Predicting Stock Prices Using Polynomial Classifiers: The Case of Dubai Financial Market

88

6. Conclusions

Two prediction models developed in this study. The first

model was developed with the well-known back propa-

gation feed forward neural network. The second model

used here is based on polynomial classifiers which are

being used for the first time in stock prices prediction.

The inputs to both models were identical, and bo th mod-

els were trained and tested on the same data in three dif-

ferent training scenarios and two prediction modes. The

data used here is the historical p rices for two of the lead-

ing stocks in Dubai F i n ancial Market.

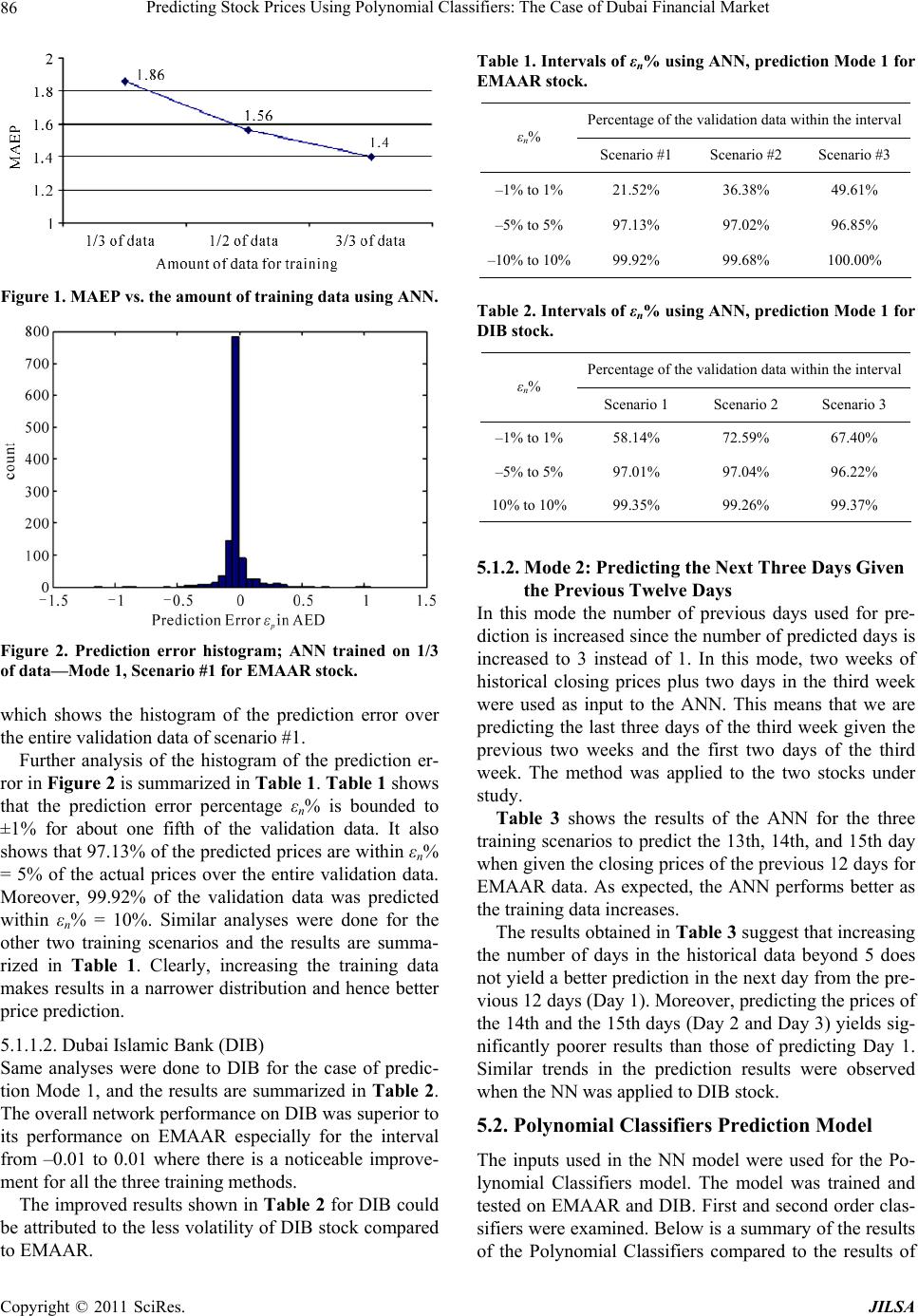

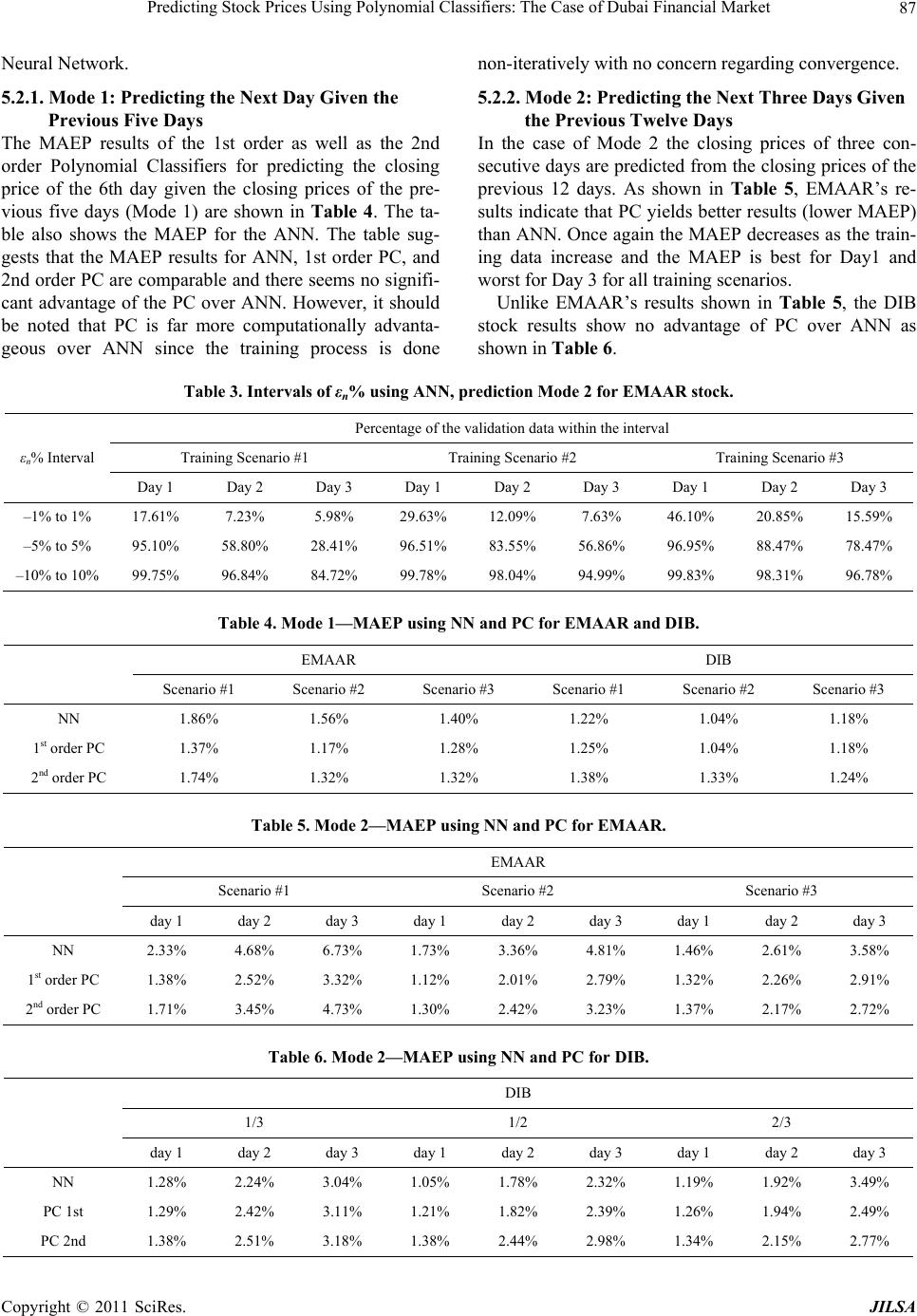

In general, both models achieved outstanding resu lts in

terms of mean absolute error percentage (MEAP). Both

models achieved around 1.5% MEAP in predicting the

next day, 2.5% MEAP in predicting the second day, and

around 4% MEAP in predicting the third day. The pre-

diction accuracy of the two models was certainly re-

markable, where around 60% of the predicted prices of

the first day, 50% of the predicted prices of the second

day, and 35% of the predicted prices of the third day,

were all within –1% to 1% of the actual prices of the

three days.

When comparing the neural network and polynomial

classifiers prediction models, it was found that first order

polynomial classifier performed comparable to or slight-

ly better than the neural network. Whereas the second

order polynomial classifier could barely achieve similar

results on the stocks used in this study. Further work can

be done using other stocks in similar emerging markets

and mature markets, to verify this conclusion.

On the other hand it should be noted that PC is a lot

more computationally efficient than ANN since its

weights can be obtained directly an d non-iteratively fro m

a closed formula as shown in Section 3.1.

REFERENCES

[1] E. Fama, “Efficient Capital Markets: A Review of Theory

and Empirical Work,” Journal of Finance, Vol. 25, No. 2,

1970, pp. 383-417. doi:10.2307/2325486

[2] J. Yao, C. Tan and H. Poh, “Neural Networks for Tech-

nical Analysis: A Study on KLCI,” International Journal

of Theoretical and Applied Finance, Vol. 2, No. 2, 1999,

pp. 221-241. doi:10.1142/S0219024999000145

[3] D. Brownstone, “Using Percentage Accuracy to Measure

Neural Network Predictions in Stock Market Move-

ments,” Neurocomputing, Vol. 10, No. 3, 1996, pp. 237-

250. doi:10.1016/0925-2312(95)00052-6

[4] K. H. Lee and G. S. Jo, “Expert System for Predicting

Stock Market Timing Using a Candlestick Chart,” Expert

Systems with Applications, Vol. 16, No. 4, 1999, pp. 357-

364. doi:10.1016/S0957-4174(99)00011-1

[5] W. Leigh, M. Paz and R. Purvis, “An Anaysis of a Hybrid

Neural Network and Pattern Recognition Technique for

Predicting Short-Term Increases in the NYSE Composite

Index,” Omega, Vol. 30, No. 2, 2002, pp. 69-76.

doi:10.1016/S0305-0483(01)00057-3

[6] R. Choudhry and K. Garg, “A Hybrid Machine Learning

System for Stock Market Forecasting,” World Academy

of Science, Engineering and Technology, Vol. 39, 2008,

pp. 315-318.

[7] G. Armano, M. Marchesi and A. Murru, “A Hqybrid

Genetic- Neural Architect ure for Stoc k Indexes Forecasting,”

Information Sciences, Vol. 170, No. 1, 2005, pp. 3-33.

doi:10.1016/j.ins.2003.03.023

[8] J. Yao and C. Tan, “A Case Study on Using Neural Net-

works to Perform Technical Forecasting of Forex,” Neu-

rocomputing, Vol. 34, No. 1-4, 2000, pp. 79-98.

doi:10.1016/S0925-2312(00)00300-3

[9] D. Senol and M. Oztuman, “Stock Price Direction Predic-

tion Using Artificial Neural Network Approach: The Case

of Turkey,” Journal of Artificial Intelligence, Vol. 1, No.

2, 2008, pp. 70-77. doi:10.3923/jai.2008.70.77

[10] A.-S. Chen, M. Leung and H. Daouk, “Application of

Neural Networks to an Emerging Financial Market:

Forecasting and Trading the Taiwan Stock Index,” Com-

puters & Operations Research, Vol. 30, No. 6, 2003, pp.

901-923. doi:10.1016/S0305-0548(02)00037-0

[11] D. Enke and S. Thawornwong, “The Use of Data Mining

and Neural Networks for Forecasting Stock Market Re-

turns,” Expert Systems with Applications, Vol. 29, No. 4,

2005, pp. 927-940. doi:10.1016/j.eswa.2005.06.024

[12] Q. Cao, K. Leggio and M. Schniederjans, “A Comparison

between Fama and French’s Model and Artificial Neural

Networks in Predicting the Chinese Stock Market,”

Computers & Operations Research, Vol. 32, No. 10,

2005, pp. 2499-2512. doi:10.1016/j.cor.2004.03.015

[13] I. Kaastra and M. Boyd, “Designing a Neural Network for

Forecasting Financial and Economic Time Series,” Neu-

rocomputing, Vol. 10, No. 3, 1996, pp. 215-236.

doi:10.1016/0925-2312(95)00039-9

[14] N. Kohzadi, M. Boyd, B. Kermanshahi and I. A. Kaastra,

“Comparison of Artificial Neural Network and Time Se-

ries Models for Forecasting Commodity Prices,” Neuro-

computting, Vol. 10, No. 2, 1996, pp. 169-181.

doi:10.1016/0925-2312(95)00020-8

[15] D. Olsona and C. Mossmanb, “Neural Network Forecasts

of Canadian Stock Returns Using Accounting Ratios,”

International Journal of Forecasting, Vol. 19, No. 3,

2003, pp. 453-465. doi:10.1016/S0169-2070(02)00058-4

[16] K. Assaleh and M. Al-Rousan, “Recognition of Arabic

Sign Language Alphabet Using Polynomial Classifiers,”

EURASIP Journal of Applied Signal Processing, Vol.

2005, No. 13, 2005, pp. 2136-2145.

doi:10.1155/ASP.2005.2136

[17] K. T. Assaleh and W. M. Campbell, “Speaker Identifi-

cation using a Polynomial-Based Classifier,” Fifth Interna-

tional Symposium on Signal Processing and Its Appli-

cations ISSPA, Brisbane, Vol. 1, August 1999, pp. 115-

118.

[18] W. M. Campbell , K. T. Assaleh a nd C. C. Broun, “Speake r

Copyright © 2011 SciRes. JILSA