The Constrained Mean-Semivariance Portfolio Optimization Problem with the Support of a

Novel Multiobjective Evolutionary Algorithm

Copyright © 2013 SciRes. JSEA

25

Figure 3. Global non-dominated solution A is assigned a

higher reproduction fitness, due to its higher Euclidian dis-

tance from the rest non-dominated solutions.

than 5 times (average reproduction) in the new popula-

tion due to the higher reproduction fitness.

3.3. The Mutation Mechanism

The number of mutants is determined by the portfolio

size and the mutation rate. For determining which stocks

will exist the portfolio is calculated the Inverse Fitness.

The Inverse Fitness is calculated as follows:

Inverse Fitness = Maximum Stock Fitness

– Stock Fitness

where: Maximum Stock Fitness: The stock with the high-

est fitness among the stocks on FTSE-100 and Stock Fit-

ness: The fitness of each individual stock that is included

in the portfolio.

That means that the highest fitness stock of FTSE-100

has an Inverse Fitness of zero. As soon as we calculate

the portfolio’s Inverse Fitness, we probabilistically select

the stocks to exit the portfolio. Obviously, the highest

fitness stock will not exit the portfolio as has an Inverse

Fitness of zero. Stocks with higher inverse fitness and

thus lower fitness are more probable to be removed from

the portfolio. This is an elitism mechanism that gives

probabilistic advantage to the higher fitness stocks to

remain into the portfolio.

Having decided which stocks will exit the portfolio,

and then we have to determine which stocks will enter

the portfolio as mutants. In this case all the stocks of the

index are taken into account, according to their fitness.

Again, cardinality constraints and lower and upper b ou nd s

are taken into account during this process. Taking stocks’

fitness into account means that stocks with higher fitness

are more probable to enter the portfolio as mutants.

3.4. The Crossover Mechanism

At this stage, the population already has been variated

through the mutation process. In order to maintain diver-

sity in the population and avoid convergence to a single

solution we make use of the crossover mechanism. The

crossover between the various solutions (portfolios) is

random, but within the maximum and minimum cross-

over rates that we have specified at an earlier stage. For

example if we specify maximum crossover rate = 90%

and minimum = 70%, that means that randomly will be

selected a crossover rate within these limits let’s say 80%.

A crossover rate 80% simply means that 80% of portfolio

A will be crossover with 20% of portfolio B and 20% of

portfolio A will be crossover with 80% of portfolio B.

Please note that the pairs to be crossover are selected

randomly.

3.5. Efficient Frontier Formulation

Next, we present the process of efficient frontier formu-

lation by quoting experimental results based on historical

data of FTSE-100. For the first experiment, as a training

set we use 63 daily historical observations of FTSE-100

from 30-Nov-2011 till 29-Feb-2012. The configuration

of the n-MOEA for this experiment is: population size 70,

maximum number of generations 200, floor constraint

5%, ceiling constraint 31%, Cardinality constraint 20

stocks, crossover rate between 70% and 90% and muta-

tion rate 20%. Below, we provide two figures with the

Efficient Frontier formulation at different stages of the

algorithm execution.

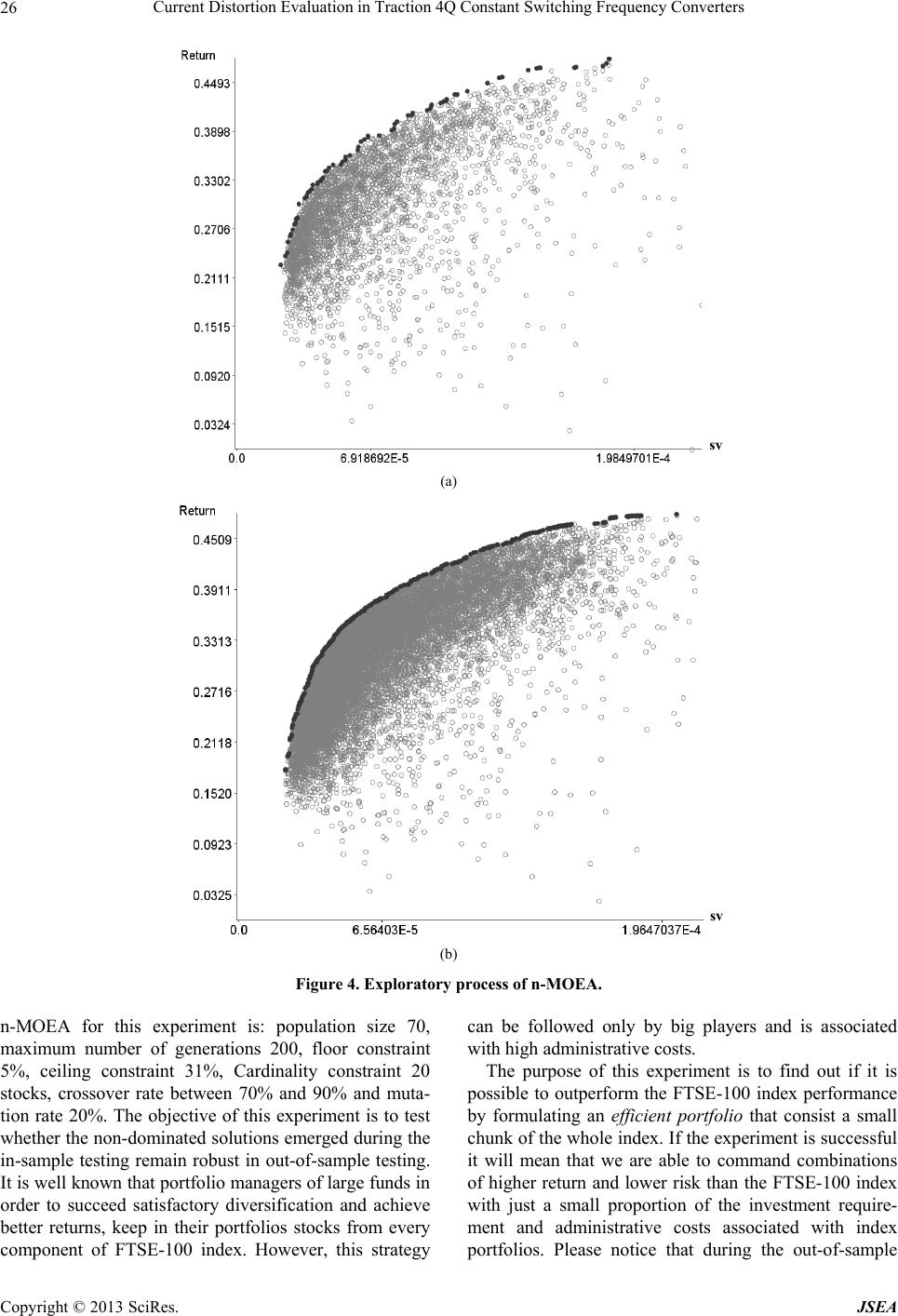

Figure 4 displays the exploratory process of n-MOEA.

It is evident even from Figure 4(a) at generation 50 that

the algorithm pusses the exploratory process towards the

left and upward corn er of the figure where the most effi-

cient solutions reside i.e. solutions that command higher

return and lower risk. At generation 200 as it is evident

from Figure 4(b) the region surrounding the efficient

frontier has been turned solid grey, meaning that given

the constraints imposed has been exhausted the possibil-

ity to move the efficient frontier further towards the left

and upward corner of the figure.

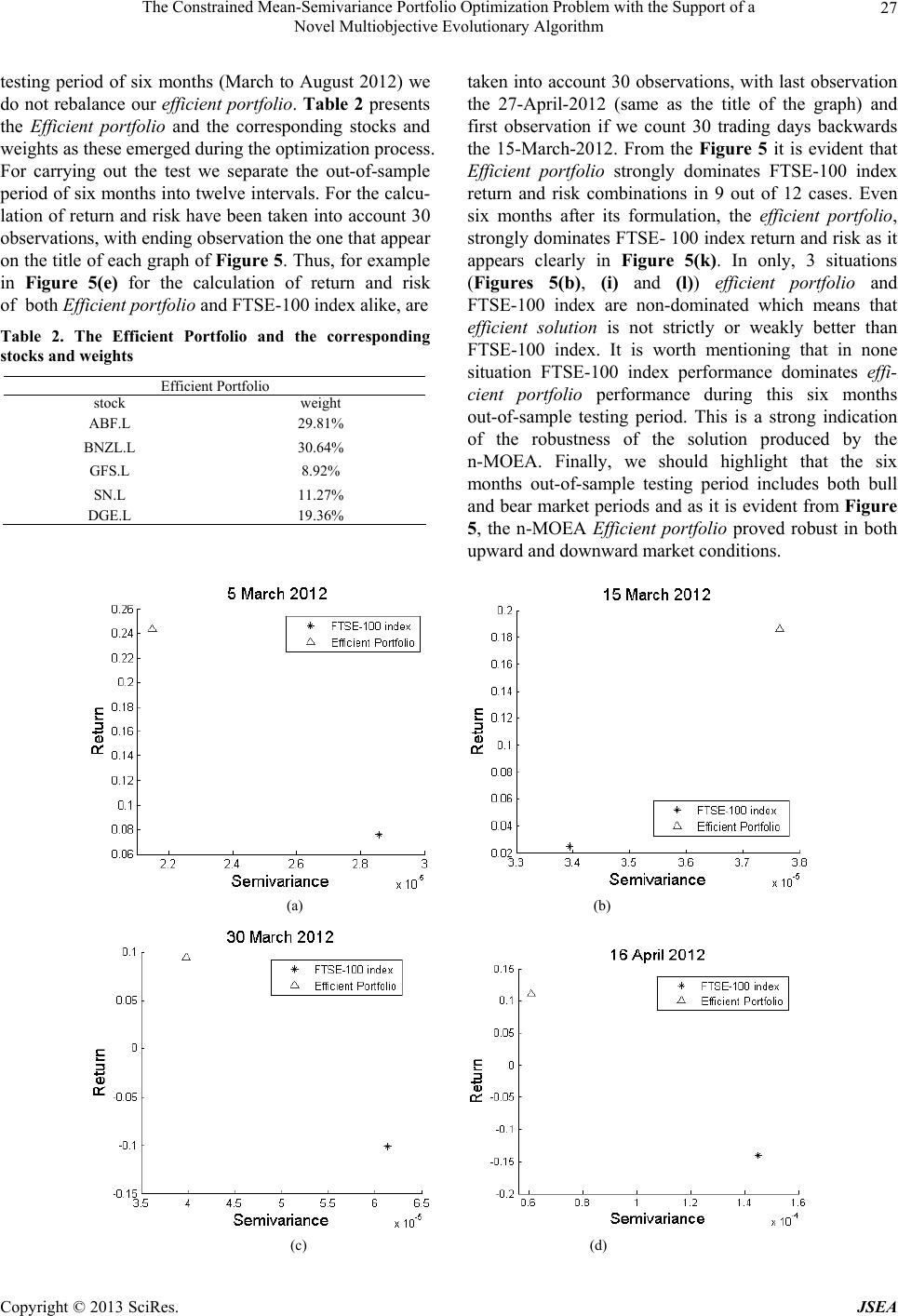

4. Robustness of n-MOEA

In relevant literature there are different views about ro-

bustness. Some scholars define robustness as the consis-

tency of results between different runs of the algorithm;

others define robustness as the insensitivity of solution to

small changes in the decision variables. We will examine

the robustness of the proposed algorithm from a practical

point of view. Specifically, we will test the robustness of

the obtained solutions in out-of-sample environments.

For this experiment we use a training set of 63 daily his-

torical observations of FTSE-100 from 30-Nov-2011 till

29-Feb-2012. The configuration of the