T. MAVRALEXAKIS ET AL.

Copyright © 2011 SciRes. JMF

36

assets are considered, Greek bonds used present a risky

class albeit of different nature from stocks. The bond

maturities used were capturing the most part of the yield

curve, and zero coupon were chosen so that the rein-

vestment coupon problem to be avoided.

Stocks with sufficient data history, which cover at

minimum the historical window, were grouped by their

national market and formed different data sets. The data

sets are the following: 1) 24 different time series of

stocks included in FTSE20 and FTSE40 Greek indexes;

2) 24 time series of stocks included in Dax30 Index; 3)

29 time series of stocks included in Dow 30 index and 4)

time series of ASE, Dax 30, Dow 30 indexes plus time

series of 10 years and 2 years Greek zero coupon bonds.

The formation of the objective function was based on

historical distribution and risk measures instead of risk

reward ratios (i.e. sharp ratios) were optimized. Keeping

the number of assumption to the minimum, rebalancing

frequencies, historical windows, risk measures, data

groups and short sales indicators were all variables to be

optimized during the credit crunch period.

During the credit crunch period rolling- window back-

-tests with a historical window of length H, and a holding

period of length F, were conducted. Overall, the time

evolution of 1440 different portfolios by using 4 histori-

cal windows, 9 rebalancing periods, 5 risk measures, 4

data groups and 2 short sales on/off indicators were

tested.

Each one of the different historical windows consid-

ered was of length 1 year, 2 years, 5 years and 10 years

and each one of the hold ing periods was of length 1 day,

1 week, 2 weeks, 1 month, 2 months, 3 months, 4 months,

5 months and 8 months.

Thus, at point in time 1

t, on data from 1

tH

to

11t, optimization is performed with the resulting port-

folio to be held until 21

ttF . At this point, a new

optimal portfolio is computed, using data from 2

tH

until 21t, and the existing portfolio is rebalanced. This

new portfolio is then held until 32

ttF and so on

and so forth until the end of the period. So during the

walk forward through the data, wealth trajectories are

computed optimizing each one of the above variables

considered and holding the others fixed. In order to per-

form the wealth trajectories through time, the initial port-

folio was set to contain only cash in amount of 100,000

EUR. No limits were imposed on the individual positions

i

. The optimal values for each of the above variables,

formed the selection criteria of the optimal portfolio to

be tested against indexing and equal weight strategies.

The software used for the computations was Matlab

R2007b. Optimizations were performed using sequential

quadratic programming methods (SQP), which transform

the constrained optimization problem into an easier sub-

problem that can then be solved and used as the basis of

an iterative process. Fmincon function capitalizes on this

method by solving the constrained problem using a se-

quence of parameterized quadratic programming uncon-

strained optimizations (more details about fmincon and

constraint non linear optimization exist in http://www.

mathworks.com).

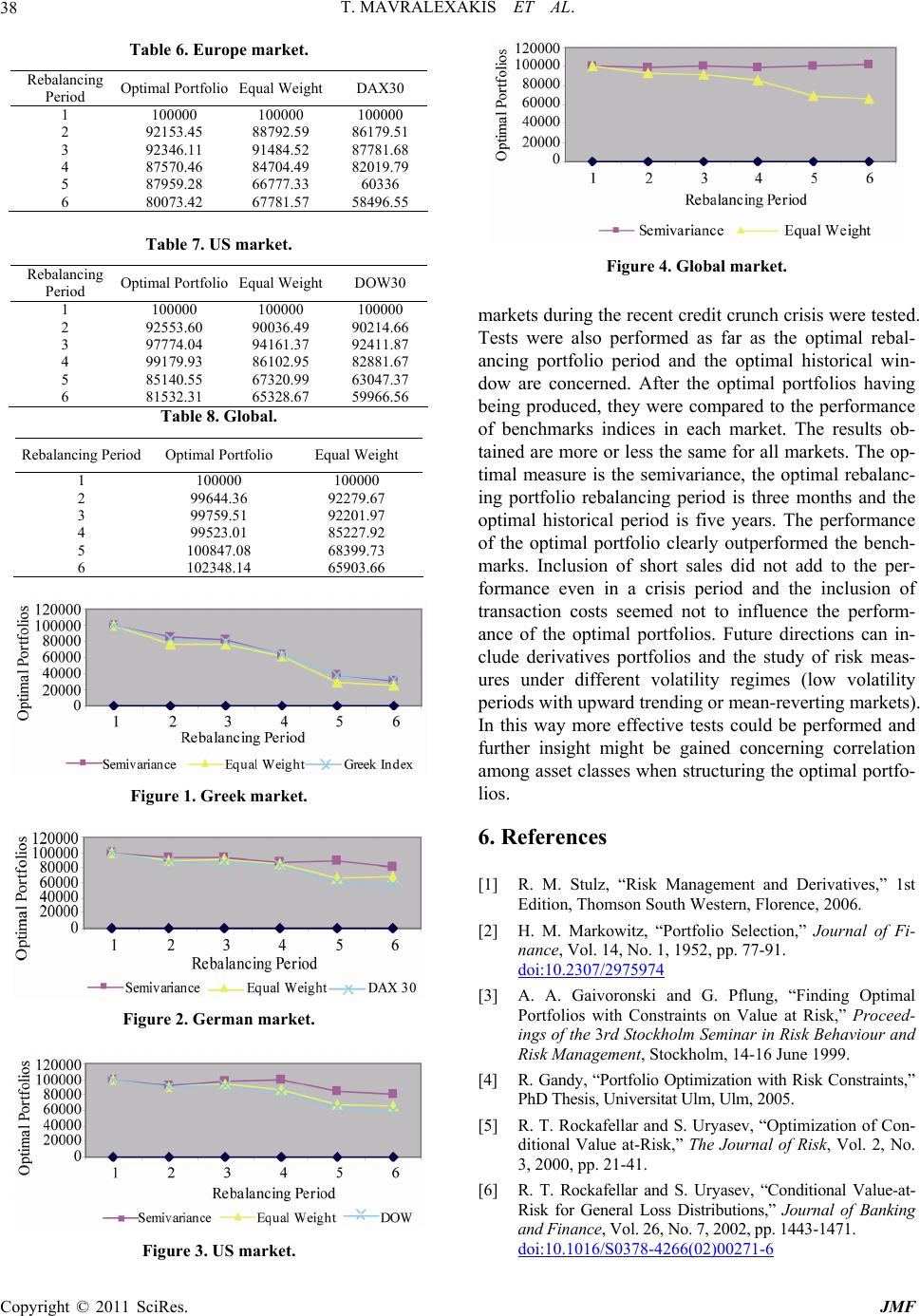

4. Results

4.1. Risk Measures Performance

Interesting results were drawn concerning the choice of

the optimal risk measure, the optimal rebalancing period,

the optimal historical window and the usage or not of

short sales. The main result from the comparison of the

risk measures was that portfolios constructed by mini-

mizing partial and conditional moments like SEMI and

ES performed better than those constructed by simply

minimizing variance. Furthermore, when considered con-

fidence levels for the ES methodology, the optimal level

was the 95% and not 90% or 99% confidence levels.

Table 1 summarizes the findings where for each risk

measure the average portfolio value and the average an-

nual percentage change was calculated.

Table 1 shows that for the different risk measures the

portfolios performances are very close to each other with

that of SEMI being the optimal.

These findings suggest that during high volatility pe-

riods, like the credit crunch crisis, the optimal risk meas-

ure selection does not play such a crucial role. Next

finding was relative to the rebalancing frequency of the

portfolios. If a portfolio is never rebalanced, it will

gradually drift from its target asset allocation to higher-

return, higher-risk assets. Compared to the target alloca-

tion, portfolio’s expected return increases, as does its

vulnerability to deviations from the return of the target

asset allocation. Therefore there is a trade-off between

risk of return deviation and expected return deviation.

This trade off accounts for the cost of rebalancing, which

in this study is set to 30 basis points for buy transactions

and 70 basis points for sell transactions. Optimizations

with no transaction costs were run and it was found that

transaction costs did not significantly influence the re-

Table 1. Risk measures.

Risk Measure Portfolio Value Change

Variance 71.32% –22.59%

ES99% 71.89% –22.12%

ES95% 72.55% –21.58%

ES90% 72.11% –21.94%

Semivariance 74.45% –20.03%