Journal of Service Science and Management

Vol.5 No.2(2012), Article ID:19195,11 pages DOI:10.4236/jssm.2012.52018

Does Board Experience Matter? Evidence from Foreign Direct Investment

![]()

1Department of Finance, National Taipei College of Business, Taipei, Taiwan; 2Department of Business Administration, Soochow University, Taipei, Taiwan.

Email: julialai@webmail.ntcb.edu.tw, lychen@scu.edu.tw

Received February 23rd, 2012; revised March 16th, 2012; accepted April 5th, 2012

Keywords: Board of Directors; Foreign Direct Investment; Corporate Governance; Resource Dependence Theory

ABSTRACT

This study contributes to the growing literatures on the importance of board expertise to their provision of counsel for management. By demonstrating that when announcing overseas investments, how a firm alleviates its liabilities of foreignness by board members possessing relevant experiences, the present work addresses the long-standing issue of what renders board the most effective. Drawing on expertise literature, we exam the efficacy of both director specific and heterogeneous experience, assessed by foreign market entry mode and targeted host country. The empirical results yield support for favorable impacts of both types of director experience. This finding corroborates the transition of board’s role from “passively” ratifying executive proposals, as predicted by agency theory, to “actively” instructing executives, as argued by resource dependence theory. The resource provision function of a board is further supported by greater benefits of director experience in situations of limited firm resources, assessed by executives’ associated experience. Finally, we find that directors who have operated independently from the CEO but without relevant experience cannot have significant influence on investment outcome. Our research result contributes to corporate governance research predominated by agency theory for the past decades, which presumes director independence as the foremost prerequisite for board effectiveness.

1. Introduction

The search for board characteristics that most contribute to a firm’s success has received considerable attention from both researchers and practitioners for the past decades. Conventional corporate governance research follows agency theory, arguing that the foremost prerequisite for an effective board mechanism lies in directors’ vigilance, which prompts active and independent overseeing of management [1], without considering directors’ individual competence. However, the implicit assumption underlying agency theory that directors are equivalently capable of fulfilling their fiduciary duties is challenged by recent anecdotal evidence that shows that some directors may not make meaningful contributions to board discussions [2,3]. Empirical studies have also failed to detect a consistent relationship between board independence and firm performance [4]. The disparity of findings reported by agency-based studies therefore suggests that elements of an effective board likely belong to variables yet to be identified.

To advance the understanding of board function beyond the limited construct as proposed by agency theory, in this study we draw on resource dependency theory and assess the value of directors’ advisory role. The resource dependence theory has received increasing academic attention in recent years [5-7]. Highlighting a board’s counsel function, resource dependency theory contends that the level of directors’ experience and expertise plays the most critical role in determining how effective a board can be. This distinct view may complement agency theory, which pays little attention to the fact that directors can be unequal in their capabilities to provide relevant expertise because of their heterogeneous knowledge domain. We evaluate how directors’ relevant experience assists executives to contend with challenges in firms’ foreign direct investment (FDI) undertakings, a crucial firm strategy in which a board is prevalently involved1. To systematically address the implications of director experience for firms’ FDI pursuits, we first discuss the challenges of FDIs to elucidate the board’s resource provision function. We then evaluate the value of various types of director FDI experience, including those within versus those outside the focal entry mode (joint venture or acquisition) or the host country (i.e., the country where the targeted entity is located). We further test whether the presence of executives’ associated experience moderates the significance of director experience to provide further support for a board’s advisory role. We particularly focus on the value of outside directors’ experience [3,8,15], as we intend to differentiate the contribution of board members from firm executives who serve mostly as inside directors. The event study approach is applied to assess FDI outcomes, following numerous studies on corporate governance and cross border investment strategies [7,16,17].

The present study may have critical implications for corporate governance research. Although the provision of advice has been increasingly recognized as an essential form of board involvement in addition to the board’s traditional monitoring function, few researchers have empirically investigated the direct relationship between the board’s advisory role and firm performance or have examined how directors’ individual experience may enhance a board’s ability to exercise this function. This study contributes to this line of research by specifying the performance effect of director experience on a vital firm strategy: FDI. Our findings can be instructive in solving the puzzle of whether and how director experience can advance firms’ strategy outcomes, as well as in clarifying the types and conditions that director experience offers the most effective assistance to the management.

Our study may also add to international business literature. Our aim to fill this research void regarding the link between director experience and FDI outcome can be insightful, because foreign investment is theoretically perceived as a superior strategy to arbitrage product and capital market imperfections across countries [18]; whereas in practice it usually incurs rigorous “liability of foreignness” and results in inferior outcomes. In view of the prevalence of cross-border investments among enterprises, as well as the board’s active participation in a firm’s internationalization process [19,20], findings from this study can elucidate this long-standing inquiry of how to realize purported FDI benefits by highlighting the vital yet rarely explored factor: board experience. In this regard, this study represents a critical step towards a clearer understanding of the determinants of FDI performance by showing whether, with aid from director experience, a firm can perform better in this highly integrated and globalized competitive environment.

The remainder of this paper is organized into several sections. In the next section, we review the literature and propose our hypotheses. Subsequently, we describe the sample construction and research methodology. We then report the empirical results of the study. Finally, we note conclusions and discuss our results.

2. Literature Review and Hypothesis Development

2.1. Challenges of FDIs

International business research indicates that investment across countries is much more complex and uncertain than its domestic equivalent. Differences in national culture, customer preferences, business practices, and institutional forces increase transaction costs when conducting investment abroad [12,19,20]. Furthermore, information asymmetry in foreign markets requires great efforts from executives to adjust to local market conditions, posting significant challenges in achieving strategic objectives [21,22]. Empirical studies demonstrate consistent evidence about the greater challenges in foreign investments, where foreign acquirers tend to pay more acquisition premiums [23] and suffer a higher failure rate [24], and in general, overseas investments receive much lower gains than their domestic equivalents [16,25]. The above evidence suggests that extracting synergies across markets is often impeded by tremendous obstacles. The inevitable transactional uncertainty confronting cross-border investments magnifies the hazard of managers making improper decisions, because such ambiguous situations necessitate a more comprehensive and sophisticated understanding in achieving precise judgment. Thus, management’s need of seeking counsel from knowledgeable third parties increases. This highlights the importance of the board’s advisory role in providing independent, intellectual counsel to supplement executives’ knowledge set. However, FDI faces challenges from multiple facets such as different entry modes and host country characteristics. This raises the question as to how directors’ various types of FDI experiences benefit a firm’s FDI pursuit, and under what circumstances director experience can best help in firm’s critical FDI situation. Below, we develop competing hypotheses by taking together expertise theory and the transition of the board’s role in establishing firm strategies.

2.2. Specific Learning from Director FDI Experience within Focal Entry Mode

According to expertise literature, individuals develop expertise on complex decision makings as they accumulate substantial amounts of relevant experience in that particular field [8,26]. In contrast to general decision makings of which information can be clearly processed and critical message can be articulately identified, complex decisions are usually subject to information overload, vague cause-and-effect relation, and ambiguity of unforeseen contingencies. With feedbacks generated from numerous trial and error processes, individuals develop a more complete understanding of the underlying causeand-effect relations of a complex strategy. Through this repeated refining process, individuals enhance their capability of distinguishing critical message from unimportant ones as found in the available information pool [27]. Furthermore, accumulating substantial experiential cases facilitates individuals in making constructive comparisons between current challenges and similar problems they have previously been exposed to, allowing them to choose the most relevant experiential lessons and apply them in resolving the focal problem. Consequently, via such experiential engagements, experienced individuals may develop a systematic, well-organized knowledge set regarding the undertaking of a complex strategy [26].

Considering the challenges inherent in FDI decisions, assistance from experienced directors therefore appears crucial. However, the aforementioned expertise argument also leads to the eventuality that only a director’s FDI experience within the focal entry mode, instead of dissimilar ones, is relevant and valuable. In particular, although joint ventures (JVs) and acquisitions (ACs) are both characterized by the involvement of an ex-anti target/partner selection, negotiation process, and ex-post integration efforts, the two modes face challenges that are qualitatively different. Contrary to the partial equity investment as found in JVs, the full-investment of capital in ACs involves in-depth resource commitment, which causes investing firms to be more vulnerable to environmental uncertainty, thereby leading to higher venture risk [20,25]. Further, ACs assume full control, and thus require greater efforts from investing firms to overcome integration challenges, such as how to harmonize culture conflicts between acquiring and target firms, reconcile discrepancy of organizational systems, and prevent turnover of acquired human capital [24]. By contrast, the partial control arrangement of JVs saves investing firms from having to exert extensive integration efforts. However, unlike ACs that brings the acquired entity into the acquirer’s existing governance system, JVs require extensive coordination efforts from the investing firms, because their shared management requires time-consuming coordination of joint activities between the partners [29]. The coordination challenges found in JVs is likely to be magnified in an international setting, because partners may have to strive even harder to achieve consensus due of dissimilar cultural and institutional backgrounds [22,30,31]. Summing up the above discussion, a pool of related experience within the focal entry mode may enable directors to develop relevant skills to apply on the focal FDI, whereas non-focal entry mode experience may generate little value. Thus, we have the following hypothesis:

Hypothesis 1: A firm’s international investment performance significantly benefits from directors’ prior crossborder investment experience that has the same entry mode of focal deal, but not from that having a different entry mode.

2.3. Specific Learning from Director FDI Experience within Focal Entry Mode

Another essential consideration affecting the performance effect of director FDI experience relates to whether it is from the country where the current targeted entity is located (i.e., the host country). In international business research, the value of firm executives’ international experience has been noted. However, previous research has not specifically considered how difference of experience gained from disparate countries affects its value to the targeted strategy [32]. Because of differences in the institutional environments among countries, knowledge for a country that creates competitive advantage may not generate the same advantage in another nation [21,30,33]. Therefore, while not incorporated in previous research, we argue that a unique value of director FDI experience exists when this experience is specific to the host country. In particular, such country specific experience may intensify executives’ awareness of local market structures, industry competition, cultural norms, common practices, and related regulations. Experienced directors can also apply local knowledge to assist executives in implementing the most effective management charts, and to adjust or change organizational resource allocations to fit the local market [34]. Furthermore, when managers gain insight into cross-cultural management relevant to the specific target culture from experienced directors, they are more able to strengthen the organization’s culture compatibility and build a harmonious relationship with the investee in the host country, thereby being more able to take advantage of the benefits available from different cultures [30]. Based on this discussion, we offer the following hypothesis:

Hypothesis 2: A firm’s international investment performance significantly benefits from directors’ prior crossborder investment experience in the targeted host country, but not from directors’ experience outside that country.

2.4. Learning from Directors’ Heterogeneous FDI Experience

The aforementioned arguments follow the insight of expertise research to posit that there are advantages from directors’ homogeneous experience, assessed by either entry mode or host country, that positively affect a firm’s FDI success. Although it is probable that directors’ experiential lessons dissimilar to the focal deal are of little value because of irrelevance, we develop a competing hypothesis here which states that board members’ heterogeneous experience, assessed by entry mode or host country, can be valuable in view of the transition the board’s role in setting firm strategy has had. A recent review of the board’s role indicates its gradual change from nominally rubber-stamping executives’ actions, to passively reviewing executives’ proposals, to more recently actively formulating strategies by guiding their content, context, and conduct [35,36]. The counseling role the board currently holds highlights the importance of directors possessing diverse experiences to offer executives ample strategic choices and help executives more thoroughly deliberate upon critical strategic issues, thereby optimizing a firm’s decisions. The learning accumulated through directors’ heterogeneous experiences is particularly critical in international environment than its domestic equivalent, because general problems in investments can be compounded by national cultures, language differences, political influences, and regulatory hurdles [32], making optimal decision more difficult to reach. Directors’ heterogeneous FDI experiences expose executives to a variety of feasible strategic alternatives and offer executives a pool of insightful comparative information on the potential markets, thereby facilitating more effectively their search for optimal strategy-environment fit within the uncertain international arena. The aforementioned discussion leads to the following hypothesis:

Hypothesis 3: A firm’s international investment performance significantly benefits from directors’ prior crossborder investment experience in non-focal host countries and in non-focal entry modes.

2.5. Contingent Importance of Director FDI Experience

If directors’ experience associated with FDI decisions can enhance a firm’s FDI performance, assistance from experienced directors should bring greater gains when executives possess less FDI experience. Specifically, managers who lack FDI-related experience should be less able to foresee the achievable synergies of FDI projects, to comprehend the underlying cause-and-effect relationships of FDI decisions, and to identify applicable experiential lessons from numerous prior engagements [32]. Firms are thus more likely to commit critical mistakes when forming FDI strategies if there is minimal access to third party expertise. Under such circumstances, improved decisions can be made when board directors have related experience and are able to give advice and counsel to managers on strategy formulation, partner/target choices, and implementation of strategic procedures. The critical importance of director FDI experience when executives lack such experience leads to the following hypothesis:

Hypothesis 4: A firm’s international investment performance benefits more from directors’ cross-border investment experience when the management team has relatively less FDI experience compared with firms whose management teams have more FDI experience.

3. Sample and Methodology

3.1. Sample Construction

To construct our FDI sample, an initial sample of international acquisitions (IACs) and international joint ventures (IJVs) made by US corporations is taken from the Security Data Corporation’s (SDC) Mergers and Corporate Transactions database. To be selected, an IAC/ IJV must have been made by a publicly held firm and have been completed. We then search for the announcement date from both the Lexis/Nexis database (including the Business Wire, PR Newswire, Southwest Newswire, Reuters, and United Press International) and the Dow Jones News Retrieval Service database (including the Dow Jones News Wire and the Wall Street Journal) for the 2002-2008 period. We obtain board member biographical data from 14As (proxy statements), 10Ks (audited annual reports), Standard & Poors Register of Corporations, Who’s Who in America, and Dun & Bradstreet’s Reference Book of Corporate Management.

In order to be included in the final sample, the FDI deal has to meet several additional criteria. First, the common stock returns for each of the sample firms has to be available in the Center for Research on Security Prices (CRSP) daily returns files over a period beginning 200 days prior to the FDI announcement and ending 60 days following the announcement. Second, sample firms must not have made other announcements five days before or five days after the initial announcement date, in order to avoid any confounding events that could distort the measurement of the valuation effects. Third, announcing firms that have no financial and operating data from the Compustat files are deleted. Lastly, we exclude financial industries (SIC code 60 - 69) due to unavailability of data. Our final sample includes 332 IAC and 267 IJV announcements made by US firms.

3.2. Research Design

To test our hypotheses, we estimate a series of hierarchical regression models that first examine the association between FDI performance and the control variables. We then sequentially enter our board experience variables and finally the moderators. The standard event-study method is used to examine stock price responses to corporate FDI announcements (our dependent variable). We follow Brown and Warner [37] by using the market model to obtain estimates of expected returns. The market model depicts the return on a security as varying with the market portfolio return, which is adjusted for the security’s risk factor. That is,

where

where  is the expected return of the ith firm at time t, given the available information

is the expected return of the ith firm at time t, given the available information  and the return on the market portfolio

and the return on the market portfolio , βi measures the risk or sensitivity of the firm’s return relative to the market portfolio, and αi is the intercept. The abnormal stock returns for the FDI announcements are calculated as the residual from the actual return and an expected return generated by the market model, with parameters αi and βi estimated over a period from 200 to 60 days before the initial announcements. Day 0 in event time is the date of the publication in which the company’s initial FDI announcement appears. The two-day period (day –1, day 0) cumulative abnormal returns (CARs) for each security are measured by the deviation of the security’s realized return over the two-day period from an expected return generated by the market model. Daily stock return information is collected from the CRSP returns files. The value weighted NYSE\AMEX\Nasdaq Index is used to measure market returns.

, βi measures the risk or sensitivity of the firm’s return relative to the market portfolio, and αi is the intercept. The abnormal stock returns for the FDI announcements are calculated as the residual from the actual return and an expected return generated by the market model, with parameters αi and βi estimated over a period from 200 to 60 days before the initial announcements. Day 0 in event time is the date of the publication in which the company’s initial FDI announcement appears. The two-day period (day –1, day 0) cumulative abnormal returns (CARs) for each security are measured by the deviation of the security’s realized return over the two-day period from an expected return generated by the market model. Daily stock return information is collected from the CRSP returns files. The value weighted NYSE\AMEX\Nasdaq Index is used to measure market returns.

3.3. Measures

Our independent variable, director FDI experience related to the focal entry mode, is calculated as follows. We first calculate the number of FDI cases (either IAC or IJV) individual directors have been involved in during their tenures as an executive or director of another firm over the five years preceding the announcement date. For each sample firm, we then sum the cases for all outside directors on the board to obtain a final number representing its board’s international investment experience. We exclude inside directors in the calculation to focus on a board’s unique contribution outside of what the firm’s executives can provide [3,8,15]. The following is the formula of director FDI experience:

FDI = IAC, IJVwhere FDI is the number of IAC or IJV cases that a director has been involved in when serving as a director or executive in F Company in year Y, which is within 5 years preceding the announcement date (t is the year of the investment announcement as determined by the announcement date). The number of companies that the directors serve in during this period is noted as N, and D is the number of directors that serve on the board of the focal firm. Director FDI experience cases are counted within the contexts of IACs and IJVs separately. We use a similar method to measure director FDI experience specific to the focal host country.

FDI = IAC, IJVwhere FDI is the number of IAC or IJV cases that a director has been involved in when serving as a director or executive in F Company in year Y, which is within 5 years preceding the announcement date (t is the year of the investment announcement as determined by the announcement date). The number of companies that the directors serve in during this period is noted as N, and D is the number of directors that serve on the board of the focal firm. Director FDI experience cases are counted within the contexts of IACs and IJVs separately. We use a similar method to measure director FDI experience specific to the focal host country.

We also include other variables that may influence FDI performance in our model specification. First, we control for corporate executives’ IAC and IJV experience to rule out their confounding impact, since firms can alternatively learn to master overseas investments internally from executives’ related experiences. We also control influences from firm size (naturl logarithm of net sales one year prior to the announcements), firms’ growth opportunity (Tobin’ Q, which equals the average ratio of the market value of the firm’s assets to the book value of the firm’s assets for the three fiscal years before the announcement), prior performance (return on asset one year prior to the announcements), debt-to-asset ratio (the ratio of total debt to total assets one year prior to the announcements), board independence( the proportion of outside directors on boards), and year and industry dummies following literature on corporate governance and international business (e.g., [7,16,17]).

4. Empirical Results

4.1. Sample Characteristics

Table 1 presents the means, standard deviations, and correlations for all the variables of the FDI sample. As can be seen, some of the correlations between the predictor variables prove significant. In particular, there is a high correlation among the director experience measures. In order to avoid the severe problem of multicollinearity, we respectively regresses our dependent variables on these measures. Fortunately, the variance inflation factor (VIF) values estimated in conjunction with our regression models do not suggest a problem with multicollinearity, as all the independent as well as control variables have VIFs below the 5.0 criterion advocated by Marquardt and Snee [38].

4.2. Cross-Sectional Regression Analyses

Table 2 examines whether a firm’s IAC pursuit benefits only from director IAC experience (as predicted by Hypothesis 1), or also from director IJV experience (as stated in Hypothesis 3). The positively significant coefficient of Director Experience with IAC (p < 0.05) shown in Model 2 suggests that firms receive significantly higher gains in their IAC engagements when their directors have more IAC experience. On the other hand, director IJV experience does not similarly impact firms’ IAC undertakings, as shown in Model 3. This result provides preliminary support for Hypothesis 1 within the sub

Table 1. Descriptive statistics and correlations.

Table 2. Cross-sectional regression analyses of 2-day announcement period abnormal returns of the IAC announcements.

sample of corporate IAC engagements. To test the robustness of these findings, we simultaneously include director IAC and IJV experience in Model 4. Our results remain unchanged, thus confirming the findings in Models 2 and 3 and providing strong support for Hypothesis 1. Finally, Model 5 tests if a firm’s IAC performance benefits more from its directors’ experience with IACs when the executives of the firm have relatively less IAC experience when compared with firms whose executives have more IAC experience. One variable, Difference in IAC Experience between Directors and Executives, which is defined as the difference between Director Experience with IAC and Executive Experience with IAC, is used to examine this hypothesis. The results show that the coefficient of Difference in IAC Experience between Directors and Executives is significantly and positively associated with abnormal returns at the five percent level. This evidence provides support for Hypothesis 4, and suggests that director IAC experience is a more significant value contributor when executives have less IAC experience.

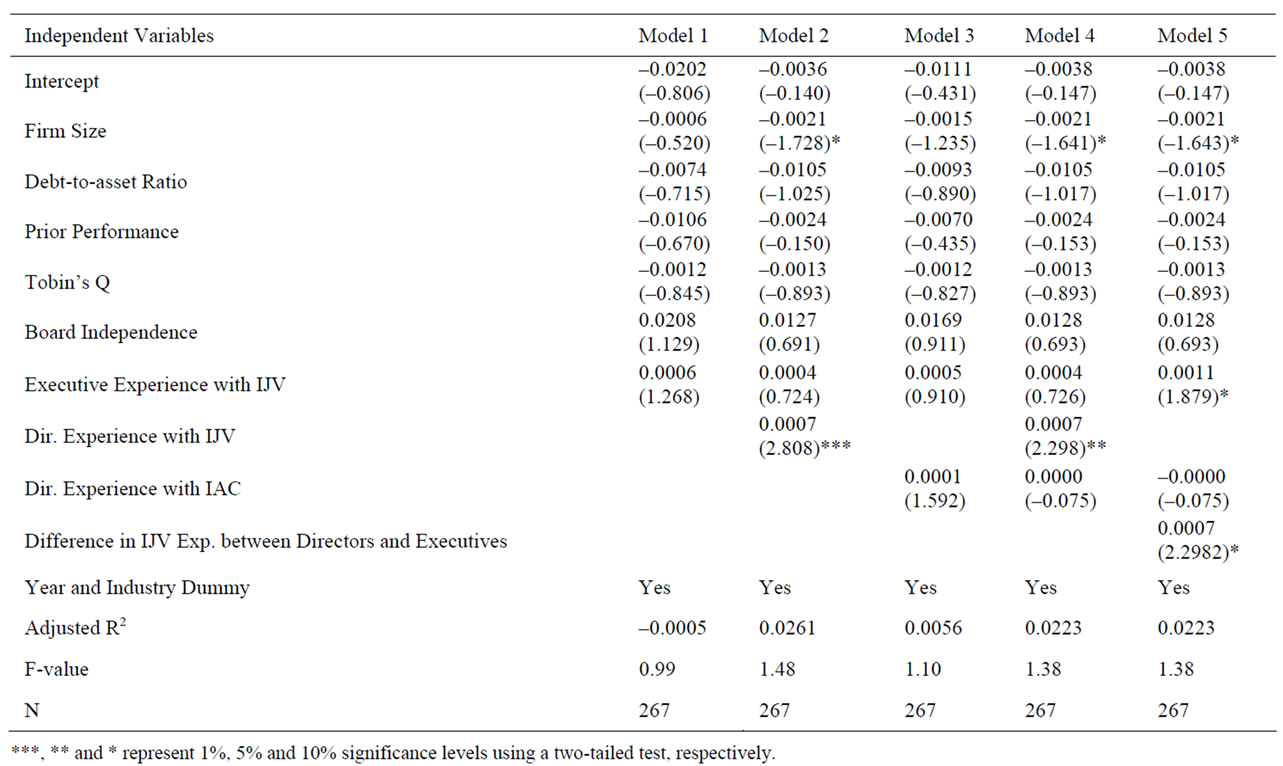

Table 3 examines the valuation effect of director’s entry-mode specific experience particularly on firms’ IJV engagements. Model 2 shows that the coefficient of Director Experience with IJV is significantly positive, suggesting that IJVs announced by firms with directors having more IJV experience is perceived as more worthwhile. In Model 3, we test the impact of director IAC experience on the stock market reactions to IJV announcements. We find that the coefficient of Director Experience with IAC is positive, but not significantly different from zero. Thus, the results in Models 2 and 3 strongly support Hypothesis 1 within the IJV subsample, as the abnormal returns of IJV announcements are positively related to director IJV experience, but not significantly associated with director IAC experience.

To investigate the robustness of these findings, we simultaneously include director IJV and IAC experience in Model 4. The results remain unchanged, suggesting that the market responds more favorably to announcements of IJV investments by firms whose directors have more IJV experience, and not those with more IAC experience. These results confirm the results in Models 2 and 3, and provide stronger support for value of director experience specific to IJV entry-mode. Moreover, Model 5 tests if a firm’s IJV performance benefits more from director IJV experience when corporate executives have relatively less such experience. The significant and positive coefficient of Difference in IJV Experience between Directors and Executives suggests that the market value of IJV investments increases with the difference in IJV experience between outside directors and executives, consistent with Hypothesis 4 when director FDI experience is assessed by directors’ prior involvement in IJV decisions.

Table 4 examines the competing hypotheses regarding whether a firm’s FDI performance only benefits from

Table 3. Cross-sectional regression analyses of 2-day announcement period abnormal returns of the ijv announcements.

Table 4. Cross-sectional regression analyses of 2-day announcement period abnormal returns of the FDI announcements.

director FDI experience specific to the host country (as predicted by H2), or also benefits from experience outside of host country (as predicted by H3). We create two variables to test these hypotheses. One is Director Experience with FDIs in the Same Country, estimated by the total number of FDI cases (including both IACs and IJVs) completed in the focal host nation by the sample firm’s outside directors over the past five years. The other is Director Experience with FDIs in Different Countries, estimated by the total number of FDI cases completed in non-focal host nations by the sample firm’s outside directors. As can be seen, the coefficient of Director Experience with FDIs in the Same Country variable is positive and significant at the 1% level (Model 2), suggesting a positive relationship between the focal firms’ FDI performance and their outside directors’ FDI experience specific to the investment country. Furthermore, the coefficient of Director Experience with FDIs in Different Countries is positively related to abnormal returns at the 1 percent level (Model 3). This evidence suggests that firms’ FDI performance can also significantly benefit from director FDI experience accumulated outside of the focal host country. Hypothesis 3, instead of Hypothesis 2, thus is supported. Model 4 tests the robustness of findings in Models 2 and 3 by taking together respective variables. Both experience measures are again found to be significant and positive, providing further support for Hypotheses 3. Finally, Model 5 tests if firms receive a greater gain from its directors’ prior host country investment experience when firm executives have relatively less such experience. We find that the coefficient of Difference in Country exp. between Director and Executive is significantly and positively associated with abnormal returns at the 5 percent level, and thus Hypothesis 4 is supported when directors’ host country experience is used as explanatory variables.

4.3. Robustness Tests

To test the robustness of our findings, we conduct several supplementary analyses. First, in our specification of the independent variables, we aggregate all outside board members’ experience with FDI decisions. To test if our results change when alternative aggregation approaches are applied, we redefine our experience measure as the average number of FDIs with which a director has had experience, either as an executive or board member. As expected, an average director FDI experience that is higher generates a more significantly positive impact on a firm’s FDI outcome (p < 0.05). Our finding of a positive impact of director experience is thus not sensitive to this alternative experience measure. We also examine whether our results are sensitive to the problem of endogeneity. The corporate governance literature has often identified the endogeneity problem of reverse causality between board member recruitment policies and corporate strategies [15]. That is, firms may specify their criteria in director election based on the anticipation of forthcoming strategic undertakings. To examine whether this possible endogeneity between director experience and FDI undertakings mediates our results, we exclude samples with directors who were recruited within the threeyear window prior to the focal FDI decision, and redo the analysis of Tables 3 and 4, with this new sample. The results are essentially unchanged. Our findings are, therefore, not driven by the problem of reverse causality. Finally we examine whether our results are subject to the potential bias of data skewness. We normalize each variable and re-perform regression analyses. The conclusions remain unchanged.

5. Discussions and Conclusions

Overall, findings of the present study confirm the value of director experiences in firms’ FDI undertakings. Our empirical analyses yield a consistent pattern of results that suggest that director experience particular to an entry mode (host country) significantly enhances a firm’s FDI performance in that specific mode (country). This suggests that directors’ FDI expertise accumulated from experience is desirable, because it forms tacit knowledge to assist managers more accurately and efficiently seize future strategic opportunities. The favorable impact from director specific experience takes on increased importance when the experience gap between directors and executives is larger, suggesting that executives’ lack of specific experience can be supplemented by expertise from FDI-experienced directors. We further find that director FDI experience not specific to the host country also positively influences firms’ FDI performance. Since directors are not limited to ratifying executives’ proposals passively, but also vigorously render advice regarding the feasibility of strategic options [36], their dissimilar FDI experience may provide managers with insightful comparisons to select a well suited host country. The advantage of directors’ heterogeneous experience can be salient in a FDI scenario because of the high environmental uncertainty surrounding it, augmenting the benefits of more thorough assessments of strategic alternatives to support a choice that better fits the focal condition.

Our research result can also add to international business research. The role of the board in corporate internationalization process has gained increasing prominence over the past years [12]. However, empirical evidence to date has mostly been limited to the relationship between board mechanism and the level of internationalization [12,13,19]. Further investigation into how the board influences the context of internationalization, however, is left little addressed in international business research. By investigating how directors apply associated experience to assist in FDI decision makings, findings of the present study can help to further the understanding of the contribution of the board in a firm’s internationalization process.

6. Acknowledgements

Jung-Ho Lai acknowledges funding from the National Science Council in Taiwan (NSC 99-2410-H-141-003- MY2).

REFERENCES

- M. C. Jensen, “The Modern Industrial-Revolution, Exit, and the Failure of Internal Control-Systems,” Journal of Finance, Vol. 48, No. 3, 1993, pp. 831-880. doi:10.2307/2329018

- C. B. Carter and J. W. Lorsch, “Back to the Drawing Board: Designing Corporate Boards for a Complex World,” Harvard Business School Press, Boston, 2004.

- Y. Y. Kor and C. Sundaramurthy, “Experience-Based Human Capital and Social Capital of outside Directors,” Journal of Management, Vol. 35, No. 4, 2009, pp. 981- 1006. doi:10.1177/0149206308321551

- C. M. Daily, D. R. Dalton and A. Cannella, “Introduction to Special Topic Forum Corporate Governance: Decades of Dialogue and Data,” Academy of Management Review, Vol. 28, No. 3, 2003, pp. 371-382. doi:10.5465/AMR.2003.10196703

- K. T. Haynes and A. Hillman, “The Effect of Board Capital and CEO Power on Strategic Change,” Strategic Management Journal, Vol. 31, No. 11, 2010, pp. 1145- 1163. doi:10.1002/smj.859

- A. J. Hillman, M. C. Withers and B. J. Collins, “Resource Dependence Theory: A review,” Journal of Management, Vol. 35, No. 6, 2009, pp. 1404-1427. doi:10.1177/0149206309343469

- J. Tian, J. Haleblian and N. Rajagopalan, “The Effects of Board Human and Social Capital on Investor Reactions to New CEO Selection,” Strategic Management Journal, Vol. 32, No. 7, 2011, pp. 731-747. doi:10.1002/smj.909

- M. L. McDonald, J. D. Westphal and M. E. Graebner, “What do They Know? The effects of Outside Director Acquisition Experience on Firm Acquisition Performance,” Strategic Management Journal, Vol. 29, No. 11, 2008, pp. 1155-1177. doi:10.1002/smj.704

- C. M. Beckman and P. R. Haunschild, “Network Learning: The Effects of Partners’ Heterogeneity of Experience on Corporate Acquisitions,” Administrative Science Quarterly, Vol. 47, No. 1, 2002, pp. 92-124. doi:10.2307/3094892

- J. L. Coles, N. D. Danie and L. Naveen, “Boards: Does One Size Fit All?” Journal of Financial Economics, Vol. 87, No. 2, 2008, pp. 329-356. doi:10.1016/j.jfineco.2006.08.008

- C. de Villiers, V. Naiker and C. J. van Staden, “The Effect of Board Characteristics on Firm Environmental Performance,” Journal of Management, Vol. 37, No. 6, 2011, pp. 1636-1663. doi: 10.1177/0149206311411506

- H. L. Chen, “Does Board Independence Influence the Top Management Team? Evidence from Strategic Decisions toward Internationalization,” Corporate Governance: An International Review, Vol. 19, No. 4, 2011, pp. 334-350. doi:10.1111/j.1467-8683.2011.00850.x

- J. Y. Lu, B. Xu and X. H. Liu, “The Effects of Corporate Governance and Institutional Environments on Export Behaviour in Emerging Economies Evidence from China,” Management International Review, Vol. 49, No. 4, 2009, pp. 455-478. doi:10.1007/s11575-009-0004-9

- L. Tihanyi, R. A. Johnson, R. E. Hoskisson and M. A. Hitt, “Institutional Ownership Differences and International Diversification: The Effects of Boards of Directors and Technological Opportunity,” Academy of Management Journal, Vol. 46, No. 2, 2003, pp. 195-211. doi:10.2307/30040614

- R. W. Masulis, C. Wang and F. Xie, “Corporate Governance and Acquirer Returns,” Journal of Finance, Vol. 62, No. 4, 2007, pp. 1851-1889. doi:10.1111/j.1540-6261.2007.01259.x

- S. C. Chang, S. S. Chen and J. H. Lai, “The Wealth Effect of Japanese-US Strategic Alliances,” Financial Management, Vol. 37, No. 2, 2008, pp. 271-301. doi:10.1111/j.1755-053X.2008.00013.x

- J. H. Lai, S. C. Chang and S. S. Chen, “Is Experience Valuable in International Strategic Alliances?” Journal of International Management, Vol. 16, No. 3, 2010, pp. 247- 261. doi:10.1016/j.intman.2010.06.004

- Y. Wang, “The Analysis on Environmental Effect of Logistics Industry FDI,” Journal of Service Science and Management, Vol. 2, No. 4, 2010, pp. 377-381.

- C. Barroso, M. M. Villegas and L. Perez-Calero, “Board Influence on a Firm’s Internationalization,” Corporate Governance: An International Review, Vol. 19, No. 4, 2011, pp. 351-367. doi:10.1111/j.1467-8683.2011.00859.x

- D. K. Datta, M. Musteen and P. Herrmann, “Board Characteristics, Managerial Incentives, and the Choice between Foreign Acquisitions and International Joint Ventures,” Journal of Management, Vol. 35, No. 4, 2009, pp. 928-953. doi:10.1177/0149206308329967

- J. K. Kang and J. M. Kim, “Do Foreign Investors Exhibit a Corporate Governance Disadvantage? An Information Asymmetry Perspective,” Journal of International Business Studies, Vol. 41, No. 8, 2010, pp. 1415-1438. doi:10.1057/jibs.2010.18

- J. J. Reuer and M. P. Koza, “Asymmetric Information and Joint Venture Performance: Theory and Evidence for Domestic and International Joint Ventures,” Strategic Management Journal, Vol. 21, No. 1, 2000, pp. 81-88. doi:10.1002/(SICI)1097-0266(200001)21:1<81::AID-SMJ62>3.0.CO;2-R

- A. Bris and C. Cabolis, “The Value of Investor Protection: Firm Evidence from Cross-Border Mergers,” Review of Financial Studies, Vol. 21, No. 2, 2008, pp. 605-648. doi:10.1093/rfs/hhm089

- K. Shimizu, M. A. Hitt, D. Vaidyanath and V. Pisano, “Theoretical Foundations of Cross-Border Mergers and Acquisitions: A Review of Current Research and Recommendations for the Future,” Journal of International Management, Vol. 10, No. 3, 2004, pp. 307-353. doi:10.1016/j.intman.2004.05.005

- W. N. W Azman-Saini, A. Z. Baharumshah and S. H. Law, “Foreign Direct Investment, Economic Freedom and Economic Growth: International Evidence,” Economic Modelling, Vol. 27, No. 5, 2010, pp. 1079-1089. doi:10.1016/j.econmod.2010.04.001

- K. A. Ericsson and A. C. Lehmann, “Expert and Exceptional Performance: Evidence of Maximal Adaptation to Task Constraints,” Annual Review of Psychology, Vol. 47, No. 3, 1996, pp. 273-305. doi:10.1146/annurev.psych.47.1.273

- K. A. Ericsson and N. Charness, “Expert Performance its Structure and Acquisition,” American Psychologist, Vol. 49, No. 8, 1994, pp. 725-747. doi:10.1037/0003-066X.49.8.725

- D. Morschett, H. Schramm-Klein and B. Swoboda, “Decades of Research on Market Entry Modes: What do We Really Know about External Antecedents of Entry Mode Choice?” Journal of International Management, Vol. 16, No. 1, 2010, pp. 60-77. doi:10.1016/j.intman.2009.09.002

- M. Musteen, D. K. Datta and P. Herrmann, “Ownership Structure and CEO Compensation: Implications for the Choice of Foreign Market Entry Modes,” Journal of International Business Studies, Vol. 40, No. 2, 2009, pp. 321-338. doi:10.1057/jibs.2008.63

- J. F Hennart and M. Zeng, “Cross-cultural Differences and Joint Venture Longevity,” Journal of International Business Studies, Vol. 33, No. 4, 2002, pp. 699-716. doi:10.1057/palgrave.jibs.8491040

- J. L. Johnson, J. B. Cullen, T. Sakano and J. W. Bronson, “Drivers and Outcomes of Parent Company Intervention in IJV Management: A Cross-cultural Comparison,” Journal of Business Research, Vol. 52, No. 1, 2001, pp. 35-49. doi:10.1016/S0148-2963(99)00081-8

- B. B. Nielsen and S. Nielsen, “The Role of Top Management Team International Orientation in International Strategic Decision-making: The Choice of Foreign Entry Mode,” Journal of World Business, Vol. 46, No. 2, 2011, pp. 185-193. doi:10.1016/j.jwb.2010.05.003

- J. D. Collins, T. R. Holcomb and S. T. Certo, M. A. Hitt and R. H. Lester, “Learning by Doing: Cross-Border Mergers and Acquisitions,” Journal of Business Research, Vol. 62, No. 12, 2009, pp. 1329-1334. doi:10.1016/j.jbusres.2008.11.005

- S. Slater, S. Paliwoda and J. Slater, “Ethnicity and Decision Making for Internationalization,” Management Decision, Vol. 45, No. 10, 2007, pp. 1622-1635. doi:10.1108/00251740710837997

- J. Petrovic, “Unlocking the Role of a Board Director: A Review of the Literature,” Management Decision, Vol. 46, No. 9, 2008, pp. 1373-1392. doi:10.1108/00251740810911993

- A. Pugliese, P. J. Bezemer, A. Zattoni, M. Huse, F. A. J. Van den Bosch and H. W. Volberda, “Boards of Directors’ Contribution to Strategy: A Literature Review and Research Agenda,” Corporate Governance: An International Review, Vol. 17, No. 3, 2009, pp. 292-306. doi:10.1111/j.1467-8683.2009.00740.x

- S. J. Brown and J. B. Warner, “Using Daily Stock Returns: The Case of Event Studies,” Journal of Financial Economics, Vol. 14, No. 1, 1985, pp. 3-31. doi:10.1016/0304-405X(85)90042-X

- D. W. Marquardt and R. D. Snee, “Ridge Regression in Practice,” American Statistician, Vol. 29, No. 1, 1975, pp. 3-20. doi:10.2307/2683673

- Y. C. Lien, J. Piesse, R. Strange and I. Filatotchev, “The Role of Corporate Governance in FDI Decisions: Evidence from Taiwan,” International Business Review, Vol. 14, No. 6, 2005, pp. 739-763. doi.org/10.1016/j.ibusrev.2005.08.002

NOTES

1For example, Lien, Piesse, Strange and Filatotchev (2005) find that board size and the presence of independent directors positively influence a firm’s tendency to undertake FDIs. Musteen, Datta and Herr- mann (2009) and Datta, Musteen and Herrmann (2009) show that board independence, CEO duality, and inside director ownership significantly impact a firm’s choice of entry mode into foreign markets.