Modern Economy

Vol.3 No.3(2012), Article ID:19159,7 pages DOI:10.4236/me.2012.33039

Central Bank Communication, Ambiguity and Market Interest Rates: A Case Study

Economics, Law and Institutions Department, University of Rome “Tor Vergata”, Rome, Italy

Email: {carlo.digiorgio, enzo.rossi}@uniroma2.it

Received January 7, 2012; revised February 19, 2012; accepted March 1, 2012

Keywords: ECB Communication; Ambiguity Indicators; Structural VAR

ABSTRACT

We asked a representative sample of European banks to judge messages released by ECB members (from February 1999 to February 2000) in terms of their ambiguity. In this paper, we use our survey to derive a definition of ambiguity and to evaluate ECB communication. A Structural Vector Autoregression model is estimated and the results show that ambiguous messages were able to affect agents’ expectations for a limited period after a speech by ECB members; moreover, they show that ambiguity had temporary effects also on volatility and moved rates away from the policy rate.

1. Introduction

The existence of a trade-off between credibility and flexibility of monetary policies is well known in the traditional literature. The meaning of such trade-off is the following: if monetary authorities perceive that the inflation bias due to a lack of credibility makes their final goals impossible to reach, they may find convenient to disclose their private information in order to gain more credibility (i.e., sharing information plays the same role of a pre-commitment); however, if monetary authorities choose to pursue stabilization, some of their strategies are more effective if they are unexpected1. Given this trade-off, we wondered whether an ambiguous communication could be a strategic choice aimed at gaining flexibility or not. More precisely, we wondered whether an ambiguous communication could make central banks less accountable or central banks’ goals easier to achieve. We believed that the answer should come from empirical studies on the effect of ambiguity on direction and volatility of interest rates. More recent literature has explored the impact of communication on the direction of interest rate, and examined the volatility of interest rates during the process of adjustment. But here, volatility is related to market movements due to the inclusion of news, and not also, if any, to ambiguity of communication. On the other side, some authors2 point out that classify and then code on a numerical scale all statements according their content and intention, is necessarily subjective and there may be misclassifications. In this view, also ambiguity of communication should be emphasized, stressing out the specific difficulty in coding it. In this literature, it could not be possible to find any definition (and measure) of ambiguity that could serve our purpose. So, we changed the focus and it has been decided to provide a new approach to ambiguity that could be of some practical use. The idea was to ask the market operators itself about their perception about intention and ambiguity of the speeches of the Central Bank. In order to do that, it has been surveyed a representative sample of European banks asking them to judge the messages released by ECB members from the 2nd of February 1999 to the 22nd of February 2000 in terms of their ambiguity. The survey was conducted immediately after the period considered. The banks sample involved in the survey include big multinational European banks: two Italian banks, one Spanish, one German, one Dutch, one French, one Luxembourgian, one Austrian, as well as other minor banks. At the date of the survey, the banks sample covered about 90 percent of the interbank transactions. Questions were addressed to treasury managers in charge of each bank. The survey has not been updated to include more recent years, since data were gathered and sent to the banks treasury manager, but over the time there were various bank fusions and acquisitions, so that it was not possible to update and replicate the survey with a homogenous sample. In this view, our model can be considered a simulation exercise related to a particular period (the first year) of the ECB history. The choice of ECB and Euro’s starting period was made not in order to evaluate the Central Bank’s policy, but because this offers a special opportunity to assess the relationship between communication and the management of money markets in general. In the following sections, the answers provided by the surveyed sample to define and measure ambiguity have been used. In terms of our new definition, we conclude that ECB communication from February 1999 to February 2000 was in general perceived as ambiguous by agents operating in European money markets. Also, we provide examples to show that, if ambiguity is measureable, its effect on money markets can be quantified. In particular, a structural VAR model has been used to capture the effects of ambiguity on a selected set of money market variables, noting that the identification of the model support the causal link from ambiguity to the volatility and the other variables but it does not support the contrary3. For the interval of time taken into consideration, the results of the estimate are the following:

1) Messages were able to affect expectations, and these in turn affected market rates;

2) Ambiguity had a strong effect on volatility;

3) Ambiguity moved rates away from the policy rate.

Given these results, we argue that ambiguity of ECB communication was not a strategic choice, but the result of a lack of coordination among members, who didn’t share a homogeneous view on the stance of monetary policy. We can speak of lack of clearness of the monetary policy as a whole, in this restricted sense. We want to point out that this paper is not aimed to criticize ECB. Notice that at the time we collected the data, we had to make a choice about the central bank whose communication was to be investigated. We chose to focus on ECB communication because ECB was recently established and ambiguity could arise from many different sources (i.e., strategic choices, different backgrounds of ECB members, initial lack of coordination).The main result is that, in the case studied, ambiguity wasn’t a strategic choice.

Considering the related literature, many economists focused on central banks’ communication in general. Among them, Blinder (1998) showed that efficiency of markets is enhanced if central bank policies are disclosed to the public [7]. Rafferty and Tomljanovich (2002) wondered whether the predictability of financial markets improved or worsened since 1994, that is since when the FED decided a more open public disclosure [8]. Using methods similar to Campbell and Shiller (1989) [9], they concluded that forecasting errors decreased. Dornbusch et al. (1998) highlighted the importance of the ability to communicate to the public for the success of ECB [10]. Bernanke (2004) has acknowledged that communication plays a seminal role in improving the effectiveness of policy [11].

The literature on central bank communication has shown it may use various channels and that there is no optimal central bank communication strategy, since one strategy could work for one central bank, but may not work for the other (de Haan et al. 2007) [12].

Coming to the importance of the speeches of a Central Bank board, as an important way of communication, there are specific studies.

Connolly and Kohler (2004), estimate the impact of four types of news on financial markets expectations of future interest rates: domestic macroeconomics news, foreign news, monetary policy surprises and central bank communication [13]. Their results suggest that central bank communication does not give a large contribution to overall movements in interest rate futures, adding only a few basis points to the standard deviation of interest rates on the day which the communication occurs, whereas in comparison they find that domestic and foreign macroeconomic news make a wider contribution to the variance of changes in interest rate futures. But this is not all the story, because other authors reach different results, which stress out the importance of communication.

Blinder et al. (2008), focus their survey on central bank communication on high-frequency channels, such as announcements and speeches or interviews, noting that it is not always straightforward to determine the timing of the communication event which causes financial markets to react. Ehrmann and Fratzscher (2007), compare the timing of communication of the FED, the ECB, and the Bank of England. They find that on average on the days preceding the monetary policy meetings, there is less communication compared to other days, showing that the intensity of communication is different before rather than after meetings for all three central banks, indicating the attempt of central banks to prepare markets for the upcoming meeting. They find that speeches and interviews by FED members generally affect financial markets in the intended direction, since statements suggesting tightening lead to high rates and viceversa [14]. Connolly and Kohler (2004), Reeves and Sawicki (2007) [15], among others, study the effects of central bank communication events on the volatility of financial variables, arguing that if communication affect the returns on the assets their volatility increase on days of central bank communications. As pointed out by Blinder et al. (2008), the researchers study whether the central bank communications create news, and whether they move the financial variables, not whether they move markets in the right direction. Reeves and Sawicki (2007), underline the possibility that communication may be endogenous, that is the central bank may choose to communicate at a particular time because of a sudden change in the economic situation or some other news, so that asset prices would probably be more volatile on the days of communication, but not necessarily because the communication may affect the volatility of asset prices, whereas the endogeneity could be a minor problem when the dates of major communications are known in advance. Kohn and Sack (2004), about Federal Open Market Committee (FOMC) communication, find that volatility of the financial variables increases significantly when there are statements released by the FOMC members, and these changes show that bank communication conveys relevant information for the markets [16]. However, it is not clear whether volatility is related to market movements due to the inclusion of news, and not also, if any, to ambiguity of communication. This turns out to the relevant methodological problem. How is pointed out by Blinder et al. (2008), classify and then code on a numeric scale all statements, according their content and intention (even more according their ambiguity), is necessarily subjective and there may be misclassifications. Moreover, when statements are identified through media intermediaries, these could be selective or misleading in their reports. In our survey, we avoid this arbitrariness collecting personally the original speeches and asking their judgment about statements to a selected sample of market participants, so for the first time it is possible to trace the direct perception of the markets.

In a first paper on this topic, Fontani et al. (2001), for the first time used a dataset of speeches of ECB members, as to give an evaluation of effectiveness of communication in conducting monetary policy. They asked perception directly to market operators [17]. Fratzscher (2008) has made the same in order to evaluate the effectiveness of oral intervention on exchange rate policy. However, his measure of markets perception of the meaning of each speech is judgmental, since it is made by the author itself and this, admittedly, is a factor of weakness of this work [18]. As for our knowledge, while many authors focused on communication tout court, nobody studied the specific effects of an ambiguous communication. We believe that this is due to the fact that in the literature the notion of ambiguity (or transparency) is too judgmental to be of any practical relevance.

Winkler (2000) tried to provide a better definition of transparency. He concluded that what matters is “common understanding” between central banks and their audience [19]. We buy his point and ask ECB audience to judge ECB communication. We come up with a set of measures for ambiguity that allow us to investigate the effects of ambiguity of communication on markets in a very original manner. The paper is organized as follows:

Section 2 is a description of the survey sent to the sampled European banks; in particular, it explains how the questions included in the survey were chosen and how the sample to be surveyed was selected. Section 3 introduces the structural VAR model and discusses the impulse response functions in order to assess the dynamic behavior of the model. Section 4 summarizes the main results.

2. The Survey: Choice of Questions and Sample Selection

The survey was divided into two parts. The first was about ECB members (speakers)4; the second was about the messages (speeches) that those members have released in both formal and informal events.

In the first part, an opinion about each speaker’s influence on European money markets was asked.

The second part included a set of 135 messages passed on to the public by ECB members from the 2ND of February 1999 to the 22ND of February 2000. These 135 messages included all messages regarding monetary policy. Also, they included messages regarding exchange rates and fiscal policy. The reason for this choice was that traders usually have a clear perception of the correlation between fiscal policy and monetary policy. So, we thought that they were able to infer the stance of monetary policy even from messages regarding fiscal matters5.

The survey was conducted immediately after the period considered. Questions were addressed to treasury managers in charge of each bank.

For each one of the 135 messages banks were asked to give two judgments.

The first one was about the direction of ECB intervention that could be inferred from the message (i.e., a rise or a decrease of the official rate, or no intervention at all), and the measure of such intervention (i.e., less than 50 basis points, equal or higher than 50 basis points).

The second one was about the ambiguity of the message. In particular, the banks were asked to judge each message: “very clear”, “fairly clear”, or “ambiguous”.

Obviously, some answer could be affected by the memory of what happened after the messages were released. So, even if the sample was asked to focus only on the content of each single message without thinking about the past, data could be biased. In order to answer this question, we have examined those messages which gave wrong anticipation. If the sample had a memory of what happened later, answers had to be biased systematically. However, we found a correct interpretation of this kind of messages.

For this reason, we feel comfortable that the results do not overestimate the effect of communication on agents’ expectations.

The sample consists of 21 subjects operating in European money markets (i.e. commercial banks, investment banks and other financial institutions). It is impossible to disclose the real names of these 21 subjects for privacy reasons. However, all of them are financial institutions of large size and most of them are included in the EONIA group. They are from many different European countries and all of them operate both in their home countries and abroad. So, they are a balanced and representative sample of agents operating in European money markets.

The following example gives an idea about the survey.

On February the 2ND 1999, Noyer (ECB Vice President) said:

“I am not concerned that Europe’s single currency will be overly strong against the US dollar and the Japanese yen, signaling the ECB might not need to cut interest rates early in 1999.”

After reading this message, 20 banks chose the following interpretation: ECB will leave interest rates unchanged; only 1 bank chose: ECB will cut interest rates by less than 50 basis point. Also, 10 banks judged this message “very clear”, 9 banks judged it “fairly clear”, and 2 banks judged it “ambiguous”.

3. The Effect of Ambiguity on Money Markets: A Structural VAR Model

Based on previous hypothesis on the role of ECB communication, a Structural Vector Autoregression (SVAR) framework6 was used to consider the behavior of a set of variables and to see if the ambiguity of speeches can have significant effects on money market rates and may influence the financial markets agents’ expectations. The following variables vector is considered to model

(1)

(1)

that is, a data set where Voleurib is one month Euribor interest rate volatility, as representative of market response to monetary policy impulse. Other interest rates, like Eonia were tested, which seems more in line with the view of ECB itself, but the results of the SVAR model were substantially the same. However, was pointed to Euribor rate as the rate which can better synthesize the status of monetary markets.

Expdisp is the dispersion of agents’ expectations about the direction and the magnitude of ECB intervention. The variable expectation that represents such expectations is a qualitative variable. It gets value 1 when a message is interpreted as an anticipation of a cut of official rates greater than 50 b.p., value 2 when a message is interpreted as an anticipation of a cut of official rates smaller than 50 b.p., value 3 when a message is interpreted as an anticipation of unchanged official rates, value 4 when a message is interpreted as an anticipation of a rise of official rates smaller than 50 b.p., value 5 when a message is interpreted as an anticipation of a rise of official rates greater than 50 b.p.

Eupolsq is the squared difference between the Euribor rate and the policy rate, identified as the ECB financing auction rate. It can be recalled that in the traditional view, the Central Bank handles policy rates in order to influence a selected market rate, which represents its operational target.

Amb is a qualitative variable that gets value 1 when a message is judged by the banks “very clear”, value 2 when a message is judged “fairly clear”, and value 3 when a message is judged “ambiguous”, then it is weighted in each point7.

The variables are all stationary, only the policy rate is taken in first difference since is I(1). The time frequency of the variables is the ECB communication periods. Our specification is oriented to model these variables by means of a vector autoregressive model since it can analyze the relationship between these variables and capturing their time development. The identification scheme allows for a contemporaneous interaction between voleurib, expdisp, eupolsq and amb. To account for these features, we specify a SVAR model given by the expression:

(2)

(2)

where Yt is the vector of endogenous variables (1),  is a vector of exogenous variables: in our case it contains only the policy interest rate, A(L) and B(L) are convergent matrices polynomial in the lag operator L,

is a vector of exogenous variables: in our case it contains only the policy interest rate, A(L) and B(L) are convergent matrices polynomial in the lag operator L, ![]() is the vector of structural shocks where its variance-covariance matrix contains orthonormal variables uncorrelated and with unit variance. In the terminology of Amisano and Giannini (1997), this is an AB-model, where A and B are two square and invertible matrices. The A matrix directly applies to the observable quantities and contains the contemporaneous interactions between the endogenous variables, while the B matrix applies to the unobservable variables of the

is the vector of structural shocks where its variance-covariance matrix contains orthonormal variables uncorrelated and with unit variance. In the terminology of Amisano and Giannini (1997), this is an AB-model, where A and B are two square and invertible matrices. The A matrix directly applies to the observable quantities and contains the contemporaneous interactions between the endogenous variables, while the B matrix applies to the unobservable variables of the ![]() vector of structural shocks. Premultiplying both sides of Equation (2) by

vector of structural shocks. Premultiplying both sides of Equation (2) by  gives the reduced form associated with the structural model:

gives the reduced form associated with the structural model:

(3)

(3)

where ,

, and

and  are the residuals of the reduced form. Then these residuals can be related to the structural shocks by the following general structural model:

are the residuals of the reduced form. Then these residuals can be related to the structural shocks by the following general structural model:

(4)

(4)

The first step of SVAR analysis is based on the estimation of the reduced form, where the lag truncation order has been set to 3 using standard test procedures. The second step of SVAR analysis consists in the identification and FIML estimation of the parameters in  and B8, for this purpose, all the sample information needed is contained in the estimated variance-covariance matrix

and B8, for this purpose, all the sample information needed is contained in the estimated variance-covariance matrix ![]() of the reduced form disturbances

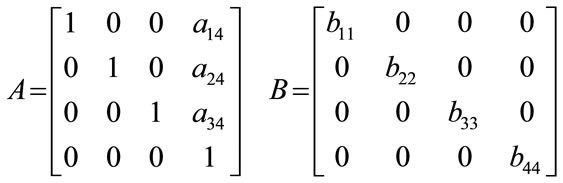

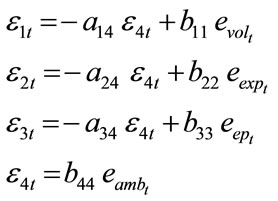

of the reduced form disturbances . In our model the set of linear constraints leads to the following form of A and B:

. In our model the set of linear constraints leads to the following form of A and B:

so, the above matrices lead at the following set of restrictions on the relation between reduced form and structural shocks of the Equation (4):

(5)

(5)

Equation (5) attribute innovations in voleurib, expdisp and eupolsq, to amb innovation and own structural shocks, respectively. Since the other parameters of the  matrix are statistically not significant at the 5% level, they have been jointly deleted, leading to a situation of overidentification of the model, that has been validated by a LR test9.

matrix are statistically not significant at the 5% level, they have been jointly deleted, leading to a situation of overidentification of the model, that has been validated by a LR test9.

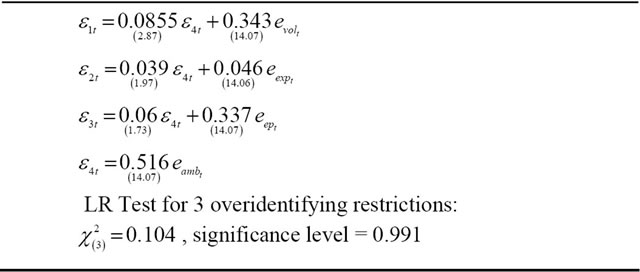

In Table 1 estimates of the A and B parameters of the model proposed are presented along with the associated t-values in brackets, where it can be noted that all the innovations are positively affected by amb innovation. In the last step of the analysis it is of interest to study the dynamic effects produced by the structural shocks, in particular by the ambiguity shock, on the behaviour of the considered variables. In order to perform this simulation analysis the techniques used are the IRF (Impulse Response Functions) for the four variables. In particular, the interest is to the study of the dynamic responses of

Table 1. Structural equations estimates of the overidentified model.

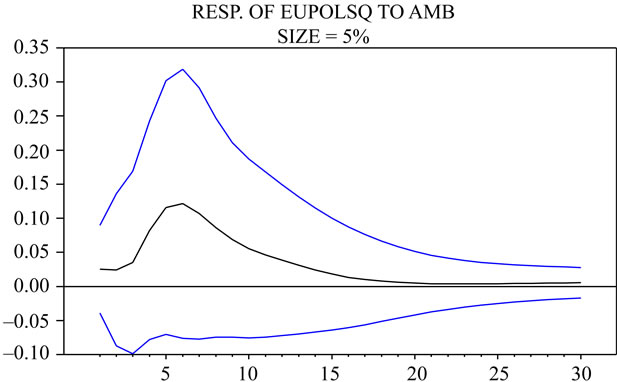

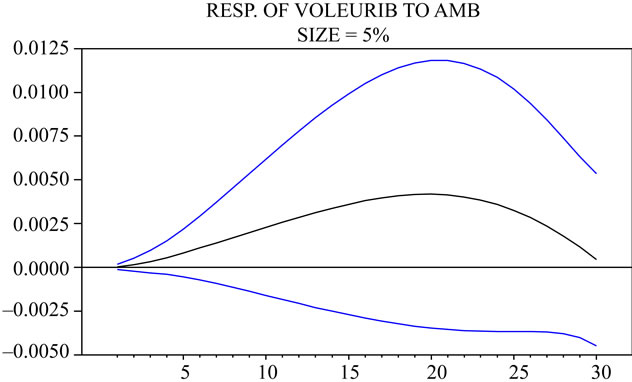

the level of each variable to a unit innovation in the identified structural amb and expdisp disturbances. The responses of the variables are displayed in Figures 1-5, along with their calculated asymptotic confidence bounds.

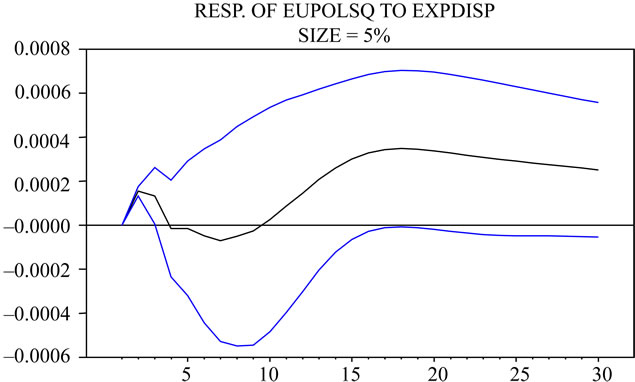

In the Figure 1 is showed the response of eupolsq to an unexpected unit innovation in the amb shock: the impact is positive and transitory, it reaches the maximum in the first five periods (about 12%), then it ends after twenty periods. In Figure 2, the response of expidsp is less marked (about 1.8%) and it reaches its steady state slowly, so that if communication is ambiguous, expectations about future interest rates are disperse. In Figure 3 the response of voleurib is positive and about 0.4%, the effect dies out after about thirty periods. In Figure 4 and 5 are shown the responses of voleurib and eupolsq to a shock in expdisp where they are positive: the first is about 0.4%, the second 0.04% but its effect is persistent, it takes over thirty periods to reach its steady state. All the responses are transitory, so that ambiguity has limited effects in few periods, the difference is that they reach their steady state in a different timing. So we can conclude that ambiguity of ECB communication and disperse expectations about future interest rates have transitory effects on the volatility of such rates, in particular, if agents’ expectations are more disperse, interest rates are more volatile, so that ECB communication could have had some effects on European money markets through its influence on agents’ expectations. In the previous section, a measure of ambiguity was provided. In terms of such measure, for the interval of time considered, ECB communication seemed to be quite ambiguous. However, given the results of IRFs, if ECB pursued stability, such ambiguity was not an optimal choice. The conclusion is that the initial ECB ambiguity was not a strategic choice, but rather the result of a lack of coordination among its members. Lately, ECB communication is much more careful and less ambiguous. IRFs show that not only ambiguity increases volatility, but also moves market rates away from the policy rate. Since it is plausible to think that ECB was willing to move market rates towards the policy rate, the graph of Figure 1 supports the idea that ECB ambiguity was the result of a lack of coordination among its members.

Figure 1. Impulse response of eupolsq to a one standard deviation shock to amb.

Figure 2. Impulse response of expdisp to a one standard deviation shock to amb.

Figure 3. Impulse response of voleurib to a one standard deviation shock to amb.

Figure 4. Impulse response of voleurib to a one standard deviation shock to expdisp.

Figure 5. Impulse response of eupolsq to a one standard deviation shock to expdisp.

4. Concluding Remarks

In this paper, we:

1) provided a new approach to ambiguity;

2) gave examples on how to use our definition for econometric purposes.

As regard 1) the focus was addressed on ECB communication. In particular, was surveyed a representative sample of European banks about the ambiguity of ECB communication from the 2nd of February 1999 to the 22nd of February 2000. Using data gathered from the surveyed sample, a set of measures to evaluate ambiguity were defined. In terms of such measures, was concluded that for the interval of time taken into consideration ECB communication was quite ambiguous.

As we already said, our aim was not to criticize ECB. However, at the time this research project started, ECB was the best possible case study because it was recently been established and its members just came from very different experiences; so, not only ambiguity could has been a strategic choice, but also it could has been the consequence of an initial lack of coordination among members.

As regard 2) was presented a Structural VAR model for the variables in the vector Yt, identified and estimated in the representation (4). IRF plots depicted that amb had positive transitory effects on Euribor volatility, the dispersion of agents’ expectations about future interest rates and the squared difference between the Euribor rate and the policy rate: ambiguity moved rates away from the policy rate, although it reaches quite quickly its long run equilibrium vanishing its effects.

So, the paper provides a new way to look at ambiguity. For the first time ambiguity is measured trough the answers of the agents who interact with ECB on a daily basis. Also, given the econometric results, we make the argument that ambiguity was not a strategic choice, but rather the result of a lack of coordination among members of the board of the Central Bank. However, the paper doesn’t focus on interpersonal dispersion, but rather on the ambiguity of the statements themselves, as perceived by the bankers. Therefore, it cannot be explicitly drawn a conclusion on lack of coordination between individuals. However, it has to be supposed that the ambiguity perception could derive from a non-homogeneous view of the monetary policy by part of the speakers, from which a not clear understanding of the speeches did arise. We can speak of lack of clearness of the monetary policy as a whole, in this restricted sense. The paper stresses out the importance of a non ambiguous communication in order to drive money markets towards the operational objectives of the Central Bank.

5. Acknowledgements

We thank Mr. Brizi, former President of Euribor A.I.C.; Mr.Drago; Mr. Cocuccioni and ATIC for their support. We also thank Marco Spallone for his useful suggestions and Luca Vitali for his effort. This paper is a chapter of a research project financed by the former MURST and supervised by Prof. Enzo Rossi.

REFERENCES

- A. Cuckierman and A. H. Meltzer, “A Theory of Ambiguity, Credibility, and Inflation under Discretion and Asymmetric Information,” Econometrica, Vol. 54, No. 5, 1986, pp.1099-1138. doi:10.2307/1912324

- A. Cuckierman, “Central Bank Strategy, Credibility and Independence: Theory and Evidence,” MIT Press, Princeton, 1992.

- L. Svensson, “Optimal Inflation Targets, Conservative Central Banks, and Linear Inflation Contracts,” NBER Working Paper, No. 5251, 1995, pp. 1-41.

- M. R. Garfinkel and S. Oh, “When and How Much to Talk. Credibility and Flexibility in Monetary Policy with Private Information,” Journal of Monetary Economics, Vol. 35, No. 2, 1995, pp. 341-357. doi:10.1016/0304-3932(95)01193-R

- A. P. Schioppa, “La Sicurezza Monetaria e le Banche Centrali,” Bollettino Economico della Banca d’Italia, Vol. No. 25, 1995.

- A. Blinder, M. Ehrmann, M. Fratzcher, J. de Haan and D.-J. Jansen, “Central Bank Communication and Monetary Policy: A Survey of Theory and Evidence,” Journal of Economic Literature, 2008, Vol. 46, No. 4, pp. 910-945. doi:10.1257/jel.46.4.910

- A. Blinder, “Central Banking in Theory and Practice,” MIT Press, Princeton, 1998.

- M. Rafferty and M. Tomljanovich, “Central Bank Transparency and Market Efficiency: An Econometric Analysis,” Journal of Economics and Finance, Vol. 26, No. 2, 2002, pp. 150-161. doi:10.1007/BF02755982

- J. Campbell and R. Shiller, “Yield Spreads and Interest Rates Movements: A Bird’s Eye View,” NBER Working Paper, No. 3153, 1989, pp. 1-42.

- R. Dornbusch, C. Favero and F. Giavazzi, “The Immediate Challenges for the European Central Bank,” NBER Working Paper, No. 6369, 1998, pp. 1-52.

- B. S. Bernanke, “Fedspeak,” The American Association Meetings, San Diego, 2004.

- J. de Haan, S. Eijffinger and K. Rybiński, “Central Bank Transparency and Central Bank Communication: Editorial Introduction,” European Journal of Political Economy, Vol. 23, No. 1, 2007, pp. 1-8. doi:10.1016/j.ejpoleco.2006.09.010

- E. Connolly and M. Kohler, “News and Interest Rate Expectations: A Study of Six Central Banks,” In: C. Kent and S. Guttmann, Eds., The Future of Inflation Targeting, Reserve Bank of Australia, Sydney, 2004, pp. 108-134.

- M. Ehrmann and M. Fratzscher, “Communication by Central Bank Committee Members: Different Strategies, Same Effectiveness?” Journal of Money, Credit, and Banking, Vol. 39, No. 2-3, 2007, pp. 509-541. doi:10.1111/j.0022-2879.2007.00034.x

- R. Reeves and M. Sawicki, “Do Financial Markets React to Bank of England Communication?” European Journal of Political Economy, Vol. 23, No. 1, 2007, pp. 207-227. doi:10.1016/j.ejpoleco.2006.09.018

- D. L. Kohn and B. Sack, “Central Bank Talk: Does It Matter and Why?” Bank of Canada, Ottawa, 2004, pp. 175-206.

- A. Fontani, E. Rossi and M. Spallone, “Ambiguity of ECB: What European Banks Think of It and How It Affects Money Markets,” OCSM Working Paper, Luiss University of Rome, No. 131, 2001, pp. 1-15.

- M. Fratzscher, “Communication and Exchange Rate Policy,” Journal of Macroeconomics, Vol. 30, No. 4, 2008, pp. 1651-1672. doi:10.1016/j.jmacro.2008.07.002

- B. Winkler, “Which Kind of Transparency? On the Need for Clarify in Monetary Policy Making,” ECB Working Paper, European Central Bank, No. 26, 2000, pp. 1-36.

- C. Amisano and C. Giannini, “Topics in Structural VAR Econometrics,” Springer-Verlag, Berlin, 1997.

NOTES

1Many authors focused on this topic. Cuckierman (1986, 1992) proved that “throwing dust in the eyes” might be a good strategy, if monetary authorities have to surprise traders in order to minimize their loss functions [1,2]. Svensson (1997) proposed the so called inflation targeting. He showed that transparency and pre-commitment may alleviate the inflation bias in case of lack of credibility [3]. Garfinkel and Oh (1995) showed that there exists a negative correlation between the degree of precision of the announcements and the inflation bias [4]. Finally, Padoa Schioppa (1995) said that ambiguity might be a good strategy in case of instability, since it helps keeping a high consideration of monetary authorities [5].

2Blinder, Ehrmann, Fratzcher, De Haan, Jansen, (2008), p. 926, among others [6].

3The identification scheme is presented in the Equations (5), and validated by a LR test.

4In particular, it was about the members of the Executive Board and the members of the Council, including two former members still considered authoritative.

5This idea was confirmed by the answers. In fact, the surveyed sample proved itself to be able to interpret messages about fiscal policy in terms of expectations on future interest rates.

6See Amisano and Giannini (1997), among others, for a general exposition of the identification and estimation methods for Structural VAR models [20].

7The weights derive from the member weighting in influencing markets reaction to statements and speeches.

8All estimations of the parameters and the impulse response functions have been carried out using RATS and MALCOLM, a RATS procedure developed by R. Mosconi.

9The LR test is χ2(3) = 0.104 with a p-value of [0.991]