P. Das

Little work was attempted in this direction. Guastello (1995) showed low-dimensional chaos for US inflation

rates during the 1948-1995 era with Lyapunov dimensionality 1.5. He also confirmed that although there was

short time linear prediction of inflation rates, the global picture was, nonetheless, chaotic [6]. In another study

(2001) he stressed the presence of chaotic attractors for inflation rate in the US [7]. Results from linear and

nonlinear analyses provide overwhelming evidence in support of the nonstationarity of the inflation rate in

Africa [8]. We like to study this situation for some EU countries, as well as some other countries having its own

ForEx rate. Obviously, we are not attempting any analysis of justification of Euro. Our analysis will be confined

to understand the economic indicators, particularly inflation data in relation to ForEx rate through data analysis.

2. Data Collection

Detailed Inflation or CPI data: The inflation rate is based upon the consumer price index (CPI). The CPI

inflation rates used are on a yearly basis (compared to the same month the year before). For example, inflation

for January 2013 is difference over that in January 2012 expressed as per cent. Inflation.eu [9] maintains

historical data for many countries which have been used in this paper. We have collected data on monthly basis

from January 2000 to September 2013 for the following countries: France, Italy, Germany, Spain, Greece, India

and UK. So each country has a dataset consisting 165 data—one for each month. For Sri Lanka, data from

January, 2001 to April, 2008 are available, so data points are 88 in number from Department of Census and

Statistics. Government of Sri Lanka [10]. Singapore CPI data was taken from ‘Time Series on Monthly CPI

(2009 = 100) And Percentage Change Over Corresponding Period Of Previous Year’, Government of Singapore

[11].

3. Nonlinear Analysis of Inflation Data

Here we shall concentrate on detailed nonlinear data analysis of inflation data collected to get more insight of it.

The basic point we like to investigate is if CPI data analysis show chaos or not. For characterizing chaos both

qualitatively and quantitatively, we have to find Largest Lyapunov Exponent (LLE).

3.1. Test for Nonlinearity Using Surrogate Data Method

We follow the approach of Theiler et al. (1992) [12]. The surrogate signal is produced by phase-randomizing the

given data. It has spectral properties similar to the given data, that is, the surrogate data sequence has the same

mean, the same variance, the same autocorrelation function, and therefore the same power spectrum as the

original sequence, but (nonlinear) phase relations are destroyed. Details of the method for the countries con-

sidered have been given in the previous work [1] or as used with additional noise reduction (Çoban et al., 2012)

[3]. We used the TSTOOL package by Parlitz et al. (1998) [13], under MATLAB (2008) [14] software to create

surro gat e data for a scalar time series. From this analysis, we got some idea about the degree of nonlinearity

associated with the time series of foreign exchange data up to year 2008. We are not repeating the same analysis

because we are considering the same countries and compared to our previous data, we now have 450 more

points, which is only 5% of total only (from January 2008 to October 2009). But we certainly have to use the

result s.

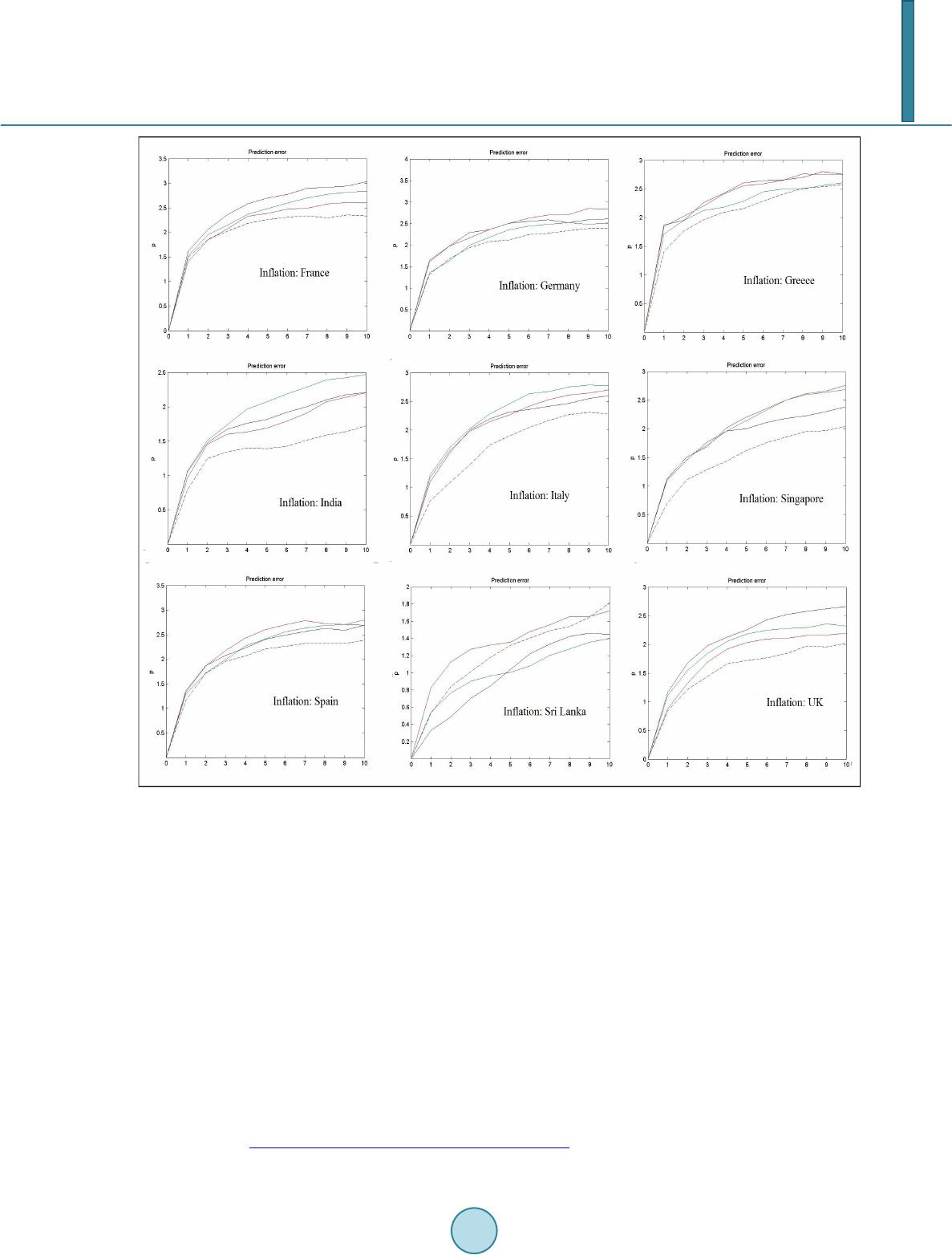

3.2. Finding Lyapunov Exponent Using TSTOOL Package

Chaotic processes are characterized by positive Lyapunov Exponent (LE)s calculated following the approach of

Wolf et al. [15], as explained in previous works [1] [2]. Again, we used the TSTOOL to find the LLE. The

function used is largelyap which is an algorithm based on work by Wolf (1985), it computes the average

exponential growth of the distance of neighboring orbits via the prediction error. The increase of the prediction

error versus the prediction time allows an estimation of the LLE [7]. In the particular MATLAB code, largelyap,

the average exponential growth of the distance of neighboring orbits is studied in a logarithmic scale, this time

via prediction error p(k). Dependence of p(k) on the number of time steps may be divided into three phases.

Phase I is the transient where the neighboring orbits converges to the direction corresponding to the λ the LLE.

During phase II, the distance grows exponentially with exp (λ tk) until it exceeds the range of validity of the

linear approximation of the flow. Then phase III begins where the distance increases slower than exponentially

until it decreases again due to folding in the state space. If the phase II is sufficiently long, a linear segment with