103

Leading Indicators of Heating Coal Pricing in Turkey: A Coal Pricing Model (2003-2009)

namely, producer price index, producer price index for

mining and stone quarrying industry, consumer price

index, and consumer price index for electricity, gas and

other fuels. Base year of the price indexes is 2003. Data

were taken from the electronic data delivery system of

Central Bank of the Republic of Turkey (CBRT). Index

of Wages per Production Hour Worked in Manufacturing

of Cook and Refined Petroleum, whose base year is 1997,

is used as a proxy for the unit labour costs. Monthly data

are obtained through an interpolation by linear method as

the wage index is available only at a quarterly frequency

in the CBRT Electronic Data Delivery System. The elec-

tricity price is used as a proxy variable to capture the

effect of prices of other cost inputs on coal price levels.

The data were taken from the Turkish Statistics Institu-

tion (TL per KWh, The COICOP code is 0451001).

Industrial Production Index, whose base year is 2005,

is used as a proxy to measure real income at a monthly

frequency. Data source is the Electronic Data Delivery

System of the CBRT. To account for the seasonal ef-

fects, the data are seasonally adjusted by using the

Tramo/Seats method. All data in this study are in loga-

rithmic form.

2. Methods

2.1. Granger Causality Test for the Leading Indi-

cators

Granger [2], [3], [4], proposed a time-series data based

approach in order to determine causality relationships

among variables. According to Granger [2], the defini-

tion of causality is based entirely on the predictability of

some series, say. If some other series contains informa-

tion in past terms that helps in the prediction of and if

this information is contained in no other series used in

the predictor, then is said to Granger cause. Granger

causality has been used in the context of rational expec-

tations, definition of strong exogeneity, and econometric

modelling strategy. A better term for Granger causality is

precedence [5]. Therefore, this test can be used for de-

termining leading indicators of any variable. We may

also use the results of Granger causality for evaluating

forecasting performance since it is concerned with one-

ahead forecast accuracy.

Park and Philips [6], Sims, Stock and Watson [7] and

Toda and Philips [8] have shown that the standard as-

ymptotic theory is not applicable to hypothesis testing in

level VAR model if the variables are integrated or coin-

tegrated. Therefore, the usual Wald test statistics for

Granger non-causality based on level VAR not only has

nonstandard asymptotic distribution but depends on nui-

sance parameters in general if variables are nonstation-

ary.

In this study, we examine Granger causal relationships

between Turkish coal prices and other variables using

Toda-Yamamoto [9] approach to determine the leading

indicators for Turkish coal price level. Toda-Yamamoto

procedure considers a lag augmented or modified Wald

(M-Wald) test which has conventional asymptotic chi-

square (2

) distribution when a VAR (p + dmax) is es-

timated where dmax is the maximal order of integration

suspected to occur in the system. In other words, this lag

augmentation procedure provides standard asymptotic

although the time series have integration/cointegration

properties, and therefore, can be applied without a priori

information about the presence (absence) and location of

unit roots. The results of Granger causality test based on

M-Wald statistic are given in Table 2.

Foreign coal future prices and consumer price index

for energy sector are Granger causes of Turkish coal

prices at 5% level. There is also Granger causality from

domestic electricity prices and industrial production to

Turkish coal prices at 10% level. These results imply that

foreign coal futures prices and consumer price index for

energy sector can be used as the leading indicators for

domestic coal prices for Turkey. Therefore, these vari-

ables will be used the next steps of our analysis.

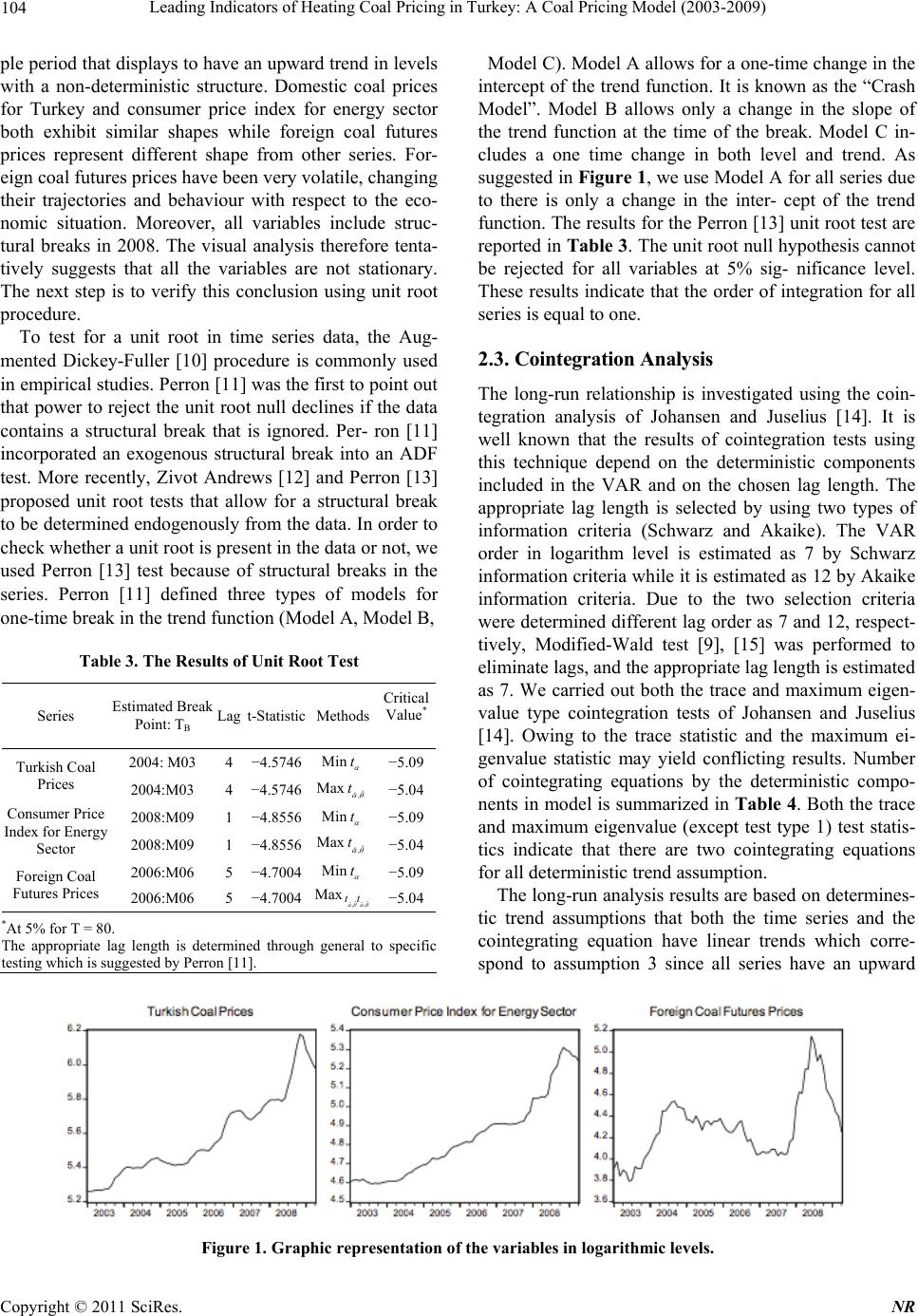

2.2. Unit Root Test with one Structural Break

Figure 1 shows a time plot of the data set over the sam-

Table 2. The Results of Pairwise Granger Causality Tests

Null hypothesis:

X does not Granger cause of Turkish coal

prices

Lag M-Wald

Statistic p-value

Foreign oil spot prices 3 2.97 0.3961

Foreign oil future prices 2 1.28 0.5273

Foreign natural gas spot prices 3 2.30 0.5122

Foreign natural gas future prices 3 0.68 0.8774

Foreign coal spot prices 11 15.94 0.1432

Foreign coal future prices 6 1454 0.0241

Consumer price index 2 3.59 0.2741

Consumer price index for electricity, gas

and other fuels 12 34.55 0.0006

Producer price index 2 0.48 0.7872

Producer price index for mining and stone

quarrying 2 1.53 0.4655

Unit labour cost 6 4.37 0.6256

Electricity Prices 10 17.58 0.0624

Industrial Production 8 14.11 0.0790

While maximum lag is 12, optimal lag length is determined by using two

types of information criteria (Schwarz and Akaike). If the two selection

criteria determine different lag order, Modified-Wald test, developed by

Toda and Yamamoto [9] is performed to eliminate lags from a general to

more specific model.

Maximum order of integration in the system is equal to 1.

Copyright © 2011 SciRes. NR