Open Journal of Social Sciences

Vol.04 No.05(2016), Article ID:66819,8 pages

10.4236/jss.2016.45001

The Mode Research of China’s Urban Land Assets Securitization

Lulu Chen1, Danyu Chen2

1College of Economics and Management, Hangzhou Normal University, Hangzhou, China

2The Director of Postgraduate Department, Hangzhou Normal University, Hangzhou, China

Copyright © 2016 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 25 March 2016; accepted 13 May 2016; published 16 May 2016

ABSTRACT

Urban land purchasing and reserving system is an innovation in urban land usage in china, despite several financial problems with it. Land securitization is the best choice for carrying out the urban land reserve system. In the framework of urban land purchasing and reserving system, the urban land securitization was divided into two subunits, land real assets securitization and land credit assets securitization, according to whether the assets are entity or not. According to the types of securities, the former includes land bonds, investment funds and land trust plan three modes, while the latter includes balance-in mode, balance-out mode, quasi-off-balance-sheet mode and off-shore four modes. Discussion the aforementioned operation modes lead to suggestions for improving urban land securitization.

Keywords:

Purchase and Reserve, Urban Land, Securitization, Modes

1. Introduction

China started urban land use system reform in 1987. It has initially established a new urban land usage system, which can not only maintain public ownership of land property, but also benefit the socialist marketing economy system after nearly 30-years long exploration. In addition, China has established a land purchasing and reserving system in 1996 [1] [2] to promote urban land utilization intensively, thus protect farmers arable land and unleash the land enterprise stock. Urban land purchasing and reserving system, also known as the “land bank”, “land development agency” etc., has nearly hundred years of history in Netherlands, France, Sweden, the United States and other western countries. Hong Kong, Macao and Taiwan of China have already implemented it and obtained full experiences. The so-called urban land purchasing and reserving system is commissioned or set up specialized agencies by city government (such as the store centre of urban land), keep urban land together through requisition, purchase, replacement, recycling, and land consolidation. By the government or their commissioned agencies for house dismantlement, land leveling and a series of preliminary development work, and then in order to ensure the urban land market supply and demand balance, guide the market into a healthy and stable development track, they will put the reserve land on the market in a planned way by means of bid invitation, auction, etc. [3] according to the urban land use planning and the annual land use planning. Although urban land purchasing and reserving system started relatively late in China, practice validated it’s positive effect and great success has been achieved in many ways. However, the operation of the land reserve mechanism is always with the movement of funds, insufficient funds for land reservation and unreasonable financing structure have become the main factors that constraint development and progress of the urban land reserve mechanism. Therefore, it is necessary to broaden the land reserve financing channels and search for land assets securitization path.

2. Land Securitization

Securitization is an important financial innovation in the financial markets of the world. Frank J. Fabozzi [4], a professor at Yale university, known as the “father” of securitization, defined securitization as a process which can turn the illiquidity assets like loans, leases, accounts receivable and so on into the market-oriented interest- bearing securities. As an asset, land has the superiority. It can keep or even add value and is resistant to inflation. Whoever owns the land can obtain a stable, predictable cash flow and its earnings is also shared in the whole survival time. Therefore, land is an asset suitable for securitization. When researching on the land problems, Japanese economists Noguchi Yukio [5] pointed out: “Land securitization means taking the land income as guarantee to issue securities, then sell the securities”. On the whole, land securitization [6] [7] is a process that takes the land income or loans as guarantee to issue securities. It aims to turn the land which has big value, immovable, inseparable and small-scale into securities on the premise that without loss the land land property rights, and use the function of the securities market to popularize land assets and specialize management.

Actually land securitization began in 1770, far earlier than the asset securitization. Germany took the lead in it’s operation, then developed slowly in Europe. It has been more than 200 years until now. European and American countries use the term “real estate securitization” which is derived from the Taiwan of China and Japan [8] instead of “land securitization”. Land securitization means creation of a kind of asset which brings the same economic interests as the land of financial assets can offer a new asset use means not only for who keep high assets, but also for small investors. It can maintain the value of acquired real estate assets in the future [9], separating land usage right from the land ownership right, thus to seek the effective land utilization. This article only discusses urban land securitization, which from the general understanding can be divided into land real assets securitization and land credit assets securitization.

3. Land Real Assets Securitization

The concept of land real assets securitization is that land developers issue land securities to the society to raise funds for land development. This article divides the land real assets securitization into land bonds, land investment funds, and land trust plan three modes according to the types of issued securities.

3.1. Urban Land Bonds

Land reserve organizations issue debt certificate to the public individuals or institutions to raise funds for solving funding shortage problem. Certificate holders [10] have the right to request issuers to pay capital and interest within agreed period. There is no difference from other bonds except the collected funds of land bonds must use for land acquisition and land consolidation.

Bond mode of urban land assets operation is shown in Figure 1. Land reserve organizations purchase land from original land right owner, then take the alienable land as a guarantee to commission the bond issuer issue the land bonds for society investors after processing and fabrication. The bond issuer gives the collected funds to land reserve organizations after extracting necessary issuing cost. At last, land reserve organizations use the funds for land acquisition and land consolidation, put the improved land into the market to make profits, part of which will be used to repay capital and interest for investors.

Land variable bonds and land rate bonds are two forms of urban land bonds. The concept of land variable

Figure 1. Bond mode of urban land assets.

bonds is same as the land price index bonds that was proposed by Japanese economists Noguchi Yukio, which puts the scheduled payments stipulated as follows: issue value of bond X escalaterate of land price during the issuance. Government will issue land variable bonds according to the speed of city development and the demand of land reserve for funds. Then, bank will redeem the bonds on land price index of that month [11] depending on the lengths of items maybe years later. Land rate bonds can either issue the fixed rate bonds or floating interest rate bonds what based on interest rates of bank. There is no denying that all of them must repay the capital and interest during the issuance.

3.2. Urban Land Investment Funds

Land reserve organization entrust the land funds management institution, including the government, the trust and investment companies and others to set up the funds. On the one hand, the money was collected by land funds management institution who take the land future earnings as the guarantee to issue income certificates is put in the land funds [12]. On the other hand, land reserve organ use the land funds to develop land and transfer them to land users. The income from land sales, rental, etc are also included in the land funds and then distributed among investors according to the land income certificates. Funds mode of urban land assets operation is shown in Figure 2.

Private offering and public offering are the two forms of funds distribution. The former is generally applicable to small funds scale, small amountofdistribution is to reduce the transaction costs. To collect the funds successfully in a limited time is a major consideration for the latter. Land funds is more suitable for the public offering because of it’s large scale in China. For choosing the funds types, it can be divided into contract funds and corporation funds. Urban land investment funds adopt the contract funds because it operates more conveniently, fully reflects the professional standards of management. The land investment funds can be divided into open- funded funds and closed-end funds according to the setup method. Open-funded funds burdens a larger redemption pressure than closed-end funds especially under a bad macro-economy, it will be easily bankruptted in lacking of circulating funds. As a result, urban land investment funds the closed-end funds is relatively safe for land funds management institution.

From the perspective of the funds that China has been set up currently, money collected per fund has reached billions what can meet the need of the land reserve organ well. Funds also play a important role in sharing risk. As the fund beneficiary, land reserve organ pay the profits to investors according to the operating condition what is beneficial to land reserve organ spread risk, rather than paying fixed interests like what land bonds and land reserve loans does.

3.3. Urban Land Trust Plan

Trust mode of urban land assets operation is shown in Figure 3. Land reserve organs take the land use right as guarantee to get loans from trust and investment companies, and then trust and investment companies issue trust certificates for investors to raise social idle funds and establish trust relationship with each other consequently. Besides, they put the funds into the city land reserve center [13] in the form of loans so that the city land reserve center can get enough money for land acquisition, land consolidation and land early development. Under this constitution, the consignor of the trust legal relation are trust beneficiary certificate holder and investors, the trustee are trust investment companies, the raised funds and the generated income from the capital are the trust

Figure 2. Funds mode of urban land assets.

Figure 3. Trust mode of urban land assets.

property, beneficiaries include the trust certificate holders and its designated other beneficiary.

“Management Regulation on Trust Investment Company” enacted in June 2002 and implemented on July 18 in the same year which provided powerful legal protection for the development about land reserve trust project after five times retrenchment of trust industry in China. As a trust variety with a stable income and smaller risk, it is bound to become the trust products that would be highly appreciated by trust companies.

4. Land Credit Assets Securitization

Land credit assets securitization is also called land mortgage securitization. Land users take the obtained land usage right as pledge for bank or other investment institutions to raise funds to exploit land. The mortgage creditors separate the factors of risk and return from land assets and regroup, then issue land mortgage debt to finance land development funds to society. It can be divided into domestic securitization and offshore securitization based on transaction form. The former is divided into balance-in mode, balance-out mode and quasi-off- balance-sheet mode according to whether underlying assets were taken out of sponsors’ balance sheet or not. Urban land mortgage securitization also has these corresponding modes.

4.1. Balance-In Mode

Balance-in mode is commercial bank sponsored to issues securities and the assets which don’t need be sell to special purpose vehicle (SPV), it also doesn’t exclude on the balance sheet from the sponsor. Assets in the asset pool are still part of bankruptcy assets when sponsor bankrupts. Therefore, it can’t achieve full bankruptcy isolation and investors have the recourse not specific to a particular portfolio but for the whole sponsoring organization. Its operation is shown in Figure 4.

Jian-Yuan asset-backed securities has been successfully issued in December 2005 [14] which is China’s first housing mortgage loan securitization product. This issue plan of China Construction Bank’s mortgage backed securities changed significantly on the basis of original plan. The original scheme is balance-in mode, construction bank set up housing loan securitization which is responsible for all related affairs of the mortgage-backed

Figure 4. Balance-in mode of urban land mortgage securitization.

securitization in its real estate financial staff. Housing loan securitization packaged individual housing loan assets entrusted by construction bank and entrust to a number of investment banks, the income assignment in the form of asset-backed securities to investors. But the ownership of assets still belongs to the construction bank, it doesn’t achieve risk isolation.

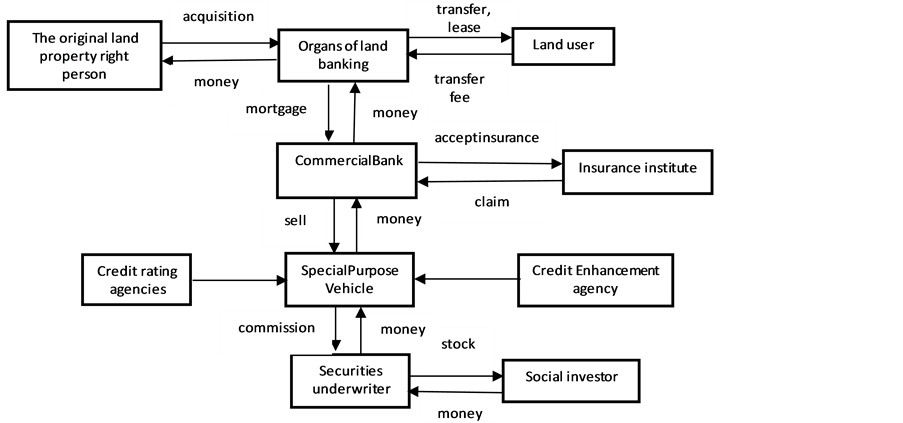

4.2. Balance-Out Mode

In this mode, the entire market is made up of land reserve agencies, insurance institutions, commercial banks, guarantee agencies, SPV, credit rating agencies and investors of the seven parts. Commercial bank as the sponsor sells the assets to SPV who puts them back together and establishes an asset pool after purchasing the assets. Then issue securities in the financial markets to collect funds supported by cash flow generated by the asset pool, the cash flow is also used to pay off the issue of securities. Because balance-out mode securitization has realized the true sale and bankruptcy isolation, so it is the most complete mode in terms of asset securitization with clear transaction structure and high operation efficiency. Its operation was shown in Figure 5.

4.3. Quasi-Off-Balance-Sheet Mode

The sponsors (commercial Banks) set up wholly owned or holding subsidiaries as SPV, then sell the assets to SPV. Subsidiary corporation puts them together and establishes an asset pool after purchasing the assets and issue securities supported by cash flow generated by the asset pool ( subsidiary is not only to buy assets of the parent company, but also buy other assets). Because profit should be transferred to the parent company and statements should be incorporated into the parent company’s balance sheet, thus subsidiary assets eventually reflect on the parent company’s balance sheet. But due to the true sale of assets from parent company to subsidiary corporation, it realizes the bankruptcy isolation. The essence of this model is balance-out mode by originator, so it is also called quasi-off-balance-sheet mode. SPV set up by banks can avoid cumbersome on loan sale pricing, rating, bargaining problems and simplify the securitization process.

4.4. Off-Shore Mode

The off-shore mode is a special form of asset securitization. The off-shore mode of land mortgage securitization is based on the future cash flow generated by the urban land mortgage loans, using the ideal mechanism of overseas securitization and issuing land mortgage securities in the international capital market to raise urban land reserve development funds through the setting up SPV and credit enhancement agency overseas. This mode of land assets securitization can use the advanced experience from developed countries, the ideal institutional environment and the relatively mature investment group to reduce [15] cost for collecting foreign funds for land reserve and development. Besides, it realizes the bankrupt-remote because of the true sale. The most important advantage is the success in avoiding various domestic institutional constraints, the lack of domestic capital market and the relatively backward economic development when setting up the SPV in China.

5. Mode Comparison

The aforementioned kinds of urban land securitization modes are currently under exploration and practice in

Figure 5. Balance-out mode of urban land mortgage securitization.

China and was proven particularly useful for solving the funds shortage problem in China’s urban land reserve institution. However, the asset securitization in China started relatively later than developed countries, such as system, environment, technology are the important factors that limit the of securitization development. Although the above modes have their own advantages in the development, there are still some disadvantages as shown in Table 1 and Table 2. We should choose the best mode in the actual operation of the various cities in China according to their size, the character of their land reserve management institutions, the development of their land securitization markets and the demand for money and so on. In general, the land trust plan is most workable and has a good development prospect in China, some metro cities such as Beijing, Xi’an have carried it out in large-scale. Land bonds mode also is a good choice considering its assured feasibility and the relatively lower cost than other modes. In addition, commercial banks have strong credit and background in China and land reserve institution is on behalf of the government with a high degree of credit guarantee, so using the balance-in mode is also an appropriate way in the starting stage of asset securitization in China. Other modes will eventually move out from behind the scenes to the front desk, and become powerful financial supports for the city land reserve with the improvement of relevant laws and regulations.

6. Conclusion

It is an inevitable trend that asset securitization will be make extensively used and widely developed, while the urban land assets securitization is a useful means for exploring land assets financing. But it is not deniable that it still faces a series of problems in carrying out the land assets securitization in the city. Therefore, a broader space should be created for developing and improving the related supporting environment as soon as possible to avoid the adverse selection in advance and regulate moral hazard after the event. First, modify and improve a series of rules and regulations including “Securities Law”, “Land Law”, “Contract Law”, “Insurance Law”, eliminate the land securitization system obstacles and make land securitization lawful by drawing lessons from [16] foreign land securitization legislation experience. Second, speed up the development of the mortgage market, guarantee market, securities market and other related market, and establish a normative intermediary service institution to lay the solid foundation for the secondary market of asset securitization. Third, set up comprehensive regulators [17] what are responsible for formulating policies, rules and regulations about land securitization, supervise and guide its implementation to prevent land securitization risk. Forth, land assets securitization needs a large number of professional technicians and managerial personnel, we should speed up the training of professional talents. The last, we should provide taxation preference policies to enhance the attraction of the securitization and inspire the enthusiasm of the participants.

Asset securitization started late in China and the development takes long time, the urban land assets securitization will undertake a tortuous path. We should explore actively to make this process effective, diverse, in-

Table 1. The comparison of urban land real assets securitization.

Table 2. The comparison of urban land credit assets assets securitization.

fluencial to play its role.

Cite this paper

Lulu Chen,Danyu Chen, (2016) The Mode Research of China’s Urban Land Assets Securitization. Open Journal of Social Sciences,04,1-8. doi: 10.4236/jss.2016.45001

References

- 1. Guo, Y.P. (2003) The Exploration Road of Urban Land Purchase and Reserve Securitization. Theory Study, No. 8, 27-30.

- 2. Qi, X.J. and Qi, B.K. (2004) The Research of the Urban Land Assets Securitization. Building Economy, No. 7, 74-77.

- 3. Zhang, X.H. (2002) Urban Land Purchasing and Reserving System and Its Securitization Financing. Nanjing Social Science, No. 9, 283-287.

- 4. Zhou, L.W. (2007) Economics Analysis of Asset Securitization. Ph.D. Thesis, Xiamen University, Xiamen.

- 5. Yuan, C.Y. (2005) The Urban Land Assets Securitization and the Analysis of Breaking through Modes in China. Ph.D. Thesis, Central China Normal University, Wuhan.

- 6. Zhang, H.B. and Jia, S.H. (2000) Try to Talk about the Urban Land Securitization and Its Operation Mode. Journal of Hangzhou Teachers College, No. 5, 32-36.

- 7. Zhu, Y.L. and Chen, H. (2006) Rural Land Securitization Financing Research. Economic Geography, 26, 412-414.

- 8. Li, J., Ma, F.L. and Li, M. (2007) The Analysis of Real Estate Securitization. Northern Economy, No. 9, 9-10.

- 9. Fan, H.S. (1995) Land Securitization and the Development of Chinese Agriculture. Economic Research, No. 11, 68-71.

- 10. Mo, X.H. (2003) Land Assets Securitization in China. China Real Estate Finance, No. 14, 39-42.

- 11. Wu, Q. (2011) The Analysis of the Urban Land Securitization Mode and Pricing in China. Financial Economy, No. 5, 52-55.

- 12. Lu, J.X. (2002) Land Securitization: A New Real Estate Financing. China Real Estate Finance, No. 3, 38-40.

- 13. Yang, D.H. (2004) The Financing Channels of City Land Reserve System in China. Shanghai Finance, No. 9, 8-10.

- 14. Liang, W. (2008) The Research of the Modes and Rish Control about Urban Land Securitization. Ph.D. Thesis, Wuhan University of Technology, Wuhan.

- 15. Bi, F.Y. and Wang, X.L. The Analysis of Urban Land Purchase and Reserve Asset Securitization in China. Urban Development, No. 5, 51-53.

- 16. Chen, X. (2006) China’s Urban Land Assets Securitization Research. Ph.D. Thesis, Southwest University, Chongqing.

- 17. Huang, X.B. (2005) Rural Land Securitization: Function, Obstacle and Countermeasures. Productivity Research, No. 10, 43-45.