other words, they concern processes, and not products—at least, not directly [1]. Among them, the ISO 14001 is an international, voluntary standard for environmental management promoted by the ISO, which formally includes five steps in an environmental man- agement system as environmental policy, planning, im- plementation and operation, checking and operation, and management review.1 In the literature, a number of studies have been under- taken on the determinants of firms’ environmental per- formance and firms’ voluntary pro-environmental action [5-18]. Among these studies, [12] employed panel data models to study how environmental innovation by US manufacturing industries responds to changes in pollu- tion abatement expenditures and regulatory enforcement during the period of 198 3 to 1992. They found that envi- ronmental innovation responds to increases in pollution abatement expenditures, however, increased monitoring and enforcement activities related to existing environ- mental regulations do not provide any additional incen- tive to innovate. [9] examined data on compliance with environmental regulations within the manufacturing sec- tor in Mexico and found that the probability of comply- ing depends on the kind of management practices of the 1For more detailed issues on the ISO 14001 management standard, see [4].  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes?381 firm and the level of environmental training. [14] inves- tigated whether firms’ characteristics influence their de- cisions to join the Environmental Protection Agency’s voluntary Green Lights program. They reported that con- trary to conventional theory, the characteristics of firms do affect their decisions to join Green Lights and co mmit to a program of investments in lighting efficiency. [11] examined empirically the determinants that led large Japanese manufacturers to voluntary environmental com- mitment and found that the costs and benefits of volun- tary actions to enhance or protect the environment, the capacity to act, as well as the environmental values, be- liefs, and attitudes of managers are significant determi- nants of voluntary environmental commitment. In addition to the above researches on the factors in- fluencing firms’ environmental performance and their voluntary pro-environmental action, we find two studies in the literature pointing to the impact of environmental performance on firm performance. [19] conducted a case study to examine the impact of environmental rating of large pulp and paper, auto, and chlor alkali firms on their stock prices and found that the market generally penal- izes environmentally unfriendly behavior. [20] conducted static and dynamic panel data analysis of the impact of environmental performance on the firm’s financial per- formance. They showed that environmental performance has a neutral impact on the firm’s financial performance, which is consistent with theoretical work suggesting that firms invest in environmental initiatives until the point where the marginal cost of such investments equals the marginal benefit. In recent years, China’s environmental problem, which is considered as a byproduct of its rapid economic growth, is becoming a well-known issue and receiving more and more attentions from both economists and en- vironmental specialists around the world. Previous stud- ies in the environmental economics literature related to environmental issues of Chinese firms paid a lot of atten- tions to the financial incentives and endogenous en- forcement in China’s pollution levy system (e.g., [15]), industrial ownership and environmental performance in China (e.g., [17]), bargaining power of Chinese factories in enforcement of pollution regulation (e.g., [13]), rela- tions among inspections, pollution prices and Chinese environmental performance (e.g., [8]), and Chinese firms’ technology development and energy productivity (e.g., [16]). However, the issue on the factors influencing Chinese firms’ practice of voluntary environmental schemes (e.g., the ISO 14001 and eco-label) has not been fully studied. For this purpose, a firm-level survey was conducted in 2008 to obtain a better understanding of a firm’s motivations, its decision-making procedures and its characteristics vis-à-vis its decision on joining a vol- untary environmental program. We consider two envi- ronmental programs here, one is ISO 14001 certification and the other is China Environmental Label (hereinafter referred to as eco-label). Consequently, th is paper tries to analyze the determinants that lead Chinese firms to im- plement ISO 14001 and/or eco-label certifications. More specifically, we provide empirical results regarding what determines a firm’s choice as to: 1) whether or not it should introduce a certified environmental management system (i.e., ISO 14001); 2) whether or not it should im- plement a certification of eco-label (i.e., China Environ- mental Label). The paper is organized as follows. Section 2 presents our data and Section 3 discusses our empirical method- ology. Our empirical findings are reported and discussed in Section 4. The final section highlights policy implica- tions of the results and provides suggestions for future research. 2. Data To investigate the determinants of Chinese firms’ choice of adopting eco-label and ISO 14001 standard, we con- ducted a firm-level survey in China in 2008. Detailed face-to-face interviews were conducted at 270 firms, which were chosen to represent China’s manufacturing industry in a set of categories defined by sector, size class and ownership structure. The majority of the inter- views were focused on Yangtze Delta Area, which con- sists of Shanghai, Zhejiang Province, Jiangsu Province, and Anhui Province, to represent its strong economic performance in China in recent years.2 As shown in Ta- ble 1, the number of firms from this area is 196, making up 72.59% of the sample. In our view, the sample is well balanced among 13 sector categories based on the study of [16]. They are 37 firms in the chemicals sector, 30 in the food and bever- age sector, 57 in the machinery, equipment and instru- ments sector, 21 in the metal processing and products sector, 16 in the nonmetal products sector, 19 in the tex- tile, apparel and leather products sector, 15 in the timber, furniture, and paper products sector, 14 in the medical products sector, 10 in the rubber and plastic products sector, 9 in the electric power sector, 7 in the automobile and related products sector, 4 in the petroleum processing and coking sector, and 31 in other sectors of manufac- turing industry. The firms are also evenly distributed along the size scale, with roughly similar numbers in large, medium, and small classes. Size classes are de- fined by employment ranges, with small firms employing 10 - 199 employees, medium about 200 - 1000 employ- es and large more than 1000 employees. About 40% in e 2The GDP share of the Yangtze Delta Area over the whole country is about 25.45% in 2006, while the population share is about 15.56% [21]. Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? Copyright © 2011 SciRes. JSSM 382 Table 1. Summary of the sample. Characteristics n % Characteristics n % Sector Ownership Chemicals 37 13.70 State-owned 48 17.78 Electric power 9 3.33 Collective-owned 13 4.81 Food and beverage 30 11.11 Private-owned 107 39.63 Machinery and instruments 57 21.11 Foreign 49 18.15 Medical products 14 5.19 Joint-venture 53 19.63 Metal processing and products 21 7.78 Automobile and related products 7 2.59 Has eco-labeled products Nonmetal products 16 5.93 Yes 69 25.56 Petroleum processing/coking 4 1.48 No 201 74.44 Rubber and plastic products 10 3.70 Textiles and leather products 19 7.04 Has ISO 14001 certification Timber, furniture, and paper 15 5.56 Yes 77 28.52 Other sectors 31 11.40 No 193 71.48 Area Total revenue in 2007 Shanghai 123 45.55 <10 million RMB 33 11.11 Zhejiang 22 8.15 10 - 30 million RMB 36 13.33 Jiangsu 31 11.48 30 - 60 million RMB 32 11.85 Anhui 20 7.41 60 - 100 million RMB 29 10.74 Other provinces 74 27.41 100 - 200 million RMB 26 9.63 200 - 500 million RMB 32 11.85 Listed firm on the stock market 500 - 1000 million RMB 26 9.63 Yes 63 23.33 >1000 million RMB 43 15.93 No 207 76.67 No answer 11 4.07 Number of the employees Number of the rivals <200 98 36.30 <10 95 35.19 200 - 1000 89 32.96 11 - 19 76 28.15 >1000 83 30.74 >20 99 36.67 Total 270 100.00 Total 270 100.00 the sample is private-owned, while the numbers of state- owned, foreign-owned, and joint-venture firms are roughly the same. In addition, 23.33% of firms are pub- licly traded in the two stock markets in China (Shanghai Stock Exchange and Shenzhen Stock Exchange). 259 firms answered their annual sales amount in the year of 2007 in our designated ranges, with roughly. similar share in each category.3 reported that they had at least one eco-labeled product and 77 firms have already certified the ISO 14001. The number of firms with both certification is 23, accounting for 8.52% of the sample. As for the reasons of the eco-label certification given by those firms with eco-labeled products, 73.91% (51 firms out of 69) concurred that products with the eco- label certification would be more easily accepted by consumers, while 40.58% admitted that they did so be- cause of the government regulation. In addition, there were 52.17% of the firms with the eco-label certification reported that they regarded eco-labeling as a strategy for promoting the firm’s prestige, and 57.97% answered that In the interview, we asked the respondent whether the firm has any eco-labeled products and whether the firm has the certification of ISO 14001 standard. 69 firms 3The purpose to ask firms to report their annual sales amount in ranges instead of in amounts is to avoid possible complaints.  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes?383 obtaining an eco-label is to demonstrate the effort for environmental protection made by the firms. The last reason that the certification fee for eco-labeling is not so high was cited by 15.94% of the sample. With resp ect to the reasons of ISO 14001 certification, 60 of the 77 firms reported that their purpose was to reduce production costs, 63 of the 77 firms admitted that they wanted to reduce the environmental load caused by their production, and 63 of the 77 firms stated that their purpose was to raise their staffs’ environmental consciousness. Addi- tionally, 54.55% of the firms with the ISO 14001 certifi- cation reported that implementing ISO 14001 manage- ment system would help them communicate with outside more easily, 75.32% answered that they did so to in- crease the firm’s credibility, and 62.34% said that their purpose was to upgrade the firm’s prestige. Finally, the number of the firms that cited other reasons (e.g., as a combination with other management systems, etc.) was 11, making up 14.29% of the ISO 14001 certified firms. 3. Methodology This paper seeks to identify the factors that induce the certifications of eco-label and/or ISO 14001. The firm’s decision to choose to certify is described by the follow- ing latent variable models. * Ecolabelii Xi (1) * ISO 14001e ii X i (2) where and denote whether a firm has eco-labeled products and whether a firm has ISO 14001 certification, respectively. Ecolabel ISO 14001 represents a matrix of explanatory variables capturing the factors that may affect the certification decision of a firm (see more detailed descriptions of these factors in Table 2). and are coefficients matrix of . represents each firm, and 1,2,3,4,,2i70 and represent the error terms in Equations (1) and (2), respectively. The vari- ables marked with asterisks in the equations are latent variables. They are linked to the observed variables in the following way. e 1a firm has eco-label ed products Ecolabel 0otherwise i (3) 1a firm has ISO 14001 certification ISO 140010otherwise i (4) The above model can be estimated using a binary pro- bit model if we assume the error terms in Equations (1) and (2) follow the standard normal distribution. It is im- portant to note that the parameters of the model, like those of any nonlinear regression model, are not the mar- ginal effects we are accustomed to analyzing. The com- putation of the marginal effect of a continuous variable in a probit model is performed in the following way. [Ecolabel/ ]() EX X X (5) [ISO 14001/]() EX X X (6) where () is the standard normal density. In this case, the marginal effects are usually evaluated at the sample means of the data. Furthermore, another complication for computing the marginal effect in a binary probit model arises because will often include dummy variables, as the case in this study. The com putation of the m arginal effect (ME) of a dummy variable can be done in the fol- lowing way. (1) (0) MEP(Ecolabel 1|)P(Ecolabel 1|) dd xx (7) (1) (0) MEP(ISO 140011|)P(ISO 140011|) dd xx (8) where is a dummy variable and d()d denotes the means of all the other variables in the model. 4. Results Tables 3 and 4 present results from a probit model of the factors associated with eco-label and ISO 14001 certifi- cations. The robust standard errors of the coefficients are reported in the tables. In addition, we also calculate the marginal effects according to Equations (5)-(8) and re- port the results in Table 5. The detailed descriptions of the variables are provided in Table 2. 4.1. Eco-label Certification Table 3 indicates the existence of significant correlation s between the reasons of eco-label certification admitted by the firms and the certification decision in all cases (models (1-4)). It is important to note that the presented reasons provide different incentives. For example, Ac- cepted_consumer and Promotion_strategy are more likely related to firm’s economic incentive, while Envi- ronment_protection seems to reflect that firms have a strong motivation to take a pro-environment approach. Whatever the differences of these incentives are, the es- timated positive signs of these variables suggest that relative to the omitted reason (i.e., the certification fee for eco-labeling is not so high), a firm motivated by any of these reasons is more likely to choose eco-label certi- fication. Concerning the factor of ownership, Foreign_ owned and Joint_venture have significantly positive signs in all cases, suggesting that foreign capital partici- pation does have an important effect on the firm’s envi- onmental certification decision. This result may attest r Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? Copyright © 2011 SciRes. JSSM 384 Table 2. Definition of the variables. Variables Description Dependent variables Ecolabel = 1 if there is eco-labeled product in the firm ISO 14001 = 1 if the firm has ISO 14001 series certification Explanatory variables Accepted_consumer = 1 if the firm admits eco-labeled products are easily accepted by consumers Government_regulation = 1 if the firm admits eco-labeling is based on the government’s regulation Promotion_strategy = 1 if the firm regards eco-labeling as a strategy for promotion Environment_protection = 1 if the firm admits eco-labeling is an effort for environmental protection Cost_reduction = 1 if the firm admits ISO certification reduces production costs Environment_load = 1 if the firm admits ISO certification reduces environmental load caused Staff_consciousness = 1 if the firm admits ISO certification raises staffs’ environmental concern Promote_communication = 1 if the firm admits ISO certification promotes communications with outside Credibility_increasing = 1 if the firm admits ISO certification increases the firm’s credibility Prestige_upgrading = 1 if the firm admits ISO certification upgrades the firm’s prestige Foreign_owned = 1 if the firm is owned by foreign capitals Joint_venture = 1 if the firm is a joint-venture enterprise State_owned = 1 if the firm is a state owned enterprise Private_owned = 1 if the firm is owned by private sectors Other_enterprises = 1 if the main client of the firm is other enterprises Individual_consumer = 1 if the main client of the firm is individual consumers Government =1 if the main client of the firm is government Listed_enterprise = 1 if the firm is a listed enterprise on the stock exchange market Rivals Numbers of the rivals reported by the firm Foreign_market = 1 if the firm mainly sells its products overseas Firm_size Logarithm of the number of employees the firm has Chemicals = 1 if the firm belongs to chemical sector Electric power = 1 if the firm belongs to electric power sector Food & beverage = 1 if the firm belongs to food and beverage sector Machinery = 1 if the firm belongs to machinery, equipment and instruments sector Medical = 1 if the firm belongs to medical products sector Metal = 1 if the firm belongs to metal processing and products sector Automobile = 1 if the firm belongs to automobile and related products sector Nonmetal =1 if the firm belongs to nonmetal products sector Petroleum = 1 if the firm belongs to petroleum processing and coking sector Rubber & plastic = 1 if the firm belongs to rubber and plastic products sector Textiles & apparel & leather = 1 if the firm belongs to textiles, apparel and leather products sector Timber & furniture & paper = 1 if the firm belongs to timber, furniture and paper products sector that foreign owners are more eager to increase environ- mental protection initiatives to secure to prevent dis- crimination or increase their legitimacy in the eyes of these authorities.4 In addition, the results show that the characteristics of firms’ client (i.e, other enterprises, in- dividual consumers, and government) do not affect their decisions on certifying eco-label. Other firm characteristics appear to have a strong im- pact as well, although the factor that a firm is listed on he stock exchange is not significant.5 As expected, the t  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes?385 Table 3. Factors that affect the eco-label certification (dependent variable: Ecolabel). (1) (2) (3) (4) Constant –1.933(0.177)*** –2.879(0.454)*** –5.538(0.976)*** –8.038(1.703)*** Reasons of certifying eco-label Accepted_consumer 1.399(0.343)*** 1.498(0.381)*** 1.978(0.467)*** 2.470(0.755)*** Government_regulation 1.572(0.520)*** 1.942(0.599)*** 1.904(0.849)** 1.672(0.793)** Promotion_strategy 0.698(0.389)* 1.001(0.438)** 1.531(0.698)** 1.754(0.869)** Environment_protection 0.786(0.364)** 0.705(0.392)* 1.303(0.658)** 1.248(0.599)** Ownership Foreign_owned - 1.292(0.482)*** 1.607(0.679)** 1.787(0.799)** Joint_venture - 1.252(0.484)** 2.283(0.692)*** 3.130(0.870)*** State_owned - 1.071(0.554)* 0.985(0.705) 1.239(0.897) Private_owned - 0.938(0.774) 1.434(0.767)* 1.155(0.918) Clients Other_enterprises - - –0.279(0.373) –0.736(0.591) Individual_consumer - - 0.171(0.351) 0.015(0.398) Government - - 0.746(0.432)* 0.264(0.658) Other firm characteristics Listed_enterprise - - 0.074(0.419) –0.319(0.496) Rivals - - 0.925(0.388)** 1.680(0.676)** Foreign_market - - 1.234(0.473)*** 1.139(0.533)** Firm_size - - 0.308(0.087)*** 0.435(0.124)*** Sector Chemicals - - - 0.242(0.835) Electric power - - - 1.257(1.176) Food & beverage - - - 1.962(0.933)** Machinery - - - 0.605(0.640) Medical - - - –0.137(0.738) Metal - - - 1.402(0.822)* Automobile - - - 1.975(0.856)** Nonmetal - - - 2.245(1.159)* Petroleum - - - 3.408(1.398)** Rubber & plastic - - - 1.762(0.887)** Textiles & apparel & leather - - - 0.762(0.539) Timber & furniture & paper - - - –0.433(0.719) Observations 270 270 270 270 Log likelihood –50.234 –44.139 –29.766 –23.499 Pseudo R2 0.608 0.655 0.663 0.725 Notes: ***, ** and * denote statistical significance at 1%, 5% and 10% levels, respectively. Numbers in parentheses are robust standard errors. number of rivals is positively correlated with the certifi- cation decision, indicating that the more bruising the competition a firm faces, the more likely it certifies eco- label to distinguish its product from others. Foreign_ market is positive and significant, suggesting that export- oriented firms are more inclined to have eco-label certi- fication. According to [11], this may occur because for- ign consumers tend to be less able to monitor the per- e Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? 386 Table 4. Factors that affect the ISO 14001 series certification (dependent variable: ISO14001) (1) (2) (3) (4) Constant –1.628(0.147)*** –2.081(0.289)*** –3.778(0.770)*** –4.424(1.054)*** Reasons of certifying ISO 14001 Cost_reduction 1.138(0.434)*** 1.295(0.459)*** 1.949(0.618)*** 2.737(0.802)*** Environment_load 1.616(0.384)*** 1.512(0.413)*** 1.438(0.427)*** 3.414(0.748)*** Staff_consciousness 0.426(0.412) 0.331(0.451) 0.377(0.602) 0.626(0.943) Promote_communication –0.890(0.597) –1.953(0.618) –1.337(0.780) –2.151(0.983) Credibility_increasing 0.896(0.404)** 0.972(0.411)** 1.273(0.685)* 2.519(1.151)** Prestige_upgrading 1.251(0.651)* 1.368(0.707)* 1.493(0.769)* 1.501(0.765)** Ownership Foreign_owned - 1.033(0.372)*** 1.513(0.504)*** 2.726(0.686)*** Joint_venture - 0.640(0.358)* 0.845(0.480)* 1.436(0.790)** State_owned - 0.436(0.449) 0.321(0.716) 0.748(0.785) Private_owned - 0.308(0.651) 0.509(0.758) 1.055(1.160) Clients Other_enterprises - - 0.538(0.515) 1.044(0.603)* Individual_consumer - - 1.010(0.386)*** 2.079(0.503)*** Government - - 1.162(0.444)*** 1.739(0.516)*** Other firm characteristics Listed_enterprise - - 0.428(0.327) 0.109(0.426) Rivals - - 1.255(0.372)*** 2.524(0.509)*** Foreign_market - - 0.624(0.348)* 1.647(0.520)*** Firm_size - - 0.289(0.111)*** 0.259(0.131)** Sector Chemicals - - - 2.766(1.052)*** Electric power - - - 4.920(1.810)*** Food & beverage - - - –1.522(1.206) Machinery - - - –0.581(0.641) Medical - - - 2.523(1.312)* Metal - - - 0.085(0.609) Automobile - - - 1.938(1.012) Nonmetal - - - –2.245(2.054) Petroleum - - - 2.175(0.824)*** Rubber & plastic - - - 3.811(1.287)*** Textiles & apparel & leather - - - –0.411(0.525) Timber & furniture & paper - - - –1.066(1.265) Observations 270 270 270 270 Log likelihood –53.696 –49.694 –28.395 –19.568 Pseudo R2 0.655 0.681 0.795 0.856 Notes: ***, ** and * denote statistical significance at 1%, 5% and 10% levels, respectively. Numbers in parentheses are robust standard errors. formance of the facility or firm, as a result, more visible signs of environmental commitment such as having a certified eco-label may legitimize their reason for doing business with the firm. In addition, there is a significantly Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes?387 Table 5. Marginal effects of the factors on the eco-label and ISO 14001 series certifications. Eco-label certification ISO14001 certification Reasons of certifying eco-label Accepted_consumer 0.168*** - Government_regulation 0.070*** - Promotion_strategy 0.067* - Environment_protection 0.025** - Reasons of certifying ISO 14001 Cost_reduction - 0.687*** Environment_load - 0.701*** Staff_consciousness - 0.068 Promote_communication - –0.080 Credibility_increasing - 0.545** Prestige_upgrading - 0.263* Ownership Foreign_owned 0.062** 0.696*** Joint_venture 0.219** 0.196* State_owned 0.022 0.171 Private_owned 0.016 0.185 Clients Other_enterprises –0.005 0.059* Individual_consumer 0.000 0.332*** Government 0.001 0.378*** Other firm characteristics Listed_enterprise –0.001 0.009 Rivals 0.085** 0.266*** Foreign_market 0.015** 0.165** Firm_size 0.005*** 0.021** Sector Chemicals 0.001 0.078** Electric power 0.032 0.082* Food & beverage 0.090** –0.052 Machinery 0.004 –0.029 Medical –0.001 0.049* Metal 0.037* 0.000 Automobile 0.137* 0.038 Nonmetal 0.164** –0.052 Petroleum 0.625** 0.049** Rubber & plastic 0.083* 0.051** Textiles & apparel & leather 0.002 –0.005 Timber & furniture & paper –0.001 –0.060 Notes: ***, ** and * denote statistical significance at 1%, 5% and 10% levels, respectively. positive correlation between the certification decision and firm size that is described by the logarithm of the number of employees.6 This result may be plausible be- cause larger firms usually enjoy economies of scale in Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? 388 implementing certification. Finally, sector effect on the decision of eco-label certification is presented in the re- sults. We find significant effect in six sectors (i.e., food and beverage, metal processing and products, automobile and related products, nonmetal products, petroleum processing and coking, and rubber and plastic products), and no significant effect in other sectors. 4.2. ISO 14001 Certification Table 4 presents several similar results as tho se in Table 3. Among the six designated reasons of certifying ISO 14001 management standard, four of them (i.e., Co st_ reduction, Environment_load, Credibility_increasing, and Prestige_upgrading) exhibit strong correlation with the certification decision, while there seem no significant effects of raising staffs’ environmental consciousness and promoting communications with outside on the deci- sion of ISO 14001 certification. It is again shown that foreign-owned and joint-venture enterprises are signifi- cantly more likely to implement ISO14001 certification. This result is consisten t with that of [17] that foreign and joint-venture firms behave better than the Chinese firms in environmental protection, but different from that of [11] suggesting foreign ownership has no significant ef- fect on Japanese firms’ decision of ISO14001 certifica- tion. The ISO 14001 certificatio n is, as expected, signifi- cantly and positively correlated with the number of rivals and foreign market orientation. In addition, same as that in the certification of eco-label, there seems also to have economies of scale in the ISO 14001 certification proc- esses because of the significantly positive sign of Firm_ size, which is consistent with the results in [5] and [11] that larger firms are more likely to undertake voluntary environmental actions. Several different results between the eco-label and ISO 14001 certifications are found in the following determi- nants. First, the characteristics of firms’ client are impor- tant in the case of ISO 14001. Firms targeting at individ- ual consumers and/or government are more likely to cer- tify ISO 14001. In addition, Other_enterprises becomes significant at 10% level if sector dummies are controlled in the model (see the last column in Table 4). Further- more, firms belonging to the sectors of petroleum proc- essing and coking or rubber and plastic products are more willing to certify ISO 14001, which is the same as those in the eco-label case. However, four significant sector dummies (i.e., Food & beverage, Metal, Automo- bile, and Nonmetal) are no longer significant in the ISO 14001 case. Instead, firms in the sectors of chemical, electric power, and medical products are more likely to undertake the ISO 14001 certification. 4.3. Marginal Effects 4In comparison to our explanation, another view explained by [11]is that foreign owners may be less willing to contribute to the social well- eing of the country in which the facility is located and, as a result less inclined to invest in environmental protection above the level o required regulation. However, our results do not support this point o view. This may occur because in comparison to the case in Japan, a large share of the products produced by most foreign-owned and oin -venture firms in China is directly exported abroad. Consequently, the characteristics of their products including the pro-environmental factor should meet what foreign consumers require. 5Whether a firm is listed on a stock exchange is used to proxy share- holder pressure here. According to [1], the pressures that shareholders exert over a firm arise as a result of discontent with environmental fines which lower profits, and disillusionment with progress toward envi- ronmental goals and with difficulties in raising new capital or attracting new investors due to poor environmental performance. Therefore, they ostulated that firms that are listed on a stock exchange are more likely to feel such pressures and, as a result, be more likely to intensify thei environmental initiatives in order to gain favor with or maintain their relations with shareholders. However, our results do not support thei ostulation in both eco-label and ISO 14001 certification decisions (see the variable of Listed_enterprise in Tables 3 and 4). In our view, a ossible explanation is that relative to the environmental performances of the listed firms, most of Chinese investors in the stock market pay much more attention to the revenues and profits of the firms. Therefore, as a result, unlike their foreign counterparts, the listed firms in China may not feel so much pressure of environmental issues from the share- holders. 6We dropped the variable related to a firm’s annual sales amount that could also be considered to proxy firm size in our final estimation. This manipulation is based on two considerations. First, the high correlation between a firm’s annual sales amount and the number of employees (0.623) may cause a possible multicollinearity problem. Second, this variable is not significant in both cases of eco-label and ISO 14001 even we dropped the variable of number of employees in the model. The estimated marginal effects of each determinant of the eco-label and ISO 14001 certifications are summa- rized in Table 5. From the table, we can see that among the reasons explaining both certifications, Accepted_ consumer has the highest marginal effect on the prob- ability of choosing to certify eco-label, while Environ- ment_load and Cost_reduction are the two largest effects in the ISO 14001 certificatio n. It may be plausib le for the former because eco-label is usually regarded as the sym- bol of presenting the product’s pro-environment charac- teristics to consumers. In other words, whether or not the product with the label can be accepted by consumers is a crucial incentive for a firm choosing to seek eco-label certification. In contrast, since ISO 14001 is an interna- tional voluntary standard for environmental management systems, firms’ decision to undertake the certification of it normally depends on how strong their incentives in raising the level of the environmental management are. Consequently, it is not surprising that trying to mitigate the environmen tal load caused by the firms and reducing their production cost become the largest two factors in- fluencing the ISO 14001 certification decision. Some determinants affect more the ISO 14001 certifi- cation decision than those in the eco-label case. For ex- ample, the effect of foreign-owned firm on the ISO 14001 certification decision (i.e., 0.696 ) is approx imately Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes?389 10 times larger than that on the eco-label certification (i.e., 0.062). The similar result is also found in the factor of foreign market orientation. The marginal effect of the variable foreign_market on the ISO 14001 certification is 0.165, which is exactly 10 times larger than 0.015 in the eco-label case. These findings may be explained by the fact that ISO 14001 is more of an international standard, while the eco-label is a Chinese certificate. So firms with international elements tend to adopt more of the ISO 14001 certification. In Addition, there is no big differ- ence between the effects of joint-venture firm on the choice probabilities of both certifications (0.219 in the eco-label case vs. 0.196 in the ISO 14001 case). Al- though the factor of firms’ main clients is not significant in the eco-label case, individual consumer and govern- ment orientations affect similarly on the probability of undertaking the ISO 14001 certification, both of which are larger than that of Other_enterprises. Furthermore, the effects of the number of rivals and firm size on choice probability of the ISO 14001 certification are, respectively, about 3 times and 4 times as those in the eco-label case. With regards to the effect of those significant sector dummies on the certification decision, we find a big dif- ference in the eco-label case. The ratios of the probab ility of certifying eco-label by firms in petroleum processing and coking sector to those firms in other sectors are ap- proximately 4 for Petroleum vs Nonmetal and Automo- bile, 7 for Petroleum vs Food & beverage, and 17 for Petroleum vs Metal, respectively. In comparison to these large ratios, the differences in the ISO 14001 case are almost negligible. 5. Conclusions Empirical investigation on the determinants of imple- menting voluntary environmental schemes at the plant level is scarce in China. To sh ade more light on this sub- ject, we conducted a firm-level survey and apply the data to study the factors influencing Chinese firms’ decision to conduct the ISO 14001 and/or China Environmental Label certifications. Our results exhibit several similar evidences between the factors affecting the decisions of these two certifications. First, in comparison to their Chinese counterparts, foreign-owned and joint-venture firms are more likely to use the certifications. Second, the number of rivals a firm has is positively correlated to its decision on the certifications. Third, foreign market oriented firms are more willing to implement the certifi- cations. Fourth, firm size defined by the number of em- ployees a firm has plays a significant role in determining its choice of different certifications. Fifth, firms in the sectors of petroleum processing and coking or rubber and plastic products are more likely to certify both ISO 14001 standard and eco-label. Sixth, whether or not a firm is listed on a stock exchange is not a significant factor in both cases. Besides the above mentioned simi- larities, it is important to emphasize that we also find a number of differences in the determinants of these two certifications. First, the factor of a firm’s main client sig- nificantly affects the decision of the ISO 14001 certifica- tion, but not in the eco-label case. Second, sector effect on a firm’s certification decision is different in the certi- fications of ISO 14001 and eco-label. Finally, except for the sector effect, other determinants influencing the ISO 14001 certification have higher marginal effects than those corresponding factors affecting the eco-label certi- fication. Despite the potential problem such that our sample size may not be large enough to ensure robust estimates, our results presented in this paper have a number of in- teresting policy implications for Chinese decision makers. First, government policy makers can benefit from the fact that the decisions of firms choosing to implement volun- tary environmental schemes are influenced by the above specified reasons other than regulation. Consequently, government can provide incentives based on these rea- sons to promote voluntary action and pollution preven- tion as an alternativ e to mandatory environmental regu la- tions. By offering appropriate incentives, programs such as ISO 14001 and China Environmental Label can bring win-win benefits to firms, consumers, and government. Second, recognizing that various characteristics of firms affect their decision makings in undertaking voluntary environmental programs can help government design more flexible policies than traditional regulatio ns such as tax and command-and-control mandates. Third, ac- knowledging that firms in different sectors have different underling motivations in certifying ISO 14001 and/or eco-label, Chinese government may form specified envi- ronmental policies based on sector specifications, which as a result could be more effective than the current un- differentiated policies in China. Finally, the present study is sugg estive of two areas for further research. First, it should be noted that the results and findings are based on firms mostly located in the Yangtze Delta Area. Therefore, future studies may in- clude firms in other areas of China, which in turn could help to ensure the validity of these findings. Second, various financial data other than annual sales amount, which may also be important in determining firms’ deci- sion of implementing voluntary environmental schemes, are not included in the present study due to the fact that most surveyed firms refused to reveal the information. We leave this issue as an open challenge and expect a greater effort to overcome it in follow up studies. Copyright © 2011 SciRes. JSSM  What Determines Chinese Firms’ Decision on Implementing Voluntary Environmental Schemes? Copyright © 2011 SciRes. JSSM 390 REFERENCES [1] I. Henriques and P. Sadorsky, “Environmental Manage- ment Systems and Practices: An International Perspec- tive,” In: N. Johnstone, Ed., Environmental Policy and Corporate Behavior, Edward Elgar Publishing, Northamp- ton, USA, 2007, pp. 34-87. [2] ISO, “The Integrated Use of Management System Stan- dards,” International Standards Organization, 2008. [3] J. Shen and T. Saijo, “Does Energy Efficiency Label Alter Consumers’ Purchase Decision? A Latent Class Approach on Shanghai Data,” Journal of Environmental Management, Vol. 90, No. 11, 2009, pp. 3561-3573. doi:10.1016/j.jenvman.2009.06.010 [4] R. Starkey, “Standardization of Environmental Manage- ment Systems: ISO 14001, ISO 14004 and EMAS,” In: R. Welford, Ed., Corporate Environmental Management 1: Systems and Strategies, 2nd Edition, Earthscan, London, 1998, pp. 61-89. [5] S. Arora and T. Cason, “An Experiment in Voluntary Environmental Regulation: Participation in EPA’s 33/50 Program,” Journal of Environmental Economics and Ma- nagement, Vol. 28, No. 3, 1995, pp. 271-286. doi:10.1006/jeem.1995.1018 [6] W. B. Gray and M. E. Deily, “Compliance and Enforce- ment: Air Pollution Regulation in the US Steel Industry,” Journal of Environmental Economics and Management, Vol. 31, No. 1, 1996, pp. 96-111. doi:10.1006/jeem.1996.0034 [7] E. Helland, “The Enforcement of Pollution Control Laws: Inspections, Violations, and Self-Reporting,” The Review of Economics and Statistics, Vol. 80, No. 1, 1998, pp. 141-153. doi:10.1162/003465398557249 [8] S. Dasgupta, B. Laplante, N. Mamingi and H. Wang, “Inspections, Pollution Prices, and Environmental Perfor- mance: Evidence from China,” Ecological Economics, Vol. 36, No. 3, 2001, pp. 487-498. doi:10.1016/S0921-8009(00)00249-4 [9] L. Gangadharan, “Environmental Compliance by Firms in the Manufacturing Sector in Mexico,” Ecological Econo- mics, Vol. 59, No. 4, 2006, pp. 477-486. doi:10.1016/j.ecolecon.2005.10.023 [10] M. Khanna, “Non-Mandatory Approaches to Environmen- tal Prot e ct i on, ” Journal of Economic Surveys, Vol. 15, No. 3, 2001, pp. 291-324. doi:10.1111/1467-6419.00141 [11] M. Nakamura, T. Taka hashi and I. Vertinsky , “Why Ja pa- nese Firms Choose to Certify: A Study of Managerial Responses to Environmental Issues,” Journal of Environ- mental Economics and Management, Vol. 42, No. 1, 2001, pp. 23-52. doi:10.1006/jeem.2000.1148 [12] S. B. Brunnermeier and M. A. Cohen, “Determinants of Environmental Innovation in US Manufacturing Indus- tries,” Journal of Environmental Economics and Manage- ment, Vol. 45, No. 2, 2003, pp. 278-293. doi:10.1016/S0095-0696(02)00058-X [13] H. Wang, N. Mamingi, B. Laplante and S. Dasgupta, “Incomplete Enforcement of Pollution Regulation: Bar- gaining Power of Chinese Factories,” Environmental and Resource Economics, Vol. 24, No. 3, 2003, pp. 245-262. doi:10.1023/A:1022936506398 [14] S. J. DeCanio and W. E. Watkins, “Investment in Energy Efficiency: Do the Characteristics of Firms Matter?” The Review of Economics and Statistics, Vol. 80, No. 1, 1998, pp. 95-107. doi:10.1162/003465398557366 [15] H. Wang and D. “Wheeler, Financial Incentives and Endogenous Enforcement in China’s Pollution Levy System,” Journal of Environmental Economics and Ma- nagement, Vol. 49, No. 1, 2005, pp. 174-196. doi:10.1016/j.jeem.2004.02.004 [16] K. Fisher-Vanden, G. H. Jefferson, J. Ma and J. Xu, “Technology Development and Energy Productivity in China,” Energy Economics, Vol. 28, No. 5-6, 2006, pp. 690-705. doi:10.1016/j.eneco.2006.05.006 [17] H. Wang and Y. Jin, “Industrial Ownership and Environ- mental Performance: Evidence from China,” Environ- mental and Resource Economics, Vol. 36, No. 3, 2007, pp. 255-273. [18] N. Mamingi, S. Dasgupta, B. Laplante and J. H. Hong, “Understanding Firms’ Environmental Performance: Does News Matter?” Environmental Economics and Policy Studies, Vol. 9, No. 2, 2008, pp. 67-79. [19] S. Gupta and B. Goldar, “Do Stock Markets Penalize Environment-Unfriendly Behaviour? Evidence from India,” Ecological Economics, Vol. 52, No. 1, 2005, pp. 81-95. doi:10.1016/j.ecolecon.2004.06.011 [20] K. Elsayed and D. Paton, “The Impact of Environmental Performance on Firm Performance: Static and Dynamic Panel Data Evidence,” Structural Change and Economic Dynamics, Vol. 16, No. 3, 2005, pp. 395-412. doi:10.1016/j.strueco.2004.04.004 [21] National Bureau of Statistics of China, “China Statistical Yearbook,” Beijing, 2007.

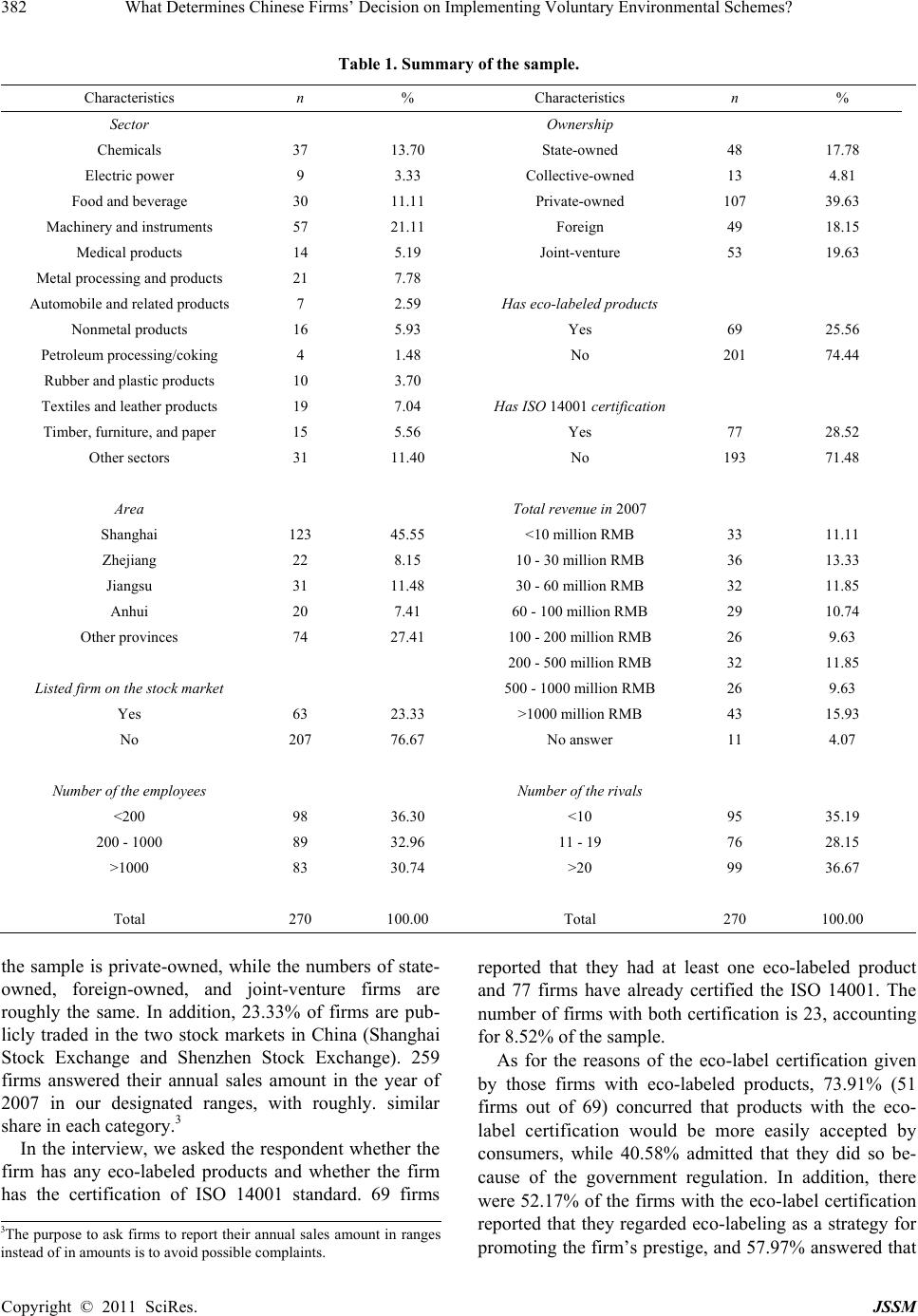

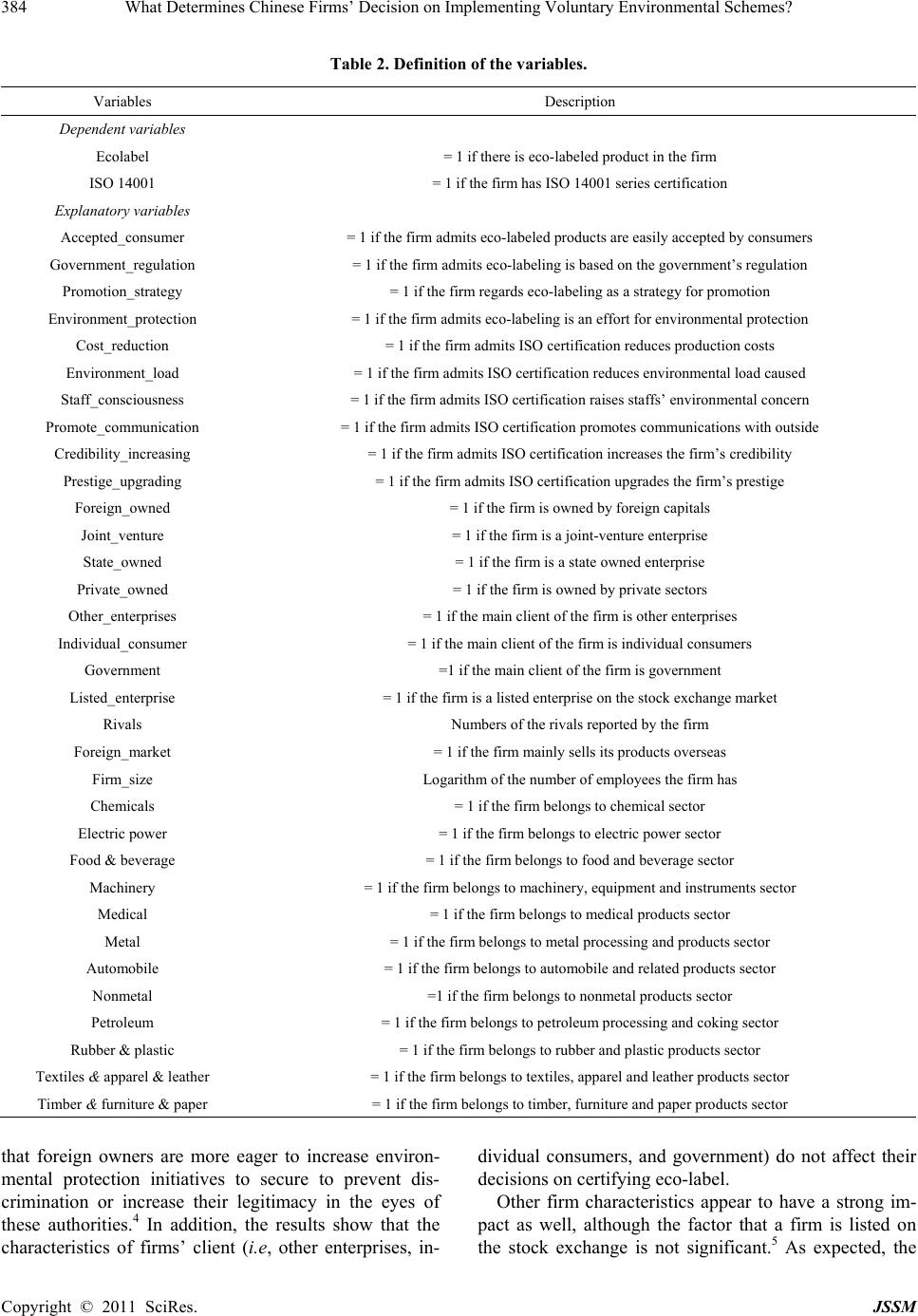

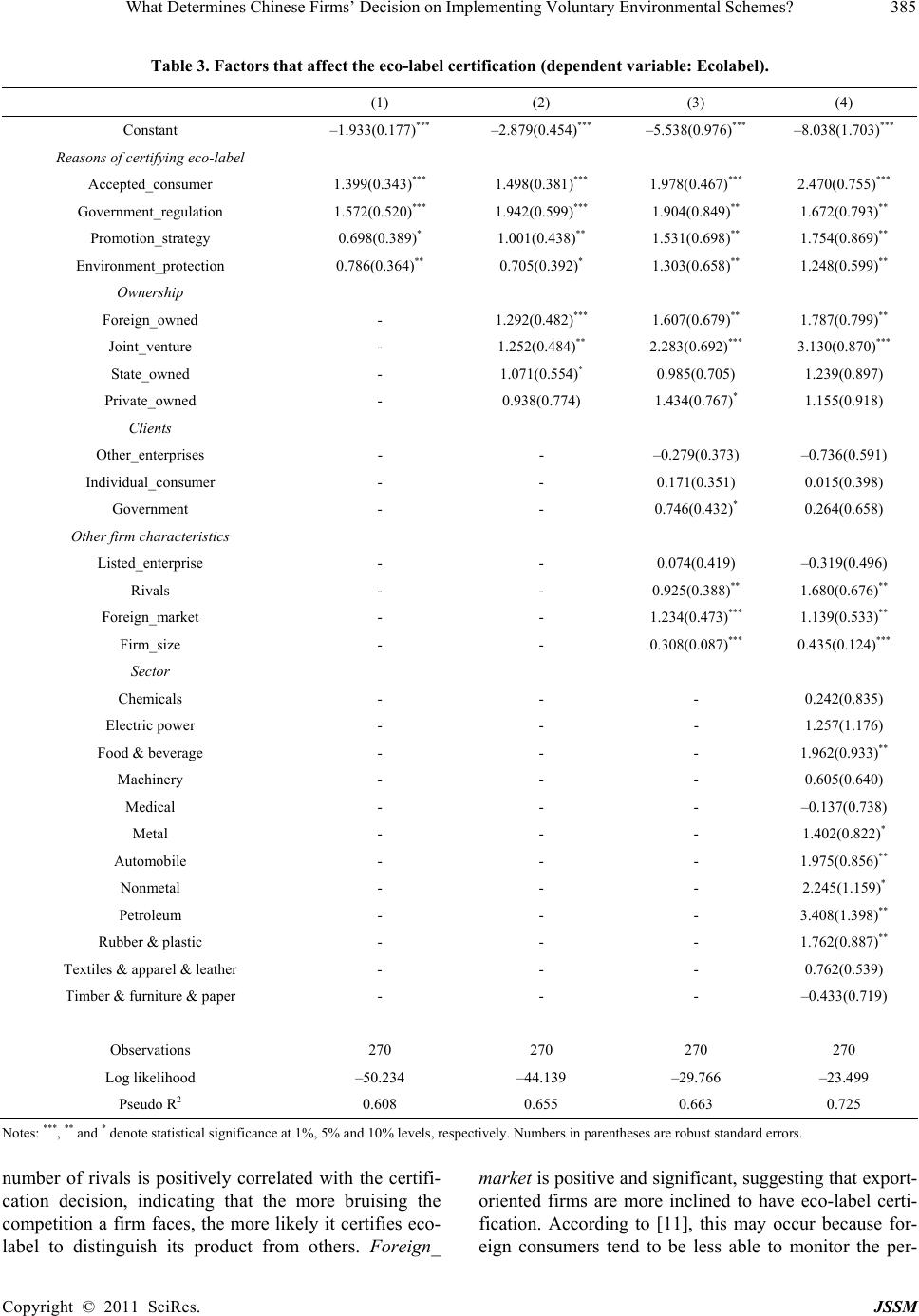

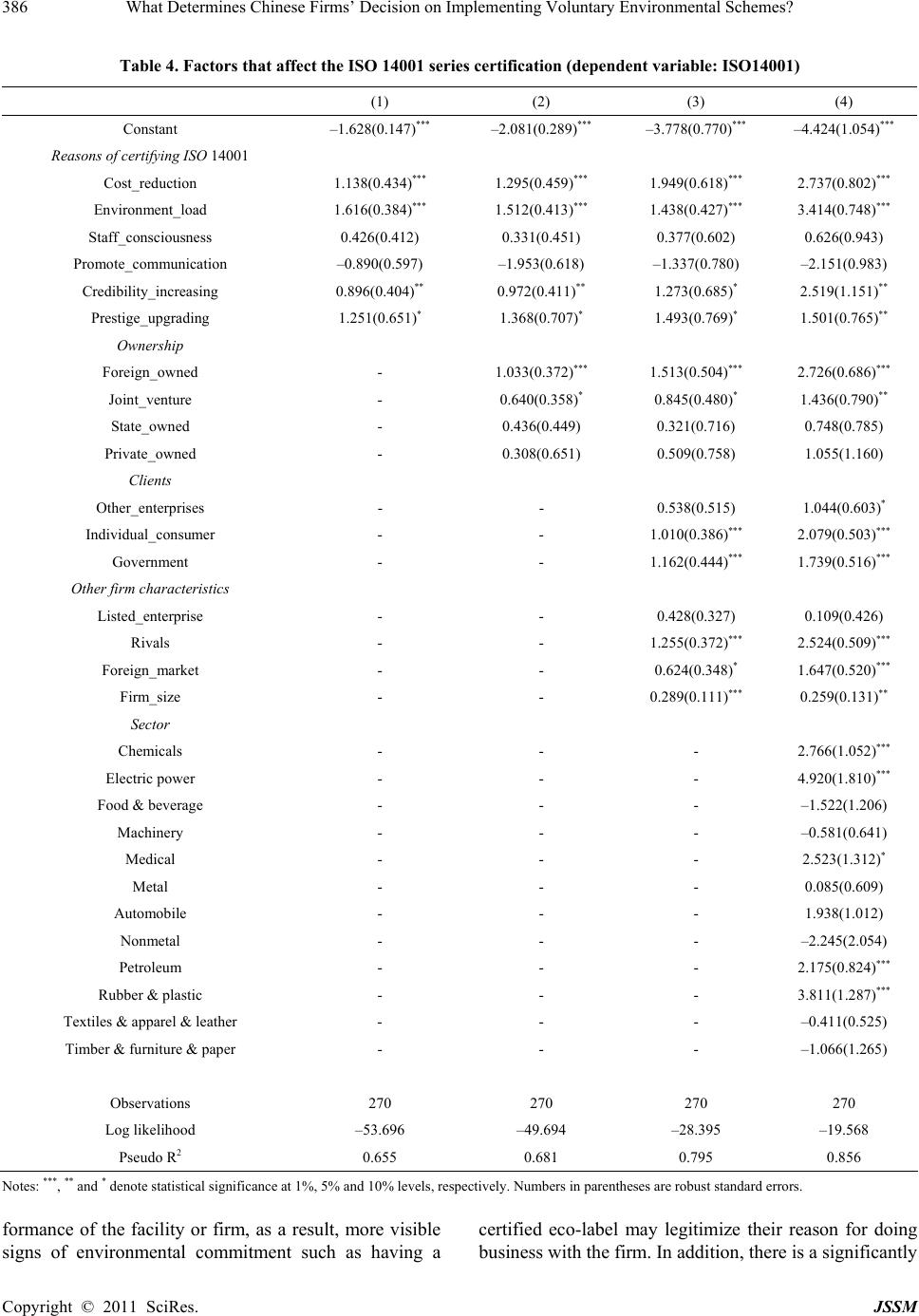

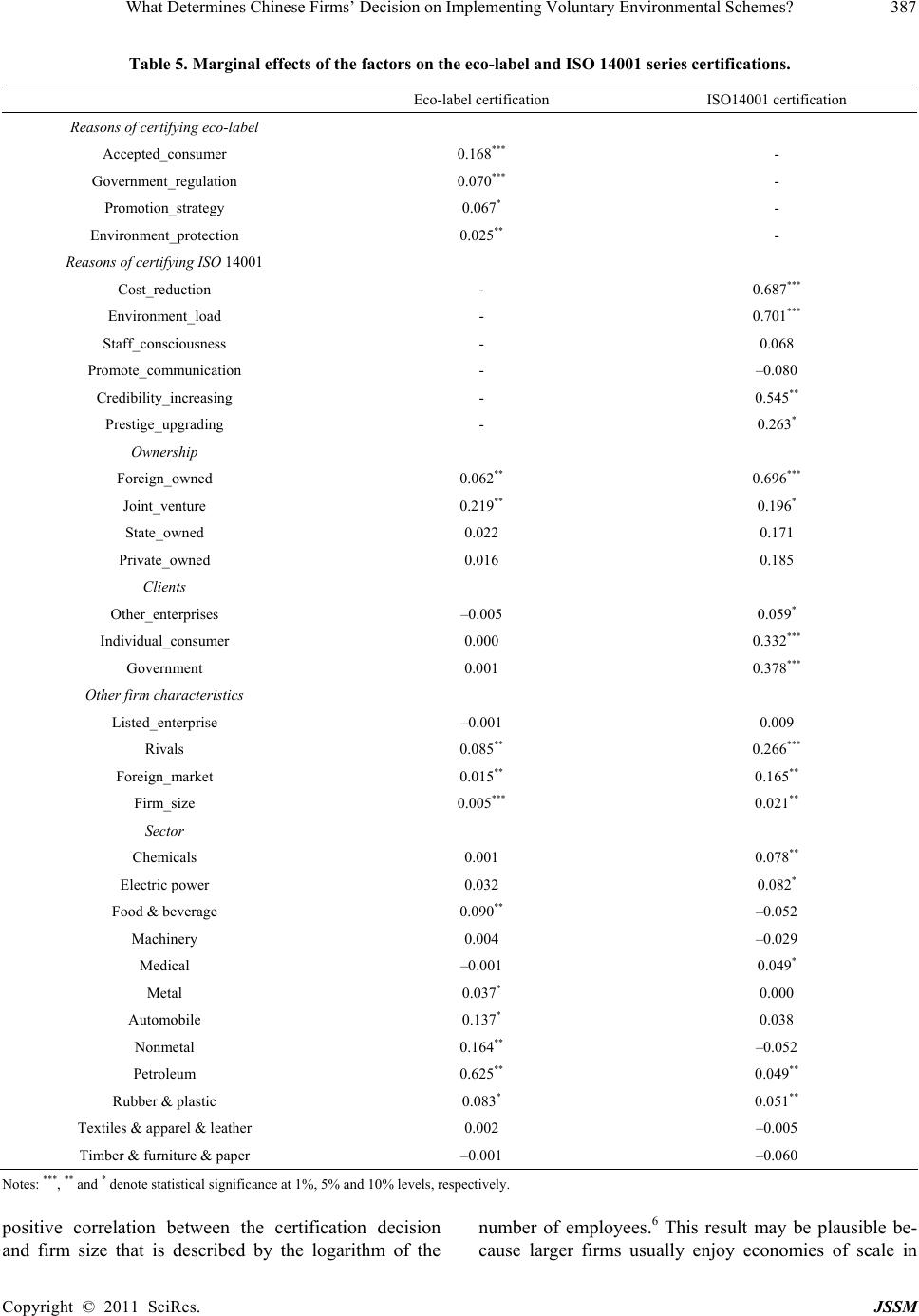

|