Study on the Efficiency of SMEs’ Bank Financing in Clusters 159

of the firm though inter-person relationships [6]. It shows

that a high level of inter-person relationship contributes

to businesses’ bank financing and played a role in the

financing process. Therefore, we assume that:

H1 The higher the level of inter-person relationship,

the higher the level of enterprise bank financing per-

formance.

2.2. Inter-firm Relationship and Bank Financing

High level of inter-firm relationships means that they do

not try to solve the problem in the process of damaging

each other's interests [7]. They do not care gain or loss in

the collaboration or have opportunistic behaviors. High

level of inter-firm relationship shows good performance

and partner history of the two sides and further improv-

ing the companies’ financial efficiency from banks [8].

Actually, mutual trusted businesses will pay extra efforts

to overcome difficulties and help each other to solve

problems because they understand the situation of each

other and have full information, so the good credit is

more likely to occur [9]. The more stable the long-term

oriented trade relationship between enterprises, the more

opportunities of external financing, the more possibilities

of enterprises’ getting financial resources from the bank.

Therefore, we assume that:

H2 The higher the level of inter-firm relationship, the

higher the level of enterprise bank financing perform-

ance.

3. Research Method

3.1. Sample and Data Collection

This paper uses statistical tool to analyze the model and

also based on through the literature review, expert con-

sultation and semi-open questionnaires, etc. Before

sending out the questionnaires, we will consult three ex-

perts about the description methods of questions and

contents, adjusting the questionnaire mainly from theo-

retical viewpoint and long-term management and con-

sulting experience. We elect several enterprises to do

further evaluation and interviews, consulting senior ex-

ecutives and in-depth interviews, and form the final

questionnaire used in this study.

On this basis, this research cooperates with Private

Enterprises Business Association in Wenzhou, Zhejiang

Province. We selected 700 companies randomly from the

Association's Business Directory, sent out700 question-

naires from early October 2007 to the end of 2008, and

collected 305 questionnaires back, reaching 43.5%.In the

returned questionnaires, there were 94 with incomplete

content or obvious errors and be removed as invalid

questionnaires. The 211 valid questionnaires were effec-

tive response, with a valid rate of 30.1%. In order to en-

sure that data does not exist non-response bias, we do

Chi-square analysis to early and late recovery question-

naire in the enterprise's employee number and sales

revenues. The result shows that the questionnaire in the

two groups has no significant difference, indicating that

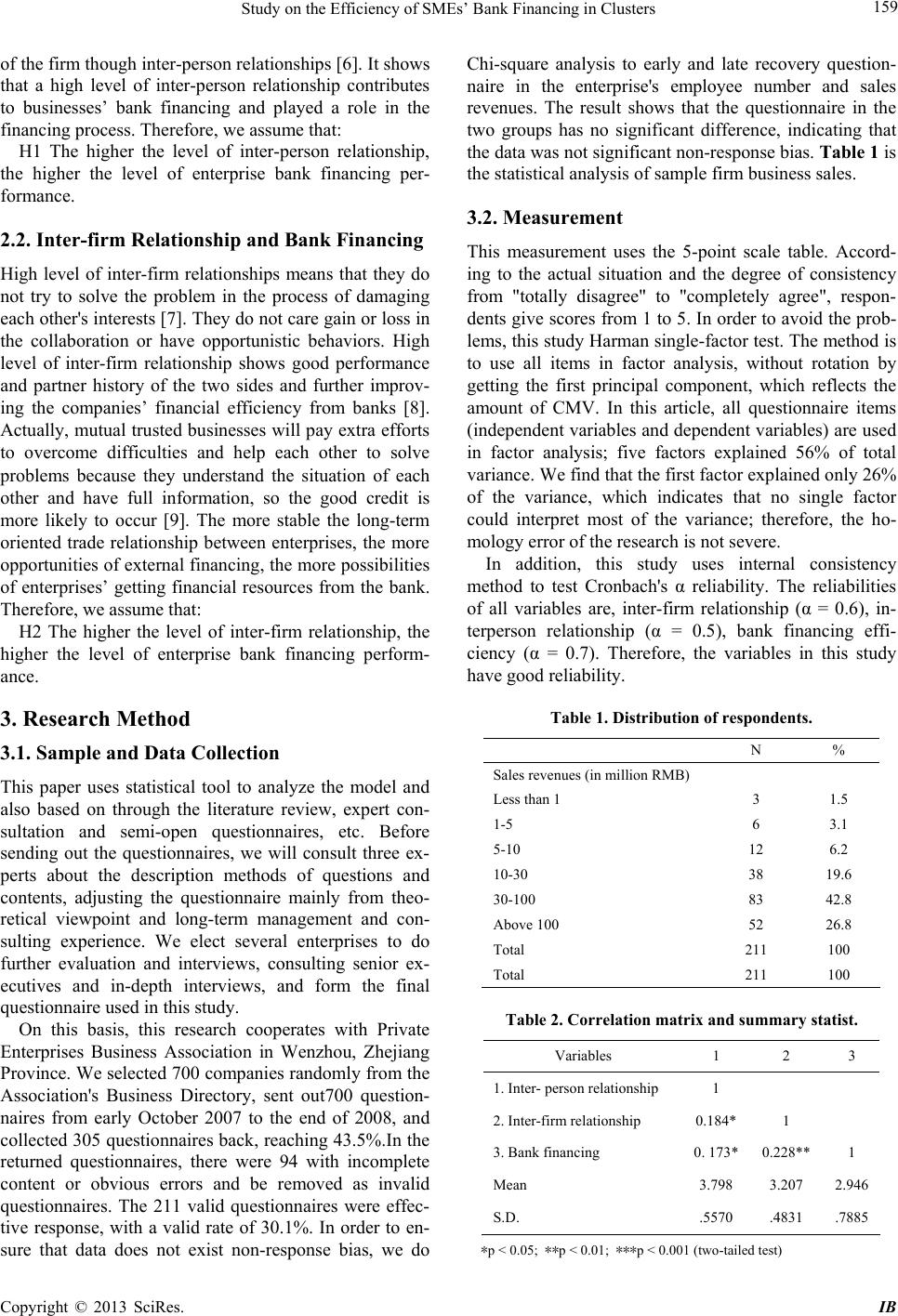

the data was not significant non-response bias. Ta b le 1 is

the statistical analysis of sample firm business sales.

3.2. Measurement

This measurement uses the 5-point scale table. Accord-

ing to the actual situation and the degree of consistency

from "totally disagree" to "completely agree", respon-

dents give scores from 1 to 5. In order to avoid the prob-

lems, this study Harman single-factor test. The method is

to use all items in factor analysis, without rotation by

getting the first principal component, which reflects the

amount of CMV. In this article, all questionnaire items

(independent variables and dependent variables) are used

in factor analysis; five factors explained 56% of total

variance. We find that the first factor explained only 26%

of the variance, which indicates that no single factor

could interpret most of the variance; therefore, the ho-

mology error of the research is not severe.

In addition, this study uses internal consistency

method to test Cronbach's α reliability. The reliabilities

of all variables are, inter-firm relationship (α = 0.6), in-

terperson relationship (α = 0.5), bank financing effi-

ciency (α = 0.7). Therefore, the variables in this study

have good reliability.

Table 1. Distribution of respondents.

N %

Sales revenues (in million RMB)

Less than 1 3 1.5

1-5 6 3.1

5-10 12 6.2

10-30 38 19.6

30-100 83 42.8

Above 100 52 26.8

Total 211 100

Total 211 100

Table 2. Correlation matrix and summary statist.

Variables 1 2 3

1. Inter- person relationship 1

2. Inter-firm relationship 0.184* 1

3. Bank financing 0. 173* 0.228**1

Mean 3.798 3.207 2.946

S.D. .5570 .4831 .7885

∗p < 0.05; ∗∗p < 0.01; ∗∗∗p < 0.001 (two-tailed test)

Copyright © 2013 SciRes. IB