L. Fu, R. Fu

1.1.2. The Recognized Bases of Technological Enterprises

In light of the loose and low-cost principles, a high-tech enterprise can be recognized if it can meet one of the

following conditions:

A. enterprise has been identified as high-tech enterp r i se s;

B. private high-tech enterprise has been registered in the Provincial Science and High-Tech Department;

C. enterprise has implemented a municipal or maniple above the high-tech project in the past three years;

D. enterprise implements patent technique or independent proprietary intellectual rights.

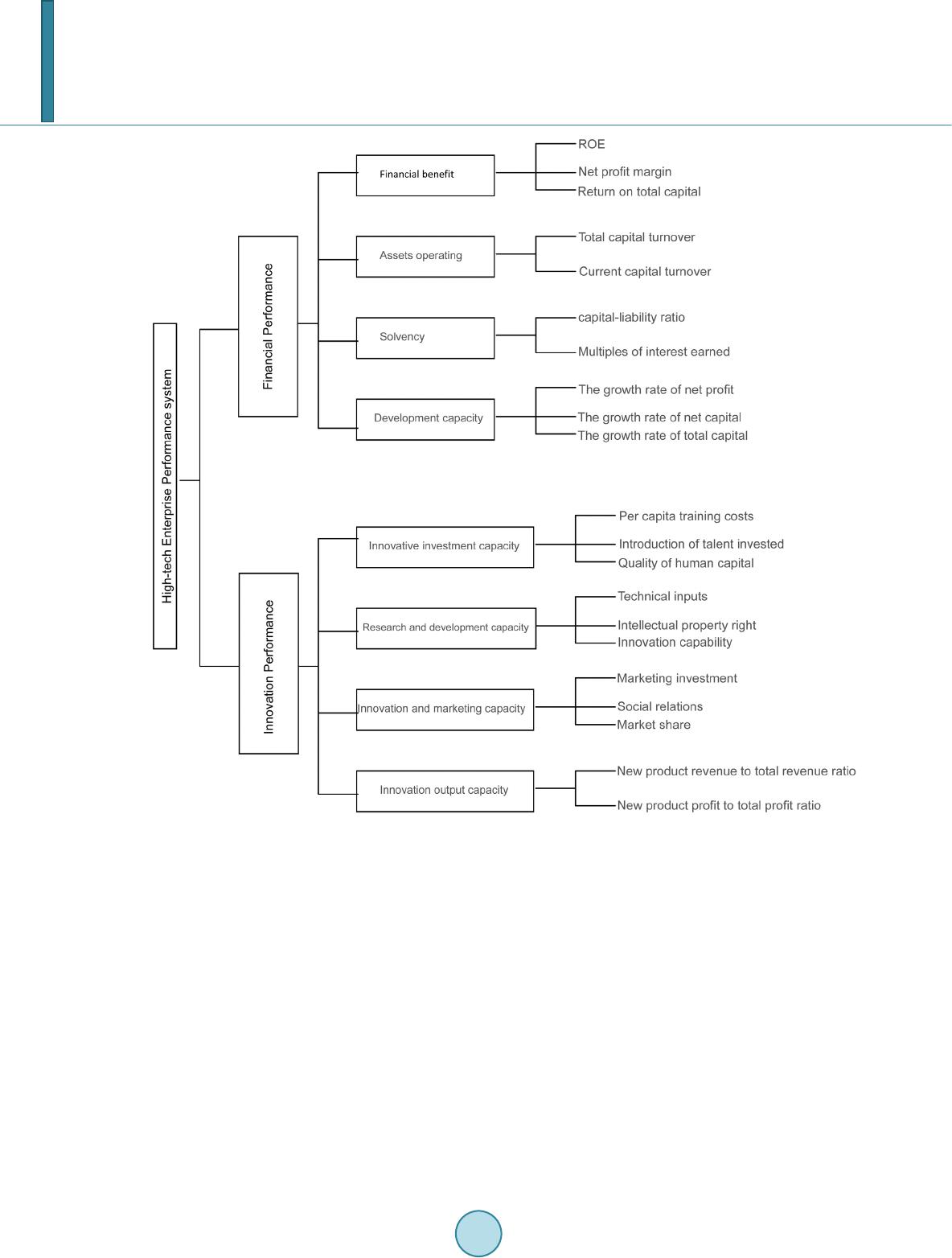

1.2. The Importance of a High-Tech Enterprise’s Performance

The essence of performance is a measure of management and control. It provides a reference to managers by the

comparison of an occurred result and a pre-determined criterion before they take a further step. Firstly, correct

performance for high-tech companies can assist investors to correctly understand the high-tech enterprises. Se-

condly, it makes the incentives function properly [2]. Furthermore, management methods and process innova-

tion of high-tech enterprises benefit from it.

However, enterprise production and management capabilities, process and results can be reflected through a

number of financial indicators and innovation ability index. According to the characteristics of technological

enterprise, its performance indicates the reality of the profitability and future growth and development potential.

Therefore, constructing a comprehensive scientific index system has become an important part of the perfor-

mance of the technological enterprises.

1.3. The Characteristics of Technological Enterprises

1.3.1. Enterprises with a Flexible Organizational Structure

The flexibility of its organizational structure is mainly reflected in two aspects. On the one hand, companies can

adjust the setting of the business functions in terms of the changes of the market. On the other hand, employees

can internally flow at any time according to the changes of the business. This flexibility allows the entire organ-

ization in a flexible flow state, able to change with the external market fluctuations.

1.3.2. Enterprises have Employees with a Strong Sense of Innovation and Innovative Capacity

The employees in the enterprise are initiative and knowledge-based. They possess the knowledge and skills of

the enterprise, the comprehensive judgment and decision-making ability, and are subject to full authorization

and incentive to work independently.

1.3.3. Speeding up the Product and Service Innovation of Enterprises .

Faced with the rapid changes in the environment, the enterprise provides products and services to the market

thro ugh the continuous, comprehensive and collaborative innovation faster than the competition to meet cus-

tomer needs, thus gaining an advantage in the market competition.

1.3.4. Production by Standardized Transition to the Non-Sta ndardized .

Enterprises should pay more attention to the market demand for d ifferentiat ion and the characteristics of indi-

vidual consumers. In addition, enterprise can adopt a non-standardized production according to customer demand.

Meanwhile, it utilizes small quantity and variety of production to replace the large quantities and single product

of traditional enterprises. Finally, high-tech enterprises obtain business growth through emphasizing innova tion.

2. The Principles of Constructing a High-Tech Enterprise Performance System

2.1. The Principle of Objective and Impartial

The inputs and outputs of the process of the hig h-tech enterprises are extremely complex and difficult to under-

stand. This leads to the performance very prone to subjective bias, which provides an opportunity to meet the

different purposes of the evaluators. Therefore, in the corporate performance, the evaluator must be judged aloof

and independent stance and exquisite competent. In order to reduce the influence of artificial factors of enter-

prise performance , enterprise should evaluate pros and cons objective stance, a fair attitude evaluate gains and

losses, reasonable way to measure corporate performance.