Communications and Network, 2013, 5, 16-19

doi:10.4236/cn.2013.53B1004 Published Online August 2013 (http://www.scirp.org/journal/cn)

A Research on the Application of XBRL in the

Independent Audit

Zhaoyang Wang

1Economy& Management School of Wuhan University

2Hunan University of Finance and Economy, Wuhan, Changsha China

Email: zhaoyangwang@126.com

Received July, 2013

ABSTRACT

XBRL (extensibility commercial language) network financial report is gradually extending in our country, which will

have a far-reaching impact on independent audit. The research on the application of XBRL’s principle, operation proc-

ess and the improvement of the audit process in the audit work is helpful for bringing some developing measures for

independent audit based on XBRL.

Keywords: XBRL; the Independent Aud it; Audit Quality

1. Introduction

In January 2011, The Treasury and the securities regula-

tory commission issued “the notice about some matters

of implementing enterprise accounting standard general

classification standards”, according to which, the first

implemented public accounting firms with qualification

of Securities and futures business and their relevant

business shall report XBRL2010 annual financial reports

instance document and expansion classification standards

made by their auditing customers of a-share listing com-

pany to the Treasury, through the certified public ac-

countants industry management system between May 1,

2011 to June 30.

China's listed company formally strides into the net-

work financial statements era, the network financial re-

port based on XBRL will have great effect on the audit of

China's capital market.

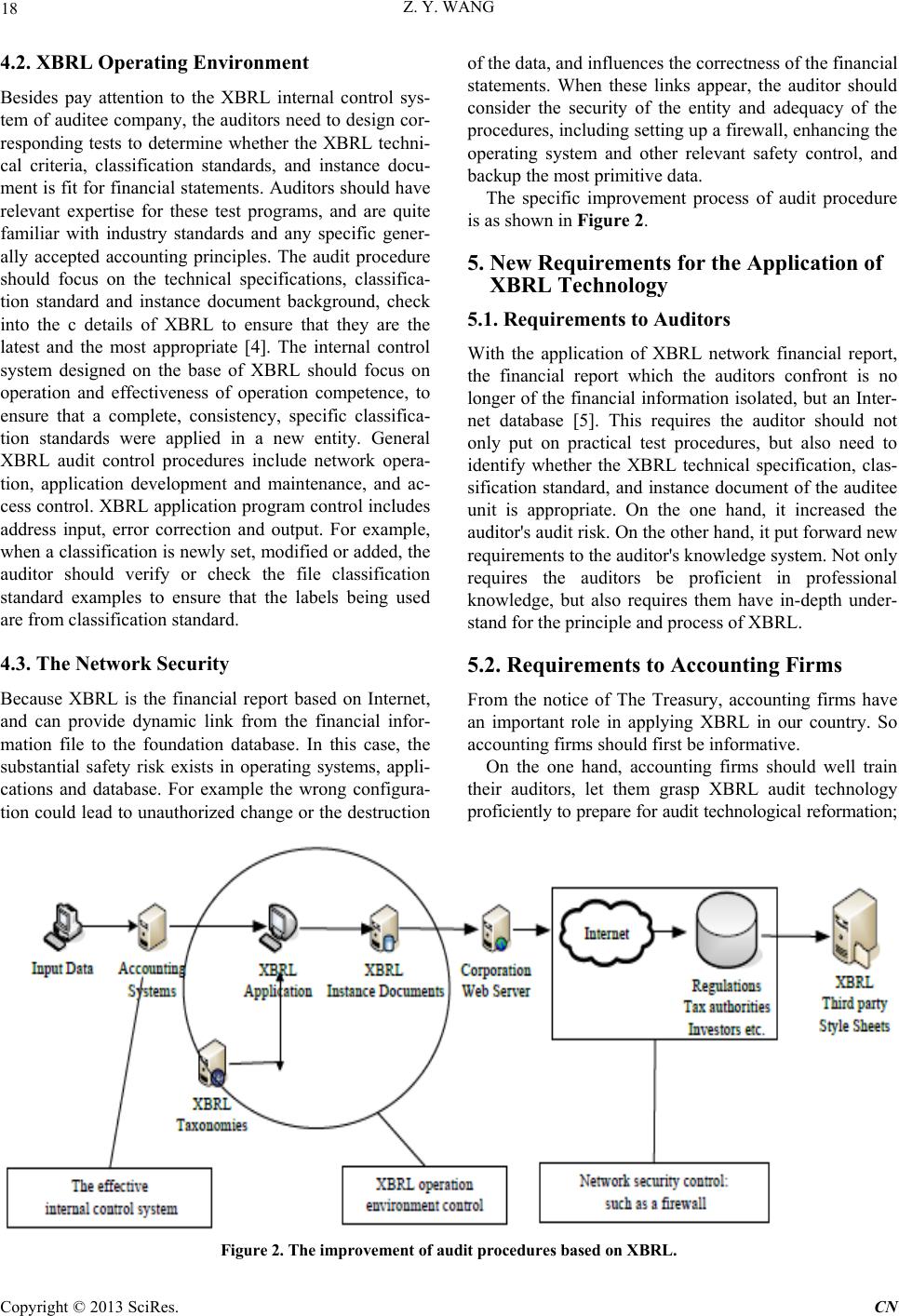

2. The Application Principle of XBRL in

Audit

To understand the application of XBRL in audit, you

should first understan d how XBRL work s. Applicatio n of

XBRL asks to understand a few major terms: specifica-

tions, taxonomies and instance documents

The XBRL specifications are the software code to de-

scribe financial information forms. Technical specifica-

tions help software developers and programmers to cre-

ate mutual exchange of digital file, it allows users of fi-

nancial information do comparison to different com-

pany’s financial statements, even if the original format of

the financial statements is completely incompatible.

Specifications are not only for financial statements, but

for dealing with all the digital report, the general ledger

and the non-financial information.

XBRL taxonomies are the describing standard to pre-

sent business information and accounting statements. It is

made up by an XML schema file and the link library

which is within the mode file or directly referred to it.

Through XBRL, financial report producers can store the

link data elements in accounting database. It forms a

standard way of using XBRL to code that based on the

classification standard [1]. For example, an annual report

including management decision and analysis, financial

statements, note disclosure, the audit opinions can use

XBRL coded.

XBRL instance documents are used to record the ac-

tual value of the business, and to provide the necessary

background information to explain the fact value. A

XBRL instance file usually consists of one or more clas-

sification standard, different classification standard links,

expanses, modifies in different ways between each other,

the explaining of XBRL instance documen t re quires con-

sideration of related classification standards [2]. For ex-

ample, one instance documents can include a company's

annual report, surplus disclosure and general ledger and

other detailed data. Instance document can make the fil-

ing work of external financial information and internal

financial information more easily, because XBRL can

output different types of data for different financial in-

formation terminal users through the computer program

and its operation. Instance document can also provide

*Humanities and social sciences youth project of the education ministry

(12 YJC790247), Hunan soft science project (2011ZK3025), and Hu-

nan social science fund project (08 YBA151)

Copyright © 2013 SciRes. CN