Modelling and Analysis on Noisy Financial Time Series

OPEN ACCESS JCC

Section 4, the experimental results are specified and

evaluated with the sample financial time series available

in book (Analysis of Financial Time Series) [3]. Section

5 concludes the paper.

2. Filters

Normally, the financial time series is embedded with

high level of noise (random trading behaviors), such as

white noise and colored noise. It is very difficult to de-

termine the level of such unknown noise and find the

appropriate filtering techniques that can separate the de-

terministic time series and random events. If the raw

noisy time series is less denoised, the prediction model

performs poorly due to the high level noise; if the noisy

time series is over denoised, the filtered time series loses

some genuine features of raw time series. The conven-

tional time series cannot filter such high level noise such

as financial time series. Indeed, the effective filtering is

dependent on the several factors, e.g., the ability to re-

move the noise, the types of noise, and the thresholds

estimation, etc.

In this paper, two different types of filtering tech-

niques are utilized in this paper: one is the traditional

non-linear low-pass filter with forward and backward

filtering (FBF) processes; another is the wavelet based

denoising method (WLD) for which the time series is

projected into orthogonal basis. Also, the measure crite-

rion known as approximate entropy (ApEn) is considered

to evaluate the performance of proposed filters.

2.1. Forward and Backward Filter

The forward-backward filter (FBF) actually is a matrix

with no-linear processing networks. It utilizes the

second-order matrix SOS and the scale vector G, by

conducting the forward and reverse the filtering pro-

cesses [5]. The scale G defines the weights of input sam-

ples. The SOS and G are defined by:

01 1121011121

02 1222021222

012 012

123456

G[ ]

LL LLLL

bbbaaa

bbbaaa

SOS

bbbaaa

wwwwww

=

=

FBF filters the time series X with the SOS filter de-

scribed by the matrix SOS and the vector G. After filter-

ing in the forward direction, the filtered sequence is then

reversed and run back through the filter. In this project,

the Butterworth second-order filtering is used for filter-

ing the time series.

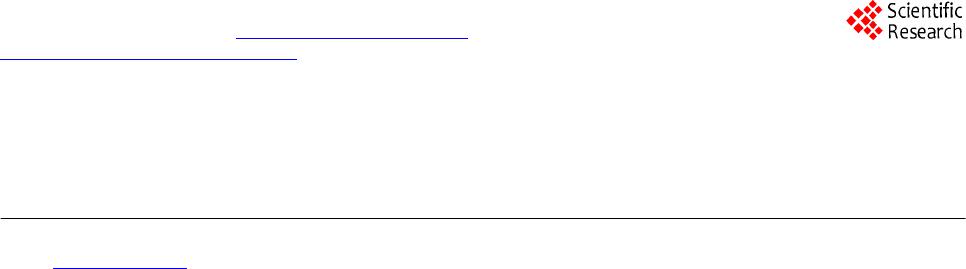

The example of FBF filtering process with the finan-

cial time series is illustrated in Figure 1.

2.2. Wavelet-Based Denosing

Wavelet theory is an emerging new signal processing

technique in recent two decades [6,7], which is called the

mathematical microscope due to it high recognition ac-

curacy in both time domain and frequency spectrum.

With the scaling factor a (dilation factor) and translation

parameter b, a, b ∊ R, and a ≠ 0. The prototype wavelet

is scaled and translated. The wavelet function can be

expressed as:

is the normalized factor, so as to make sure for

all a, b, Ψ() has the unit energy.

The concept of multiresolution was proposed by Mal-

lat and Meyer in 1989 [8], meaning that one signal can

be decomposed into the orthogonal projections and can

also be fully reconstructed. The components of the de-

composition are divided into the approximation (a) and

details (d) at different levels. The approximation repre-

sents the major feature of the signal and the details de-

scribe the detailed changes and noise. The time series can

be denoised by removing some ingredients from the pro-

jections in details.

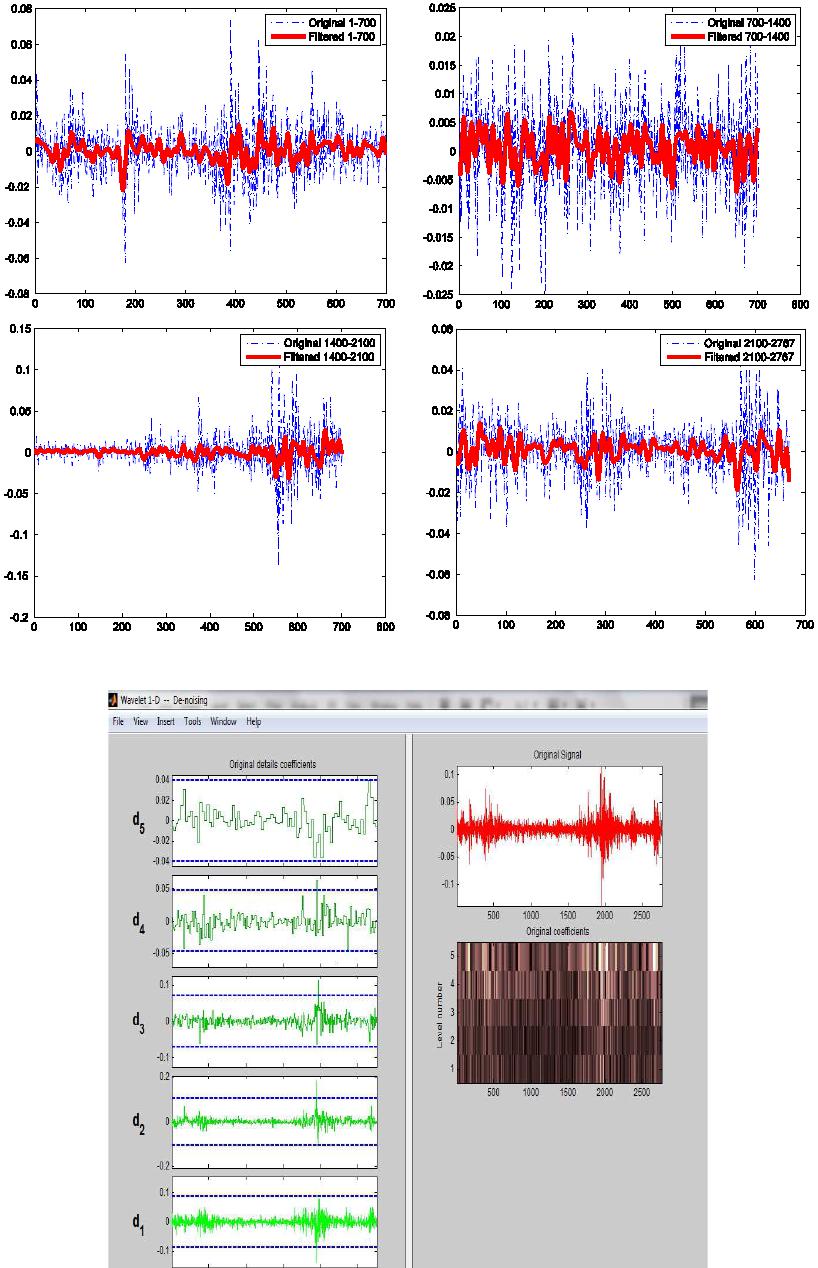

The example of wavelet denoising is given in Figure s

2 and 3.

2.3. Performance Measurement

To evaluate two filters proposed above, two measure-

ments are introduced: 1). One indicator is the fit rate of

autoregression model (AR), the details about AR model

are available in Chapter 3. 2). Another criterion known as

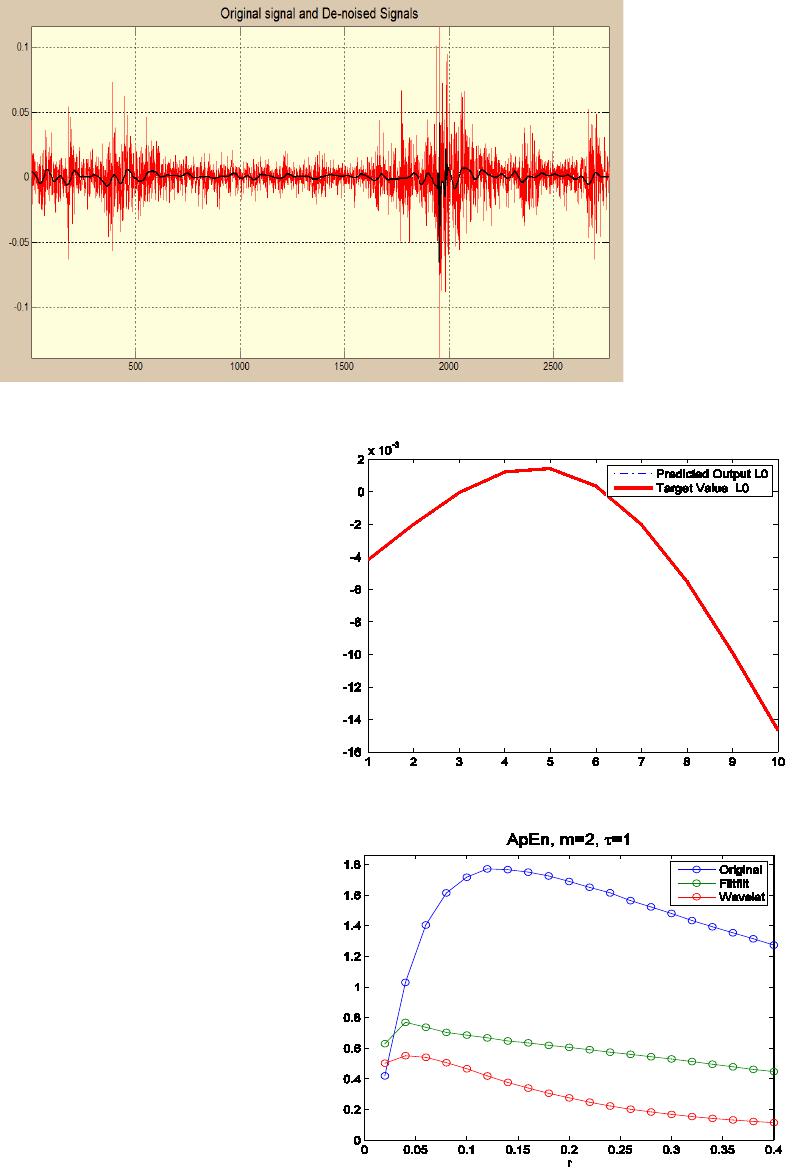

the approximate entropy (ApEn) [9] is also introduced.

The major ability of ApEn is to evaluate the time se-

ries by quantifying the amount of regularity and the un-

predictability of fluctuations. The successful applications

have been found in EEG signal diagnosis [10] and in

financial time series [11]. In [11], it was reported that the

uncertainty events such as the Asian financial crisis can

be detected by analyzing Hang Seng index. There are

two parameter m and r in ApEn. The value of m is be-

tween 2 - 3, and the value of r is about 0.2 × σ (σ is the

value of standard deviation of the time series).

The smaller of ApEn, the better regularity and trends

of the time series.

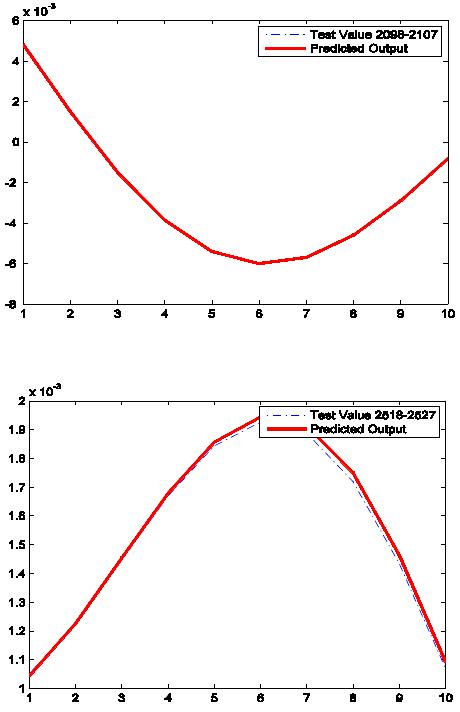

Here, an example is given to assess the performance of

two filters using AR model and ApEn. Firstly, I compare

the quality of filtering with time series L0 using AR(p)

model, detailed as below (FPE—final prediction error,

MSE—mean square error):

• For original signal L0, the results with AR (6) are: Fit

to estimation data—0.3754%, FPE—0.0002323, MSE

—0.0002308. Even AR with order of 30, the results