Journal of Service Science and Management, 2011, 4, 191-202 doi:10.4236/jssm.2011.42023 Published Online June 2011 (http://www.SciRP.org/journal/jssm) Copyright © 2011 SciRes. JSSM 191 On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Vicente González Díaz1, François Pérès2, Adolfo Crespo Márquez3 1General Dynamics European Land Systems, Seville, Spain; 2Laboratoire Génie de Production, ENIT –INPT Université de Toulouse, Toulouse, France; 3Department of Industrial Management, School of Engineering, University of Seville, Seville, Spain. Email: vicente.gonzalezdiaz@gdels.com, francois.peres@enit.fr, adolfo.crespo@esi.us.es Received March 24th, 2011; revised May 7th, 2011; accepted May 16th, 2011. ABSTRACT This paper deals with the problem of efficiency in warranty management programs, where efficiency is understood as provisioning an effective prod uct warranty service to the lowest cost. For that purpose, this paper first d efines the con- cept of warranty and its interaction with other disciplines. It introduces all the necessary stages that should be included within a framework for warran ty management. This brief introduction will help the reader to plac e the work presented in this paper within a context of tools and methods already developed in the literature for similar areas management. Later on, an analysis on risk and cost is presented applying these methodologies to the development of a warranty pro- gram. We show how generic tools developed for project management can now be adapted, in a very useful way, to or- ganize and control the technical assistances to customers during the warranty period. Finally, conclusions of the work are presented, where the main concepts of the paper are summarized and further potential research is suggested. Keywords: After-Sales, Cost Management, Decision-Making, Earned Value Analysis, Reference Framework, Risk Management, Warranty Assistance 1. Introduction Warranty is a written and/or oral manufacturer’s assur- ance to a buyer that a product or service is or shall be as presented [1]. Guarantees the integrity of a product and specifies the warrantor (generally the manufacturer) re- sponsibility in case of the failure of the product per- formance. This assurance is applied during a period of time after a product has been sold. The management of warranty combines technical, administrative and mana- gerial actions during the warranty period of an item in order to maintain or restore the item to a state in which it can perform the required function, needed to provide a given service [2]. We can find different types of warran- ties, each one suited for a different type of product (con- sumer, commercial and industrial; standard versus cus- tom-built, etc.) [3,4]. In this paper we will consider a complex system such as a custom-built product, where multitude components and conditions must be taken into account. For this case, our literature review shows im- portant interactions between warranty and other disci- plines [2,5] impacting warranty efficiency. Among all of them, we underline warranty interactions with: Maintenance: In many cases, during the warranty period the manufacturer still has a strong control over its product and its behavior. Additionally, the ex- pected warranty costs depend normally not only on warranty requirements, but also on the associated maintenance schedule of the product [6]. Outsourcing: warranty service or in general, the af- ter-sales department of a company, is usually one of the most susceptible to be outsourced due to its low risk and due also to the fact that, among other features, outsourcing provides legal insurance for such assis- tance services [7]. Quality: The improvement of the reliability and qual- ity of the product has not only an advantageous and favorable impact in front of the client; it also highly reduces the expected warranty cost [8]. Costs Analysis: In reference to costs estimations, there are nowadays methods to estimate accurately the final cost of a specific acquisition contract as, for instance, the “Estimate at Completion” (EAC) method [9], a management technique that can be used in a project for the control of the costs progress. The main contribution of this paper is to show how generic tools developed for project management could be adapted in an efficient way, to organize and control the  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 192 technical assistances to customers during the warranty period. As already introduced, the literature review on this research subject is properly illustrated in some ref- erences as [2] and [3]. The structure of this paper is as follows: first it is briefly depicted a framework for the warranty management and, particularly, it is defined the warranty efficiency. Afterwards, the paper deepens in the analysis about risk and cost regarding warranty assis- tances. With this, the paper continues with the project management definition of earned value, considering the after sales management point of view. To finish, the con- clusions will suggest some possible further researches. 2. Warranty Efficiency and Management Where do warranty efficiency efforts fit within a generic framework for warranty management? What techniques can be used to improve warranty management efficiency? In previous contributions we have addressed these issues, and proposed a reference framework (Figure 1), consist- ing in a process (steps to follow) and a supporting struc- ture (techniques and methods to improve decision mak- ing at each step) to manage warranty [10,11]. This refer- ence framework consists of four building blocks (BB): The Warranty Program Effectiveness BB: Here we suggest applying the Balanced Scorecard (BSC) model to avoid strategic contradictions between the warranty program and the overall business strategy. Then, it is necessary to determine the product critical- ity, i.e. how crucial is the complaint of a client (due to a failure) and its consequences to the business. Fi- nally, the Root Cause Failure Analysis is proposed for those high impact specific failures showing rare and high failure frequency. The Warranty Program Efficiency BB: In order to attend warranties at the minimum waste or expense it is necessary to design an adequate plan for the war- ranty program. An adapted reliability analysis and maintenance design tools can be extracted from the maintenance field (for instance RCM). In reference to costs, the Warranty Policy Risk-Cost-Benefit Analy- sis will depend on the information available. The Warranty Program Assessment BB: A RAMS (Reliability, Availability, Maintainability & Safety) analysis of every single warranty program is impor- tant here due to the huge amount of restrictions and conditions that any complex product warranty ob- serves. In this 3rd step is also important to include a Life Cycle Cost Analysis [12]. The Warranty Program Improvement BB: It is con- sidered the last step. Tools that can be used in this point are related to the implementation of new tech- nologies to warranty (here the “E-Warranty” concept comes to play, including resources, services and the necessary management to enable proactive decisions). Also for this step, Customer Relationship Manage- ment and Six Sigma tools, for instance, can be very beneficial for the warranty program of the company. 3. Cost-Risk-Benefit Analysis in Warranty Once described the main lines of the suggested warranty management framework, an important aspect to fulfill Step 1.Effectiveness Step 2.Efficiency Step 4.Improvement Step 3.Assessment BalanceScore Card Criticality Analysis Failure Root CauseAnalysis Maintenance Design Tools adapted to Warranty Warranty Policy Risk‐Cost‐ Benefit Analysis Life Cycle Cost Analysis Relia bility,Availability, Maintenability and Safety Six Sigma Customer Relationship Management E‐Technologies(E‐Warranty) Step 1.Effectiveness Step 2.Efficiency Step 4.Improvement Step 3.Assessment BalanceScore Card Criticality Analysis Failure Root CauseAnalysis Maintenance Design Tools adapted to Warranty Warranty Policy Risk‐Cost‐ Benefit Analysis Life Cycle Cost Analysis Relia bility,Availability, Maintenability and Safety Six Sigma Customer Relationship Management E‐Technologies(E‐Warranty) Figure 1. Proposed Framework for Warranty Management.  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 193 the proposed step on warranty efficiency is to analyze those costs, risks and benefits applied to the development of a warranty program. Notice that here the term “bene- fit” refers to a cost which is intended to decrease. The profit reverted from warranty is considering such a war- ranty as a competitive one and a marketing tool which can increase the sale of a robust product, with higher quality than others competitors in the market. Concerning warranty costs modeling, there is a huge range of diverse approaches, analytical and empirical, related to other fields [1]. In general terms, to carry out a Warranty Policy on Risk-Cost-Benefit Analysis, such activity will depend of course on the objective that the own model builder keeps in mind. In any case (as here with the management of a warranty program), the prob- lem is influenced by the information available. In addi- tion to this, the complexity of the issue is usually high and considerations must be taken under certain assump- tions in order, either to simplify the analytical resolution, or to reduce sometimes the computational needs. This section will try to present and adapt the main concepts related to costs, risks and earned value to a warranty program and for the improvement of its management and control. 3.1. Warranty Cost Management A project cost management includes those processes re- quired to ensure that the project is completed within the approved budget [13,14]. Regarding warranty tasks, it will be primarily concerned with the cost of the resources required to fulfill the complete activities related to the after-sales service in order to provide to the customers a proper technical assistance. It is possible to observe from different points of view the warranty cost management. On one hand, the general cost management should consider the effect on the cost of the product of decisions taken for the whole project. For example: limiting the number of design reviews may reduce the cost of the project, but at the expense of an increase in service and customer’s operating costs. A broader view of warranty cost management should be referred also to the life-cycle cost, considering therefore acquisition, operating, and disposal costs when evaluating with the Balance score- card the different project strategies. Consequently, a creative approach applied to optimize life cycle costs will: Save time Increase profits Improve quality Expand market share Use resources more effectively Solve problems not only for the warranty assistances but for the whole business. This approach is usually called as value engineering which is used together with the life cycle cost analysis as techniques to reduce cost and time, improve quality and performance, and optimize the decision-making. On the other hand, the particular cost management does not re- quire considering all those decisions taken during the whole product life cycle (for instance, recycling costs or the number of design reviews). The particular costs for warranty refer just to those activities needed to resolve a problem during a specific period of time at the beginning of the phase of use or product operation. Such activities will depend just on the product quality (see Figure 2). Frequently, estimating and analyzing the financial per- formance of a product launched to the market does not consider warranty issues. In this case, controllable and uncontrollable costs should be estimated and budgeted separately to ensure that the expected benefits will be obtained from the actual performance of the product. In order to influence in warranty costs, it will be easier at the early stages of the project during the pre-launch stage, due to the fact that a soon definition and identification of the expected product requirements are critical to reduce future costs during the warranty period. The process of determining what resources (people, equipment, materi- als) and what quantities of each (when needed) should be used to perform warranty activities is dealt as part of the product logistic support but supposes of course an im- portant part to take into account when the budget to these activities must be established. In addition to this, the process of developing an approximation of the costs for the resources needed to perform the warranty tasks should be preferably done prior to budget request rather than after budgetary approval is provided, developing an assessment of the likely quantitative result and how much will cost to the organization to provide this product service. The product pricing will be a business decision where the above mentioned costs should be taken into account, together with other factors. As inputs for the warranty cost approach can be included: Resource requirements Estimated activities duration Historical information Used structure of the organization Commercial available data on cost estimating, and risks (either as threats or opportunities)… All these factors have a significant impact on cost which the management board should consider to budget properly the future technical assistance. The Figure 3 illustrates as an example those costs to have into consid- eration, in connection to the already mentioned para- graph about that logistic support which should be applied or taken into account during the management of a war- ranty program. We suggest using the following methods  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 194 Manufacturing department Totalwarranty cost Usage patterns Repair quality Claim execution patterns Warranty costper claim After‐sale department Warranty costper claim Warranty costper claim After‐sale department Marketing department Manufacturing department Totalwarranty cost Usage patterns Repair quality Claim execution patterns Warranty costper claim After‐sale department Warranty costper claim Warranty costper claim After‐sale department Marketing department Figure 2. Integrated model for total warranty costs (adapted from [3]). Training Cost (Operator and Maintena nce Training) Acquisition cost (Research, Design, Test, Poduction) Poor Management Software Cost (Operation and Maintenance Software) Supply and Support Cost (Spares, Inventory) Product Distribu tion Cost (Transportation, Traffic and Material Handling) Operation Cost (Personnel , Facilities, Utilities and Energy) Retirement and Disposal Cost Test and Suppor t Equipment Figure 3. Costs iceberg related to Logistic Support. for warranty cost estimation: Analogous estimating: It uses the actual warranty cost of a previous similar product as the basis for estimat- ing the cost of the current product [15,16]. It is fre- quently used when there is a limited amount of de- tailed information about the product in the early product phases. Generally less costly than other esti- mating techniques, but it is also generally less accu- rate. Most reliable when the previous product is simi- lar in fact and not just in appearance (that includes a similar market target), and the staff to prepare such estimation have the needed expertise (because the ap- proach will be considered as a form of expert judg- ment). Parametric modeling: It uses product characteristics (parameters) in a mathematical model to predict product failures and consequently the costs of spare parts, repair time, logistic… as well as staff training, technical documentation, tools and equipment etc. [15, 16]. Models can be simple or complex, but they are more reliable when the historical information used to develop the model is accurate, and the parameters are quantifiable. Bottom-up estimating: It involves the cost estimation of individual activities or work packages related for instance to the product maintenance, adapted and summarized to warranty tasks [15,16]. Its cost and accuracy will depend on the size and complexity of the individual activity or work package taken into consideration. Therefore, the management board must weigh the ac- curacy against the cost, due to the fact that smaller ac- tivities or packages increase both cost and accuracy of the estimating process. There are of course other methods to estimate warranty costs. All of them should finally express a quantitative assessment of the likely costs of the resources required to complete the warranty activities (labor, materials, supplies, and maybe special categories such as inflation allowance or cost reserve). The estima- tion is expressed in currency units to facilitate compari- sons with other budgets of the whole business or with the warranty costs of other products. For instance, it is very useful for large companies with a specific range of prod- ucts in the market (e.g. the automotive sector); to control multiple warranties cost baselines to measure different aspects of the warranty performance or different degrees in demands or requirements of specific customers’ pro- files. In any case, the warranty cost estimation must be refined during the course of the warranty period, adding new details which can be available during this time, making all this exercise more accurate. The estimation report usually includes other supporting details as a de- scription of the scope of work estimated and how this estimation has been developed, with justified assump- tions and an indication of the range of possible results. Once the cost estimation is done, it must be described how such costs will be managed during the warranty pe- riod. This description is usually expressed in a warranty cost management plan, which will be an element of the overall product plan. In order to simplify the use of the  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 195 mentioned methods there are many software applications, simulation or statistical tools widely used to assist with cost estimating and failure modeling [15,16]. 3.2. Warranty Risk Management The warranty risk management is the systematic process of identifying, analyzing, and responding to risk likely appearing during a program of warranty assistances. It includes maximizing the probability and consequences of positive events and minimizing the probability and con- sequences of adverse events to warranty objectives. Sev- eral contributions deals with issues regarding risk and spare parts estimation, or risk and maintenance decisions [17,18] can now perfectly be applied to warranty man- agement. Warranty risk is understood as an uncertain event or condition that, if occurs, has a negative effect on the program objective. Nevertheless, it brings the oppor- tunity to improve the product quality. Any risk has a cause and, if it occurs, a consequence. Therefore, known risks are those that have been identified and analyzed and may be possible to plan for their occurrence and mitiga- tion. On the other hand, unknown risks cannot be man- aged or their probability of occurrence cannot be as- sessed. Nevertheless, executive managers may address them by applying a general contingency based on past experience with similar programs, in our case, related to the after-sales service. Those known risks that are threats to the warranty program may be accepted if they are balanced with the reward that may be gained by taking the risk. Likewise, risks that are opportunities may be pursued to benefit the program’s objectives. Conse- quently, organizations (particularly the after-sales de- partment or the management board) must be committed to addressing risk management throughout the whole warranty program. One measure of an organization’s commitment is its dedication to gathering high-quality data on warranty and product risks and the characteristics of these risks. In Figure 4 we illustrate the risk management process [obtained from 19-21], divided into different steps. In the next paragraphs we will apply this process to the war- ranty management case. Step 1: Risk Management Planning. In order to approach the risk management activities to a warranty program, a planning for such processes can help to ensure that the level, type and visibility of this management are proportional with both the risk and im- portance of the warranty assistance to the whole organi- zation. Tools to prepare the mentioned planning are for instance program charts; business policies which prede- fine an approach to risk analysis on the warranty assis- tance; defined roles, responsibilities as well as authority levels for decision-making; risk flexibility; etc. In order to identify risks, the plan must analyze them qualitative and quantitative, including a monitoring and control structured and performed during the product life cycle, and being addressed to general risks of the after-sales service. We suggest that main parts to include in a risk management plan [22], but particularized for a warranty program, are: Methodology: This part defines the approaches, tools, and data sources used to perform the risk manage- ment on the warranty program. Different types of as- sessments can be appropriate, depending on the pro- gram stage (product pre-launch, launch or post-launch stage), the amount of available data, and the tolerance admitted in the risk management. Roles and responsibilities: The plan must define the lead, support, and risk management team membership for each type of action. The risk management team may be able to perform independent and impartial analyses of the warranty program. Risk Management Risk Analysis YesNo Ris k Management Planning 1 Ris k I d enti ficati o n 2Qualitative Ri sk Analy sis 3Quantitati ve Ri sk Analy sis 4 Acce ptabl e Ri sk? Ris k Response Planning 5Cal culate Ris k Contingency Ris k Monitoring & Con t rol 6 1, Deci de how 2. F i nd t hem 3. Filter 4. Measure 5. Deci de ac ti ons 6. Act and m eas ure Figure 4. Risk management workflow.  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 196 Budgeting and Timing: It establishes a budget for risk management of the warranty assistances program. Due to the fact that the risk management process is a continuous process based on the observation of the environment which can evolve all the time, it is therefore necessary that decisions should be reviewed periodically during the warranty program execution. Scoring and Interpretation: The scoring and interpre- tation methods must be determined in advance to en- sure the consistency of the plan, being them appropri- ate for the type and timing of the qualitative and quantitative risk analysis Thresholds: The “boundaries” that identify which risks will be acted upon, by whom, and in what man- ner. The product owner, customer, or user can have a different risk threshold. The acceptable threshold will constitute the objective which the management board (or risk team) will measure. Reporting formats: It describes the content and format of the risk response plan, including also how the re- sults will be documented, analyzed, and communi- cated to other parts of the company. Tracking: The plan has to take into account how risk activities will be recorded for the benefit of the cur- rent warranty program, future needs, and lessons learned. In addition to this, this part can also inform whether these risk activities will be audited and how. Step 2: Risk Identification. Once the planning is done, the risk identification can be carried out through various steps [23]. This is the process of determining which risks can affect the war- ranty program and to document the characteristics of each one. This identification supposes an iterative proc- ess according to the risk management plan. Methods to use for the identification of risks in warranty programs are for instance: Documentation reviews (as warranty assumptions, hypotheses or considered scenarios, as well as other data sources). Techniques to compile information (as brainstorming; expert and technicians interviewing; strengths, weak- nesses, opportunities, and threats -SWOT- analysis). Checklist (based for instance in historical data or pre- vious warranty programs of similar products). Diagramming techniques (as cause-effect diagrams; process flow chart; etc.). Step 3: Qualitative Risk Analysis. Afterwards, a qualitative analysis of risks [24] must be performed which is the process of assessing the impact of the identified risks in the warranty assistances. It priori- tizes risks according to their potential effect on the pro- gram objectives, determining the importance of address- ing specific risks and guiding risk responses. This analy- sis requires that the probability and consequences of the risks be evaluated using established qualitative-analysis methods and tools. The importance of a risk can be mag- nified due to time-criticality of risk-related actions. Therefore, trends in the results when qualitative analysis is repeated can indicate the need for more or less risk-management action. In general terms, the use of these tools can be helpful to correct trends that are fre- quently present in the warranty program. Consequently, this analysis should be reviewed during the product’s life cycle in order to be warned to any change during the warranty program. Step 4: Quantitative Risk Analysis. After the qualitative analysis, a quantitative analysis [25] of the possible risks during the application of the warranty assistance is also important. This is a process which measures the probability and consequences of risks, estimating their implications for program objec- tives. It helps to analyze numerically the probability of each risk and its consequence during the warranty service. There are techniques for that purpose [26] as well as other decision analysis which help, for instance and among others issues, to identify risks which require more attention by quantifying their relative contribution to warranty risk, as well as to determine realistic and achievable cost, schedule, or scope targets for the war- ranty program. The quantitative and qualitative risk analysis processes can be used separately or together. Anyway, when there are repeated results in the quantita- tive analysis which mark a trend, it is an index about the need for more or less risk management action. Methods to quantify risks during a warranty program are for in- stance: Decision tree analysis (in order to consider different alternatives and their implications). Simulation (using for instance the Monte Carlo tech- nique on a specific model [26]). Afterwards, a sensitivity analysis should be applied, which is not really a method of quantifying risks such as decision trees or simulation. The sensitivity analysis al- lows detecting how variances in warranty elements affect the achievement of the whole program objectives. Step 5: Risk Response Planning. The following step on the risk management of a war- ranty program is the response planning, which is the process of developing options and determining actions to enhance opportunities, reducing threats to the program’s objectives. It includes the identification and assignment of individuals or parties to take responsibility for each agreed risk response. This planning ensures that identi- fied risks are properly addressed and the effectiveness of response will directly determine whether risk increases or decreases during the development of the warranty pro-  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 197 gram. The risk response planning must be appropriate for our case of warranty assistance. In addition to this, it has to take into account, for warranty programs, among other features: The severity of the risk The cost to meet challenges The time to be successful The context of the warranty program The influences on every involved part The response planning must be under the responsibil- ity of a person, who must be able to determine and select the best response from the available options to the identi- fied risks for the warranty program. Step 6: Risk Monitoring and Control. Finally, the last step is to monitor and control risks [22], which is the process of keeping track of the identi- fied risks, monitoring residual risks and identifying new risks, ensuring the execution of risk plans, and evaluating their effectiveness in reducing risks. The records risk metrics are usually associated with the implementation of contingency plans, providing information that assists with effective decision making in advance of the risk occurrence. Therefore, the risk monitoring is in few words an ongoing process for the product life cycle which helps to determine if: Responses have been implemented as planned. Response actions are effective as expected. New responses should be developed. Warranty assumptions are still valid. Risks have changed (trends analysis). Proper policies and procedures are followed. Occurred risks were not previously identified. Anyway, risk control should involve the choice of al- ternative strategies, the implementation of contingency plans, the application of corrective actions, or replan the whole warranty program in order to mitigate risks. In the following chart (see Table 1) are included those inputs and outputs of the already commented steps for the Table 1. Inputs/Output summary . Risk manage ment in a warranty program. Warranty risks management Warranty risks management Input Output Risk Management Plan- ning Warranty program chart. Company’s risk management policies and plan templates. Defined roles and responsibilities. Risk tolerances in the warranty program. Work breakdown structure for warranty assistances. Risk plan for the warranty management Risk Identification Risk plan for the warranty management Scope and objective of the warranty program Risk categories: -Technical or quality risks -Warranty management risks -Organizational risks -External risks -Historical information List of identified risks Risks symptoms or warning signs Insufficient detail in the inputs of other steps Qualitative Risk Analysis Risk plan for the warranty management List of identified risks Status of the warranty program Product type Data precision Probability and impact scales Warranty assumptions Risks ranking for the whole warranty pro- gram List of prioritized risks Trends in the results of the qualitative analy- sis Quantitative Risk Analysis Risk plan for the warranty management List of identified risks List of prioritized risks Historical information Expert technicians judgment Prioritized list of quantified risks Probabilistic analysis of the warranty pro- gram (for achieving expected costs and times) Trends in the results of the quantitative analysis Risk Response Planning Risk plan for the warranty management Risks ranking for the whole warranty program List of prioritized risks Prioritized list of quantified risks Probabilistic analysis of the warranty program List of potential responses Common risk causes in warranty assistances Trends in the results of the qualitative and quantitative analysis Response plan for warranty risks Residual risks Secondary risks Contractual agreements Contingency reserves Alternative strategies Revision to the warranty risk plan Risk Monitoring and Control Risk plan for the warranty management Response plan for warranty risks Program data and records Additional risk identification and analysis Scope changes Work plans (for emerging risks) Corrective actions Changes request on the warranty program Update to the risk response plan Risk database for the warranty assistances  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 198 management of warranty risks. Further researches on this field can be oriented to deepen in the methods and tools to develop and execute each commented step in the risk management for a warranty program. 4. Earned Value Management Applied to Warranty Once described the influence of factors like cost, risk and time in the warranty management, we melt all these fea- tures in a technique which allow us the economical fol- low-up of the warranty service [1,27]. An accounting system developed for general projects management, ap- plied and well-balanced to warranty management, is now presented. This system implies the monitoring of cost performance to detect and understand variances from warranty plan, ensuring that all appropriate changes are recorded accurately in the cost baseline, in order to pre- vent incorrect or inappropriate changes (out of acceptable limits) which can affect negatively to the business goal. The inputs required for this control are, for instance, warranty cost baseline, performance reports (regarding budget issues), change requests, and cost management plan etc. It may also alert the management board to war- ranty issues that may cause problems in the future and should be integrated in the general budgetary control system [28-31]. We first compile the meanings of all those acronyms (internationally accepted) that are used in this section in Table 2. It is important here to underline, that the best warranty service is the one that is not needed to be ap- plied. Nevertheless (and unfortunately), it does not sys- tematically happen, so the company must be prepared for any eventuality that may occur. The following account ability system referred to warranty management is for the Table 2. Acronyms meanings. Acronym Meaning EVMS Earned Value Management System EVA Earned Value Analysis EV Earned Value ITD Incurred To Date ETD Estimate To Complete EAC Estimate At Completion BAC Budget At Completion BCWS Budgeted Cost of Work Scheduled BCWP Budgeted Cost of Work Performed ACWP Actual Cost of Work Performed Cv Cost Variance Sv Schedule Variance CPI Cost Performance Index SPI Schedule Performance Index case when failures in the sold product are foreseen and they must be handled under warranty. As commented before, the concept of “benefit” or “earned value” etc. must be understood in the case of warranty management as a lower cost in the incurred value applied in the tech- nical assistance, keeping high levels of service quality. Earned Value Management System (EVMS) or Earned Value Analysis (EVA) is an integrated management sys- tem that allows the progress monitoring, combining (for our specific case) the technical assistance planning with the warranty cost. The traditional practice of project management (Figure 5) tends to compare incurred costs (actual costs) with planned costs (planned expenditure) [32]. The level of incurred cost in warranty issues is not necessarily a good measure of progress of the technical assistances tasks. Therefore, EVA applied to after-sales provides a third reference point which represents an ob- jective overview of the status of the warranty contract: the value of work completed to date and earned value. This earned value is difficult to understand in warranty terms, since the warranty application does not imply any direct income. On the contrary, it is usually considered as an expenditure centre. Consequently, the philosophy here is to consider as earned value all this benefit obtaining by saving resources but applying at the same time a proper service to the customer. This proper service means fast, effective and without any additional eventuality to the customer which supposes a decrease of the confidence in the company. In the case of Figure 5, one can ask if there is an excess in the incurred warranty cost, if the product is behaving in an unexpected (and negative) way, or if the product launch is advanced in comparison to the scheduled product positioning in the market. In this fig- ure, the abscissa axis refers to the percentage of the whole program time. This program time refers to the warranty period since a new product is launched to the market, till the warranty expiration of the last sold unit. What is here suggested is that the level of incurred cost is probably not the right choice to determine the progress of Figure 5. Traditional practice: ITD vs. planned costs.  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 199 the warranty program or the reliability of the product [33-35]. The concept is to compare the budgeted cost and plan- ning with the actual planning at any time of the program, integrating the program’s operational progress (earned value). The basis of the Earned Value Management Sys- tem applied to after-sales service is the structured de- composition of the warranty program in work packages. A value must be assigned to each work package linked to the completion of activities such as milestones, deliver- ables related to the warranty schedule. That is in formu- las as follows: EV = Earned Value = [Completed% of the Warranty Schedule] × [Budget for the Warranty Program] EV = Σ ([Completed% of the Work Package] × [Budget for the Work Package]) There are other concepts to have in mind during the benefit analysis of a warranty program. Such concepts are for instance the following ones, regarding of course the work of the warranty program taken into considera- tion: BCWS: Budgeted Cost of the Work Scheduled BCWP: Budgeted Cost of the Work Performed ACWP: Actual Cost of the Work Performed The graphic (Figure 6) illustrates the meaning of the above mentioned concept. As we can see comparing the two above figures, the Actual Cost of the Work (ACWP) performed corresponds to the Incurred to Date (ITD), and the Budgeted Cost of the Work Scheduled (BCWS) cor- responds to the Budget Scheduled at the beginning of the warranty program. The Budgeted Cost of the Work Performed (BCWP) which corresponds to the already defined Earned Value (EV). In order to implement all this, the warranty pro- gram must have a defined work breakdown structure. It does not require being an exhaustive list of tasks; how ever this is a tool which helps to organize the total work scope of the warranty program by the subdivision in dis- crete work elements or tasks of the warranty program. Consequently, by combining the following information it Figure 6. Budgeted costs vs. actual costs. is possible to calculate the earned value, making an early diagnosis of the warranty program evolution: Budget for packages of the warranty program Incurred cost by packages Warranty program planning Degree of the operative program advance Comparing the obtained curves (Figure 7), it is possi- ble to control the reserves and to determine risks along the warranty program. Here, the EAC (Estimate At Completion) corresponds to the Incurred To Date (ITD) plus the Estimate To Complete, and the BAC (Budget At Completion) corresponds to the originally planned value of the complete warranty program. The commented work packages in terms of warranty are related to that techni- cal assistance which must be given to the corresponding amount of product units that are foreseen to be sold ac- cording to a determined schedule. The product delivery schedule can be transformed in terms of warranty costs which are expected to be spent for a specific amount of units in a specific moment. In other words, if we know the units delivery schedule and the foreseen average of warranty costs per unit sold, it is direct to know the expected warranty cost for the whole program. Reader can find case studies [36-38] describing a context very useful to illustrate and facilitate the com- prehension of these concepts related to warranty terms. Additional concepts related to this benefit analysis are: Cost variance (Cv) is the difference between the Earned Value and the Actual Cost of the warranty program at any specific time: Cv = BCWP – PTCA = Earned – Actual Schedule variance (Sv) is the difference between the Actual and the Planned Earned Value of the warranty program at any specific time: Sv = BCWP – BCWS = Earned – Budget. Cost Performance Index (CPI) is the rate about how much costs to generate each € of Earned Value: CPI = BCWP/ACWP = EV/ITD Schedule Performance Index (SPI) is the rate about how fast supposes to generate real value in com- Figure 7. Comparison between EAC and BAC.  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 200 parison to the budgeted one: SPI = BCWP/BCWS = EV/Quoted The meaning of such indexes is as shown in the fol- lowing chart (Table 3). These commented indexes are “backward looking”. However, one of the main advantages of this benefit analysis is the ability to use these indexes to foresee the future direction of the warranty program. This is due to the fact that the calculation of the Estimate to Complete (ETC) is adjusted to the performance level achieved to that date: ETC = (BAC – ITD)/(SPI × CPI) EAC = ITD + ETC = ITD + (BAC – ITD)/(SPI × CPI) With these results we can observe that: If the past performance is good: CPI & SPI > 1, ETC↓ and EAC < BAC If the scheduled activities are not been achieving: CPI & SPI < 1, ETC↑ and EAC > BAC If CPI & SPI = 1, EAC = BAC Summarizing, the Earned Value Management provides integrated data about cost, operations and planning re- garding (in our case) a warranty program. It is also useful for an early detection of deviations as well as a provision of objective information on the status of the warranty contract. It has the ability to objectively determine the EAC and the warranty program planning, integrating risk management and the improvement of cost prediction. 5. Conclusions and Further Research Throughout this document we have seen various aspects of the efficiency related to the improvement of the war- ranty management. Once defined the usual concept of warranty and briefly proposed a framework for its man- agement, it has been analyzed risk and benefit as crucial parts in the warranty efficiency. Nowadays, concepts and methods for project management are being applied in many different areas. The intention here has been to summarize and focus them to the case of a warranty pro- gram, considering such program as a project with a spe- cific budget and milestones. Therefore, for such a con- sideration, a deep knowledge in the product is of course essential. These tools, in general terms, enable to control evolution of the warranty program, to foresee possible new expenses and, summarizing, to take proactive deci- sions which improve, in last term, the satisfaction of the Table 3. Chart about CPI and SPI meaning. >1 (good) <1 (bad) CPI Under budget Over budget SPI Ahead schedule Behind schedule client with the company and with the product provided. About these financial aspects on warranty management, further research can be focused to improve the budgetary control as for instance through the implementation of the concept of e-warranty in order to foresee the possible necessity of spare parts, or future complaints from the user. E-warranty can be therefore defined as the support to a warranty program which includes those resources, services and management needed to enable proactive decision-making. This support not only includes the e-technologies but also typical activities from warranty, as monitoring, diagnosis, prognosis, etc. In other words, these further researches can be oriented to the costs as- sessment by applying advanced mathematical methods with the support of electronic technologies, such as re- mote surveillance and monitoring, and e-diagnosis, etc. in order to develop more elaborate models. Though the application of new technologies, the perception of quality by the customer will not be only related to the internal production. The external company behaviour is also to be taken into account, once the product has been launched to the market. At the same time, it is important to influ- ence the internal personnel into the search of a continu- ous improvement. For that intention, the evolution of the warranty program has to be quantified, making easy the decision process as budget distribution, marketing ac- tions, personnel motivation, etc. Warranty has been here considered as an activity valued in terms of cost and over the amount of used resources. Therefore, we have tried to condense the warranty contribution in an indicator re- lated to consensual criteria according to the company strategy, taking into account the internal affections, af- fections in the market and in the customer. In this paper we have related the quality service to a failure, in order to improve the decision making in warranty and the company strategy. REFERENCES [1] K. Lyons and D. N. P. Murthy, “Warranty And Manufac- turing, in Integrated Optimal Modelling in Piqm: Produc- tion Planning, Inventory, Quality And Maintenance,” Kluwer Academic Publishers, New York, 2001, pp 289-324. [2] V. G. Díaz, J. F. Gómez, M. López, A. Crespo and P. M. de León, “Warranty Cost Models State-of-Art: A Practi- cal Review to The Framework of Warranty Cost Man- agement,” ESREL 2009, 2009, pp. 2051-2059. [3] D. N. P. Murthy and W. R. Blischke, “Warranty Man- agement and Product Manufacturing,” Springer-Verlag London Limited, London, 2005, p. 302. [4] V. G. Díaz and A. C. Márquez, “Book Review: Reliabil- ity Engineering. Warranty Management and Product Manufacture,” Production Planning & Control: The Management of Operations, Vol. 21, No. 7, 2010, pp.  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 201 720-721. [5] D. N. P. Murthy and I. Djamaludin, “New Product War- ranty: A Literature Review,” International Journal of Production Economics, Vol. 79, No. 3, 2002, pp. 231-260. doi:10.1016/S0925-5273(02)00153-6 [6] B. Dimitrov, S. Chukova and Z. Khalil, “Warranty Costs: An Age-Dependent Failure/Repair Model,” Wiley Peri- odicals, Inc., Wilmington, 2004. [7] J. Gómez, A. Crespo, P. Moreu, C. Parra and V. G. Díaz, “Outsourcing Maintenance in Services Providers,” Taylor & Francis Group, London, 2009. [8] S. Chukova and Y. Hayakawa, “Warranty Cost Analysis: Non-Renewing Warranty with Repair Time,” John Wiley & Sons, Ltd., Chichester, 2004. [9] D. Christensen, “Determining an Accurate Estimate at Completion,” National Contract Management Journal, Vol. 25, 1993, pp. 17-25. [10] V. González Díaz, C. Parra; J. F. Gómez and A. Crespo. “Reference Framework Proposal for the Management of A Warranty Program,” Congress Euromaintenance 2010, Verona, 2010. [11] V. G. Díaz, L. B. Martínez, Juan F. G. Fernández and A. C. Márquez. “Contractual and Quality Aspects on War- ranty: Best Practices for the Warranty Management and Its Maturity Assessment,” International Journal of Qual- ity and Reliability Management, Vol. 2, 2010. [12] C. Parra, A. Crespo, P. Moreu, J. Gómez and V. G. Díaz, “Non-homogeneous Poisson Process (NHPP), Stochastic Model Applied to Evaluate the Economic Impact of the Failure in the Life Cycle Cost Analysis (LCCA),” Taylor & Francis Group, London, 2009, pp. 929-939. [13] Ehrlenspiel, Klaus; Kiewert, Alfons; Lindemann, U. Hundal and S. Mahendra, “Cost-Efficient Design,” Sp- ringer-Verlag Jointly Published with ASME, New York, 2007. [14] S. Seuring and M. Goldbach, “Cost Management in Sup- ply Chains,” Springer-Verlag, New York, 2002, p. 109. [15] D. Mayhew and R. Bias, “Cost-Justifying Usability,” Elsevier, Amsterdam, 2007. [16] D. Doyle, “Cost Control: A Strategic Guide,” Elsevier, Amsterdam, 2002. [17] B. Ghodrati, P. A. Akersten and U. Kumar, “Spare Parts Estimation and Risk Assessment Conducted at Choghart Iron Ore Mine: A case study,” Journal of Quality in Maintenance Engineering, Vol. 13, No. 4, 2007, pp. 353-363. [18] F. Backlund and J. Hannu, “Can We Make Maintenance Decisions on Risk Analysis Results?” Journal of Quality in Maintenance Engineering, Vol. 8, No. 1, 2002, pp. 77-91. [19] P. M. Collier, J. B. Anthony and G. T. Burke, “Risk and Management Accounting. Best Practice Guidelines for Enterprise-Wide Internal Control Procedures,” Elsevier, Amsterdam, 2006. [20] L. S. Spedding and A. Rose, “Business Risk Management Handbook: A Sustainable Approach,” Elsevier, Amster- dam, 2007. [21] L. X. Zeng, “On the Basis Risk of Industry Loss Warran- ties,” The Journal of Risk Finance, Vol. 1, No. 4, pp. 27-32. [22] A. Lester, “Project Management, Planning and Control,” Elsevier, Amsterdam, 2006. [23] L. Tchankova, “Risk Identification—Basic Stage in Risk Management,” Environmental Management and Health, Vol. 13, No. 3, 2003, pp. 290-297. doi. 10.1108/09566160210431088 [24] J. Emblemsvag and L. E. Kjølstad, “Qualitative Risk Analysis: Some Problems and Remedies,” Management Decision, Vol. 44, No. 3, 2006, pp. 395-408. doi.10.1108/00251740610656278 [25] J. Buglear, “Quantitative Methods for Business. The A to Z of QM,” Butterworth-Heinemann, New York, 2004. [26] A. C. Marquez, “A Structured Approach for the Assess- ment of System Availability and Reliability Using Con- tinuous Time Monte Carlo Simulation,” Proceedings of the 24th International Conference of the System Dynam- ics Society, Nijmegen, 2006, pp. 56-56. [27] W. R. Blischke and D. N. P. Murthy, “Warranty Cost Analysis,” Marcel Dekker, New York, 1994. [28] R. Howes, “Improving the Performance of Earned Value Analysis as a Construction Project Management Tool,” Engineering, Construction and Architectural Manage- ment, Vol. 7, No. 4, 2008, pp. 399-411. [29] J. S. Page, “Conceptual Cost Estimating Manual,” El- sevier, Amsterdam, 1996. [30] D. N. P. Murthy, W. R. Blischke, S. Kakouros and D. Kuettner, “Changing the Way We Think about Warranty Management,” Warranty Week, 2007. [31] T. Hines, “Supply Chain Strategies: Customer Driven and Customer Focused,” Elsevier, Manchester, 2004. [32] M. Raby, “Project Management via Earned Value,” Work Study, Vol. 49, No. 1, 2000, pp. 6-10. [33] D. N. P. Murthy, M. Rausand and S. Virtanen, “Invest- ment in New Product Reliability,” Reliability Engineering & System Safety, Vol. 94, No. 9, 2009, pp. 1593-1600. doi:10.1016/j.ress.2009.02.031 [34] D. N. P. Murthy, P. E. Hagmark and S. Virtanen, “Prod- uct Variety and Reliability,” Reliability Engineering & System Safety, Vol. 94, No. 10, 2009, pp. 1601-1608. doi:10.1016/j.ress.2009.02.030 [35] D. N. P. Murthy, T. Osteras and M. Rausand, “Compo- nent Reliability Specification,” Reliability Engineering & System Safety, Vol. 94, 2009, pp. 1608-1617. doi:10.1016/j.ress.2009.02.029 [36] V. G. Díaz, J. F. Gómez and A. Crespo. “Case Study: Warranty Costs Estimation According to a Defined Life- time Distribution of Deliverables,” World Congress on Engineering Asset Management, Athens, 2009. [37] N. Jigeesh and M. S. Bhat, “Modeling and Simulating the Dynamics in Project Monitoring and Earned Value Ana-  On the Risks and Costs Methodologies Applied for the Improvement of the Warranty Management Copyright © 2011 SciRes. JSSM 202 lysis,” Journal of Advances in Management Research, Vol. 3, No. 1, 2006, pp. 26-43. [38] A. Owen, “Accounting for Business Studies,” Elsevier, Manchester, 2003.

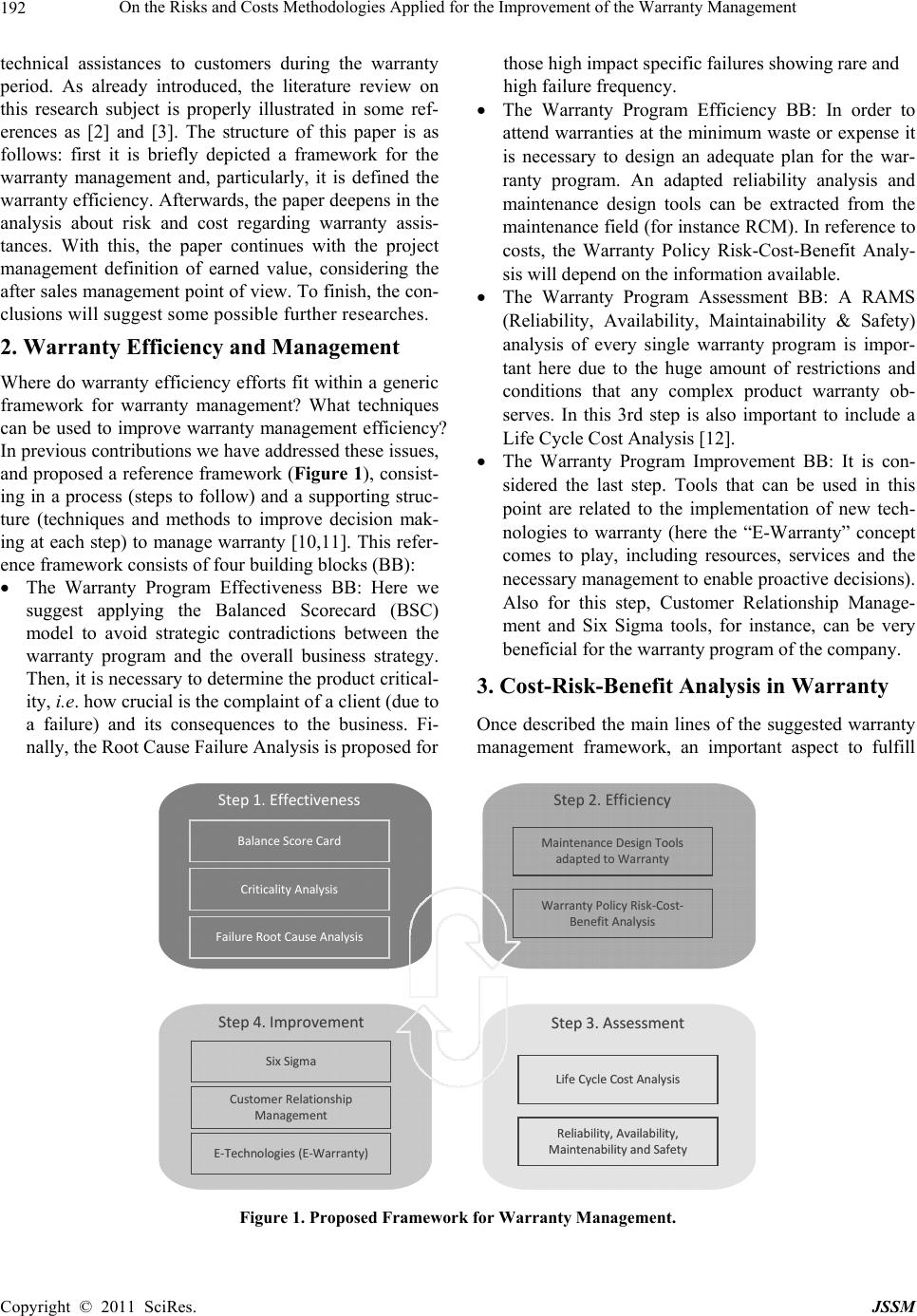

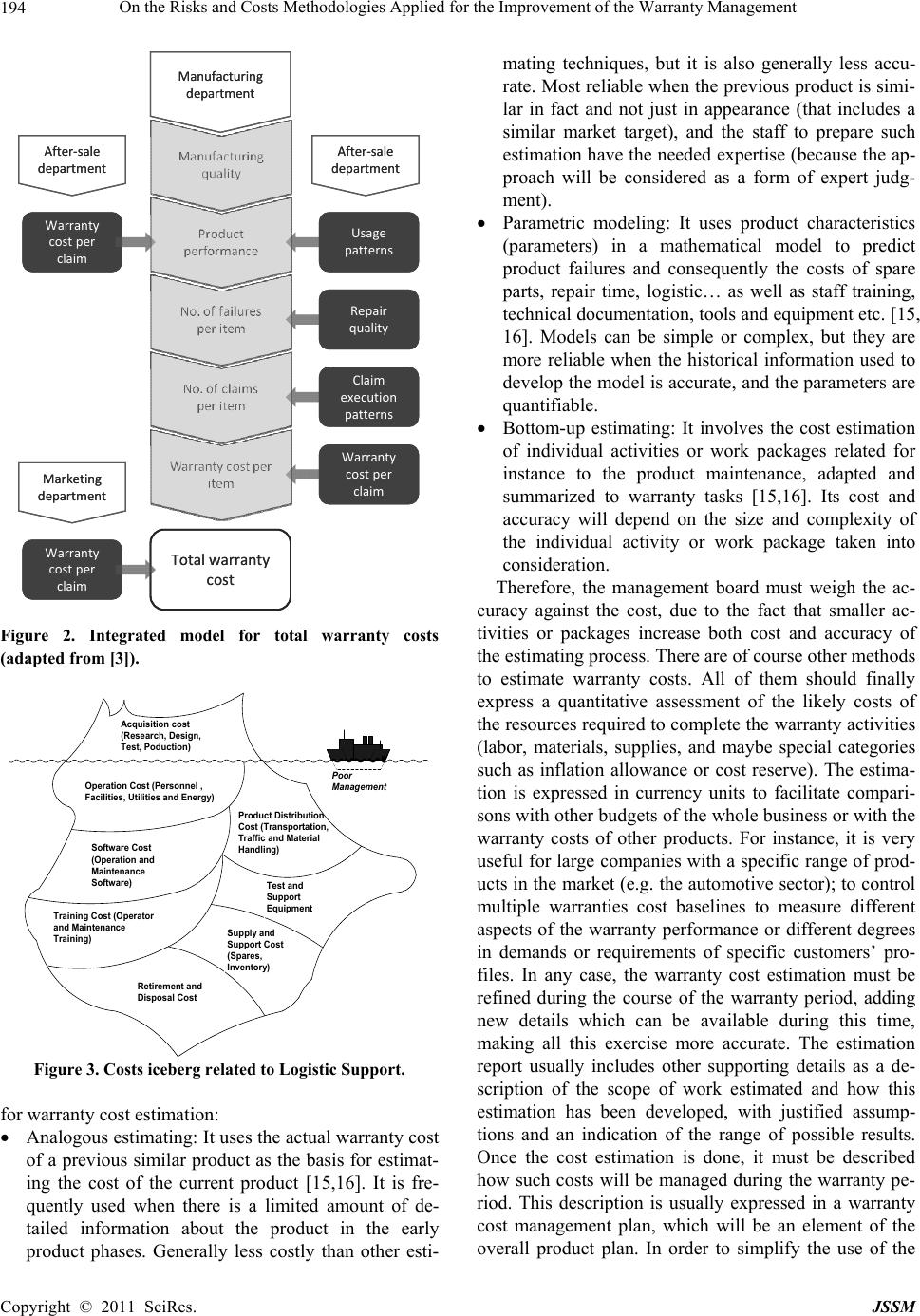

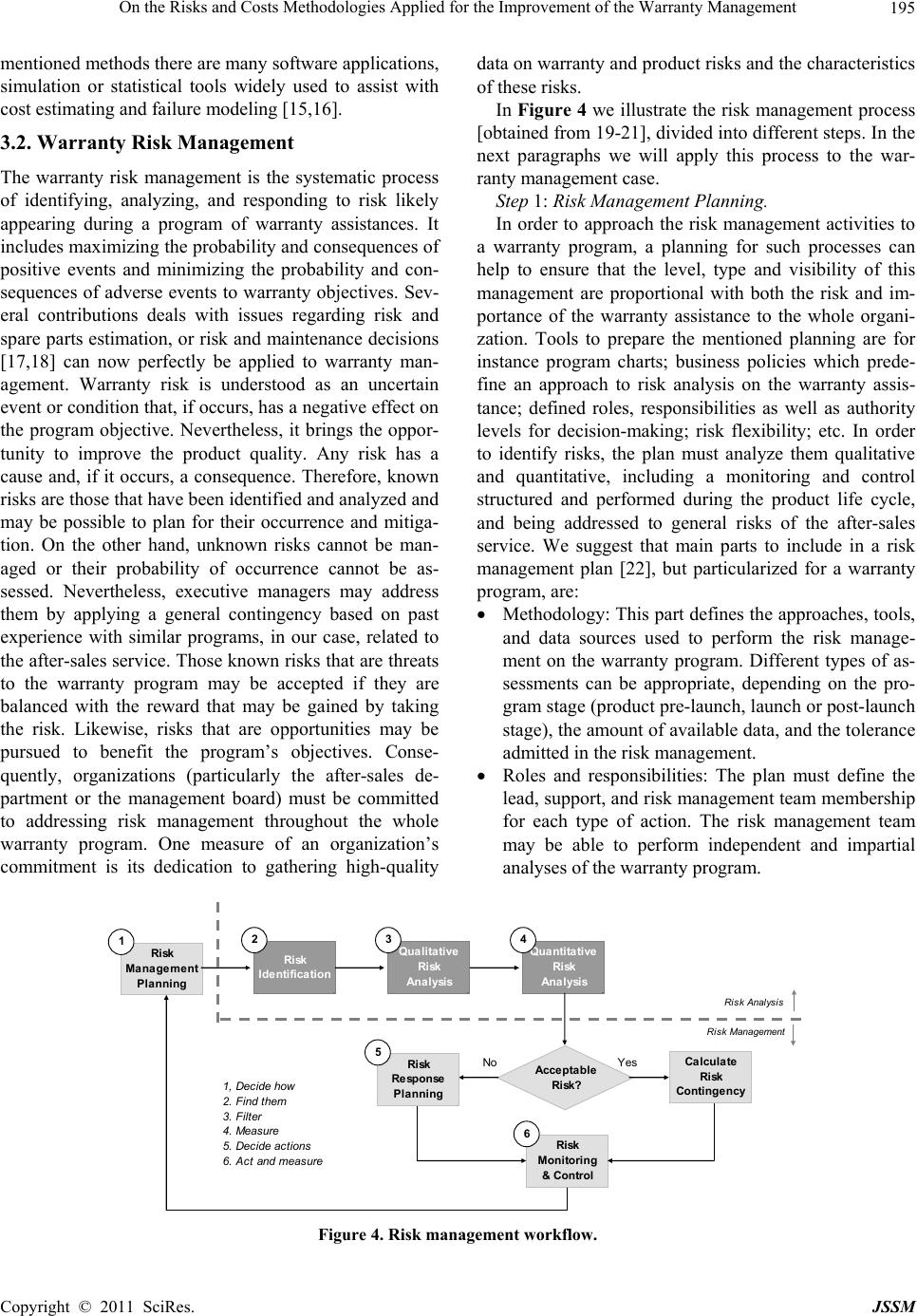

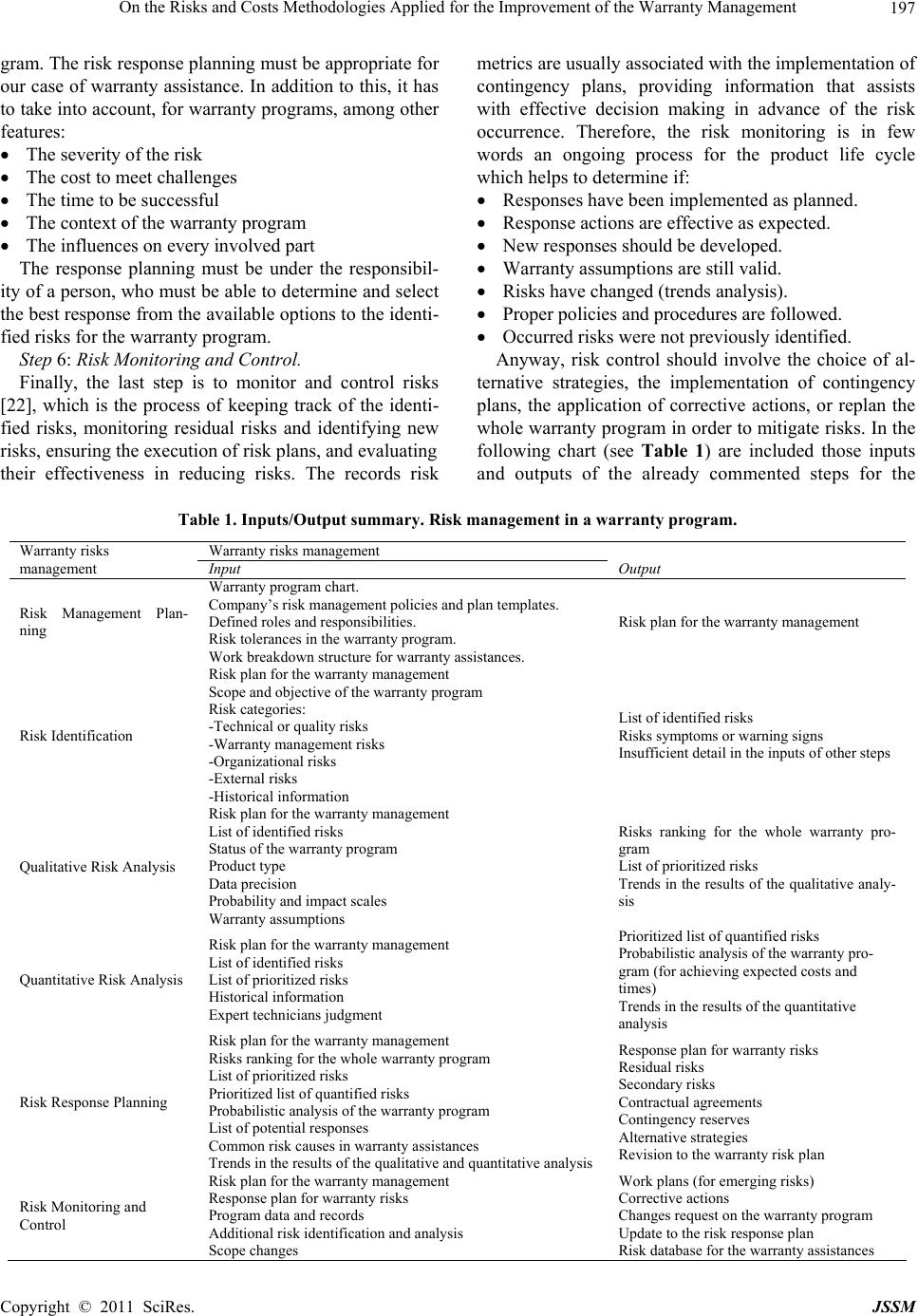

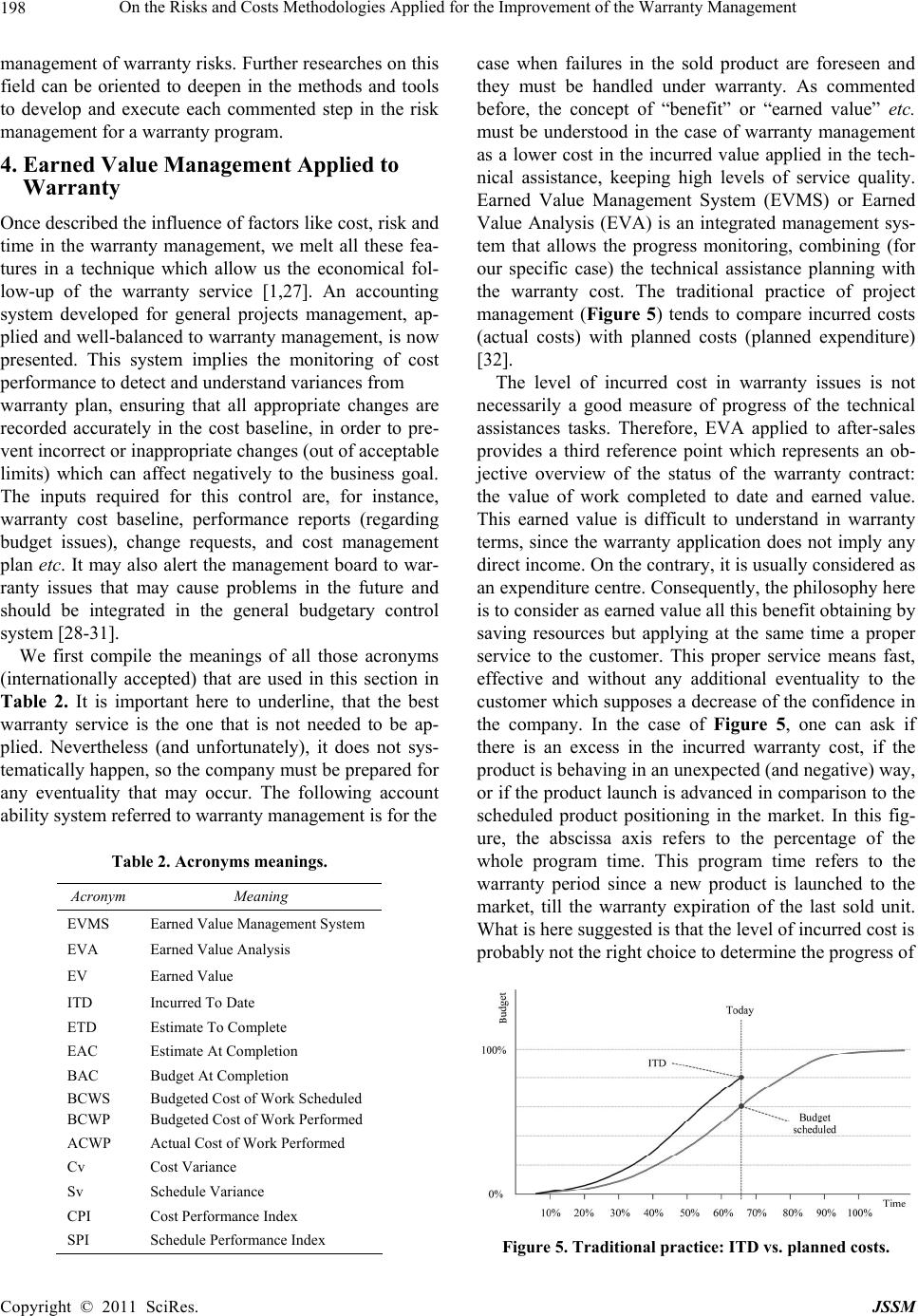

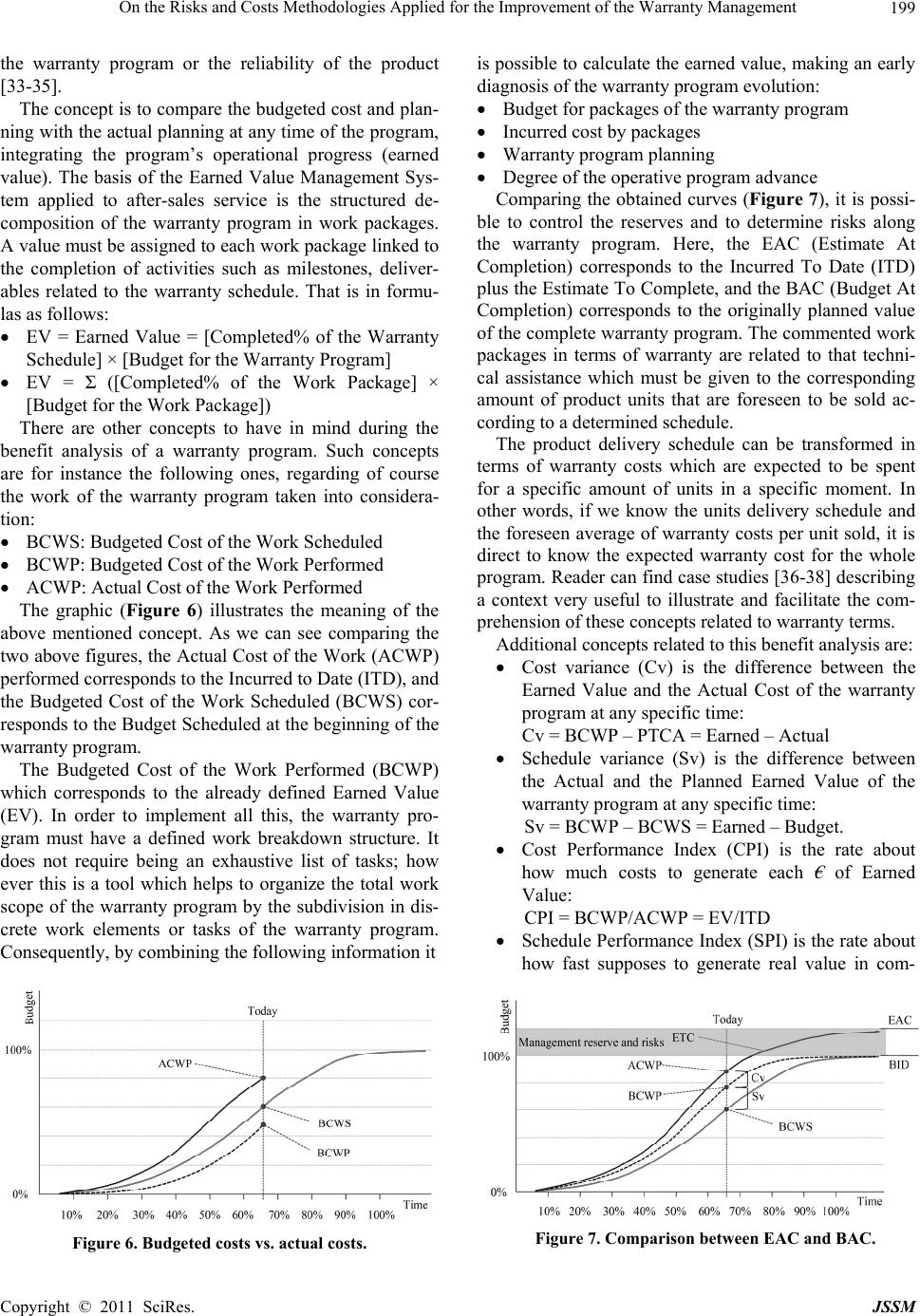

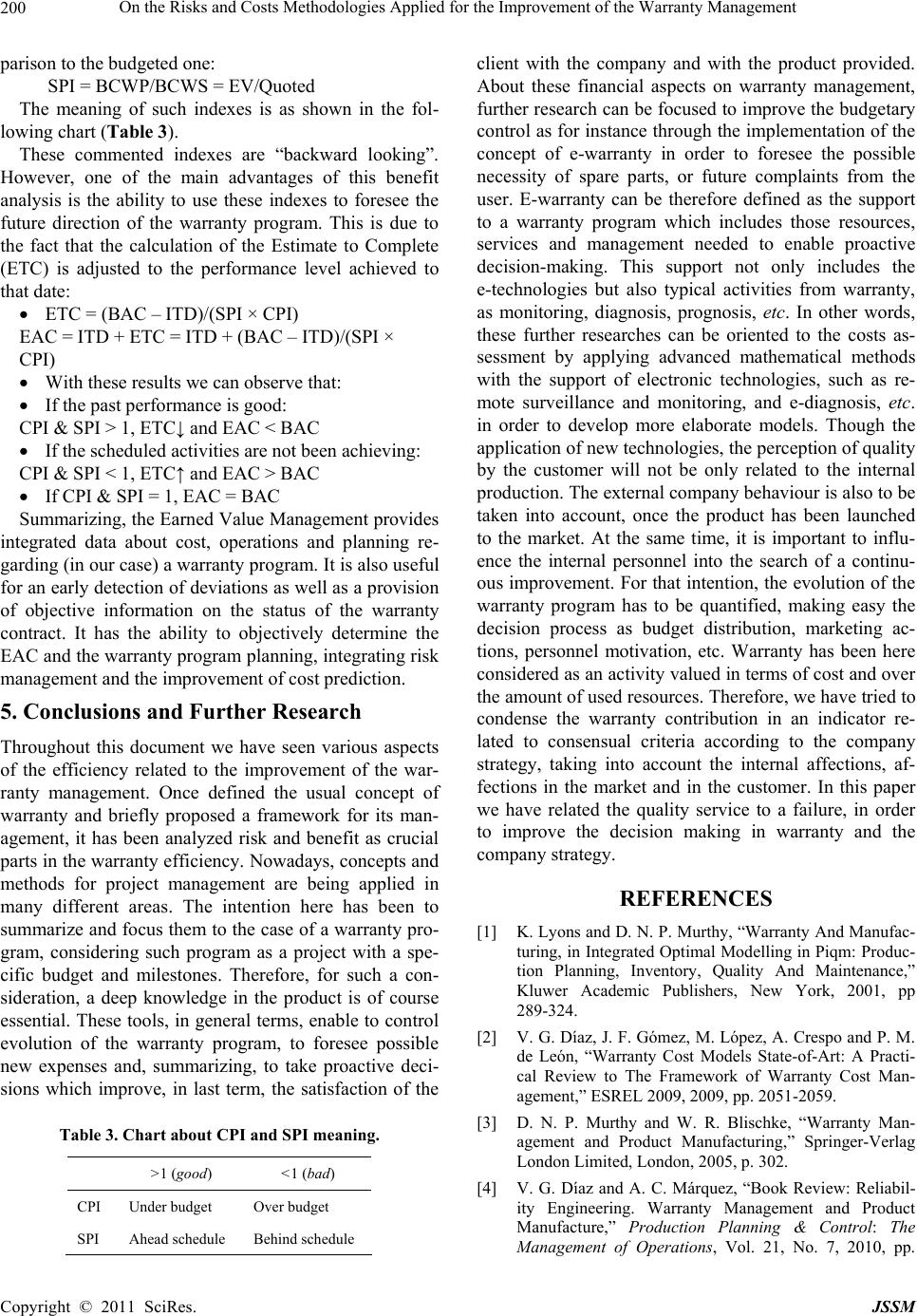

|