Modern Economy, 2013, 4, 596-599

http://dx.doi.org/10.4236/me.2013.49064 Published Online September 2013 (http://www.scirp.org/journal/me)

Emerging Asia’s Version of the Mundell-Fleming Model

Suresh Ramanathan*, Kian Teng

Economics Department, Faculty of Economics and Administration, University Malaya, Kuala Lumpur, Malaysia

Email: *skrasta70@hotmail.com, ktkwek@um.edu.my

Received July 17, 2013; revised August 7, 2013; accepted August 13, 2013

Copyright © 2013 Suresh Ramanathan, Kian Teng. This is an open access article distributed under the Creative Commons Attribu-

tion License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly

cited.

ABSTRACT

This paper explains the Mundell-Fleming model in the context of Emerging Asia economies management of capital

mobility. Central Banks and Financial Regulators in Emerging Asia adopt a modified version of the model that incor-

porates two vital levers, a policy driven and a market driven method that is adaptable to the magnitude of capital flow.

A policy combination mix of both policy and market driven provides smooth monetary policy signal transmission to

exchange rates.

Keywords: Mundell-Fleming Model; Capital Mobility; Foreign Exchange Markets; Monetary Policy; Emerging Asia

1. Introduction

Stable exchange rates, independent monetary policy and

free capital flow, the trilemma or impossible trinity, sug-

gest that only two of the above three objectives can be

accomplished simultaneously according to Fleming and

Mundell (1962 and 1963) [1,2]. In assessing the trilemma,

findings by Mankiw (2010) [3] indicate China managed

to achieve stable exchange rates and independent mone-

tary policy that was accompanied by capital controls. But

can the trilemma be considered as a guide for macroeco-

nomic policy framework? Obstfeld et al. (2005) [4] sug-

gest economies that are without a pegged exchange rate

and have barriers to capital mobility can retain sufficient

amount of monetary policy independence whereas

economies with pegged exchange rates and do not have

barriers to capital mobility would lose significant mone-

tary policy independence. In a case study by Yu Hsing

(2012) [5] on selected EA economies, findings in support

of trilemma were evident in Malaysia, Philippines and

Singapore, while there was no evidence of a trilemma

situation in Indonesia and Thailand. Different macro-

economic policy combinations prevailed in Malaysia,

Philippines and Singapore, rendering the ability to switch

to different policy combination over time in order to deal

with major economic events. In conceptualizing the

Mundell-Fleming model within the trilemma objective, it

is pertinent to take into account the risk premium element

in the form of barriers to capital mobility. In EA foreign

exchange markets, barriers to capital mobility play a sig-

nificant role in managing the overall macroeconomic

policy framework. There are two key aspects of the EA

version of the Mundell-Fleming model, the market and

policy-driven space.

2. The Model

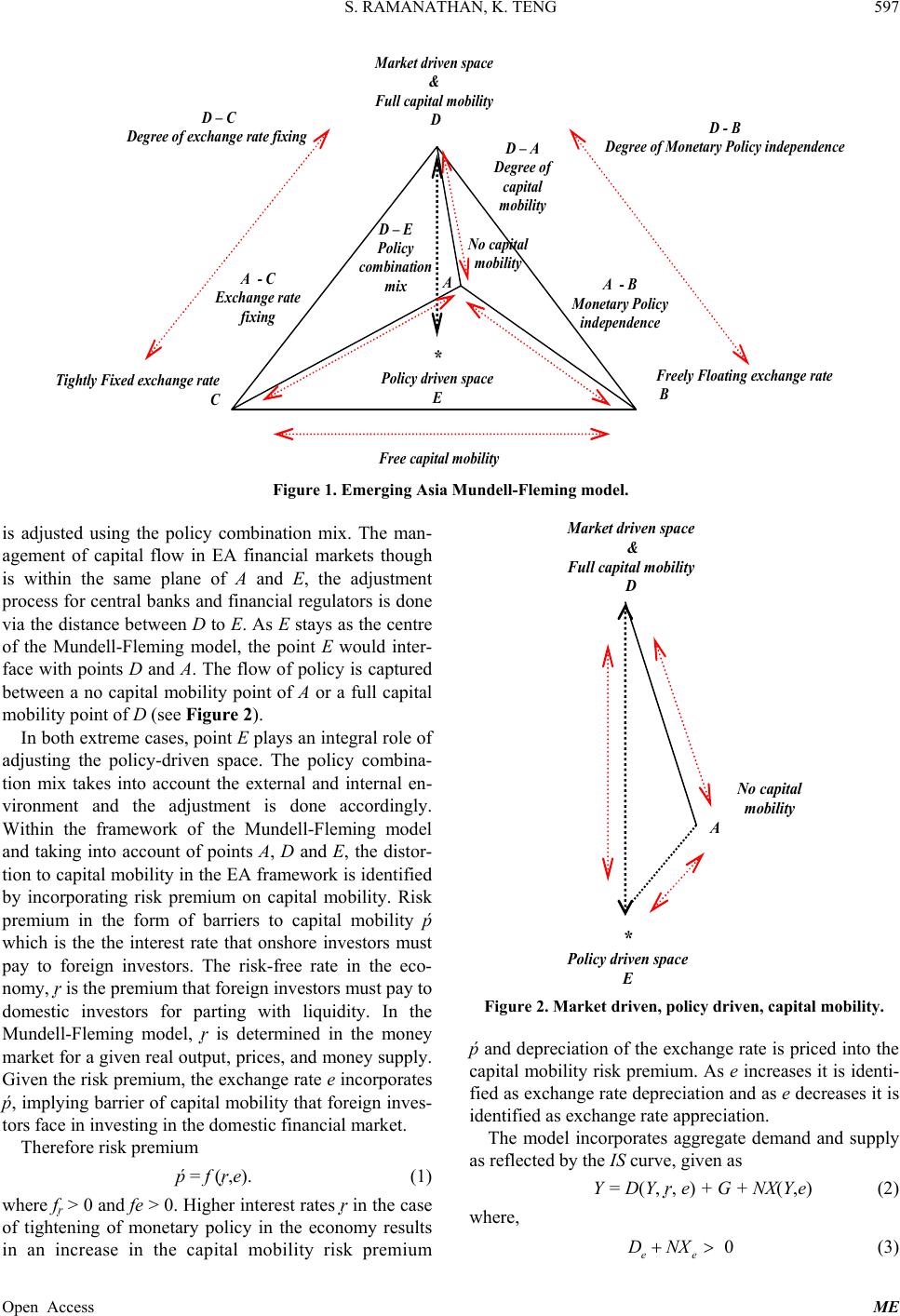

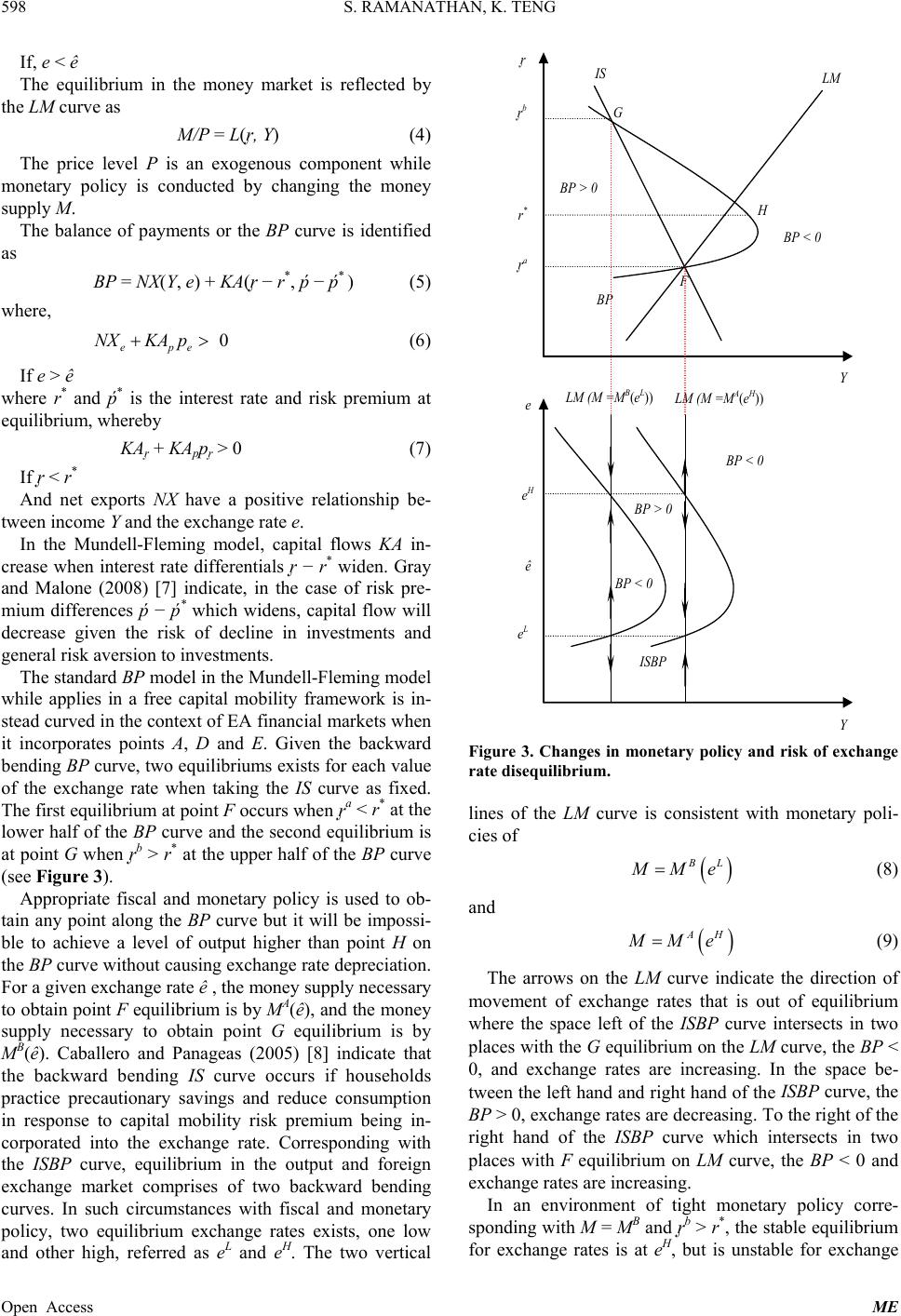

The Mundell-Fleming model for EA incorporates mar-

ket-driven, D point and policy-driven. E point (see Fig-

ure 1).

In the context of the standard model, points A, B and C

remain, indicating the choice for central banks and finan-

cial regulators being limited to adhering only two points

of preference, where the distance between A to C being

exchange rate fixing, A to B as monetary policy inde-

pendence and B to C as free capital mobility. In EA a

strict proposition of the Mundell Fleming model is a

constrain for central banks and financial regulators fol-

lowing the lessons learnt during the 1997/98 Asian Fi-

nancial Crisis. Consistent with this objective, Aizenman

et al. (2011a) [6] finds that for developing economies,

maintaining exchange rate stability was a key priority up

to the period of 1990, and since 2000, developing

economies pursued managed exchange rate flexibility

and retained partial monetary policy independence. The

task of managing capital mobility is to keep it in line

within the macroeconomic policy framework of the do-

mestic economy, therefore, the introduction of points D

and E. The midpoint of D to E is a policy combination

mix where the degree of capital mobility between A to D

*Corresponding author.

O

pen Access ME