American Journal of Industrial and Business Management

Vol.08 No.02(2018), Article ID:82411,56 pages

10.4236/ajibm.2018.82017

Online Money Flows: Exploring the Nature of the Relation of Technology’s New Creature to Money Supply

―A Suggested Conceptual Framework and Research Propositions

Victoria E. Erosa

International Graduate Center (IGC), City University of Applied Sciences (Hochshule), Bremen, Germany

Copyright © 2018 by author and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/

Received: November 24, 2017; Accepted: February 9, 2018; Published: February 12, 2018

ABSTRACT

Framing the analysis of Technology influences in an extended scenario of macroeconomic topics of the kind of Money Supply, attention is given to changes in economic paradigms that technology is constantly creating globally, focusing the research interest in the nature of the relation between cross border E-Commerce online money flows and Money Supply. As this context requires to find an explanation that cannot be provided by pre-existing theory, the abduction or abductive approach is considered to be suitable to investigate how far available data on the matter fits with the stated research subject identified at a crossroad of Technology Theory, Business Theories and Monetary Theory. The findings disclose that the nature of this relation is rooted in the Directionality, Dynamism, Intensity and Structural Properties, connected in a relational net that favors the configuration of a Theoretical body of knowledge. From the propositions’ relational models shape, a key finding come into sight as is supported the notion that cross border E-Com- merce online money transfer, is a process by which cash money in circulation (Money Aggregate M1) is transformed into highly liquid assets other than cash, referred to as Quasi-Money, leading to dynamic changes for Money Supply net value and in the velocity of money. This view is consistent with the appreciation that being online money flows one new additional component of M2, they are absorbed by Money Supply being for that reason a priority issue for monetary policy interest. The emergent relational net, outlines a theory in which recognizing online money flows as a technology derived component―a technology creature―Technology influences reach the Economy at macro level by means of its effects over Money Supply M2 Aggregate. The research process is completed with a Case developed to explore how the suggested conceptual framework works, as well as to exemplify how the set of propositions formulated are actionable by observable indicators.

Keywords:

Technology and Money Flows, E-Commerce Online Money Flows, Abduction Method, Online Money Flows and Money Supply (M2), Complex Systems Interaction

1. Introduction

Information Technology (IT) development is recognized as a major technological breakthrough that has had a transformative impact over business practices, business processes efficiency, human and society communication modes as well as major changes in economic structures. IT impact has been widely analyzed from diverse perspectives such as competitiveness and operational efficiency as supported by early works of Brynjolfsson & Hitt [1] as well as by reports of a prestigious consultant such as McKinsey [2] , top management sphere of decisions regarding technology, the effects over persons’ attitudes and behavior as drivers of change as is generally accepted since Davis’ development of the Technology Adoption Model [3] , as well as regarding awareness of the need to incorporate technological issues within strategic decision making issues of the kind of new business models’ development and operation. Global IT infrastructure platform enables firms to operate interactions among business partners resulting in collaborative and synchronized processes transactions such as the ones involving money flows between and among business partners and customers, as well as those operations related to tax administration compliance, being adopted in a growing number of countries as is reported in a recent OECD publication [4] .

Business interactions and transactions conducted through Internet as an open network and other comparable systems are referred to by organizations [5] , as well as by consultant firms [6] , and International Organizations [7] , as Digital Economy, Information Economy [8] , Virtual Economy, the Web Economy or The New Economy. As Information Technology impact strikes most of economic activities, changes emerge surprisingly creating new business technology- based paradigms as well as economic components, among which online/elec- tronic money flows emerge as a new technology creature of key importance due to its cross border field of action in Global Electronic Commerce transactions, velocity of money movement among countries, and multi-currency operation possibilities, all of them framed by macroeconomic components referring to the measurement of the total amount of monetary assets available in a particular economy at a particular point of time, known as Money Supply or Money Stock structure [9] . The concern about the relation of a monetary component of the Digital Economy termed electronic money/EMoney was introduced by Helleiner in a seminal article by since late 90s [10] , providing basis to evolve into the emergent issue of monetary policy under the Information Economy context introduced by Woodford [11] . Following this ideas, the implications of Technology on Monetary Policy were introduced into the macroeconomic field discussion [12] , reaching recently into the analysis of the impact on Monetary Policy of the use of Electronic Money [13] , as a key advance of a theoretical field still in progress.

As Digital Economy does not distinguish itself by a rich heritage of theory development analysis on the matter usually search for explanation in theories borrowed from different scientific fields, as identified for issues of the kind of the relation between Money Supply and the amounts of electronic money―EMoney- moving in a stream/circulating by means of a technological infrastructure support, identified as an open network-online―such as Internet, referred to as online money flows. The explicit distinction of this concept is set by its dynamic- flow [14] ―and its aggregate―amount/sum total or more quantities or sums/the full effect [15] ―characteristics, underlying the difference as a unit of analysis from the specific character of surrogate for coins and banknotes of EMoney concept defined by the EC Directive as… monetary value as represented by a claim on the issuer which is stored on an electronic device, issued on recipient of funds of an amount no less in value than the monetary value issued, and accepted as means of payment by undertakings other than the issuer, an electronic store of monetary value on a technical devise that may be widely used for making payments… [16] [17] .

Two main areas of knowledge in which online money flows concept interacts are identified in the IT arena, due to the technology infrastructure component that enables their movement from buyer to seller, as well as in the business field considering its operational nature in transactions completion and its revenue generator purpose. Both views are rooted at micro economic level. The macroeconomic level perspective emerges when is faced a wide array of Digital Economy definitions existing in-between dictionary sources and text books such as:

…a Digital Economy is an economy which functions primarily by means of digital technology, especially transactions made using internet [18] ,

…an economy that is based on digital technologies [19] ,

to results from academy’ recent works focused on the matter containing the following declaration:

….we therefore define the digital economy as “that part of the economic output derived solely or primary from digital technologies with a business model based on digital goods and services” [20] .

A deep view into the first and the second definitions suggest the existence in parallel of two economies differentiated by the setting-place/space―in which their activities are performed and the technology means by which the economic activities are operated, while the second definition consider it as a part of the economic output. Differences among definitions jump at sight.

Comparison of these definitions, presented as a brief insight on the matter, express indirectly that Digital Economy as a theoretical construct seems to be in the initial development phase, being clear that to be operationalized or measured, diverse concrete representations or variables and their observable indicators and measures should be determined. Any connection to emergent specific economic components created, such as the online money flows, is observed in the definitions analyzed raising from this reasoning the interest to focus the attention in online money flows created by ECommerce transactions, as considered to be one concrete representation or variable with its specific measures and indicators.

To move forward in theory formulation, a necessary step is to benefit clarity over the diversity of views stated in the many and different construct’ definition found in the literature review, by means of the identification of the role of online money flows either as a component of a new Economy structure or as a new component of the existing Economic structure. In this context, knowledge regarding the nature of online money flows and Money Supply relation emerges as a key issue to conduct theoretical research activities oriented to gain understanding regarding the characteristics of the relation between the Digital Economy monetary component derived from ECommerce transactions―online money flows―and the Economic Structure monetary component―Money Stock/ Sup- ply―as the effects of ECommerce online money flows may be considered as possible triggers of changes in Money Stock/Supply structural composition, its size and/or in the velocity of money. This relation has been discussed under the approach of the impact of electronic money on monetary policy providing a wide range of views gauged from those declaring that there are no implications [21] , to the ones declaring that the influence of EMoney on Monetary Policy― using indistinctly the term digital money [22] ―can be seen through Money Supply Money Aggregates [23] [24] . For the research interest this view results of particular interest as relies in established regulations on the matter such as the one of the European Central Bank (ECB) concerning the balance sheet of the monetary financial institutions sector, registering EMoney on the liability side as part of the money aggregates, included in transferable deposits, in the category of overnight deposits or balances of immediate conversion into currency or to be used for cashless payments [25] and [26] .

The possible influence of EMoney on the monetary policy has already been reviewed, identifying a reference in the results of a survey, with data from the 2002-2003 years period, applied to 95 central banks and financial institutions by the Bank for International Settlements declaring that even when major implications of EMoney for monetary policy were not expected―at the survey time-the participating central banks report that they were considering to monitor such development, or to include EMoney data in monetary statistics, being some of them implementing activities on the matter such as data collection [27] . Interestingly, none of the referred surveyed institutions indicated adverse effects on them balance sheets of EMoney over Money Supply Aggregates such as money in circulation (M1), neither a specific policy response envisioned. This scenario seems to be fairly similar after more than a decade.

The wave of effects of the relation between online money flows and Money Supply extends to the imminent emergence of requirements for diverse register venues of the Import/Export transactions undertaken between one country and others, traditionally incorporated as a credit-debit in the Current Account register of the Foreign Trade Balance, as ECommerce business models foster operations in which online money flows move back and forth countries where online transactions are completed following a path diverging from the one configured by the countries where the correspondent traded goods are shipped and/or delivered. Such operations representing non parallel intangible movement of money flows and tangible movement of goods, seems to require traceability records for each own as necessary input to be registered in National Accounts System and in specific Census Indicators, for reliable hard data creation to build solid ECommerce activity measurement in terms of GNP contribution, its impact over international currency reserve, as well as for the definition of taxation (VAT) control criteria over online flows operations, among other macroeconomic issues at country level.

2. The Research Framework

2.1. Online Money Flows: A Construct of Interest

Works on the theoretical dimension starts with the identification of the constructs of interest as a basis to describe the relations among them and then determine the observable indicators required for the constructs measurement. The path to online money flows is traced since the E-Commerce and Digital Economy constructs measures and indicators. From literature review emerges evidence of the concern regarding Internet Economy measurement in a work published more than a decade ago by the Center for Research in Electronic Commerce of the University of Texas [28] , that presents a Conceptual Framework developed to understand how the Internet economy works considering four layers, identified as 1) Internet Infrastructure (networking/connectivity); 2) Internet Applications (software, standardized messages, languages); 3) Intermediaries such as companies that link buyers and sellers (market spaces, content, etc.) and 4) a layer named Internet Commerce which stands for companies involved in direct commerce transactions to business and/or consumers. This proposed framework by determining Internet Commerce activities as one of the Internet Economy layers introduce the idea of different theoretical constructs, identifying Internet/ Electronic Commerce as one observable indicator of the Internet/Digital Economy construct able to be expressed in terms of monetary units.

Being the first construct’ differences acknowledged, literature review takes the search into the data sphere. At present, important efforts―applying different methods―have been realized regarding macroeconomic approaches to measure the impact of Internet on Growth as the one identified in works released by The UNCTAD [29] and in the previous mentioned MacKinsey report [2] , with estimations sizing Internet Economy―for GDP quantification purposes,―the first source covered 137 countries while the second source include results of a survey applied in 13 countries (representing 70% of world’ GDP), being considered the first as the sum of Internet consumption in terms of ECommerce, Services and Access, public expenditure and private investment on the matter, and interrelated Trade Balance of goods and services. In regard of ECommerce measurement, key works developed by The ECommerce Foundation that also serves as ECommerce Europe’s research institute provide reliable data from European and more than 15 other countries based on Global Online Measurement Standard for B2C ECommerce (GOMSEC), organized by Global, Regions and Country’ amount of revenue classified on areas/sectors, as an indicator of ECommerce activities defined broadly by them as …Any B2C contract regarding the sale of goods and/or services, fully or partly concluded by a technique for distance communication… [30] . Measures at national country level are found in sources such as the US Census Bureau, which provides national estimates of ECommerce activity in key sectors of the economy [31] . A mention is made to the methodology developed for such a purpose, as well as the one applied in the Annual Retail Trade Survey (ARTS) series [32] . The revision made reveals the existence of a crucial differentiation of two entities, the first refers to Internet/Digital Economy measurement, while the second refers to the measurement of ECommerce transactions identified as one component/layer of the Internet/Digital Economy, being feasible to manipulate data of the construct in terms of data aggregation as illustrated in data referring to ECommerce sales at national country level. From this order of ideas rise the notion in which ECommerce is a construct able to be measured by its amount/value in terms of diverse observable indicators such as amount value, sales value, cross border operations, packages, volume, etc.

Selecting ECommerce value as one of the variables considered to measure the Digital Economy construct, the value amount in monetary units of each ECommerce transaction (purchase/sale) completed in an open network by means of an electronic transfer (payment), creates online money flows representing an intangible monetary component in circulation in the figure of highly liquid assets in foreign and national currencies, that ends being absorbed by the engaged country’s Money Stock, making then reasonable to consider that it receives an effect over its total amount, the velocity of money, or both. Upon this basis Online Money Flows became a construct with observable indicators in terms of value, under varying conditions determined by the cross-border characteristic, the question of interest emerging here refers to …what is the nature of the relation involving the monetary components of both the Digital Economy―cross border ECommerce Online Money Flows―and the existing-Money Stock/ Supply-Economic Structure? The notion of online money flows in this research question refers to amounts of paperless monetary transactions―monetary value as defined by the European Central Bank―, being transferred by electronic means―instantaneous delivery―, and not to a new mode of issue of currency. Safety and security of these operations rest in several measures such as data encryption―coded data that once received are decoded by the recipient’s service or bank―and data transmission processed by an independent agency (Automated Clearing House). Examples of e-money transactions are online payments completed using Internet by means of debit card, smart card, credit card as well as electronic fund transfer from bank to bank enabled by technology infrastructure such as computers, tablets, mobile phones apps or ATMs. It must be noticed that in this context the term Electronic Transfer, is used as a general reference for the transfer of money funds using Internet as an operational enabler, regardless its online payment mode, payment scheme selected, or electronic device used for such a purpose.

As the search horizon on the matter of interest moves defining its boundaries to the mentioned research focus, an important finding supporting the research interest on the matter is that even when ECommerce turnover―money transferred via electronic means―shows an incremental growth estimated by Ecommerce Foundation 2015 in 17.5% in 2016 [33] , there is no evidence of online money flows control by a specific macroeconomic policy until the publication by the European Commission in December 1, 2016, of a legislative proposal to regulate taxes from cross-border Ecommerce termed “VAT Package” in the context of the strategy to create a single Digital Market for the European Union (EU). The VAT Package proposal aims to provide business conditions in which “instead of having to declare and pay VAT directly to each individual Member State where the customers are based, businesses are able to make a single declaration and payment in their own Member State” [34] . Currently Ecommerce activities in the EU reap benefits from VAT exemption regulation on import goods from non-EU suppliers with a declared value below 10/22 Euros, operating since 1983. The European Commission argues as a powerful reason for the VAT modernization for Ecommerce activities in the EU, the annual loss estimated in at least 5 billion Euros in VAT revenues for Member States [35] . Advances related to a common payment scheme, are identified in The Single Euro Payments Area (SEPA), developed by the European Payments Council as a set of rules and technical standards that can be regarded as instruction manuals to move founds from one account to another within the SEPA schemes that operates with open access criteria (Article 28 of the Payment Services Directive/Directive 2007/64/ EC of the European Parliament and of the Council of the EU of November 2007 on payment services in the internal market). The transference between banks of SEPA payment messages is operated by means of ISO 20022 XML message standards (UNIFI). Regarding this topic, ongoing works on the matter have reach the point of decisions among EU member states for strong security measures oriented to financial institutions’ protection from fraudulent transactions risk. The context briefly described strongly supports the topic of interest declared for this research.

2.2. Money Stock/Supply a Construct of Interest

The relation between online money flows and Money Supply attracts attention when considering that as result of the Global span of operations, cross-border ECommerce transactions give rise to online money flows moving from one country to another with an expected impact at macro level on Money Stock (velocity and size of Money Stock available), domestic currency reserve (expenses/ payments in foreign currencies), internal demand (international purchases) and/or Trade Balance (imports-exports). A key tool of macroeconomic policy, the concept of Money Stock/Supply―the total amount of money/monetary assets available in an economy at a particular point in time,―is configured by a set of measures or Money Aggregates (M0, M1, M2, etc...), frequently classified under each countries criterion, reflecting diverse levels of liquidity. In its general acceptation, M1 is the term designating liquid forms of money, currency in hands of the public, demand deposits, travel checks and other deposits against which checks can be written [36] . Money Aggregate indicated to as M2, is configured by M1 as well as by a component known as Quasi-Money or Near Money representing highly liquid assets other than cash, not suitable as exchange mediums, that can be quickly changed into cash or checking deposits [37] . Being Money Supply the key construct setting the foundations of the research focus, to benefit clarity and construct validity its configuration is described in Figure 1, introducing as well the M2 definition break down.

Figure 1. The configuration of Money Stock/Supply and M2 concept breakdown.

The concept of M2 defined by The World Bank provides general criteria to move forward in the referred research interest …M2 includes M1 plus time and savings deposits with banks that require prior notice for withdrawal… [38] . M2 main measurement components are currency in circulation (M1), deposits redeemable at a 3 month up period notice, overnight deposits and deposits with agreed maturity of up to two years [39] .

2.3. Framing Concepts’ Interactions

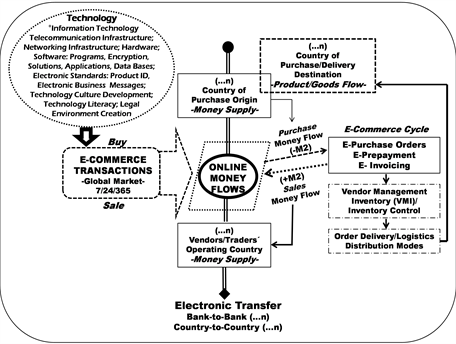

The link formed by technology as new business models enabler of ECommerce kind, with emergent components such as the online money flows, drafts a basic complex contextual background presented in Diagram 1, describing the conceptual systems interactions, suggesting as well the related data required to address the importance of a deep understanding of the nature of the relation between the digital and the structural monetary components, and to take attention that, so far, there is no evidence that ECommerce online money flows are captured by country’ Money Supply referred as well as Money Stock as an autonomous component particularly linked through many interconnections with its money aggregate (M2), specifically with its Quasi-Money/Near Money component. The intriguing question is if ECommerce money flows―identified as electronic/online money flows―affect involved countries’ Money Stock by adding and/or subtracting monetary resources resulting from the operation of the emerging commercial model, or if local/domestic ECommerce money flows have an impact in the velocity of money, or if both of them are affected. The connection of the Technology-Business-Macro Economic systems has never been made

Diagram 1. Contextual background of the interactions of Technology, Business and Money Flows generated by ECommerce transactions.

possibly because figures with direct hard data―fact data―on ECommerce money flows fully disaggregated by country of origin to country of destination, are not available as result of the absence of Global harmonized measures and indicators on the matter in National Accounts Systems, ―such as an ECommerce Trade Balance or an ECommerce Satellite Account by Country could be―as a means to monitor and control the effects over the economy and its main policies of such complex interactions. Following this order of ideas emerges a challenging analytical perspective connecting Competitive Theory, Technology Use Theory and Monetary Theory, which could contribute to draw focus of attention to changes in economic paradigms that technology is constantly raising globally.

3. The Systems’ Interaction

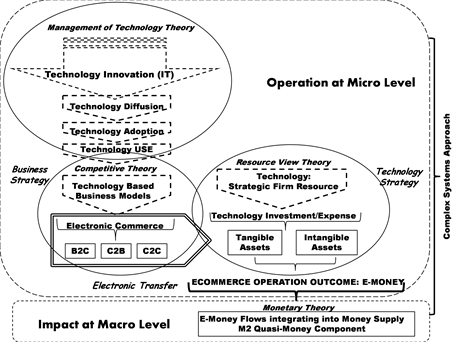

The research interest presented in the contextual framework draft suggests the interaction of three heterogeneous and autonomous but interrelated dynamic systems,―technology, business and money flows―revealing some type of order, as result of such interactions, identified with the Complex Systems perspective. This view is considered to be adequate to benefit the initial conceptual framework by organizing its complexity as a general frame to work along the process followed to determine Propositions that could make a contribution addressing this challenging issue. Complex Systems definition [40] , as well as its view over its application to Social Sciences [41] , declare that they exhibit properties that emerge from the interaction of their parts and which cannot be predicted from the properties of the parts, as identified with the interaction of Business System and Technology System that is expected to be extended to the Monetary System as a final effect. This view is consistent with the complexity approach of economics in which it states that what happens in the economy is determined by many dispersed, possible heterogeneous agents acting in parallel, with no global control interactions, which are instead provided by mechanisms of competition and coordination among agents [42] . The revision of the contextual framework of Diagram 1, lead to identify that as a result of the interactions of the three systems involved in the research interest, a type of order is exhibited providing basis to consider the presence of a complex system supporting the reserch focus of interest, as presented in Diagram 2.

The introduction of complex view perspective is considered to be necessary to identify properties that emerge from the systems interaction, which cannot be drawn from the properties of the parts as a unit. The first of these interactions corresponds to Technology System/Business System that leads to the ECommerce business model’s emergence. Understanding a business model as the general term describing how a firm creates, deliver and captures value to/from market opportunities, the Business System in this research is identified with Electronic Commerce (ECommerce) as a general frame of reference for electronic business models operating transactions in which the sales of goods and services are completed, where the buyer places an order, or the price and terms

Diagram 2. Business, technology and monetary systems interactions in E-Commerce Business Processes Operations.

of the sale are negotiated over Internet networking, extranet, proprietary networks such as Electronic Data Interchange (EDI) network, electronic mail, or other comparable online system. Embedded in ECommerce transactions are key operational business functions such as digital marketing, inventory management, dispatch and delivery programming, sales register by item, volume and money indicator taking advantage of existing ID product and communication standards (GS1), accountancy registers and electronic invoicing, all of them configured as a commercial cycle that starts with electronic order management, payment moving forward until close with the electronic invoice issue, at the heart of this operations online money flows do their bit.

In this complex research context, a word of attention is required regarding the phenomena in which the interest is focused. Due to the nature of the money flows involved―identified as highly liquid assets moving by electronic means in/and to countries’ Money Stock (Money Supply), the key component to conduct the analysis are online money flows created by the transactions executed in a Business System referred to as ECommerce, understood as defined in the US Census Bureau [43] operated in three main types of business models on the Web [44] Business-to-Consumer transactions (B2C) as in webpage-store business model; 2) Consumer-to-Business transactions (C2B) as a service platform-busi- ness model where the customer post a requirement and business bid on that requirement; and 3) Consumer-to-Consumer transactions (C2C) where the service-platform business model support transactions through sites offering auctions, free classified, and forums where persons can buy and sell using online payment systems. This definition is considered to benefit the research analysis bringing accuracy to the term “sale of goods and/or services” component of the broad definition introduced into the business model perspective. Money flows derived from personal transfers, investment processes and banking transactions are a different matter of analysis, out of this research study’ boundaries.

Ecommerce business models’ operation starts with the mentioned technological system configuration based on Information Technology infrastructure required as the support platform for enabling connectivity, communications, products/sender/receiver identification and traceability, and money transfer transactions between and among business partners operating in an electronic based processes context. Driven by innovation development, Technology System has produced major breakthroughs in fields such as communications infrastructure that extended Internet use as the open channel for business interactions, solving technology investment problems that existed during the EDI private network era that provided access to electronic business interactions to limited number of big businesses’ partners. The advent of XML standardized electronic messages, opened the doors for information flows management of the business cycle by online means paving the road for ECommerce diffusion as a new business model―linking the technology system to the business system-, that soon was perceived as a solution to create and rise profit growth. Innovation on the matter has extended to Product ID standards in the form of Electronic Product Code (EPC) that enables cost efficient operations such as product traceability along the order cycle management, logistics, delivery and fulfillment operations required to honor the promise of ECommerce sales, as well as electronic transfer solutions that created new payment schemes operated under integrity and security conditions within and across countries. From this operational interdependence, the link between these two systems emerge due to the diffusion of ECommerce business models that fuels the adoption of technology- based processes and business practices of the kind of Supply Chain Management (SCM) accelerating the use of technology as business enabler and support. Such changes contributed to a technology culture creation in which trust, confidence and efficiency are characteristics.

Under the clear understanding of the first interaction between Technology Systems and Business Systems, a second interaction with the Monetary System takes place forming a network shape of links as presented in Diagram 3. The operation of ECommerce business models under a cross border environment, leads to the creation of money flows resulting from online payment of the transactions realized, and from derivate activities such as Logistics and Fulfillment operations, generating either a positive or an adverse effect over the correspondent country’s Money Supply mainly through electronic payment schemes (Electronic Transfer) and/or still directly by the banking system.

ECommerce transactions shapes a loop involving sellers placing and taking orders over the Internet, transaction partners such as physical movement enablers, banks and institutions that offer transaction clearing services, as well as

Diagram 3. Complex Systems Perspective. Theoretical Interaction supporting research oriented to explore the nature of the relation of online money flows with Money Supply.

authentication authorities playing as a third party to validate integrity and security of those transactions,―and customers with a mindset to search-select-pur- chase goods available online by means of electronic devises and pay for them using Electronic Transfer schemes. Known as commercial cycle, the loop is framed by Governments’ legal dispositions and infrastructure built for this purpose such as electronic signatures assignment-management-control, electronic invoices, and laws and regulations as means to protect consumers and businesses involved in such transactions [45] . This commercial cycle operation is supported and enabled by the Technology Infrastructure constantly updating due to innovations. The emergence of business models enabled, supported, derived, and/or designed in/by/from Information Technology infrastructure leaded to the foundation of a new business paradigm that operates in parallel, as substitute, instead, as complement, or independent to traditional business models.

The Complex Systems view of the research interest results to be suitable to provide sense to dispersed concepts working under the same roof by introducing an order to leads to identify theories behind the systems interaction, as a first step to build a theoretical referent to be used as a base to perform Theory Matching or Theory-Data Dialogue. Diagram 3 shows the interaction among sets of concepts from Management of Technology Theory and Competitive Theory working upon business strategy by means of new business models conception―such as ECommerce―introducing Resource View Theory as the executable support in which technology became a tangible and/or intangible asset at firm level, of strategic nature. So far theoretical interactions happen at microeconomic level, becoming a macroeconomic issue when emergent online money flows reach country’ Money Supply, being established then, a relation between the constructs from the two dimensions in which this research is interested.

4. Methodology

The stated focus of this study is on the nature of the relation between cross- border online money flows and Money Supply. Considered as a technology creature [46] , created by IT infrastructure development and its use as business enabler in the emergent paradigm of Electronic Commerce’ Business Models, with the ability to move independently on Global basis upon borderless conditions and timeless limitations, electronic or online money flows became an essential element of the Digital Economy identified as its monetary mass component matching the requirements to be used as one observable indicator for its measure. As such online money flows nature, as well as the nature of its relation with macro policy components of Money Supply sort and their correspondent measurement indicators, call the attention for a research exploration. The term nature stands for the fundamental qualities, the essential properties and/or causes of an individual phenomenon which in this case of interest is the relation stated. As the actionable verb, in this research exploring correspond to identify, collect and evaluate key issues of theory and available data to formulate a set of propositions that further on could contribute into theory building.

Consistent with the four main blocks of social research perspective [47] denoted as: The Analytic Frame, the Theories, data as evidence and the resulting new ideas generated by the analysis, this research process began by sketching a representation of the initial research idea framing its main components. When used to differentiate and/or classify key elements of the phenomena under analysis, such frame is identified as one of the aspect based type. Upon this basis, is reasonable to consider being the contextual framework developed as Diagram 1 modelled through the Complex Systems interaction view as shown in Diagram 3, represents the Conceptual Framework to be operationalized in one Research Question addressed to cover the issue involving both micro and macro level dimensions. This framework is expanded and adjusted as the analysis moves forward into the theory matching stage.

RQ. What is the nature of the relation between online money flows and Money Supply?

The stated Research Question reveals the complexity of the context of analysis involving constructs and observable indicators from two dimensions, the first identified as a major component of the digital business dimension at firm level, while the second is grounded in the macroeconomic monetary policy arena of the Economy Structure dimension. To understand the relational statement presented, is taken into consideration that the analysis should be carried on in a context in which a) established theory cannot fully explain the new phenomena [48] , b) the e-monetary mass component―online money flows―is not computed because is on the conceptual level, and c) hard-fact data on the direction of e-money flows among correspondent countries involved in transactions of the kind are not fully available at the required disaggregate/granulated level. Under these constraints, the Grounded Theory Approach (GTA)―discovery of theory from data―is considered appropriate for analysis as focused on Theory generated by describing what happens and finding explanations to why it happens on the basis of observation leading to formulate Propositions that express a deterministic relation [49] [50] . The described approach gains understanding when considering the research characterized by being set in the Social perspective dimension [51] -identified by its Qualitative Research type nature [52] ―using as a research strategy the Grounded Theory Approach (GTA) [53] ―applying its procedures and techniques [54] . A key component of GTA method is abductive reasoning [55] [56] .

Being the Research Question of this analysis focused in finding an explanation that cannot be explained by pre-existing theory, the abduction or abductive approach―understood as the process which starts with an observation to form explanatory hypothesis [57] ―is used to investigate how far available data on the matter fits with the stated research subject identified at a crossroad of Technology Theory, Business Theories and Monetary Theory. Abduction is the pragmatic approach that implies the constant movement between existing theories and data,―the Theory Matching/Systematic Combining process approach [58] ― making comparisons to identify deviations and patterns for further interpretation in the quest of possible explanations which could suggest new theory expressed by general rules, Propositions (P) or Hypotheses (H) [59] [60] . Here the knowledge rests upon observed facts, empirical events or phenomena related to a rule. The full process structured in a logic sequence that goes from rule to result to case [61] , is considered a suitable methodological approach to identify how the stated propositions works in an empirical setting or case that supports a plausible conclusion considered to be as the best explanation.

To support the Theory Matching operations embedded in the selected method, as a second step of the research process, a Theoretical Framework was built to frame and contrast data with existing theories focusing in Online Money Flows derived from cross border Electronic Commerce activities. Data is collected by means of archival analysis technique from registers and statistical data on the matter published in the WWW―Internet access/direct request―by Government, Institutional and Ecommerce specialized Sources at World, International and Country level. Results are analyzed to identify characteristics of the nature of the relation between Online Money Flows and Monetary Supply components at country level framing the research in data of countries that account for around 70% of the Global ECommerce transactions. Insights on Money Supply data are based on statistics available online from The World Bank.

5. Theoretical Referent

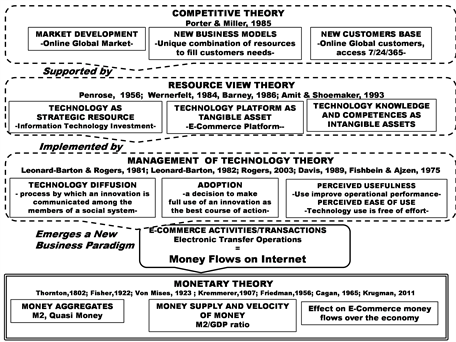

The backbone for this research approach is configured by an array of theoretical bodies from the Business arena, Management of Technology discipline, and Monetary Theory. This view fits with Electronic Commerce activities because each one of the systems involved in the research context has a supporting Theoretical Referent interacting with the others which is not completely suitable by itself to again understanding in regard of the determined phenomenon under study. The components of the complex theoretical frame in which the analysis is supported are organized as a necessary step to identify the role of each theoretical body in the structure of the research focus, being further used as the basic input of Theory Matching technique applied here to develop a set of Propositions.

Fine grains of the theories are identified to piece together in the theoretical jigsaw presented in Diagram 4, being the business arena the detonator of the phenomena. Competitive Theory [62] provides basis to understand new business models quest as profit generator means, supporting business strategies among whom emerge Market Development envisioned as a means to create feasible Global Markets, bringing a new customer base and/or extending the existing. To face the competitive environment, firms turns into the search of efficiencies in their resources among which the relevant contribution of Information Technology is the coordination of the firm’s value chain either as a commercial enabler (E-Commerce) or/and as support of the inter-firms’ operation of the business processes through electronic means, named E-Business [19] . The business view is related to the firms/competitors’ internal organization perspective, coming from Resource View Theory tradition, the firm performance is determined by its resources [63] [64] . Technology is considered as a key strategic resource oriented

Diagram 4. Theoretical Framework developed to explore the nature of online money flows and Money Supply relation.

to support business strategies implementation as a means to gain efficiencies, reduce operational costs and built a unique a non-imitable defensive barrier against competitors [65] .

In this business atmosphere, grows the recognition of the importance of Technology Innovation, recognized by Economic Theory―since decades ago― as source of economic development changes due to its role as production factor [66] . This view is extended when is accepted as strategic competitive resource, with its own management process of planning, investment and operational budget requisites, etc. As such, Technology Innovation is involved in diffusion processes among the members of a social system―either horizontally [67] , or as a driver of change [68] ,―who eventually take the decision to make full use of it as business strategy enabler, support and/or production means [69] . Theoretical body from Management of Technology discipline suggests the feasibility of new markets development (Online Global Market), that leads to the creation of new business models (ECommerce typology) oriented to cover a new customer base (online customers) under new competition basis of 7/24/365 atomized countries attention (cross-country transactions), working under conditions of paperless monetary transactions (Electronic Transfers generating online money flows). To face the challenge, technology is considered a strategic resource to be invested either as a tangible asset (ECommerce platform/outsource) and as an intangible asset to be developed by means of knowledge and professional competences mastering [70] .

E-Commerce activity depends upon decision making by consumers―the use of technology based sales channel, product selection, trust, etc.-, and from firms selling direct or through a third-party marketing mixes of products targeted to specific online market segments. Introduced by Davis [3] , within the technology adoption requirements, the concept of Technology Use is declared to be an initial condition to improve firm’s operational performance. Upon the basis of The Theory of Reasoned Action [71] the concepts of Perceived Usefulness (PU) and Perceived Ease of Use (PEU) are key determinants that lead to use a specific technology. Davis [3] defined Perceived Usefulness as the extent to which a person believes that using a specific technology will improve the operational performance, while Perceived Ease of Use is defined as the extent to which a person believe that the use of a specific technology is free of effort. PEU is related to intrinsic characteristics of Information Technology (easy to use and easy to learn how to use), while PU relates to extrinsic factors such as technology efficiency and efficacy, precious for the businesses to gain benefits from operating cost reduction.

Interactions of Business and Management of Technology theoretical referents provide sustain to the idea in which the diffusion of ECommerce business models follows an adoption cycle for users―from being part of the innovators or first to adopt segment, to the early adopters, the early majority, the late majority and the final adopters segment termed the laggards-, extending user’s acceptance span due to their usefulness in gaining operational efficiencies and access to new markets. Thus, matching theory with available estimated data of Ecommerce value amount, is reasonable to consider that ECommerce is becoming a competitive requirement in its way to be a common business practice, and that its trend of online money outcomes will continue to grow enlarging its transference to countries’ Money Supply. The ECommerce-Monetary System connection emerges in user’s adoption-acceptance-use of the technology figure of Electronic Transfer operations that refers to payment schemes over Internet that enables the operation of online money flows within and across countries. The percentage of a country’ ECommerce purchased at foreign sites is known as Cross Border ECommerce [30] being this a business context of main interest for this research purpose the reference in this paper is extended to include sales and purchases recognized as the two ongoing transactions of trade supported by payment operations. Assuming that online money flows are captured by countries’ total Money Stock, a relation is expected through the Money Aggregates that constitute the structure of Money Supply/Stock, referred to as M2. As previously stated in this research, within the M2 concept, money flows on the Internet are identified with highly liquid assets other than cash that can be quickly exchanged by cash known as Quasi-Money, Money plus Quasi-Money, Money Aggregate M2 or Broad/Near Money. The nature of the relation between the two monetary elements is the core interest of this research.

6. Formulating Propositions

The theoretical framework developed favors the view in which Technology Innovation in the figure of Information Technology developments, leverage business competitiveness by providing strategic resources that enable operational performance and creates new business models among which Electronic Commerce takes place. Diffusion of Ecommerce activities leads to the adoption of online business models as a new business venue either operating simultaneously with the traditional mode, or as new electronic business structures operating exclusively online. Being the new business model adopted with unprecedented dynamics, Technology Innovation shortens its development cycle to create a growing number of Technology solutions to fuel operation requirements to cover electronic transactions among all stakeholders and business partners engaged in Ecommerce operations worldwide. It is said that the moment of truth in business is payment, therefore electronic payment emerges by electronic transfer means creating a new creature: Electronic or Online Money Flows moving instantaneously among business partners operating in National, International and Global arenas. The observed theoretical interactions among Management of Technology/Resource View Theory and Competitive Theory notions, lead to declare a first Proposition regarding the effect of online money flows over Money Supply according to their direction in terms of country of origin and country of destination. Attention must be taken to the condition implicit in the Research Question regarding the analysis of the nature of the relation of online money flows, resulting from cross-border ECommerce operations, with country’ Money Supply.

Proposition 1. Under a cross-border ECommerce environment, Online Money Flows effect over Money.

Supply varies accordingly to the type of ECommerce transaction involved.

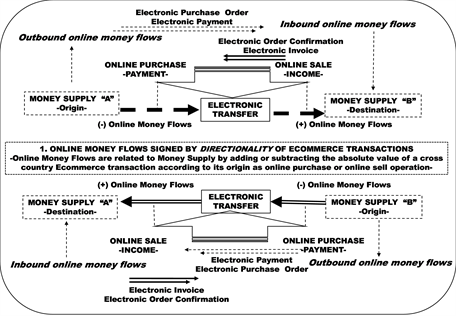

As a business operation, ECommerce broadly comprises online buying and selling transactions completed by payment usually made by electronic transfer modes. As this transactions could take place either in a same country and/or in different countries, it is reasonable to ponder that Money Supply receive different effects from online money flows generated in/within the same country than those online money flows generated by cross border ECommerce transactions operating as in a kind of misplaced pattern of trade in which the source and destination country of online money flows is not necessarily the same country in which the transaction is made, or the country from where the goods are shipped from or delivered to. Constituted by the amount of payments, outbound money flows are formed in countries where the purchase transaction is filed and steered to a country of destination where the payment is defined by the seller, being then recognized as inbound online money flows for that country of destination. The unique characteristic of ECommerce business model is that the money flows direction usually diverges from the direction of the physical flows of purchased goods to be delivered, introducing then, the key issue of the divergent patterns followed by the online money flows and their correspondent physical goods. For this reason, regardless the goods flows―registered traditionally by means of a Trade Balance account-, under cross-border conditions online money flows effect over Money Supply seems to be associated with their directionality, meaning that online money flows have a positive effect (adding) on Money Supply of countries of destination in which the payment by electronic transfer is received, a reverse or negative effect (reduction) on countries in which the purchase payment is completed or registered, and a neutral effect if transactions takes place within the same country or international economic block.

This proposition is identified as focused over the what happens with the effect of online money flows when considering their source of origin and their determined destination. Proposition 1 configuration discloses a deterministic relation in which concept (A) is considered to be a necessary condition―must be satisfied for concept (B). The model evolves in complexity due to the introduction of a moderating concept that qualifies the relation and links the two main constructs, representing (C) the type of ECommerce transaction identified as an import (generating outbound flows) or as an export (generating inbound flows). Here the effect of (A) over (B) exists or is stronger if (C) has a positive (inbound flows) or a negative (outbound flows) value. Proposition 1 relational model is put together as presented in Figure 2, containing two key relations in terms of necessary conditions: (1.1) There must be A―online money flows directionality―,

Figure 2. Proposition 1. Relational Model Configuration.

to obtain B―an effect over Money Supply―; and (1.2) there must be C―export/ import type of ECommerce transaction―, to obtain A―an effect over online money flows―, to be related to B. In this relation is observed that Concept A (online money flows) is divided in two classifications (inbound/outbound) that dichotomizes this concept, generating a differentiated effect that leads to recode Concept B into a dichotomous concept (+/−) as well.

Property 1) Directionality. The rationale expressed above leads to consider Directionality as an essential property of the relation between cross border online money flows and Money Supply that could be stated as follows: Online Money Flows are related to Money Supply by adding or subtracting the absolute value of an ECommerce transaction according to its origin as online purchase or online sell operation. From the theory building perspective, Directionality property effect is measured by the positive or negative value amount of online money flows affecting Money Supply size. Diagram 5 explains how Proposition 1 is operationalized.

Upper segment of Diagram 5, explains the connection between the electronic business cycle chain activities (order/purchase/payment/electronic transfer/con- firmation/invoicing) from which paperless money transactions emerge and online money flows networks configured for its connection to Money Supply of countries engaged in such transactions. Aware that the physical movement of goods (storage, shipping, delivery, transportation, etc.) has an origin/destination pattern of its own, it is expected that cross border ECommerce Total Amount Value results became the net effect of online money flows over country’ total Stock of Money, registered as growth or reduction of its M2 Aggregate the changes in its amount could have either a positive effect, a negative effect and/or internal compensation effect on Money Supply size and composition if ECommerce transactions are completed within a country. Lower segment of Diagram 5 shows the bidirectional character of the connection when simultaneous

Diagram 5. The directionality property identified in the relation between online money flows and money supply.

executions of buying-selling operations by a same country are included, shaping in this way countries’ online money flows network profile.

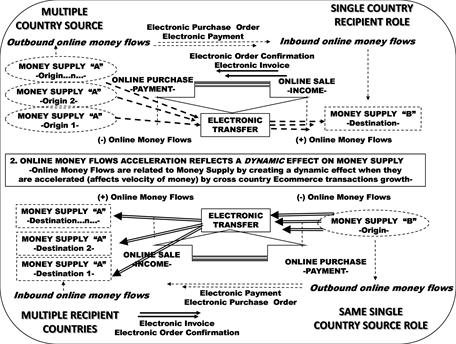

Property 2) Dynamism. As ECommerce activities grow in both directions- marked by simultaneous action in upper and lower segments of Diagram 5-, online money flows accelerate its frequency making money pass faster from one holder to the next. This dynamic connection is related to the concept of velocity of money that refers to the velocity by which money in circulation changes from one holder to other. The rationale behind this idea is framed by Money Theory. The concept introduced as money rapidity by Thornton [72] , appears as main component of Fisher’s [73] Money Theory as velocity (v), referring to the rate at which money passes in a given time period from one holder to the following. Monetary authorities explain that this rate of turnover of money supply or money speed measures the number of times that a currency unit (USD$, RMB, $MEX Peso, etc.) is used to purchase final goods or services included in the country’s GDP [74] . The importance of money flows moving through Internet to their Money Supply destination is taken to a view through the lens of Quantitative Theory of Money assumptions [75] [76] , hat postulates that the amount of Money Supply has a direct, proportional relationship with the price level, inflation , the exchange rate and the business cycle [77] , as it evolved into Monetarism [78] whose main statement is that there is a close and stable association between money supply and inflation, mainly because it is possible to avoid inflation with proper regulation of monetary base’s growth rate. Quantitative Theory of Money has been challenged during one Century by figures of the field either arguing that Money Supply does not strictly determines the price level pointing that is focused on the supply of money without explaining the demand of money, or providing reasons that even in the case of an excess of liquidity Money Supply has no measurable effect on prices [79] . The theoretical discussion of this issue and/or its effect is out of the scope of this research study. This property is identified as Dynamism in the relation between online money flows and Money Supply, observable in terms of the effect of online money flows rate of growth over Money Supply, as expressed in Proposition 2 as follows.

Proposition 2. Online money flows are related to Money Supply by creating a dynamic effect on the total amount of money when they are accelerated by cross-border Ecommerce activities growth.

Ecommerce market growth, as consequence of acceleration of the frequency of transactions among business partners, creates a faster movement of online money flows which is identified with the velocity of cash money in circulation. This proposition is oriented to identify what happens to Money Supply when online money flows increase their speed of growth, being for this reason identified as a deterministic relation of (A) and (B) that could be stated either as an increasing or a decreasing relation, even when it is a partly increasing/decreasing relation, under this perspective the relevant issue is one specific value for each (B) and (A) components.

Based on this reasoning, Proposition 2 is build up by a complex model based on a deterministic relation in which (2.1) online money flows low/high dynamism is a sufficient condition (A) if satisfied for Money Supply (B) growth/re- duction. Complexity rises by the introduction of a mediating concept (Y) that links (A) and (B) concepts as necessary condition (2.2)―there must be ECommerce dynamism―to obtain (A)―an effect over online money flows value amount―.

As Figure 3 describes, if there is an online money flows acceleration due to cross border ECommerce activities growth, (A), then there will be a (B) dynamic effect on the amount of Money Supply. In this relation the condition A and the effect B can each have only two values: the condition A can be present or absent and the effect of B can be present or absent, then there are three possible combinations, being the third one out of the scope of this research.

Figure 3. Proposition 2. Relational model configuration.

The configuration of the relations operationalized in Diagram 6, suggests that is reasonable to consider Dynamism as a characteristic of the relation existing between online money flows and Money Supply stated as follows: Online Money Flows are related to Money Supply changes in its total amount, because online money flows acceleration reflects the velocity of use of cash money in circulation―Money Supply’s, M1 Aggregate/narrow money stock―that is transformed into highly liquid assets other than cash that can be quickly exchanged by cash known as Quasi-Money/Near Money, being both of them M2 Aggregate’ components. In consequence, is reasonable to identify Money flows on the Internet with highly liquid assets other than cash that can be quickly exchanged by cash, known as Quasi-Money, being then favored the idea of the emergence of a new different component to be integrated into the Money Stock structure. This is a key finding, under the light of theoretical considerations sustaining that the proportion of transactions facilitated by quasi-money as medium of payment measured by the M2/GDP ratio is considered as a reliable macroeconomic indicator of Money Oversupply [80] , because if money growth is outpacing the total economic growth, there will be a larger amount of money after the same amount of goods. The core component of the dynamism property relies on the notion that cross border ECommerce electronic money transfer is a process by which cash money in circulation (M1)―covering orders placed―is transformed into highly liquid assets other than cash, not suitable as exchange mediums, that can be quickly changed into cash or checking deposits referred to as Quasi-Money (M2), making reasonable to expect that the combination of the two forces―growth and acceleration―results in dynamic changes for Money Supply net value.

Diagram 6. The Dynamic property of the relation between online money flows and Money Supply.

3) Intensity Property. The diffusion of Ecommerce business models as well as the diversification of the models lead to a Global Marketspace creation with a growing number of countries acting as multiple source of payment when a purchase transaction is completed there. Such expansion generates outbound online money flows directed to recipient/destination countries where the money value of the transaction (payment) is registered, representing to the partner inbound online money flows introduced with different intensity.

To benefit clarity over the complexity of this relations, they are illustrated in Diagram 7 identifying in the left side, as country’ outbound online money flows, the value of the transactions in which the payment is completed. The block of countries registered in the left side became the multiple source of incoming or inbound online money flows to the recipient countries as represented in the right side of the diagram. A deep analysis following the lines of Origin 1 of down the left side, indicate that its outbound online flows are connected to Destination 1 and Destination 2, completing payment operations by means of electronic transfer. In that sequence of ideas, it is reasonable to expect that if the multiple country source expands (Origin…n…), the number of transactions will increase creating an effect over the value of inbound online money flows of the correspondent recipient country playing as seller in the right side. The described effect works on the other way when the multiple country source is reduced. The size of the total value of the number of transaction executed from one country to another is referred to as intensity considering it as the quality of having a strong effect as well as to the strength of something that can be measured [81] .

ECommerce transactions growth may possibly be originated either by the expansion of prevailing ECommerce markets, as well as by the incorporation to

Diagram 7. The Intensity property of the relation between online money flows and Money Supply, under a cross-border environment.

these operations of new countries that introduce more Global suppliers and push forward the size of the customers base, thus generating an effect over the number of transactions implicated in cross border online money flows due to increasing payment operations. Intensity of transactions reflects in the amount of their correspondent online flows value, providing basis to the view of the extended effect over the Money Supply amount of countries engaged in the activity accordingly to the directionality property of online money flows and Money Supply relation. As previously explained in the stated research purpose, an explicit mention is given to the importance of the cross-border condition in which the referred relation is hold. Upon this reasoning Proposition 3 is stated as follows:

Proposition 3. The amount or size of Money Supply is related to online money flows reaction to the intensity of ECommerce cross border operations.

The rationale behind this proposition is that accordingly to ECommerce number of transactions amount, or size and growth rate, cross border online money flows amount has a changing effect over the amount or size of Money Supply value,―that eventually can be measured by means of quantitative hard data analysis―, suggesting a property of intensity in the relation existing between them. As stated, Proposition 3 is focused in the what happens to Money Supply amount when the amount or size of cross border online money flows is accentuated either by growth/reduction in the number of ECommerce transactions, as presented in Figure 4.

The Model in Proposition 3 structure, disclose a complex deterministic relation combining two types of conditions, being concept (A) a sufficient condition (3.1) for concept (B) if there are online money flows intensity (A) then there will be Money Supply (B) amount-requires to be enabled by (C) as (3.2) a necessary condition affecting (A)―there must be intensity in the amount size/rate of growth of cross border ECommerce transactions (C) to obtain an (A) to be related with (B). In this model other difference with Proposition 1 model is observed by the introduction of (C) a mediating concept that links (A) and (B) concepts as a necessary condition for the existence of a causal relation, being ECommerce cross border operations amount value size, or growth rate-referred

Figure 4. Proposition 3. Relational Model Configuration.

to as Intensity―component (C) to which online money flows amount value size, or growth rate directly reacts, with the consequent effect over (B).

4) Structural Property. As previously explained, Monetary Aggregates are key components of measures used for money supply and GDP comparison. Flows of money moving through Internet (Electronic Money, Virtual Money or Digital Money), by means of Electronic Transfer, are identified with Quasi-Money due to its characteristic of being liquid assets that can be quickly exchanged by cash. Considering this premise, if cross border ECommerce money flows are captured into M2 of countries engaged in such transactions, support is found for the idea that they could either reduce or fuel velocity and amount of this money aggregate. If so, attention must be taken to the changes provoked, because there is a light indicating that a danger for prices could be at sight.

This rationale supports the previous idea that cross border online money flows from ECommerce as introduced into engaged countries’ money stock became a new M2 aggregate component that should be monitored through monetary police. Then, cross border ECommerce money flows play a role as liquid assets, being for that reason a structural component of Money Supply, in the clear understanding that they are not a new issued currency displacing or acting in parallel of any existing currency. Originated by ECommerce transactions worldwide, online money flows represent intangible, paperless liquid assets moving instantly across borders, by means of Information Technology infrastructure creating direct links between buyers and sellers enabled by electronic transfer schemes. These liquid assets are not identified so far with existing money aggregates included as Money Supply components, even though when they are fully accepted as money representation of transactions completed online. This order of ideas give significance to the notion of online money flows as a new and autonomous component of quasi-money or Money Aggregate M2, being then a structural component of a country’ total amount of Money Stock (Money Supply), with a consequent effect―either positive or negative―over its structural configuration as well as on its size and growth rate. This implication brings visibility to the importance of online money flows in Money Supply, as a component of M2 revealing a structural connection, supporting Proposition 4:

Proposition 4. Online Money Flows identified as a new and autonomous component of Quasi-Money in Money Aggregate M2, has a structural connection with Money Supply with a resulting effect over its total amount and growth rate.

This proposition as is stated, is focused in the why happens, as changes are expected to happen in Money Supply amount, size and growth rate when online money flows are incorporated into its structure as a new and autonomous Quasi Money/Near Money component. The Model in Proposition 4 rises complexity featuring a network configuration by interweaving concepts and conditions from the previous propositions, shaping a single theoretical body of relations or online money flows effects theory. Starting from the basic A affect B structure relation, identified as a deterministic relation (4.1) where If A is higher, then B is higher, being a sufficient condition linking A and B (4.2). The directionality property from Proposition 1 is introduced (4.3) as a means to distinguish online money flows’ type effect on Money Supply as moderating concept (C.0) to qualify the relation in accordance to the positive or negative differentiated effects that the type of ECommerce operations produce as a necessary condition affecting A to be related with correspondent differentiated effects of (B), the relation is expressed as differentiated types of (A: A1, A2) affects differentiated types of (B: B1, B2) explained previously as dichotomy.

The model presented in Figure 5, describes how Proposition 4 evolves into two paths opened according to (C1) the sales-export-inbound online money flows process or to the (C2) purchases-import-outbound online money flows process affecting (A) to be related to (B). This differentiation is at the core of Proposition 4, as directionality moderates the effect of (A) on different Money Supply components (B1 or B2) or Money Aggregate M2 components as identified previously: M1 Aggregate/narrow money stock that is transformed into highly liquid assets other than cash that can be quickly exchanged by cash known as Quasi-Money. Upon this reasoning, Dynamism from Proposition 2, and/or Intensity of Proposition 3, takes their place as C0 (:C0.1-dynamism, C0.2-intensity) a mediating concept that links A (: A1, A2) and B (: B1, B2) concepts as a necessary condition for the existence of a causal relation (4.4). Being M2 the focus of interest in this research, the essence of this proposition is that the effect of online money flows on Money Supply is different for Money Aggregate M2 components: Quasi-Money/Near Money and M1, as identified in Figure 5.

Figure 5. Proposition 4. Relational model configuration.

The relation stated in Proposition 4 introduces a new perspective into the research, as it provides a basis to ponder that online money flows―as M2 componentmight be acknowledged as the operational link between the digital/elec- tronic commerce activities and the physical monetary structure of a country’ economy, supporting the notion that being online money flows one new additional component of M2, they will be absorbed by a country’s Money Supply―as already reported by the European Central Bank-, challenging so the idea of the presence of a new digital economy operating in parallel by itself. The introduction of Monetary Theory view into the research Conceptual Framework developed for this analysis, takes the initial Research Question into a second layer of analysis as follows:

RQ. What is the nature of the relation between online money flows and Money Supply in its Money Aggregate (M2) component referred to as Quasi- Money?

The hypothesized relations expressed by the set of four propositions could be considered as the foundation of the theory development process in which causal relations between two constructs are hypothesized under determined conditions. Each of the properties derived from the propositions formulated are actionable by observable measurement indicators as required by the research purpose. Results from the theory/data matching process realized to this point, provide an insight to the answer to this question, remaining implicit that online money flows refers to those derived from cross border ECommerce operations following a close loop type of movement that set in motion inbound flows for destination countries playing as exporters, and outbound flows for those in the purchaser side, creating a net value that is far to be quantified due to the general acceptance of E-Commerce sales value amount as indicator of the activity and/or to the absence of direct registers of the referred flows. The set of propositions formulated suggest that the relation between online money flows and Money Supply has four major characteristics: directionality, dynamism, intensity, and structural, that integrate the nature of that relation as a foundation for theory building. As displayed in Diagram 8, the directionality (+/−) property configures a loop due to inbound and outbound flows constantly affecting Money Supply by their dynamism (xxxx)―growth rate―and their intensity (++++)―number of transactions,―producing continuous change effects over Money Supply size due to the structural (%) characteristic.

7. The Analysis Results

7.1. Abduction Process. Stage 1: The Rule

A necessary next step in the selected research approach is to identify how the theoretical findings related to the Research Question works in the field of the phenomena interpretation. Following the abduction process sequence, in order to focus the analysis in the phenomenon under study a rule is identified from the analysis of Ecommerce key data estimations. The configuration of this rule is

Diagram 8. Characteristics identified for the nature of the relation between online money flows and Money Supply under cross border ECommerce context. Basic Propositions set.

made by two main components: 1) the new business model based on a technology infrastructure operated with the purpose to gain benefits from a new market created on a Global basis―which is the microeconomic view―and 2) the composition of a macroeconomic policy component which is the country’s Money Supply regulated as a Monetary Policy by Central Banks. Other meeting points of electronic money flows and macroeconomic policies are identified in Tax Policy, Trade Balance, GNP structure/composition and International Reserves among others. The interaction of the two elements is ruled by the fact that: each time a purchase or business transaction occurs―is completed―there is necessarily a matching money transaction completed by means of Electronic Transfer resulting in the creation of intangible online money flows circulating within and across countries 24/7, representing highly liquid assets other than cash identified as Quasi-Money in M2 Aggregate of Money Supply components.

The rationale behind this rule is provided by the shortening of Information Technology innovation cycle that leaded to the emergence of Internet as a public network infrastructure, the development of Product ID and electronic communications standards, software development and hardware design improvements. IT role in Internet moved from being a passive informative channel to be an active transactional channel with its own new payment schemes operating intangible online money flows in an emerging online market available 7 × 24 × 365 to worldwide atomized customers requiring for payment methods using the same technology infrastructure. In this scenario market boundaries changed due to the emergence of a new mode of commerce termed Electronic Commerce/E- Commerce/B2C and to the development and adoption of new technology based interactive processes among business partners referred to as Electronic Business/E-Business/B2B by a previoulsly quoted text book [19] , both of this new business practices require to close their commercial cycle by money transfer modes to be used through the Open Web. Under this context, emerged the electronic transfer as the highway to move money flows resulting from inter and cross border ECommerce transactions representing highly liquid assets other than cash moving either within a country and/or with a determined origin in or a destination to country’ Money Supply.

7.2. Abduction Process. Stage 2: The Results

7.2.1. The Online Money Flows Insights

Moving forward in the abduction process, results in terms of data are incorporated into the analysis. The rule is supported by the available estimated data in regard of the amount of online flows created by ECommerce transactions, representing liquid assets related to Money Supply structural components, as revealed by the size of the online market in permanent growth, estimated by eMarketer in a range from 23%―per year in average from 2012 to 2015 [82] to 24% by Ecommerce Foundation for the same time period [33] . The relevance of this business mode is appreciated considering that in 2016 according to the mentioned first source, E-Commerce registered 26.4% of Worldwide buyer penetration in terms of population being Mobile payment, as well as mobile commerce solutions rapid changes, considered to be drivers of ECommerce’ share significant growth. Latest numbers on the matter registered by the Ecommerce Foundation reveals descendent annual growth rates of 23.3%, 19.9% and 17.5% in 2014, 2015 and 2016, suggesting that the market is on its way to maturity [30] . The firsbt referred source on the matter [82] provide data in terms of worldwide retail, considering that Global web sales accounted for nearly 6.4% in 2014 moving to 8.6% in 2016, forecasted to reach 12.8% by 2019, representing an estimated worldwide ECommerce retail money value estimated in year 2014 in US$ 1336 billions growing to US$ 2050 billion in 2016, with a projection to US$ 3578 billion by the year 2019. Data from this same source [82] shows that China and the USA accounted for 55% Global internet retail sales during the period 2014-2016, leading world’s Ecommerce during that time frame.

Comparing data sources, estimations in Table 1, from ECommerce Foundation reports from 2015 [33] and 2016 [30] , expressed in Euros register higher numbers for the same years, as identified in the grow pattern moving from 1 895 billion Euros in 2014 to 2 273 billion in 2015 and a sales amount value of 2 671 billion for 2016. If this tendency is sustained, eMarketer forecasts could be closer than 2019. The use of data aggregated at macro level provides insight regarding the magnitude of ECommerce transactions worldwide, the money flows involved on it and the dynamic of its growth exposing the expansion of the business model and its influence over traditional commerce paradigm.

From macroeconomics indicators view, the share of Ecommerce in worldwide Gross Domestic Product (GDP) moved from 1.34% in 2011 to 3.11% in 2015 according to Ecommerce Foundation [33] . Data from Table 2 disclose the

Table 1. Global ECommerce growth.