An Empirical Analysis of Credit Card Customers ’ Overdue Risks for Medium - and Small-Sized Commercial Bank in Taiwan

Copyright © 2011 SciRes. JSSM

240

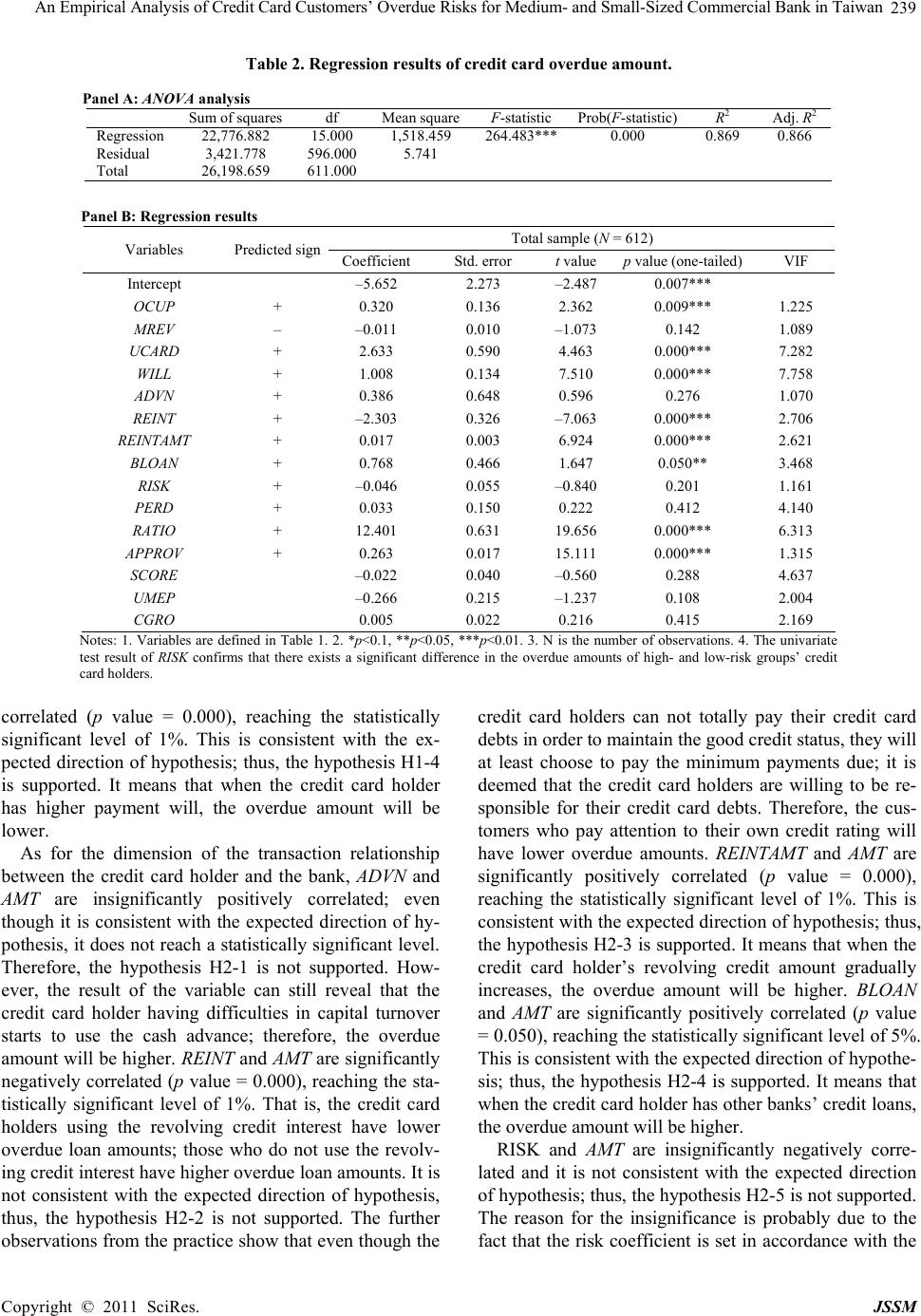

credit card holder’s occupation and the acquisition chan-

nel. In practice, even though the bank sets the credit card

holder to a high risk category, if the credit card holder is

willing to maintain a good credit status and pay the

monthly credit card payments on time, it will not result in

an increase in the amount of overdue loans. PERD and

AMT are insignificantly positively correlated; even

though it is consistent with the expected direction , it does

not reach the statistically significant level. Thus, the hy-

pothesis H2-6 is not supported. RATIO and AMT are sig-

nificantly positively correlated (p value = 0.000), reach-

ing the statistically significant level of 1%. It is consis-

tent with the expected direction of hypothesis; thus, the

hypothesis H2-7 is supported. It means that the higher

the ratio of used credit to the credit limit is, the higher the

overdue amount will be. APPROV and AMT are signifi-

cantly positively correlated (p value = 0.000), reaching

the statistically significant level of 1%. It is consistent

with the expected direction of hypothesis; thus, the hy-

pothesis H2-8 is supported. It means that the higher the

credit card holder’s credit limit issued by the bank is, the

higher the overdue amount will be.

Even though the three macroeconomic control vari-

ables, SCORE, UMEP, CGRO do not have significant

impacts on the overdue amount, the results of these three

variables can still indicate that when the economy in

Taiwan is good, the overdue amount will be lower; when

the unemployment rate is higher, the customers using

credit cards more conservatively will not increase the

overdue amount. When the annual growth rate of total

credit card accounts increases, it means that customers

use credit cards more frequently; therefore, the overdue

amount will be higher.

5. Conclusions and Suggestions

The paper makes the following recommendations about

the credit amount of credit card lending for the banking

industry and management decision-making units: 1) the

recommendation to th e card issuing b anks’ planning unit:

it is suggested that before the issuance of credit cards, the

ad hoc planning unit’s credit card promotions should

engage the consumer market segmentation and consider

the potential customers of professional levels as the

choice of target customers; 2) the recommendation to the

card issuing banks’ credit approval unit: it is suggested

that after improving plans, the planning unit’s credit re-

viewer and loan approval staff should rigorously control

applicants’ credit conditions; while examining their pro-

vided written credit reports, the bank s should refer to the

purpose of customers’ consumption and use of a credit

card and customers’ financial status in order to perform

the detailed assessment of applicants’ future ability and

willingness to repay their debts; 3) the recommendation

to the card issuing banks’ audit unit: the audit unit is

suggested to implement the rigorous internal control to

ensure that no fraud circumstances will happen. It is also

suggested to appropriately adjust the lending regulations

of current financial situation under the present social

economy situation in order to avoid the outdated regula-

tory information and prevent the front-line workers from

facing the dilemma of not immediately dealing with a

contingency or emergency; 4) the recommendation to the

card issuing banks’ highest decision-making unit: the

business development should be based on the concept of

sustainability and stability. The op erating environment of

the financial industry is highly changeable; it repeatedly

tests the highest decision-making unit’s wisdom and

common sense. If banks only seek temporary profits and

hurt business foundation, it will be worth the candle. In

the pursuit of return on equity, it should be more prag-

matic to face the potential change of perspective, but also

to take into account the social responsibility in order to

reduce the generation of business cost and social cost.

6. Acknowledgements

The authors would like to thank the National Science

Council of the Republic o f China, Taiwan for financially

supporting this research under Contract No. NSC

98-2410-H-259-010-MY3 and NSC 99-2410-H-141-

007-MY2.

REFERENCES

[1] K. J. White, “Consumer Choice and Use of Bank Credit

Cards: A Model and Cross-Section Results,” Journal of

Consumer Research, Vol. 2, No. 1, 1975, pp. 10-18.

doi:10.1086/208611

[2] M. Howard, “Shifting Risk and Fixing Blame: The Vex-

ing Problem of Credit Card Obligations in Bankruptcy,”

The American Bankruptcy Law Journal, Vol. 75, No. 1,

2001, pp. 63-143.

[3] M. Griffiths, “Consumer Debt in Australia: Why Banks

will Not Turn Their Backs on Profit,” International Jour-

nal of Consumer Studies, Vol. 31, No. 3, 2007, pp. 230-236.

doi:10.1111/j.1470-6431.2006.00524.x

[4] L. L. Gan, R. C. Maysami and H. C. Koh, “Singapore

Credit Cardholders: Ownership, Usage Patterns, and Per-

ceptions,” Journal of Services Marketing, Vol. 22, No. 4,

2008, pp. 267-279. doi:10.1108/08876040810881678

[5] P. Lopes, “Credit Card Debt and Default over the Life

Cycle,” Journal of Money, Credit and Banking, Vol. 40,

No. 4, 2008, pp. 769-790.

doi:10.1111/j.1538-4616.2008.00135.x

[6] A. Kara, E. Kaynak and O. Kucukemiroglu, “An Empiri-

cal Investigation of US Credit Card Users: Card Choice

and Usage Behavior,” International Business Review, Vol.

5, No. 2, 1996, pp. 209-230.

doi:10.1016/0969-5931(96)00006-6