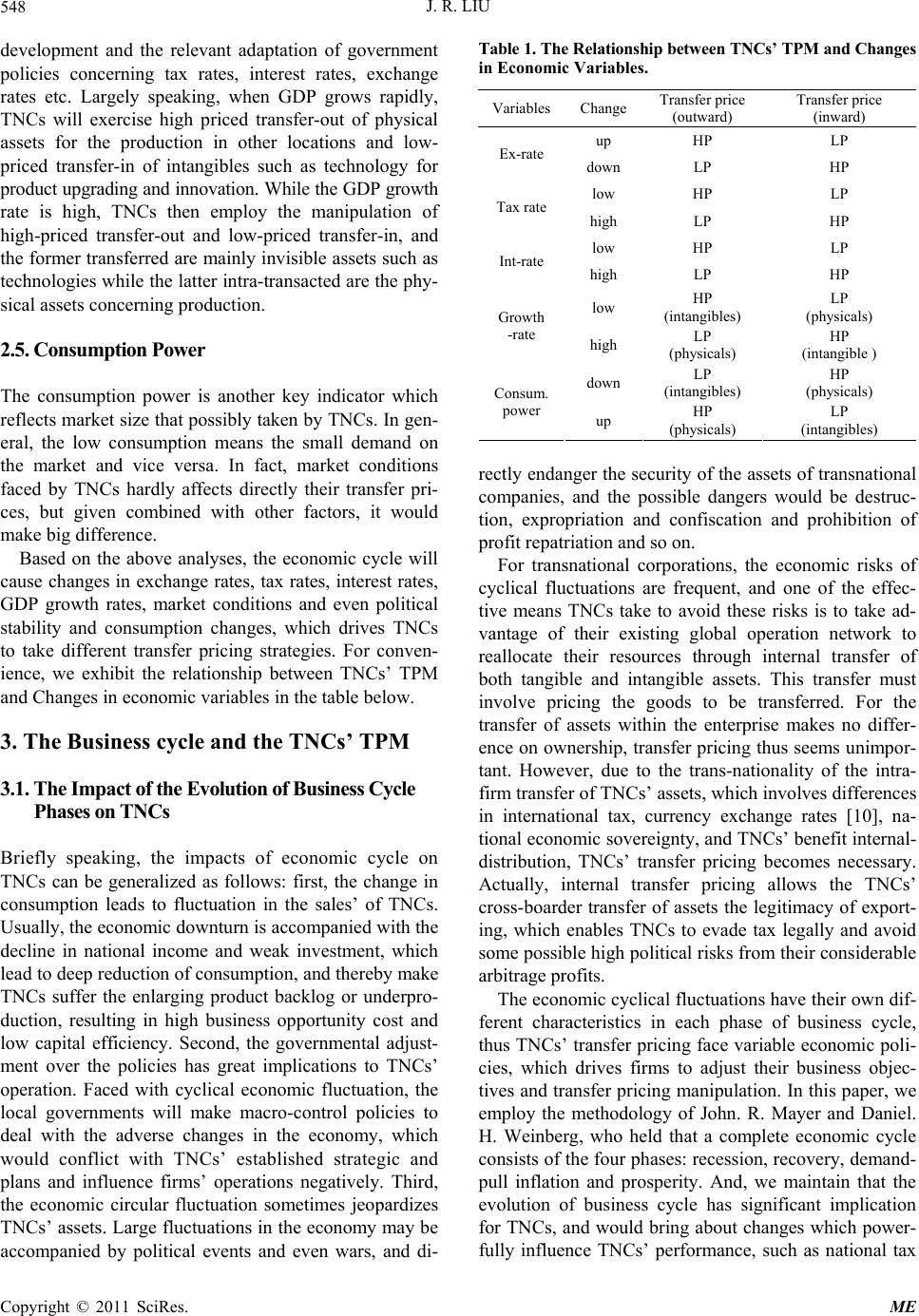

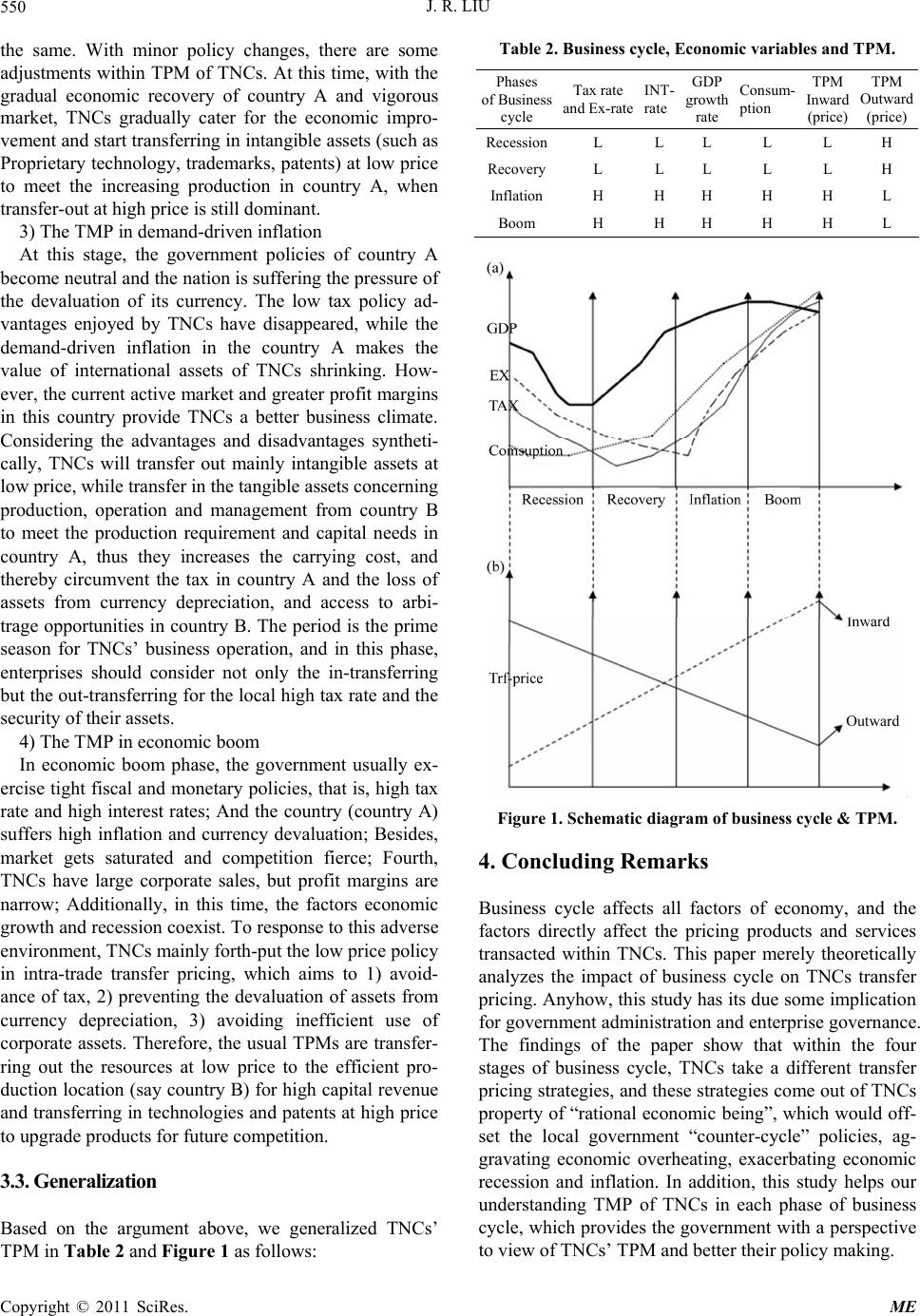

J. R. LIU549

policy change, the changes in exchange rates and interest

rates, the changes in, and as an unusual situation, the

risks over ownership of TNCs’ asset from political risks.

Before The analysis over the impacts of the four

phases on TNCs’ transfer pricing, we first make the fol-

lowing assumptions: First, the governments act on the

theories of business cycles; Second, the enterprises re-

spond to the outside environmental change and the ad-

justment in economic policies in accordance with the

“rational economic man” approach; Third, all countries

(say country A and country B) be at different phases of

business cycles; Fourth, national economic activity are

independent from the political ideology; Fifth, other fac-

tors within enterprises are fixed. The purpose of these

assumptions is to simplify our analysis, and in fact, these

assumptions are consistent with economic theories and

the traditional practice of g eneral economic activity.

1) Economic recession. In recession phase of business

cycle, the particular country (say country A) adopts loose

monetary and fiscal policies of economic expansion, say

lower interest rates, low tax rate and high governmental

transfer and so on. In the economic downturn phase, the

Government welcomes the entry of foreign capital, while

the outflow of assets and funds are under strict control;

At this time, tax rate decreased significantly, while the

country's currency is expected to appreciate; And the

difficulties faced with by TNCs are baggy consumption,

sluggish sales, rising inventories and underemployment.

2) Economic recovery. In this period, the country

(country A) will continue to maintain accommodative

monetary and fiscal policy, and hold the welcoming atti-

tude to foreign investment, but policy efforts are to be

weakened, and the market conditions faced by transna-

tional corporations continue to improve, sales increase,

and excess inventory decreases.

3) Demand-driven inflation. Because people’s demand

and investment are increasing, the economy grows rap-

idly, but the signs of inflation become clear for faint,

while the economy is still being steadily improved.

Meanwhile, the government policies turn neutral and

hence the preferential policies offered by government to

TNCs have gone. However, at this time, TNCs enjoy

better business climate with increasing product sales,

boosting corporate income and a gradual expansion of

production and larger market share. The only drawback

is that the cost of TNCs expresses a significant upward

trend, which further encourages th e inflation in the coun-

try, and change in exchange rate will makes TNCs suffer

losses in profit repatri a t i o n and from export.

4) Economic booming. With the further development

of the economy, the country (country A) entered the

boom phase of business cycle, with rapid production

promotion, investment scale-up, credit expansion, the

price level rising and increasing employment. Meanwhile,

consumer demand is climbing up and the market is in its

expansion. At this stage, the macroeconomic contains

two forces, that is, the power driving economy to grow

and the strength forcing the economy down-turning. In

the boom phase, the country (country A) mainly takes

tight monetary policies and fiscal policies to deal with

the economic overheating, and thereby the bank interest

rates rise, and corporate tax increase. The government

would manage the expectation of investment revenue to

control the total investment, thus preventing the econ-

omy from reducing to be of recession from excessive

expansion. In this phase, the government in short run

restricts the entry of foreign capital, while depreciation

of the currency lies under strong expectation, which

brings some detriment on TNCs in prof it repatriation and

exporting. And in spite of increasing corporate sales, due

to the rise of costs, TNCs’ actual profit would drop from

that of the previous phase, making TNCs lack for moti-

vation for business exp a nsion.

3.2. The TPM Employed in Each Phase

With the environment faced by the four stages pictured

above, TNCs will employ transfer pricing strategy ac-

cordingly in order to achieve reasonable tax avoidance,

and thus optimize the global resource allocation, corner

greater arbitrage opportunities and ensure the efficiency

of asset proliferation.

1) The TPM in recession

At this stage, due to underemployment and glissading

sales, TNCs will ship resources in a branch in a particu-

lar country (country A) to its sister branch in another

country (country B)to ensure the effective use of total

corporate resources. Country A in recession should take

low-tax policies to stimulate economic development,

whereby TNCs would transfer out at high-price to enjoy

the advantages o f low taxation ; Add itionally, becau se the

currency of country A are to appreciate, TNCs can corner

arbitrage opportunities for exchange rate fluctuation. For

TNCs in any country in recession, they are witnessing

the market shuff le and product upgrading, so they would

transfer out tangible assets concerning production, op-

eration and management through intra-trade channel, and

move into technologies at low prices to equip the new

production for the future market. Besides the transfer of

capital, TNCs can also take advantage of the loose mo-

netary polices to financing in country A and then transfer

the fund to country B, reducing corporate costs and en-

hancing asset utilization, harbor tax relief and interna-

tional arbitrage opportunities.

2) The TPM in recovery

In the economic recovery period, as TNCs face the

similar fiscal and monetary policy with that in economic

recession, their transfer pricing strategy is also roughly

Copyright © 2011 SciRes. ME