D. OLAYUNGBO ET AL543

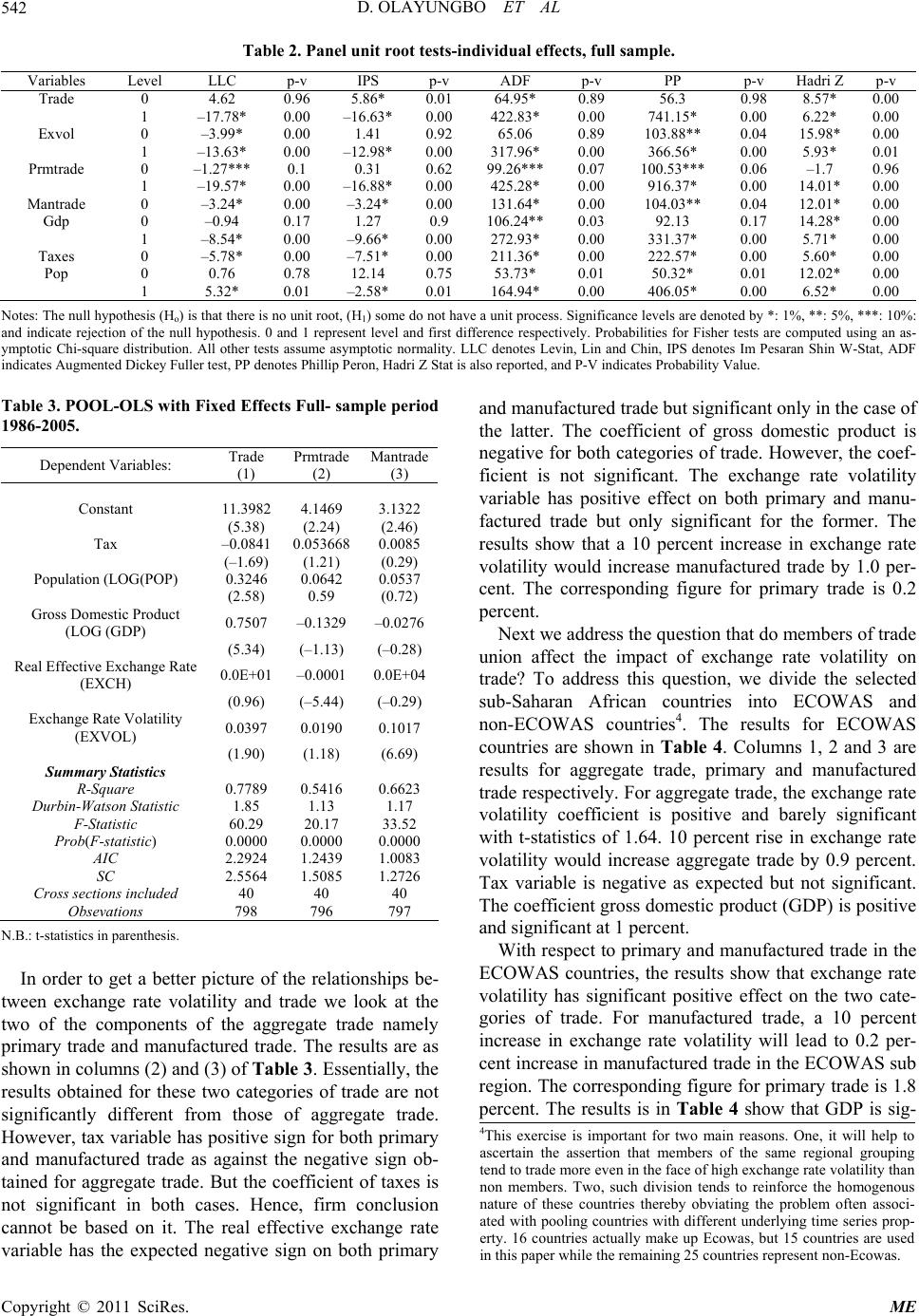

nificantly positively related to manufactured trade. The

reverse is the case with primary trade though the coeffi-

cient is not significant. Real effective exchange rate has a

significant negative effect on primary trade while the

coefficient is positive for manufactured trade though not

significant.

In the case of non-ECOWAS countries, the results for

aggregate, primary and manufactured trade are as shown

in columns 1, 2 and 3 of Table 4 respectively. The re-

sults in Table 4 for aggregate trade show that the ex-

change rate volatility variable is significantly positively

related to aggregate trade for non-ECOWAS countries.

The results indicate that a 10 percent increase in ex-

change rate volatility will lead to 0.3 percent increase in

aggregate trade in non-ECOWAS sub region.

The coefficient of tax is negative and significant. This

is means that an increase in taxes will lead to reduction

in aggregate trade in non ECOWAS sub region. Popula-

tion and gross domestic product both have significant

positive impact on aggregate trade in the non-ECOWAS

sub region.

With respect to primary and manufactured trade, the

results show that tax variable has positive impact on both

primary and manufactured trade though the coefficient is

only significant in the case of primary trade. In the same

way, population variable is positively related to both

primary and manufactured trade but only significant in

the latter. The coefficient of GDP is negative and sig-

nificant for both manufactured and primary trade. Real

effective exchange rate variable has negative impact on

the two categories of trade but only significant for pri-

mary trade. Finally, the coefficient of exchange rate is

positive for both primary and manufactured trade. The

variable is only significant in the case of manufactured

trade.

Further Consideration

The basic assumption behind Pooled Ordinary least

Square (POLS) results presented above is the exogeneity

of explanatory variables. However, when this assumption

is relaxed, the POLS breaks down. Therefore, relaxing

the assumption requires that we use another approach

capable of correcting biases introduced by including the

lagged dependent variable on the right hand side of the

equation. Therefore, a Generalized Method of Moments

(GMM) estimator in [13] approach was used to obtain

consistent estimates. Such panel techniques allow one to

control for endogeneity or simultaneity of some of the

explanatory variable in particular GMM estimators, as

well as for potential biases due to correlation between the

explanatory variables and the regression residual. More-

over, the use of GMM estimation technique provides the

robustness check for for the results obtained through the

pooled OLS technique. The panel GMM with fixed ef-

fects is performed on aggregate trade, primary product

and manufacturing product trade5. The results are pre-

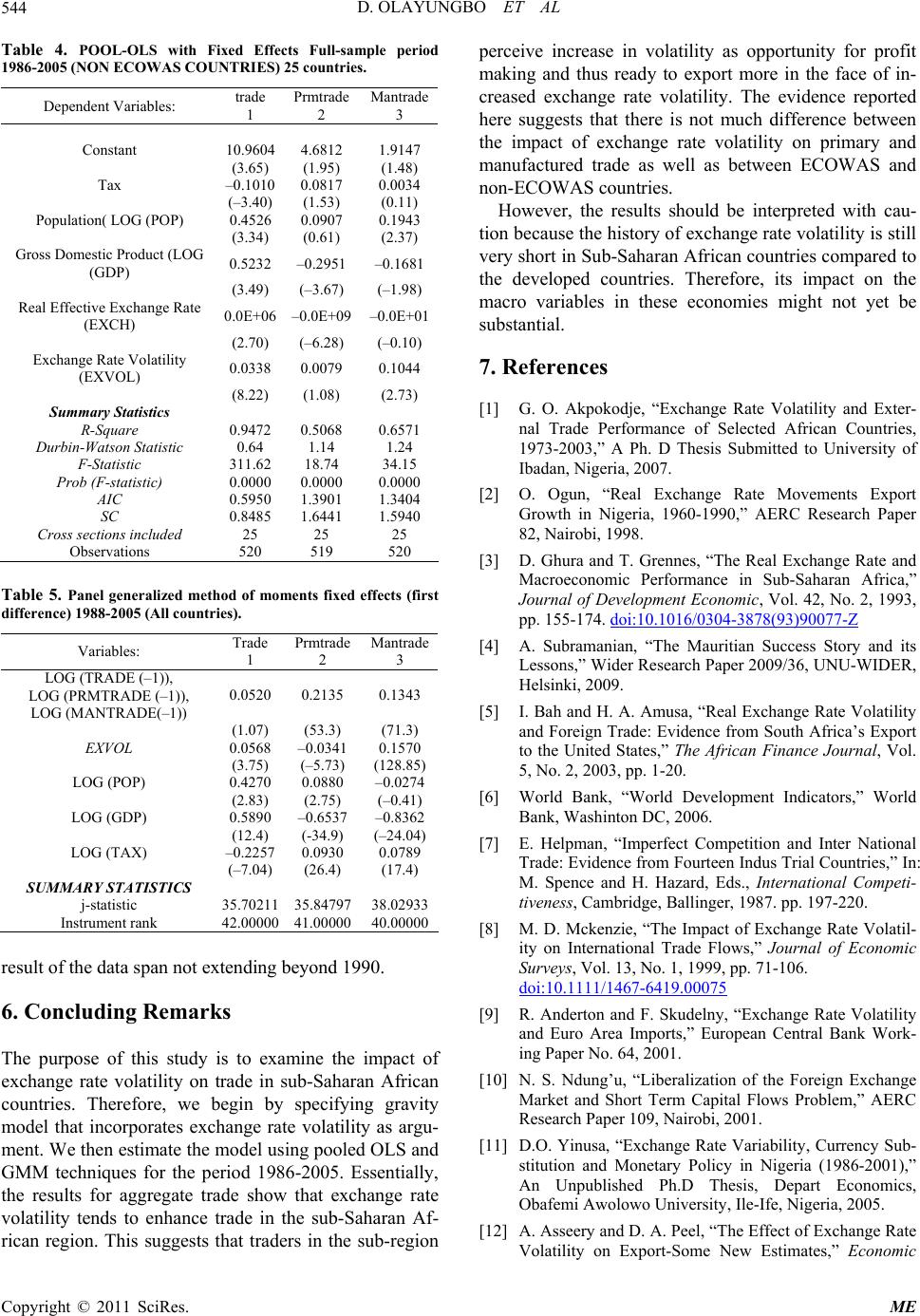

sented in Table 5.

Columns 1, 2 and 3 of Table 5 show the GMM results

for aggregate trade, primary and manufactured trade re-

spectively. Overall, the results from Generalized Method

of Moments (GMM) perform better considering the

j-statistics, instrument rank, significant t-statistics, and

the coefficients. With respect to aggregate trade from

Table 5 column 1, the coefficient of exchange rate vola-

tility is positive and significant. The results show that a

10 percent increase in exchange rate volatility would

increase trade by 0.6 percent. In the same way, the coef-

ficients of population and gross domestic product are

positive and significant. A 10 percent increase in GDP

would lead to 6 percent increase in aggregate trade. Tax

variable is negative and significant as expected. The re-

sults indicate that a 10 percent increase in taxes would

reduce aggregate trade in sub-Saharan Africa by 2 per-

cent.

As regards primary and manufactured trade, the results

show that exchange rate volatility has significant nega-

tive effect on primary trade while it has significant posi-

tive effect on manufactured trade. The results indicate

that increase in population would lead to increase in pri-

mary trade. The reverse is the case with manufactured

trade though the coefficient is not significant. The coef-

ficient of gross domestic product is negative and signifi-

cant for both primary and manufactured trade. The coef-

ficient of tax is positive and significant for both primary

and manufactured trade. A similar panel study carried

out by [3] between 1972-1987 on sub-Saharan Africa

reported a negative effects of exchange rate volatility on

trade. However, the estimation period was a period of

fixed exchange rate regime and this might have biased

the result. A Study conducted also by [2] analyzed the

effects of bilateral exchange rate movements in terms of

real effective exchange rate misalignment and volatility

on the growth of non-oil exports in Nigeria over the

1960-1990 periods. The findings of the study showed

that exporters in Nigeria are less risk averse and would

readily substitute other activities for exporting should

adverse movement in real exchange rate occur. Apart

from a single country study, the conclusion may be as a

5However, the reliability of the GMM estimator depends very much on

the reliability of the instruments. The validity of the instrument was

evaluated using the popular Sargan test [14]. The Sargan test is a test

on over-identifying restrictions by comparing both the j-statistic and

instrument rank. It is asymptotically distributed as χ2 and tests the null

hypothesis of validity of the (over-identifying) instruments. P-values

report the probability of incorrectly rejecting the null hypothesis, so

that a P-value above 0.05 implies that the probability of incorrectly

rejecting the null hypothesis above 0.05. In which case, a higher

P-value makes it more likely that the instruments are invalid. Our

P-values are generally lower than 5% with the value of 0.03, which

means that instruments used are valid.

Copyright © 2011 SciRes. ME