An Early Warning Model with Technical Indicators: The Case of Ise (Istanbul Stock Exchange)

180

00

10

ˆ

ˆ

H

H

A t-test was accomplished: 0

stat

ˆ

ˆ

tS

By the fulfillment of the condition tstat < ttable the H0

hypothesis is not rejected and the stability of the esti-

mated parameter values of the regarded 32 shares was

confirmed.

The estimated parameter values and stability test de-

termined for the selected 32 shares are in the appendix.

The results displays that the change of the number of

collections do not cause statistic change of the estimated

parameter values.

5. Conclusions

In summary, we can say that during the derivative of NSI

E: NSI C takes the value (−1) assumes that it is smaller

as it is; NSI C takes the value (0) if it lies between; NSI

C takes the value (+1) if it is larger as it is.

For all technical indicators with the computation of the

variables one day lagged, values are used. The conclu-

sion values of 250 shares are raised for the calculations

of the technical indicators. The technical indicators as the

argument were used for the determination of the parame-

ter values, and thereby altogether 250 models are set up.

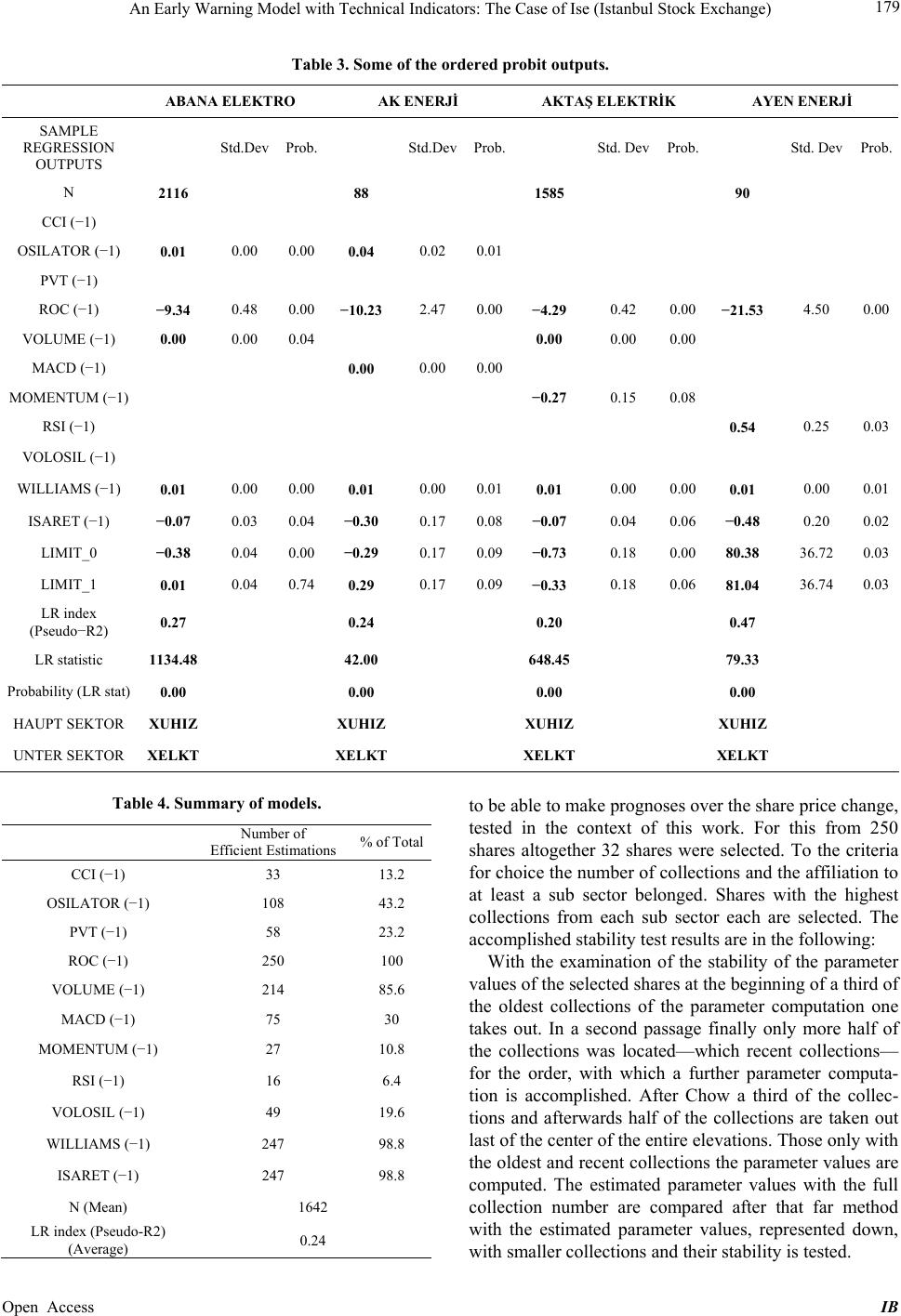

It participated interesting that the estimated parameter

values of the 250 shares were close. The CCI variable for

33 models, the OSILATOR variable for 108 models, the

PVT variable for 58 models, the ROC variable for all

models, the volume variable for 214 models, the MACD

variable for 75 models, the moment around variable for

27 models, the RSI variable for 16 models, the volume

OS IL variable for 49 models, the WILLIAMS variable

for 247 models and the NSI (−1) variable for 247 models

are efficient.

With those models, in which the technical indicators

represent the arguments, Turkcell, Anadolu Efes and

Ayen Enerji had extreme parameter values. Since the

number of collections is very small with these shares,

one can meet the acceptance that iterated parameter val-

ues are not reached.

5.1. Model Prognoses

With above the 32 shares select for the stability test of

the estimated parameter values, prognoses become for

one period of three months (10 October to 24 January

2007) accomplished. With these prognoses, the “NSI R”

(NSI calculated) of values is determined and derived

from these the “NSI E” (NSI estimated). The derived

“NSI E” of values is compared afterwards with the “NSI

R” (NSI real) values.

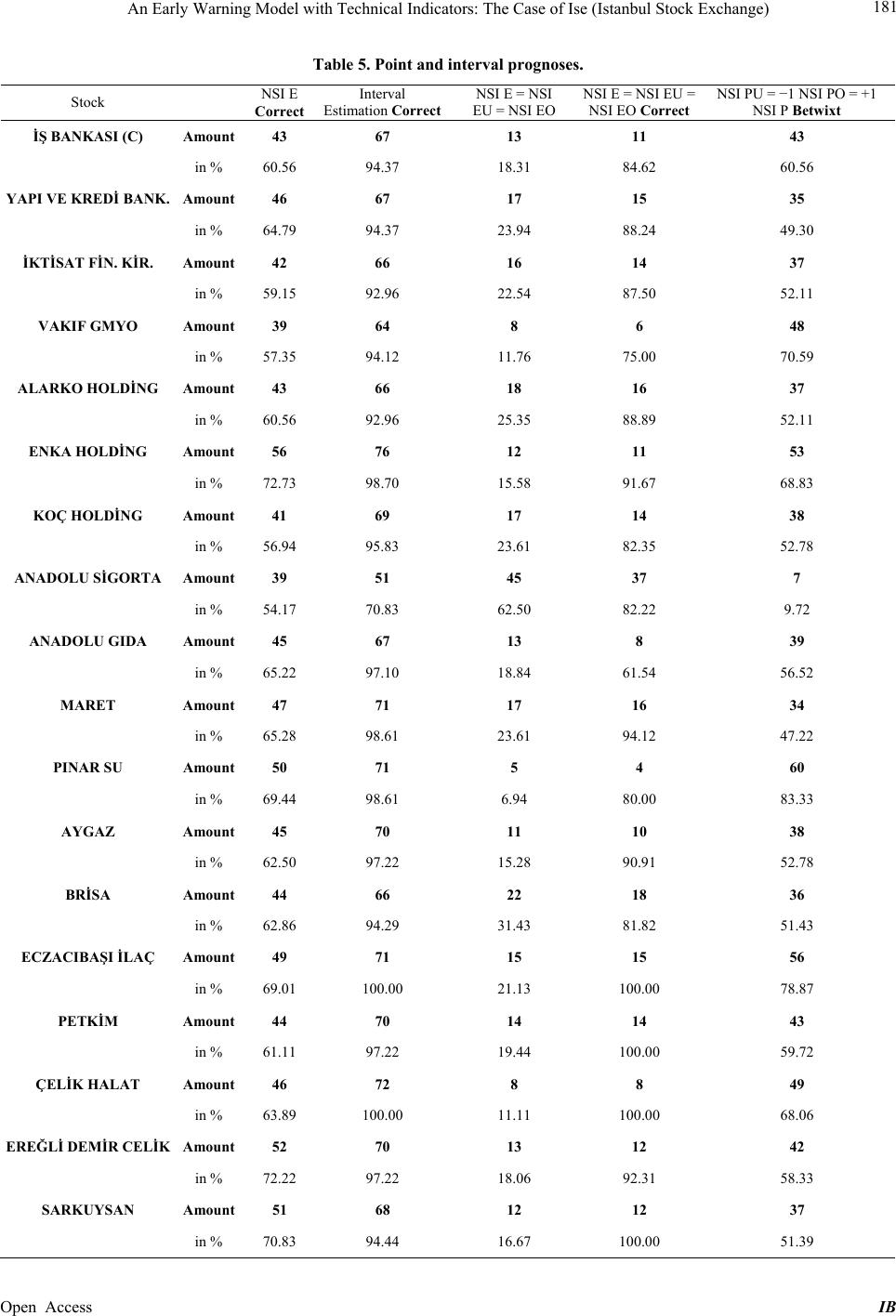

Point prognoses and interval prognoses are accom-

plished. In the context of the point prognosis, the values

of “NSI C” were determined with the Limit_0 and

Limit_1 being compared and “NSI E” derives from it.

“NSI C” was under Limit_0 to “NSI P” on (−1) and was

then specified. With the “NSI C” between Limit_0 and

Limit_1, “NSI E” is specified on (0) with a “NSI C” over

Limit_1 on (+1). After derivative of “NSI E”, it is com-

pared with “NSI R” and prognosis accuracy is deter-

mined. In the case of the point, prognoses resulted is

prognosis accuracy between 54 to 72 percent.

For the execution of the interval prognoses, addition-

ally the “NSI still becomes CU” value (NSI calculated

lower one limit) and “the NSI CO” value (NSI calculated

upper one border) is determined. With the help of these

two limit values, during the derivative of the “NSI E”,

the “NSI of EU” values (NSI prognosticated lower ones

limit) and “NSI of EO” values (NSI prognosticated upper

one border) are derived. It was checked whether the “NSI

R”-value is within these two values (between “NSI EU”

and “NSI PO”). With the regarded 32 models (ever a

model per share), “NSI R” is observed within these in-

terval values with a frequency from 70 to 96 percent.

The intervals (“NSI EU” and “NSI EO”) failed some-

times very closely and again very broadly. With very

close intervals (ex.: “NSI EU” = +1 and “NSI EO” = +1).

“NSI E” can speak with the interval borders of safe prog-

noses with the agreement of the point prognosis. On the

other side the interval borders far apart (“NSI EU” = −1

and “NSI EO” = +1) cannot be made safe statements

about the point prognosis “NSI E”. The reason for the far

interval borders lies in the high standard deviation and

the Limit_0 and Limit_1 values, for which again as in-

fluence of external factors is lying far apart, speculation

behavior is responsible.

With the regarded 32 shares, one could observe the in-

terval width of “NSI EU” within the observed period of 3

months = −1 to “NSI EO” = +1 between 9 percent and 83

percent, an average value of 57.4 percent for 32 shares

results. “NSI EU” = +1 to “NSI EO” = +1 was observed

with the 32 shares within the period by 3 months with a

frequency from 5.5 to 62.5 percent, and resulted in an

average value of 20.1 percent. When agreeing the “NSI

E”, “NSI EU” and “NSI EO” value an agreement with

“NSI R” which is determined between 61 and 100 per-

cent, i.e. with an average value of 89 percent.

In principle, one can say that with all securities with

18 (= 0.201 * 0.89) percent of probability safe prognoses

can be accomplished. In summary, we can say that one

with 63 percent of correct point prognoses altogether

with approx. 57 percent of all prognoses about no safe pro-

gnoses to talk can lie apart, and there the interval borders

far and with approx. 18 percent about safe prognoses to

tal can lie apart. 25 percent of the remaining can be k

Open Access IB