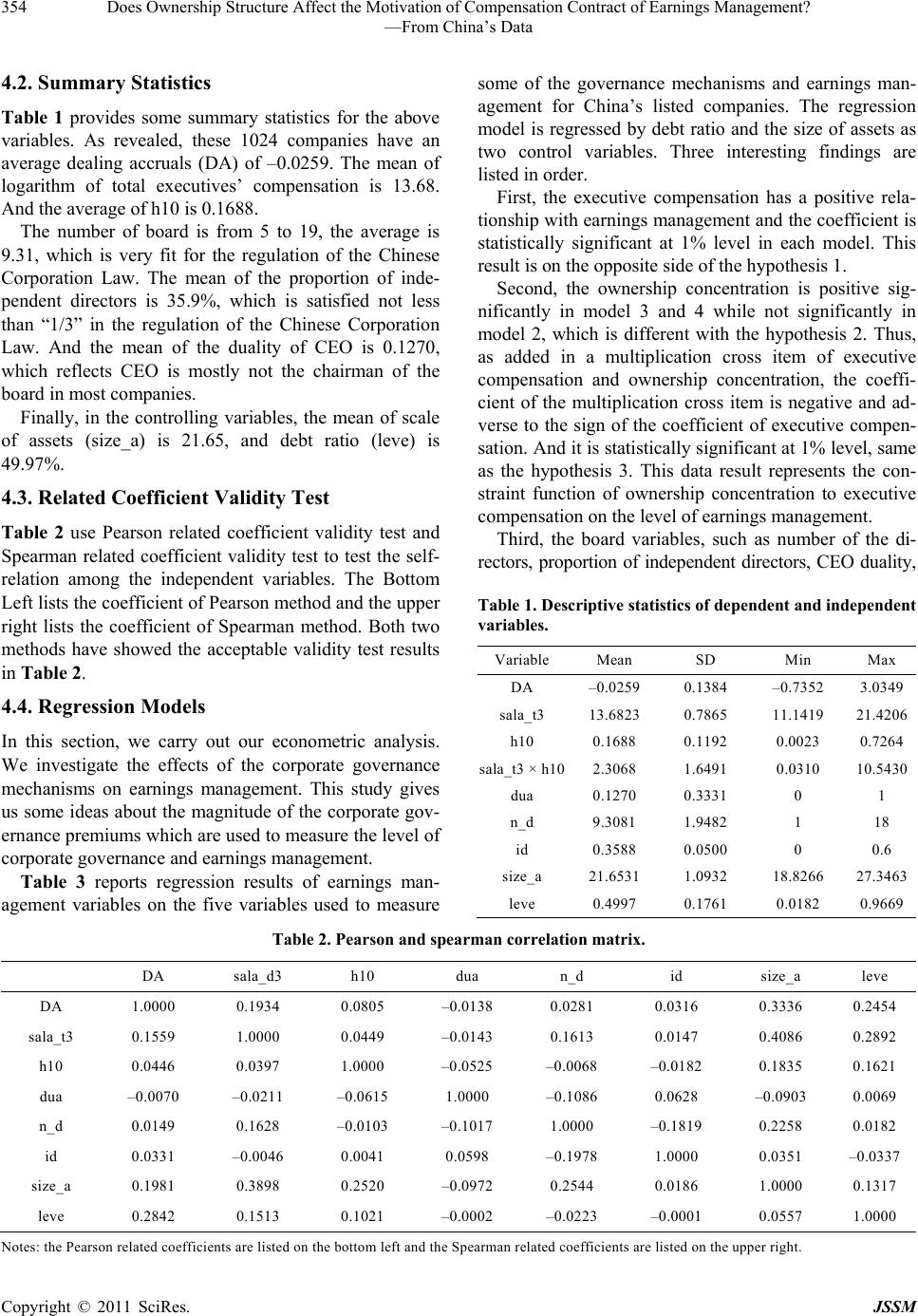

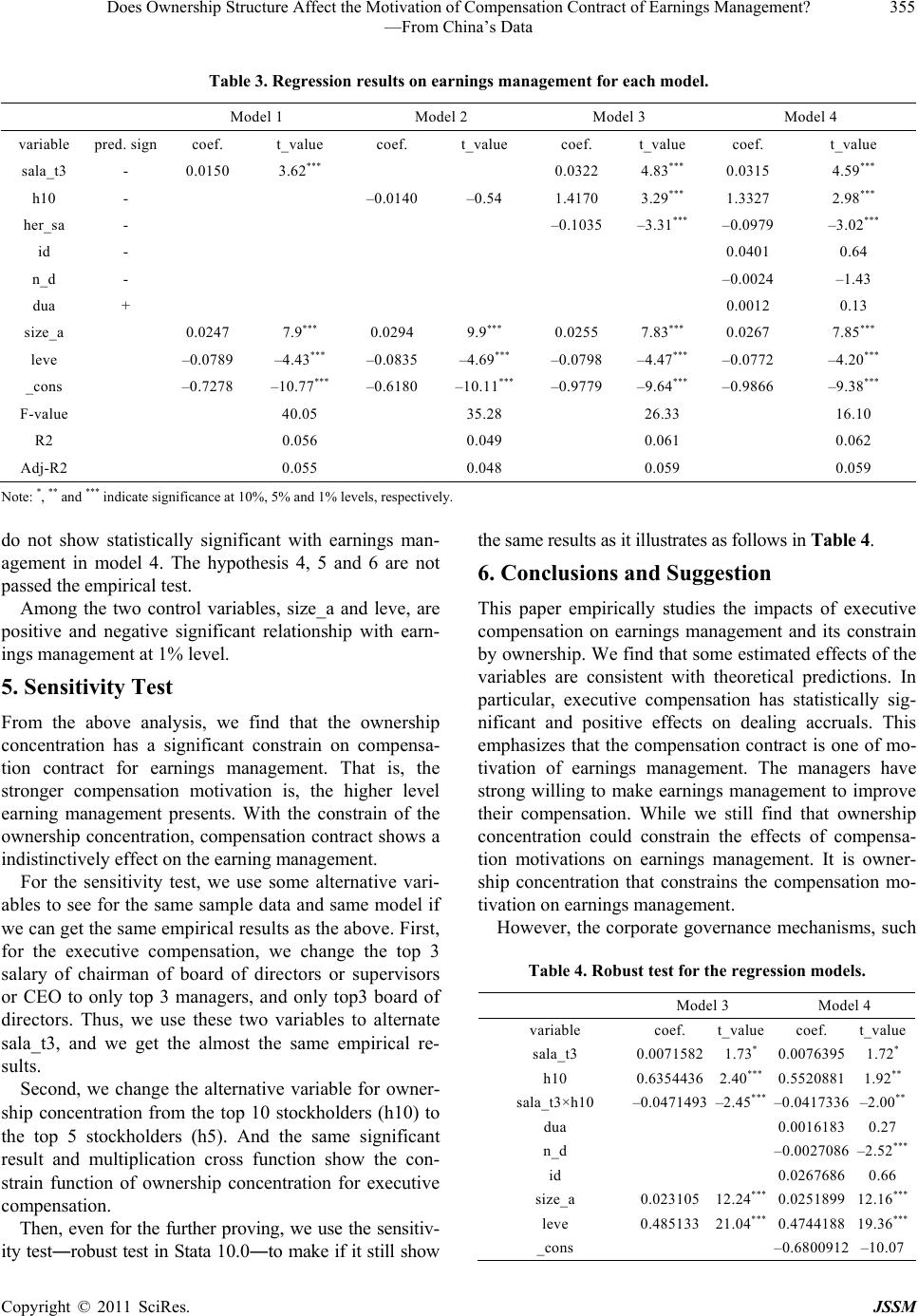

Does Ownership Structure Affect the Motivation of Compensation Contract of Earnings Management?

356

—From China’s Data

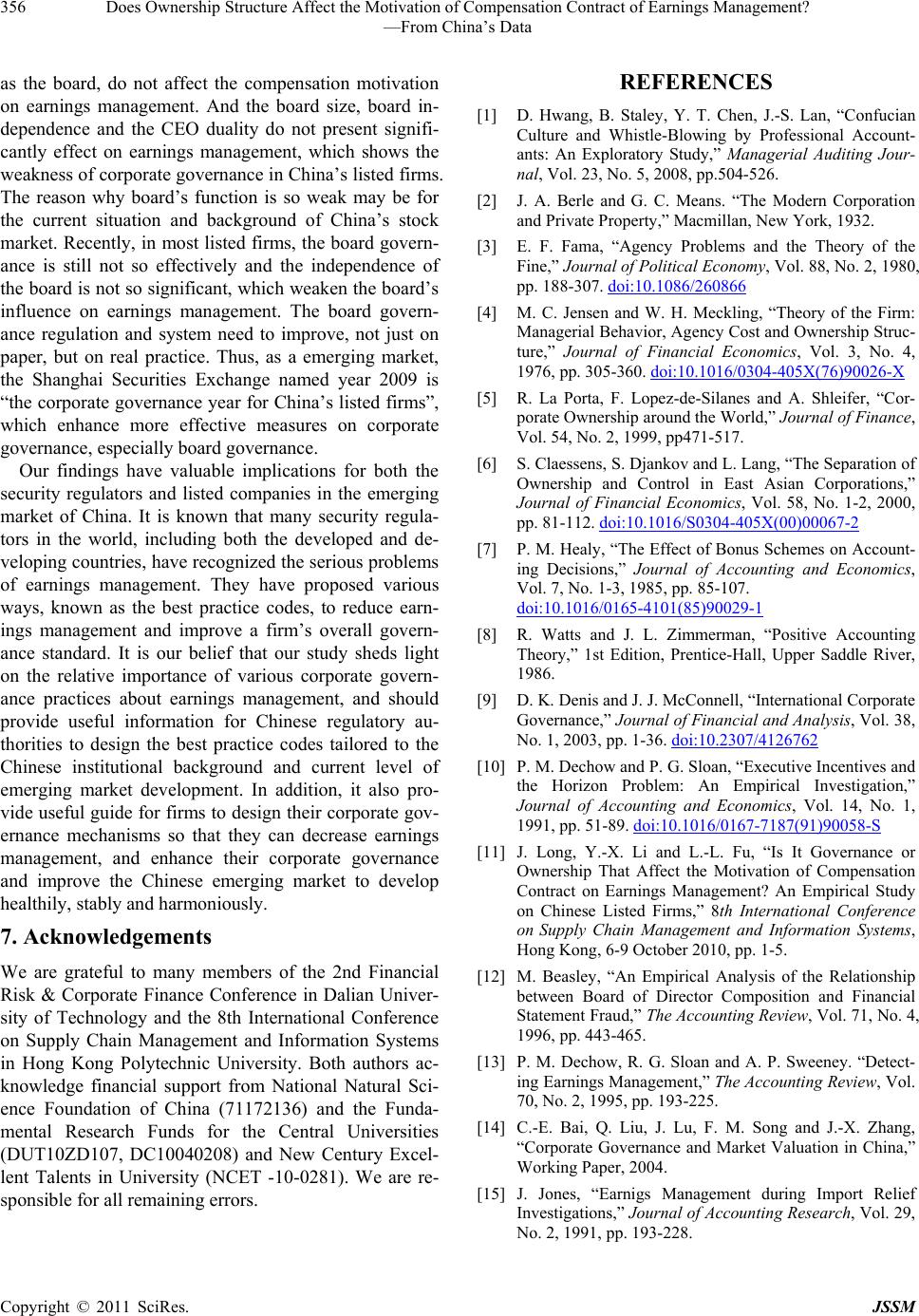

as the board, do not affect the compensation motivation

on earnings management. And the board size, board in-

dependence and the CEO duality do not present signifi-

cantly effect on earnings management, which shows the

weakness of corporate governance in China’s listed firms.

The reason why board’s function is so weak may be for

the current situation and background of China’s stock

market. Recently, in most listed firms, the board govern-

ance is still not so effectively and the independence of

the board is not so significant, which weaken the board’s

influence on earnings management. The board govern-

ance regulation and system need to improve, not just on

paper, but on real practice. Thus, as a emerging market,

the Shanghai Securities Exchange named year 2009 is

“the corporate governance year for China’s listed firms”,

which enhance more effective measures on corporate

governance, especially board governance.

Our findings have valuable implications for both the

security regulators and listed companies in the emerging

market of China. It is known that many security regula-

tors in the world, including both the developed and de-

veloping countries, have recognized the serious problems

of earnings management. They have proposed various

ways, known as the best practice codes, to reduce earn-

ings management and improve a firm’s overall govern-

ance standard. It is our belief that our study sheds light

on the relative importance of various corporate govern-

ance practices about earnings management, and should

provide useful information for Chinese regulatory au-

thorities to design the best practice codes tailored to the

Chinese institutional background and current level of

emerging market development. In addition, it also pro-

vide useful guide for firms to design their corporate gov-

ernance mechanisms so that they can decrease earnings

management, and enhance their corporate governance

and improve the Chinese emerging market to develop

healthily, stably and harmoniously.

7. Acknowledgements

We are grateful to many members of the 2nd Financial

Risk & Corporate Finance Conference in Dalian Univer-

sity of Technology and the 8th International Conference

on Supply Chain Management and Information Systems

in Hong Kong Polytechnic University. Both authors ac-

knowledge financial support from National Natural Sci-

ence Foundation of China (71172136) and the Funda-

mental Research Funds for the Central Universities

(DUT10ZD107, DC10040208) and New Century Excel-

lent Talents in University (NCET -10-0281). We are re-

sponsible for all remaining errors.

REFERENCES

[1] D. Hwang, B. Staley, Y. T. Chen, J.-S. Lan, “Confucian

Culture and Whistle-Blowing by Professional Account-

ants: An Exploratory Study,” Managerial Auditing Jour-

nal, Vol. 23, No. 5, 2008, pp.504-526.

[2] J. A. Berle and G. C. Means. “The Modern Corporation

and Private Property,” Macmillan, New York, 1932.

[3] E. F. Fama, “Agency Problems and the Theory of the

Fine,” Journal of Political Economy, Vol. 88, No. 2, 1980,

pp. 188-307. doi:10.1086/260866

[4] M. C. Jensen and W. H. Meckling, “Theory of the Firm:

Managerial Behavior, Agency Cost and Ownership Struc-

ture,” Journal of Financial Economics, Vol. 3, No. 4,

1976, pp. 305-360. doi:10.1016/0304-405X(76)90026-X

[5] R. La Porta, F. Lopez-de-Silanes and A. Shleifer, “Cor-

porate Ownership around the World,” Journal of Finance,

Vol. 54, No. 2, 1999, pp471-517.

[6] S. Claessens, S. Djankov and L. Lang, “The Separation of

Ownership and Control in East Asian Corporations,”

Journal of Financial Economics, Vol. 58, No. 1-2, 2000,

pp. 81-112. doi:10.1016/S0304-405X(00)00067-2

[7] P. M. Healy, “The Effect of Bonus Schemes on Account-

ing Decisions,” Journal of Accounting and Economics,

Vol. 7, No. 1-3, 1985, pp. 85-107.

doi:10.1016/0165-4101(85)90029-1

[8] R. Watts and J. L. Zimmerman, “Positive Accounting

Theory,” 1st Edition, Prentice-Hall, Upper Saddle River,

1986.

[9] D. K. Denis and J. J. McConnell, “International Corporate

Governance,” Journal of Financial and Analysis, Vol. 38,

No. 1, 2003, pp. 1-36. doi:10.2307/4126762

[10] P. M. Dechow and P. G. Sloan, “Executive Incentives and

the Horizon Problem: An Empirical Investigation,”

Journal of Accounting and Economics, Vol. 14, No. 1,

1991, pp. 51-89. doi:10.1016/0167-7187(91)90058-S

[11] J. Long, Y.-X. Li and L.-L. Fu, “Is It Governance or

Ownership That Affect the Motivation of Compensation

Contract on Earnings Management? An Empirical Study

on Chinese Listed Firms,” 8th International Conference

on Supply Chain Management and Information Systems,

Hong Kong, 6-9 October 2010, pp. 1-5.

[12] M. Beasley, “An Empirical Analysis of the Relationship

between Board of Director Composition and Financial

Statement Fraud,” The Accounting Review, Vol. 71, No. 4,

1996, pp. 443-465.

[13] P. M. Dechow, R. G. Sloan and A. P. Sweeney. “Detect-

ing Earnings Management,” The Accounting Review, Vol.

70, No. 2, 1995, pp. 193-225.

[14] C.-E. Bai, Q. Liu, J. Lu, F. M. Song and J.-X. Zhang,

“Corporate Governance and Market Valuation in China,”

Working Paper, 2004.

[15] J. Jones, “Earnigs Management during Import Relief

Investigations,” Journal of Accounting Research, Vol. 29,

No. 2, 1991, pp. 193-228.

Copyright © 2011 SciRes. JSSM