Risk Migration in Supply Chain Inventory Financing Service

Copyright © 2011 SciRes. JSSM

226

one period considering the demand forecast for the new

period, which is now available. Therefore, the determi-

nistic formulation next described comprises a set of

planning periods, and only the first one includes the de-

tailed scheduling decisions with shorter time increments.

Such detail period moves as the model is solved in time,

thus the term rolling horizon.

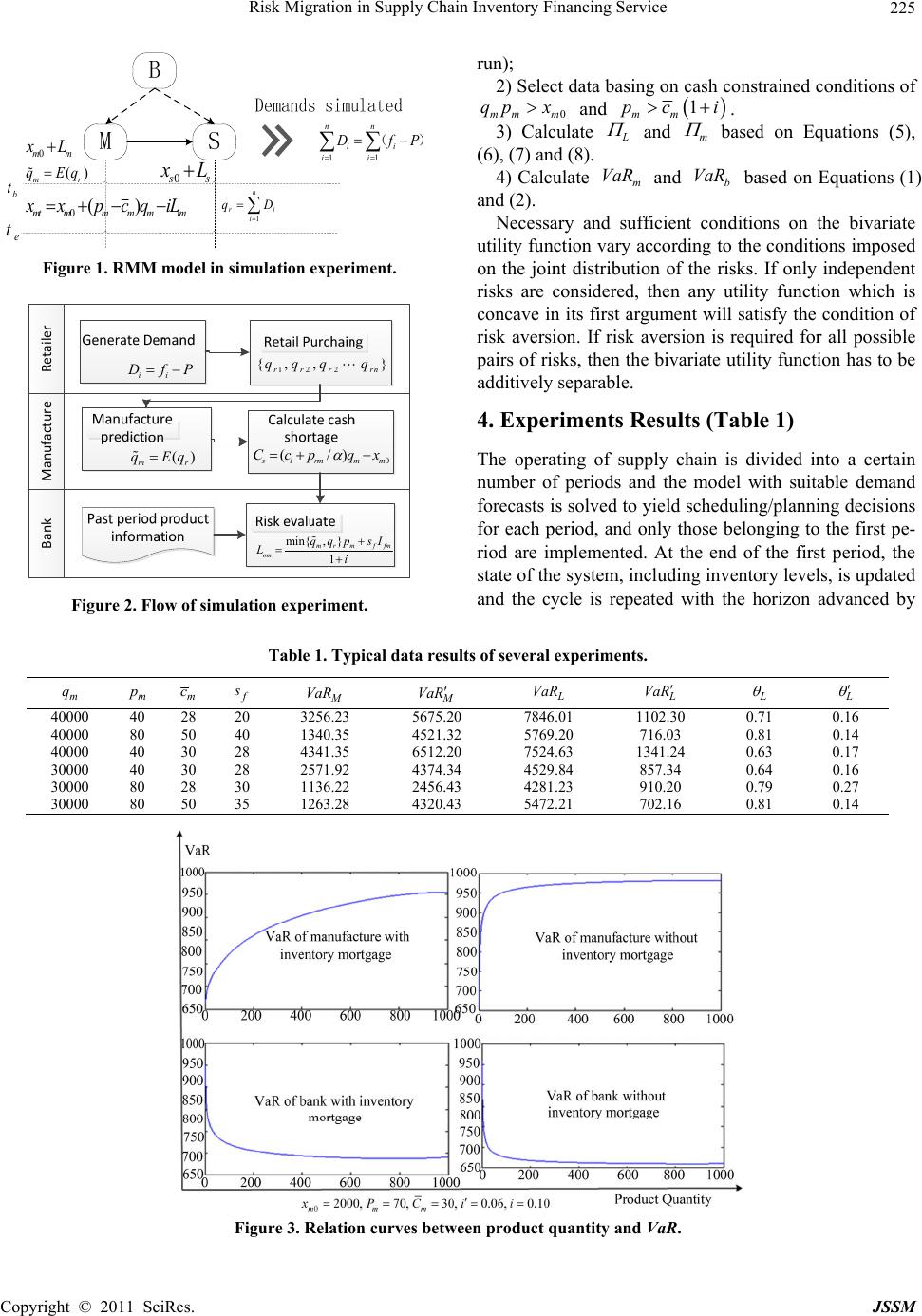

Calculate VaR of both manufacture and bank, then

standardize VaRto [0,1], then we can get

LL L M

VaR VaR VaR

basing on Equation (1) and

(2). Get

by 1

L

, Table 1 shows the typical

data results of several experiments in computer simula-

tion when 01000

m

x、0.10i and '0.06i. With

different initial variables, the bank Va R will decrease

when adopt inventory mortgage, the potential profit is

growing. For the manufacture, after use inventory mort-

gage, VaR is larger than before. The potential income is

growing because bank can offer more loans which reduce

the manufacture shortage of cash, so the manufacture can

produce more to maximum profit.

When the manufacture satisfies 0mm m

qp x and

1

mm

pc i

, accompany with market demand in-

creasing, the VaR of bank decrease because manufac-

ture’s capability of making profit. If using inventory

mortgage, the VaR value for manufacture is increasing

because more cash are put in producing and inven-

tory(Figure 3).

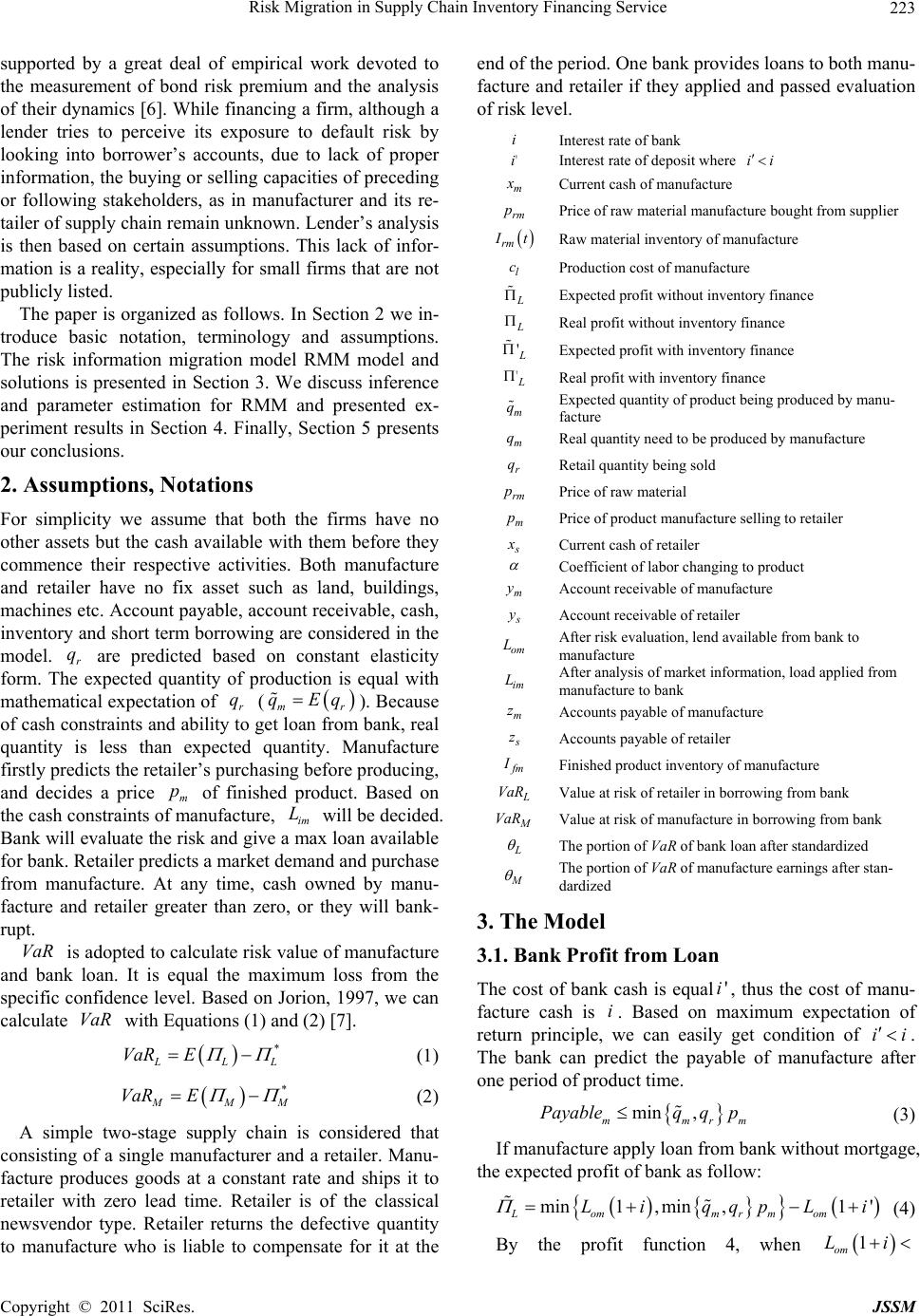

5. Conclusions

We discussed manufacture and retail supply chain struc-

ture which both facing cash-constrain and a bank that

finances the manufacturer. Supply chain inventory mort-

gage must satisfy preconditions of 0mm m

qp x and

1

mm

pc i, that is member of supply chain will use

self-owned capital before using inventory mortgage, and

the cost of loan must less than the profit rate. In inven-

tory mortgage, both bank and manufacture are benefit

because the risk migration. After migration of risk, it is

more compatible with the information shared between

supply chain member and bank. For supply chain mem-

bers, they have more market information than bank in

production operate process, after sharing inventory in-

formation with bank, this reduce the bank shortage in-

formation. So the migration of risk can help optimize the

whole supply chain and bank.

REFERENCES

[1] J. L. Cavinato, “Identifying Interfirm Total Cost Advan-

tages for Supply Chain Competitiveness,” International

Journal of Purchasing and Material Management, Vol.

27, No. 4, pp. 10-15.

[2] J. A. Buzacott, R. Q. Zhang, “Inventory Management

with Asset-Based Financing,” Management Science Vol.

50, No. 9, 2004, pp. 1274-1292.

doi:10.1287/mnsc.1040.0278

[3] T. Y. Choi and Y. Hong, “Unveiling the Structure of Sup-

ply Networks: Case Studies in Honda, Acura, and Dail-

mer Chrysler,” Journal of Operations Management, Vol.

20, No. 5, 2002, pp. 469-494.

doi:10.1016/S0272-6963(02)00025-6

[4] D. M. Lambert and M. C. Cooper, “Issues in Supply

Chain Management,” Industrial Marketing Management,

Vol. 29, No. 1, 2000, pp. 65-84.

doi:10.1016/S0019-8501(99)00113-3

[5] N. R. Srinivasa Raghavan and V. K. Mishra, “Short-Term

Financing in a Cash-Constrained Supply Chain,” Interna-

tional Journal of Production Economics, Vol. 11, No.14,

2009.

[6] D. Backus and J. Wright, “Cracking the conundrum,”

Brookings Papers on Economic Activity, Vol. 38, 2007,

pp. 293-329.

[7] P. Jorion, “Value at Risk: The New Benchmark for Con-

trolling Market Risk,” Irwin, Chicago, 1997.

[8] H. Sonnenschein, “Market Excess Demand Functions,”

Econometrica, Vol. 40, 1972, pp. 549-563.

doi:10.2307/1913184