Technology and Investment

Vol.2 No.3(2011), Article ID:6979,13 pages DOI:10.4236/ti.2011.23018

Do “Newly Oligopolistic Reaction” and Host Technology Resources Matter for MNC’s Location?

Sorbonne Centre of Economics, School of Economics, University of Paris 1 Panthéon-Sorbonne, Paris, France

E-mail: Pei.Yu@malix.univ-paris1.fr

Received June 21, 2011; revised July 15, 2011; accepted July 23, 2011

Keywords: Industrial FDI, Newly oligopolistic reaction, Host technology resources, Technology industries, China

Abstract

This paper aims at studying the determinants of inward Foreign Direct Investment (FDI) varying with sectors, by considering particularly multinational corporation (MNC)’s location strategies and local technology resources in host industries. Using data from China’s National Bureau of Statistics and National Development and Reform Commission, we empirically analyze the main determinants of industrial inward FDI, across 20 manufacturing sectors (2-digit) in China, over the period 2001-2008, and we are particularly interested in 9 high-technology (HT) and medium-high-technology (MHT) industries. The random effect panel estimations reveal that when industrial technological intensity is controlled, host technology resources are significantly positive determinants for newly inward FDI. The dynamic econometrical approach by System Generalized Method of Moment (GMM) estimations for HT and MHT industries obtain interesting results, which show evident impacts on MNC’s strategic behaviors, brought about by geographic agglomeration (or industrial concentration) effects and local protection (that we will call “new oligopolistic reactions”). Besides, FDI in HT and MHT industries are both market and export seeking. High productivity, large economies of scale, and abundant technology resources attract newly FDI in these industries. This study has two contributions: firstly, it covers the deficiency that many researches on FDI in China only focus on aggregate flow without distinguishing host sector’s characteristics; secondly, it provide the local government some useful suggestions on regional development and industrial policies, especially in technology industries.

1. Introduction

MNCs’ FDI location strategies are caused by various reasons. During the 1970s, FDI were mainly “NorthNorth” flows which concentrated in Triad regions (US, Europe and Japan) [1]. The majority of MNCs’ overseas activities in that period are explained by home country characteristics and specialties of mother firms, such as exploitation of firm’s monopolistic advantages [2] or oligopolistic advantages [3].

Since late 1980s, abundant labor resources in several developing countries have attracted FDI in labor intensive industries and “North-South” FDI flows emerge. Some researchers interpret this kind of FDI flows by using Heckscher-Ohlin model [4,5]. Host country’s cheap labor costs are their comparative advantages to attract low technology FDI. FDI in textile and toys assembly factories located in China’s coast provinces in the 1990s are typical examples.

More recently, the development and technical progress in emerging countries (e.g. BRIC: Brazil, Russia, India and China) bring about new FDI trends. FDI inflows toward these countries are upgraded from low technology industries to higher technology ones. We call this kind of FDI “New North-South” flows, which are influenced by host industries characteristics such as technology intensity and high productivity. Taking China as an example, its comparative advantages are no longer “unskilled and cheap labors”, high technology industries become new niches for MNCs. [6] indicates that China’s exports have shown a more rapidly growing sophistication of its products than other emerging countries. For instance, China’s international specialization index in high technology industry is close to Germany since 2007, ranking the third place in the world. By this way, analyses on determinants of “New North-South” FDI trends need new researches.

The majority of researches investigating FDI determinants in China focus on host country’s characteristics, including market size, political instability, openness degree, trade policy and geographical proximity [7,8]. However, FDI flows are far from homogenous [9], for instance, FDI in primary sector may be due to abundant natural resources in host country, and FDI in manufacturing sector may be caused by other endowment factors, such as unskilled labor or skilled labor pooling. Thus, the studies based on aggregate FDI inflow without distinguishing the investments by sectors are deficient. This study wants to cover this deficiency.

Traditionally, the cross-industry analyses of FDI determinants are based on hypotheses in microeconomics and industrial organization theory on production allocation and also their derivative theories [1,3,10-12].

Nowadays, with prevalence of New Economic Geography (NEG) initiated by [13-15], etc., the impacts of agglomeration on newly inward FDI have attracted researcher’s interests. [16] adapts the total number of manufacturing French affiliates and the total number of French affiliates in host sector, to evaluate French FDI agglomeration effects across European countries from 1987 to 1994. [17] uses three agglomeration variables which considered both home country agglomeration effects and host industrial specialization, by studying 3902 manufacturing FDI locations in France.

Taking China as host country, [18] employs “location quotient” of Japanese FDI in each Chinese province as an indicator of Japanese agglomeration and the number of Chinese domestic industrial enterprises in each province as non Japanese agglomeration effect when analyzing Japanese FDI in China over the years 1997-2002. [19, 20] take into account four different variables to measure home country agglomeration and foreign firms agglomeration effects, by comparing different location strategies conducted by 457 US and 537 European manufacturing affiliates in China, over the periods 1995-2007.

Moreover, as a transition from planned economy to market economy, local protectionism’s impact on FDI location in China’s manufacturing sectors is an attention-getting subject in a number of studies [21,22]. Local protectionism is essentially embodied by State-owned investments ratio in an industry. For example, in 2007, state-owned investments held at average 48.5% of total capital in China’s manufacturing sectors. In the ICT (Information Communication Technology) sectors, which are highly opened for foreign investors, FDI accounted for 60% of total capital in 2007 and State-owned capital took only 37%. However, opposite situations happen in more protected sectors such as lumbering processing and tobacco sectors. Hence, State-owned capital ratio in an industry is considered as centrifugal forces against potential newly FDI location.

In order to distinguish from traditional oligopolistic reactions initiated by [3], we introduce MNC’s “newly oligopolistic reactions” strategies, including geographic agglomeration (or industrial concentration) effects and local protectionism at industrial level.

Further, since technological advantages are increasingly worldwide fragmented, host technology resources are equally considered as important Marshallian externalities to attract newly FDI. [23] employs Total Factor Productivity (TFP) as a proxy of technical efficiency of factor usage and number of people employed in R & D in each industry for measuring labor quality, when analyzing determinants of FDI in manufacturing sectors in Czech Republic. Another group of studies prefer to use labor’s education level as a measurement of technology resources [7,24,25].

In this study, we seek to analysis the main determinants of industrial FDI, across 20 manufacturing sectors (2-digit) in China, over the period 2001-2008. Data obtained from Statistics on Science and Technology activities of industrial enterprises (SSTAIE), edited by National Bureau of Statistics (NBS) and National Development and Reform Commission (NDRC), and China Industry Economy Statistical Yearbooks edited by NBS of China. We are, in particular, interested in answering the following three questions: Firstly, which are the determinants for FDI across sample industries China? Do MNCs’ “newly oligopolistic reactions” matter? Secondly, to what extent is the industrial FDI influenced by industrial technology intensity? Thirdly, do our empirical effects provide valuable suggestions for industrial development policies in China?

To begin with, our study introduces theoretical background of determinants on industrial FDI, based on industry performance in host country; secondly, it gives the descriptions of variables and hypothesis; thirdly, econometric methods and results are presented; fourthly, it discusses the main findings and gives suggestions on regional development and industrial policies; then the final section draws conclusions and outlines perspectives for future research.

2. Theoretical Determinants of Industrial FDI: Based on Industry Performance in Host Country

[23] argues that industrial allocation can be explained primarily by the pure theory of trade, and only the industries with comparative advantages can attract FDI. By synthesizing the motives of FDI in manufacturing sectors proposed by [26-29] and also previous empirical studies on industrial FDI determinants, we discuss three groups of determinants based on host industry performance: host assets exploiting, MNC’s newly oligopolistic reaction, and traditional factors such as host industry competitiveness in export and market size.

2.1. Host Assets Exploiting

Traditional MNC’s theory predicts that a foreign affiliate needs to maintain firm specific advantages relative to its rivals, by transferring a part of its home specific advantages abroad and by exploiting specific assets in the host country. The combination of firm specific advantages, such as efficient producing process or advanced technology, with location advantages in host country, should increase inward FDI.

When studying inward industrial FDI determinants in the U.S. in the 1970s, [2] divides the host industrial assets into two groups: one is based on technology resource and cost advantages, e.g. advanced technology, skilled labor and cheap labor costs, and the other is focused on economies of scale produced by plant-level economies of scale or the existence of multi-plant operations.

In the first group of host assets, among developing countries in the 1990s in particular, low wages and low skills might be detrimental in attracting FDI into higher value added industries [30]. For instance, [31] indicates that inward FDI in late 1990s in China are concentrated in low technology industries. In a study on the determinants of FDI among the Caribbean countries, [32] find that relative lower local costs provides an environment that is conducive to low technology FDI both in the long and short run.

Taking developed countries as the host, technology resources, such as R & D intensity and skilled labor, become important. In the study on determinants of inward FDI into the US, over the periods 1987-1990, [33] find R & D expenditures in host industries work in tandem with increasing FDI. In research on FDI in Swedish manufacturing, [34] argues that host industries characterized as advanced technology, capital intensity and research intensity are positive correlated with inward FDI. [35] also proves that skill intensity in host industry attracts inward FDI in Sweden. When host country keeps ahead home country in technology, MNCs may invest in host for technology sourcing motive. [24] points out local talents can help MNCs’ to adapt their ownership advantages to local environment and strengthen these advantages. With the development of R & D capability in developing country, R & D intensity in host country has become an attractive factor of FDI in China [25] which supports the viewpoint of [36]: MNCs prefer to enter into host industry with advanced technology, in order to benefit from technological innovation environment.

The second group of assets emphasizes industrial scale or scale economies at plant level. The nature of scale economies was initiated by traditional model on information spillovers [37]. In an empirical test on determinants of HQ’s agglomeration, [38] find that scale of HQ in base period has positive effects on newly establishments of HQ over the period 1977-1997 in the US [39] discover that in European manufacturing industries, cross-sector “urbanization” economies are dominant. Based on new trade theory, [40] establish a testable theoretical framework on mode of foreign market access, which argues that only the most productive firms engage FDI when serving foreign market. Thus an industry with economies of scale and high productivity may be attractive for newly FDI.

2.2. MNC’s Newly Oligopolistic Reactions in Host Country

[3] assumed that MNCs operate in an oligopolistic market structure where competition is intense, thus, locations or industry structure, providing the firm with advantages such as lower operation costs and lower risk, could attract more FDI. In the background of oligopolistic strategies, by merging Hymer’s contribution and New economic geography theory, we introduce the new global concept of MNCs’ “newly oligopolistic reactions”, which mainly emphasize geographic agglomeration (or industrial concentration) effects and local protection effects at the industrial level in host country.

On the side of oligopolistic strategies and agglomeration (or concentration) behavior, MNCs prefer to follow their competitors or their clients when investing abroad [24]. It has been also found that, when investing in the U.S., MNCs tend to base their location decisions on the actions of previous foreign investors [35,41,42]. [35] points out that agglomeration is motivated by MNC’s strategic asset seeking, which is particularly important in oligopolistic markets with rival firms pre-empting competitors gaining any advantage. [9] finds empirical evidence of agglomeration effects when testing FDI determinants among 27 countries over the period 1985 to 2008. They explain that foreign firms appear to agglomerate is due to “herding as a larger existing FDI stock”. In an agglomeration, foreign firms can benefit from external scale economies produced involved by existing investors in the host. [7] considers spatial agglomeration effects across regions. He argues that industrial FDI stock in the neighbor regions could have a positive shock to newly inward FDI in a region.

On the other side, MNCs may avoid investing in industries with strong state ownership. The correlative researches concentrate on protectionism in China’s economy. [43] employs the ratio of value-added tax and income tax in sales revenues, the ratio of sales profits in sales revenues and the ratio of state-own capital in total capital per industry as the proxy of local protection. They detect that all these three variables have negative impacts on FDI agglomeration at the provincial level in China. [44] points out that the share of output of state-owned firms from total output per industry discourages agglomeration. Besides, [45] indicate that the share of state-own firms employment by industry disfavor agglomeration; [46] obtains similar results as previous studies and proves that local protection is a centrifugal force of agglomeration in China. [47] uses the share of state-owned output in total industrial output as a measure of local protection, and they attest that local protection disfavor agglomeration in China. [25] also finds that state investment intensity disfavor newly inward FDI in China.

2.3. Host Industry Competitiveness of Export and Market Size

MNCs’ overseas investments locations also consider host industry’s competitiveness of export and host market size.

[35]’s industry level results reveal that the host industry export intensity has positive impact on inward FDI in Sweden. [24] argues that a country has fewer restrictions on international trading activities, would be more attractive in international production. In a study of manufacturing FDI in Central and Eastern Europe, [48] find that a sector, in which trade flows in intermediate goods are important, could attract largely vertical FDI.

Host market size and potential growth are determinants for “market seeking” FDI. [9] reveals that transition economies with larger population in Central and Eastern Europe tend to attract more FDI, and real GDP growth rate favor inward FDI in secondary and tertiary sectors in 27 sample countries. [33] also finds that market size affect positively inward FDI, which is consistent with the finding of [34]. [24] figures out that market seeking FDI emphasizes the market size, the buying power in local market as well as potential growth. Thus, market factor is the single most widely used determinant of manufacturing FDI flows. [7] shows that market size has a positive effect on FDI location in China, at both provincial and industrial level. Meanwhile, [25] proves that in recent years in China’s manufacturing industries, FDI flows have double motives: host market orientation and re-export orientation.

3. Description of Variables and Hypothesis

Based on theoretical determinants of industrial FDI discussed above, we construct 8-year panel data set over the periods from 2001 to 2008 for total 20 manufacturing industries (2-digit) in China, in order to investigate the main determinants of newly inward FDI at industrial level, especially for FDI in high technology and medium and high technology sectors. The statistics come from Statistics on Science and Technology activities of industrial enterprises (SSTAIE), edited by National Bureau of Statistics (NBS) and National Development and Reform Commission (NDRC), and China Industry Economy Statistical Yearbook edited by NBS of China. The samples are composed by big and medium industrial enterprises (BMIE) per manufacturing industry. BMIE indicates the enterprise having more than 300 employees, with annual sales revenue larger than 30 million Yuan and total capital surpassing 40 million Yuan.

3.1. Dependent Variables

Following [23], our dependent variable ( ) is FDI intensity in a given industry i in year t in China, measured by inward FDI per value added (

) is FDI intensity in a given industry i in year t in China, measured by inward FDI per value added ( = yearly inward FDI industry i in year t/industrial value added in industry i in year), which avoids the problem of industry size.

= yearly inward FDI industry i in year t/industrial value added in industry i in year), which avoids the problem of industry size.

3.2. Independent Variables

3.2.1. Host Specific Assets

[2] employs average value-added per plant in each industry to measure plant-level scale economies, when analyzing MNCs’ FDI determinants in the US. In our study, we consider both productivity and technology resources in industry i in year t to measure specific assets in an industry of China.

Productivity: total firms’ yearly output divided by total employment in industry i in year t (Unit: Yuan/Person. Year)

Scale: industrial total employment divided by the total number of firms in industry i in year t (Unit: Person)

Hypothesis 1: Higher productivity and larger scale of economies can reduce firms’ production costs and attract more inward FDI. Positive signs are expected.

[8,49-52] found a positive relationship between various measures of skilled labor and FDI inflow. Karpaty and Poldahl (2006) prove that FDI arises in industries where technical knowledge is important. In this study, we bring into following three variables to measure technology resources in our estimations, e.g. technology and skills intensity:

R & D intensity (R & D): share of R & D expenditure in total sales revenue of BMIE of industry i in year t;

S & T intensity (S & T): share of Science and Technology expenditures in total sales revenue of BMIE of industry i in year t;

Skills: fraction of engineers and technicians in total employment of BMIE of industry i in year t;

Hypothesis 2: Higher labor quality increases firm’s productivity and becomes China’s new comparative advantages to attract newly FDI. Positive signs are hoped.

3.2.2. MNC’s Newly Oligopolistic Reactions

MNCs’ FDI strategic locations are decided by industrial structure and tradeoff between strategies of FDI firms and those of state-owned firms. Newly oligopolistic reactions comprise impacts on FDI by agglomeration, foreign firm concentration and state firm concentration at industry level in China. In this study, agglomeration indicates geographic concentration of producing activities in an industry and concentration means FDI activities in an industry without considering geographic scope.

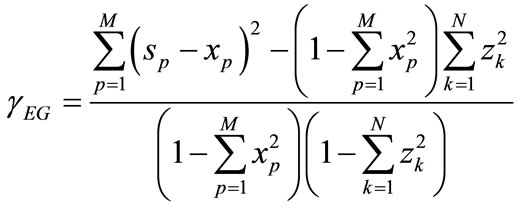

Agglomeration (EG): Ellison-Glaser index of industry  in year t.

in year t.

Based on [53], we denote  as the EG index for a sample 2-digit industry:

as the EG index for a sample 2-digit industry:

(1)

(1)

In Equation (1),  is the portion of industry employment located in province p and

is the portion of industry employment located in province p and  is the portion of aggregate manufacturing employment located in province p. There are M provinces in this study (M = 31). In origin model,

is the portion of aggregate manufacturing employment located in province p. There are M provinces in this study (M = 31). In origin model,  represents the share of employment in firm k in a sample industry. However, China’s State Statistical Bureau doesn’t offer in public the statistics at firm level. Thus, we have to adjust the form of

represents the share of employment in firm k in a sample industry. However, China’s State Statistical Bureau doesn’t offer in public the statistics at firm level. Thus, we have to adjust the form of . We suppose that industry i in province p has equal firm size. For instance, there are

. We suppose that industry i in province p has equal firm size. For instance, there are  firms in province p, and firm’s average size of industry i in province p can be written as:

firms in province p, and firm’s average size of industry i in province p can be written as:

(2)

(2)

then for each industry we have:

(3)

(3)

Combining (1), (2) and (3), we obtain  for each sample industry over the period 2001-2008.

for each sample industry over the period 2001-2008.

FDI stock (Fstock): lagged FDI stock in industry  in year

in year ;

;

FDI firm (Ffirm): lagged FDI firms’ number in industry  in year

in year ;

;

State owned firms (State): the share of state-owned firms’ output in total output of industry i in year t.

Hypothesis 3: Industrial foreign firm concentration promotes newly inward FDI in the same industry. However, MNCs avoid locating in industries with high state owned ratio, a proxy of local protection. The impact of agglomeration index measured by EG is ambiguous.

3.2.3. Host Industry Competitiveness of Export and Market size

[35] emphasizes a high degree of export competitiveness in a host country promote inward FDI. [24] accents the impacts of openness degree on inward FDI in a country. We use export intensity to capture “export seeking” of MNCs in China:

Export: share of export in total output of industry i in year t.

Hypothesis 4: High productivity and abundant skilled labors in China’s HT and MHT industries increase their industry competitiveness of export, which in turn attract newly export-seeking FDI in technology sectors. Positive sign is expected.

Based on previous studies [47,54,55], [24] concludes that market seeking FDI emphasize the size of the market, the buying power of the host market as well as its growth potential. [56] states that market factors is the single most widely used determinant of manufacturing FDI flows. For measuring “market-seeking” FDI at industrial level, we employ:

Market: share of domestic consumption in total output of industry i in year t.

Hypothesis 5: China’s huge consumption market promotes “market seeking” FDI. In order to save transportation costs and satisfy demands of local customers, a group of MNCs have established production plants in China. Positive sigh is expected.

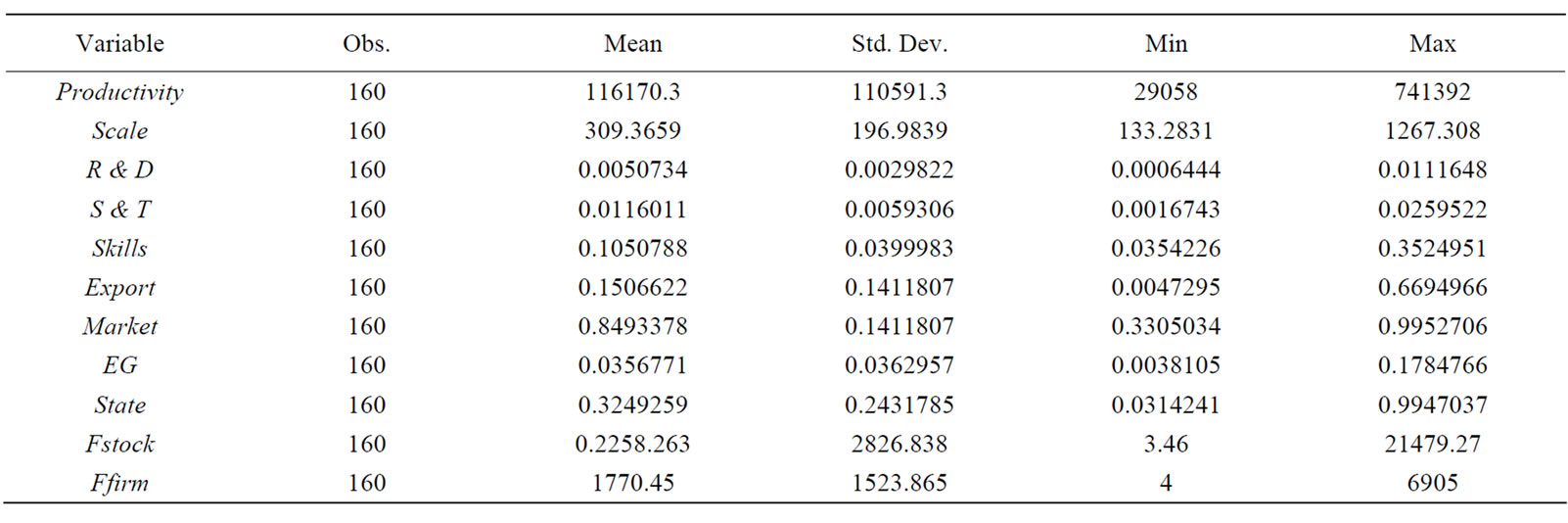

Table 1 reports statistical descriptions of independent variables. We find industry structure varies among 20 sample industries. For instance, the maximum value of state owned ratio (state) is 30 times of its minimum value. FDI stock and FDI firms also fluctuate among different industries. It’s very significative to investigate FDI determinants across different industries in China.

4. Econometric Specifications and Results

[23] points out that self-reinforcing effects of FDI and industrial characteristics can be addressed only if there is panel data of FDI. We construct 8-year panel data set over the periods from 2001 to 2008 for total 20 manufacturing industries.

4.1. Panel Model: Total Sample with Industrial Technology Intensity Dummies

The capability of attracting FDI varies with industrial characteristics. [25] points out that industrial FDI determinants in China significantly vary with industrial characteristics, for instance, high technology industries have different determinants of inward FDI from those in low technology industries. Our basic specification adopts traditional panel data approach:

(4)

(4)

is dependent variable defined in Section 3.

is dependent variable defined in Section 3.  represents a series of the independent variables,

represents a series of the independent variables,  is the constant;

is the constant;  means time effect;

means time effect;  measures the individual effects, e.g. four industrial technology intensity (ITI) dummies, which respect to [59]’s criteria on industrial technology intensity, and

measures the individual effects, e.g. four industrial technology intensity (ITI) dummies, which respect to [59]’s criteria on industrial technology intensity, and  is the error term.

is the error term.

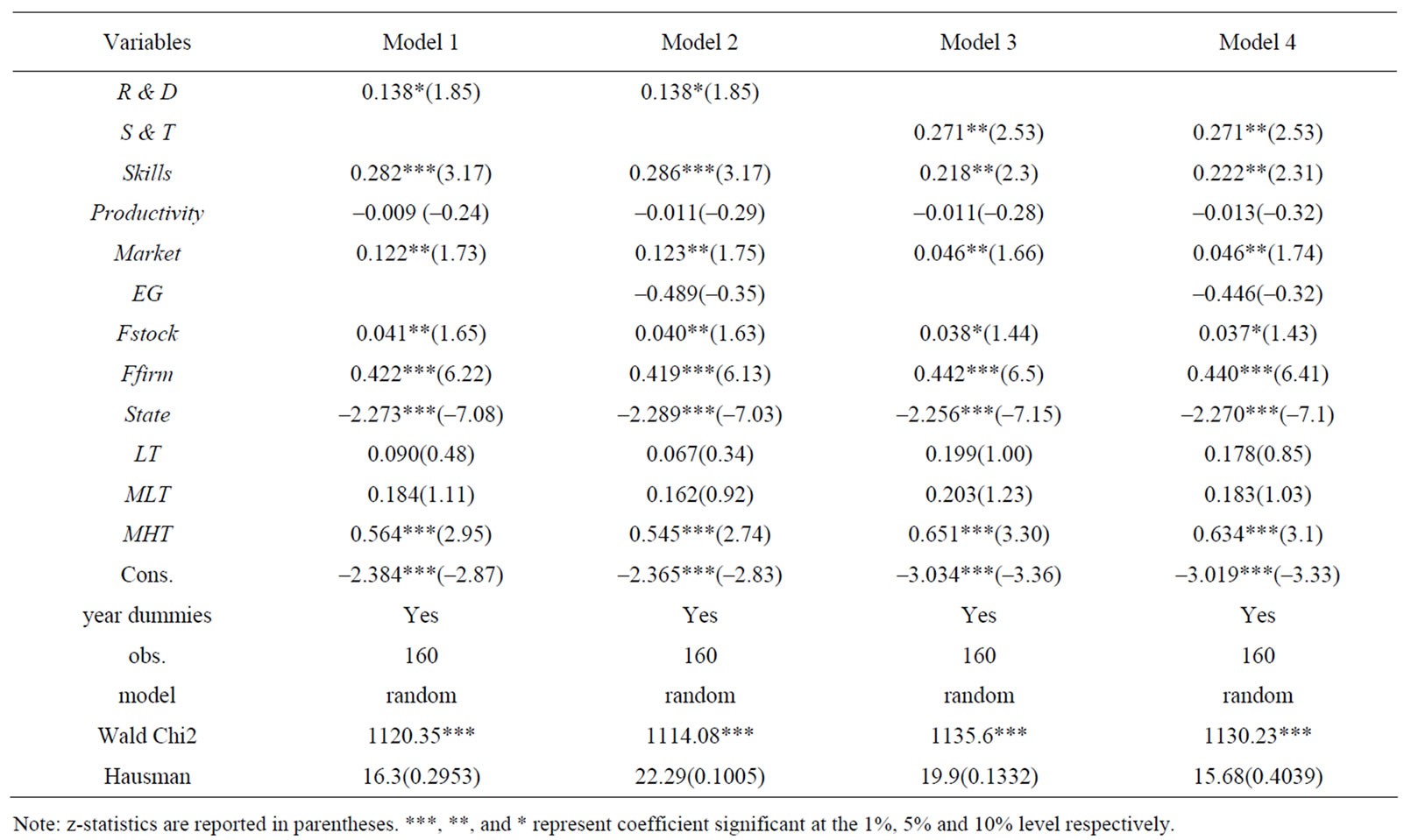

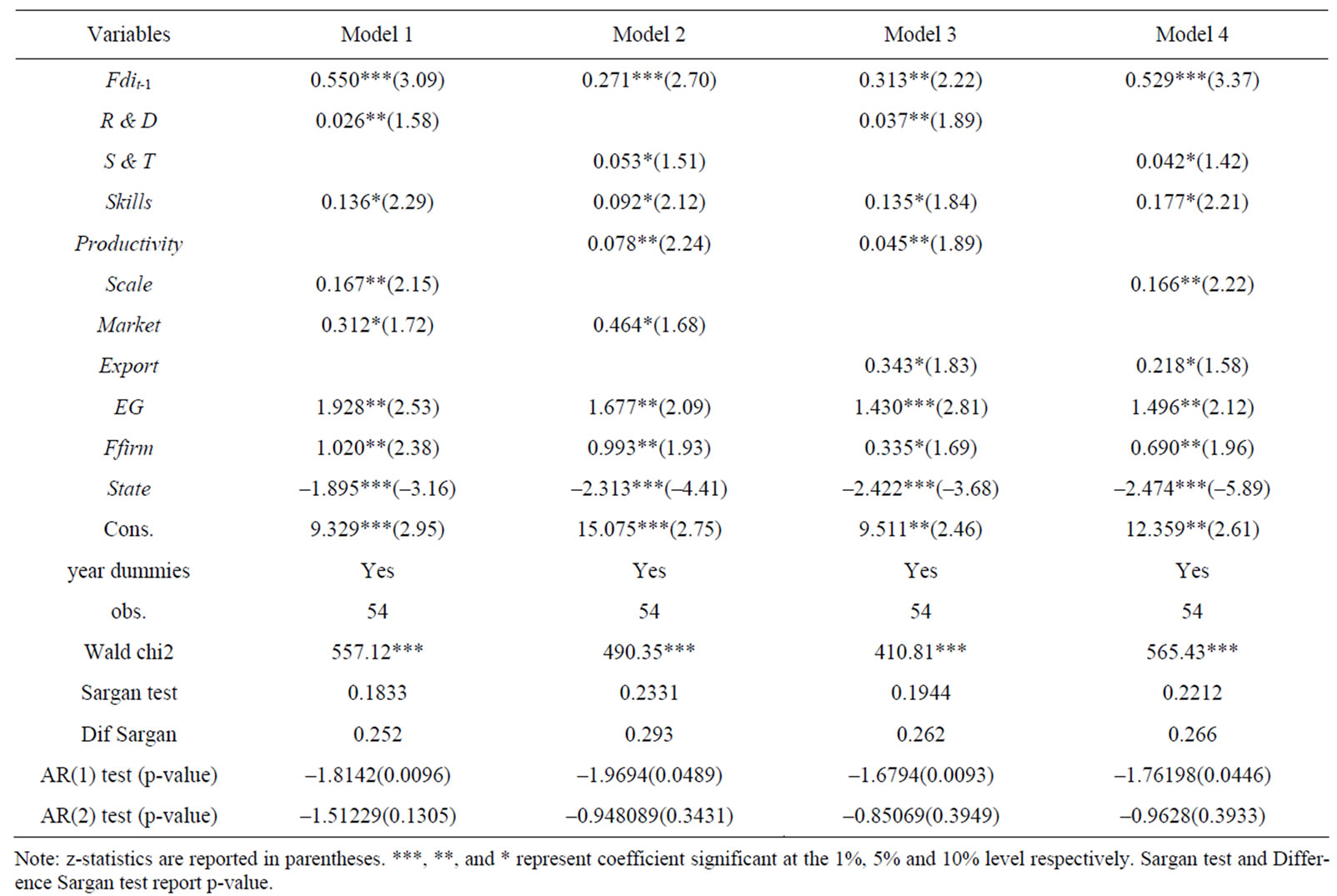

The four dummies considered are: high technology (HT), high and medium technology (HMT), medium and low technology (MLT) and low technology (LT) (refer to p.172 Annex 4 A1 in [59]). Since industrial technology intensity is consistent over the period tested, we use a random effect model to assess industrial FDI determinants. Table 2 presents estimation results. High-tech industry (HT) is reference group.

Table 1. Summary of statistical descriptions of independent variables.

Table 2. Random effect Estimations on industrial FDI determinants in China. (Total sample with industrial technology intensity (ITI) dummies).

In panel model, Hausman test compares fixed versus random effects under the null hypothesis that the individual effects are uncorrelated with the other regressors in the model [58]. If uncorrelated ( is accepted), random effect estimators and fixed effect estimators are both unbiased, and a random effect model is more efficient. In Table 2, at first, the results of Hausman Test show that we can’t reject

is accepted), random effect estimators and fixed effect estimators are both unbiased, and a random effect model is more efficient. In Table 2, at first, the results of Hausman Test show that we can’t reject  and random effect model is valid. Secondly, comparing with high-tech industry, medium and high industries such as motor vehicles, electrical machinery are more attractive for newly FDI, and low and medium low technology industries have disadvantages. This finding proves industrial characteristics’ impacts on FDI and FDI in China concentrate in high-tech or medium-tech industries. Thirdly, localized technology resources, measured by R & D intensity, S & T intensity and skilled labor ratio, have positive and statistically significant (at least 10% significant level) on newly FDI at industrial level, which are consistent with [23,35]. Fourthly, foreign firms’ concentration effects and local protection have distinct influences on industrial FDI. At last, the huge domestic consumption attracts newly FDI.

and random effect model is valid. Secondly, comparing with high-tech industry, medium and high industries such as motor vehicles, electrical machinery are more attractive for newly FDI, and low and medium low technology industries have disadvantages. This finding proves industrial characteristics’ impacts on FDI and FDI in China concentrate in high-tech or medium-tech industries. Thirdly, localized technology resources, measured by R & D intensity, S & T intensity and skilled labor ratio, have positive and statistically significant (at least 10% significant level) on newly FDI at industrial level, which are consistent with [23,35]. Fourthly, foreign firms’ concentration effects and local protection have distinct influences on industrial FDI. At last, the huge domestic consumption attracts newly FDI.

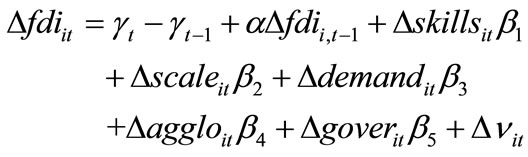

4.2. Dynamic Panel Model: High-Tech and Medium-High-Tech Industries Sample

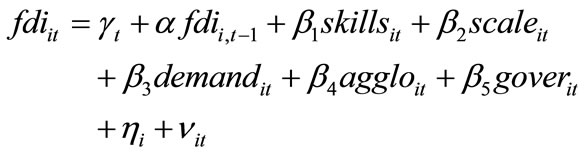

Our estimation results of total sample reveals that determinants of industrial FDI vary with industrial technological intensity and high and medium technology industries have more advantages for attracting FDI. We do further investigation on industrial FDI determinants in high-tech (HT) and Medium-High-tech (MHT) industries. Our sub sample comprises 8-year panel data set over the periods from 2001 to 2008 for 9 HT and MHT1 industries.

Since FDI is a special capital flow and has a positive self-reinforcing effect [7], for capturing this dynamic process, we use system Generalized Method of Moments (GMM) method, which takes into account the volume of FDI in one year before ( ) as one of the determinants. The impact of FDI in previous year on newly investments represents strategic intent of MNCs, and it’s also an agglomeration effect [24]. Other independent variables include technology and skills (

) as one of the determinants. The impact of FDI in previous year on newly investments represents strategic intent of MNCs, and it’s also an agglomeration effect [24]. Other independent variables include technology and skills ( ), scale of economies (

), scale of economies ( ), demand (

), demand ( ), and newly oligopolistic reactions including agglomeration and industrial concentration (

), and newly oligopolistic reactions including agglomeration and industrial concentration ( ) and also government intervention (

) and also government intervention ( ).

).

The level equation is written as:

(5)

(5)

where i and t represent respectively different high-tech and high-medium-tech industries and years.  means time effect,

means time effect,  is the individual effect and

is the individual effect and  is the random effect or other invisible independent variables.

is the random effect or other invisible independent variables.

In order to eliminate individual effect , we bring into the first-differenced form of (5) and obtain (6):

, we bring into the first-differenced form of (5) and obtain (6):

(6)

(6)

The GMM approach popularly discussed mainly based on the first-differenced equation. However, using firstdifferenced GMM estimator will suffer from serious efficiency loss, for example, some time-invariant variables, such as policy reference and trade costs in [7,46]. Following [7,46,59,60], the more efficient system GMM estimator is obtained by adding the valid level moment conditions into the first-differenced moment conditions. Thus, in our study, for first-differenced equation in system GMM regressions, we use instrument sets: ( ) and (

) and ( ,

, ), where x represent skills, scale, demand, agglo and gover. And for level equation, we bring into instrument set

), where x represent skills, scale, demand, agglo and gover. And for level equation, we bring into instrument set . Moreover, we also employ year dummies to measure common macro shocks that uniformly affect the industrial FDI. Being consistent with previous classic panel models, in system GMM regression, skills comprise R & D, S & T and skills variables,

. Moreover, we also employ year dummies to measure common macro shocks that uniformly affect the industrial FDI. Being consistent with previous classic panel models, in system GMM regression, skills comprise R & D, S & T and skills variables,  includes productivity and scale, agglo involves EG and Ffirm, demand consists Market and export, and

includes productivity and scale, agglo involves EG and Ffirm, demand consists Market and export, and  indicates State. Results are presented in Table 3.

indicates State. Results are presented in Table 3.

Three tests in Table 3 confirm the validity of system GMM regressions. Sargan test of over identification does not reject the validity of the instrumental variables (pvalue is large enough). Difference Sargan test proves that our additional instrument for level equation is valid. Further, the autocorrelation test indicates that there is no second-order serial correlation.

Concerning the coefficients of variables, we find that:

Firstly, foreign firms concentration effect measured by FDI in one year before has significantly promoted newly industrial FDI in HT and MHT industries, and its magnitude is larger than FDI stock lagged one year in general panel model estimations. The 1% increase in FDI in one year before contributes to 0.31% - 0.55% increases in newly inward FDI. Besides, the magnitude of coefficient of foreign firms is increased and the significance of this variable keeps at 5% level. Our finding approves positive impacts of previous foreign firms’ investments on newly industrial FDI. Moreover, positive and significant coefficients of EG show a simulative interaction between industrial agglomeration and newly FDI in HT and MHT industries. Thus, agglomeration and concentration effects are testified as centripetal forces of FDI in technology industries.

Meanwhile, the coefficient of state ownership reveals that newly FDI in HT and MHT industries avoid industries which have high ratio of state ownership. The 1% increase in state ownership ratio leads to more than 1.89% decrease of newly inward FDI in an industry. Our finding proves that local protection acts as centrifugal forces of FDI in technology industries.

Secondly, both Market and Export are positively significant. We deduce that FDI in HT and MHT industries adapt both market seeking and export seeking strategies. Our findings echo with [25]. On the one hand, the huge domestic consumption market in China attracts foreign firms to establish local plants, aiming at satisfying local demands; on the other hand, abundant skilled labor with lower costs compared with developed countries and higher productivity with other developing countries bring about China comparative advantages in HT and MHT manufacturing industries. Some MNCs are attracted by this industry competitiveness of export in China. For instance, in electronic-communication industry, 89.6% of the total export of processing goods was taken by foreign invested firms in 2005 (cf. National Bureau of Statistics of China).

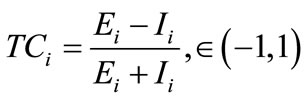

Following [61], we employ Trade competition index ( ) to evaluate international competitiveness of an industry i:

) to evaluate international competitiveness of an industry i:

(7)

(7)

In which  represents export volume in industry i and

represents export volume in industry i and  indicates import volume.

indicates import volume.  ranges from –1 to 1. When

ranges from –1 to 1. When  is positive and approaches to 1, it means industry i has strong international competitiveness of export.

is positive and approaches to 1, it means industry i has strong international competitiveness of export.

Using data from “China Statistics Yearbook on High technology industry”, we find that  in Electronic Communication industry has been changed from 0.105 in the year of 1995 to 0.592 in 2006. [6] also indicates that processing trade accounts for 90% of total export from China in technology industries. The rapid upgrading of China’s sophistication of exports in high-tech industries

in Electronic Communication industry has been changed from 0.105 in the year of 1995 to 0.592 in 2006. [6] also indicates that processing trade accounts for 90% of total export from China in technology industries. The rapid upgrading of China’s sophistication of exports in high-tech industries

Table 3. System GMM estimations on industrial FDI determinants in China (HT and MHT sample).

seems to be driven essentially by foreign invested firms. China’s industry competitiveness of export in these in dustries brings MNCs location advantages.

Thirdly, being different from results of total sample estimations, higher productivity, scale economies and more important agglomeration effect in an MHT and HT industry (measured by EG index) can attract more newly industrial FDI. Marshallian externalities are more evident in technology industries.

Fourthly, R & D (or S & T) intensity and skilled labors are favorable conditions for attracting inward FDI.

These findings are consistent with total sample models.

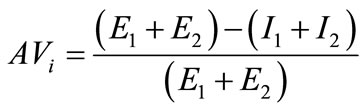

In practice, researchers usually use Added value ratio of trade processing ( ) and share of new products export in total export in industry i (

) and share of new products export in total export in industry i ( ) to measure the position of export goods in global value chain.

) to measure the position of export goods in global value chain.

(8)

(8)

where E1 and E2 represent separately export volume of processing of imported materials and that of processing of supplied materials, and I1 and I2 are each import volume.

(9)

(9)

We take electronic-communication industry as an example. Table 4 shows that added value ratio in this industry is higher than average level of manufacturing industries in China. We deduce that the position in global value chain of this sector in China has been gradually upgraded (although still having a distance from R & D centers), which call for more knowledge inputs. Moreover, Newi in electronic-communication industry has been raised from 5.9% in 1995 to 12.2% in the year of 2006, which also reveals the increasing of industrial technology intensity in China. The positive and significant coefficients of R & D (S & T) intensity and skills prove this fact.

5. Discussions and Implications

By using random effects and dynamic panel models, we investigate main determinants of China’s newly industrial FDI, especially in HT and MHT industries. Based on estimation results, we give following suggestions on industry development in China.

Agglomeration and foreign firms’ concentration effects: these effects, measured by EG index, one year lagged FDI stock, lagged number of FDI firms, and lagged FDI, positively affect newly FDI at industrial level. Thus, how to attract high quality FDI rationally is important for industry development in China. We detect that MNCs in China use “following the competitors” strategies. The demonstration effect of first mover foreign investors is essential. For instance, the establishment of third manufacturing plant in Hubei province in 2010 has attracted locations of affiliates of Saint Gobain; locations of R & D centers of GE and Dupont have encouraged 1881 foreign invested firms to locate in Shanghai Zhangjiang Hi-Tech Park at the end of 2006, etc.

State-owned ratio: our finding reveals that newly FDI avoid high state-owned ratio industries. Foreign firms and state-own firms reluctantly co-operate in the game. On the one hand, FDI firms prefer unrestricted business environment, on the other hand, due to intellectual property protection and globalization strategies, MNCs reluctantly transfer core technology to local partners, and assembly line work is usually located in China because of its relative lower labor costs and higher productivity. Thus, high FDI control ratio tends to constraint local firm’s autonomous development and innovation capability, and high state-owned ratio prevents newly inward FDI. Central government needs to adjust the power between FDI firms and domestic firms. The success of Zhangjiang High-tech Park is an example of cooperation in R & D between MNCs and local firms. At the end of 2006, there are 4862 firms registered in the park, among which 1881 are foreign invested2. The stanchion industries in the park are biopharmaceutical and electroniccommunication, and in 2006, 10 world leaders in these two industries established R & D centers (Novartis, Dow Chemical, Advanced Micro Devices, etc.) in Zhangjiang. Statistics have shown that foreign invested firms’ total sales revenue in 2006 has arrived at 39.05 billion RMB (with 45.8% increase than 2005), of which 17.93 billion

Table 4. Added value ratio of trade processing in China’s electronic-communication industry.

RMB is gained in foreign markets. Besides, local human capital is a key input of production. Among 92,542 total labors in 2006, 46,303 (more than 50%) are at least bachelor degrees holders, and in electronic communication industry, this ratio was 73.29% in the same period.

Host technology resources variables: these variables have become important determinants of inward FDI in technology industries. Abundant unskilled labor in low technology industries are no more China’s comparative advantages in global competition. High productivity, industrial R & D intensity and skilled labors at industrial level have become its new comparative advantages in China’s manufacturing industries. The central government needs to consolidate and improve these advantages by supporting firm-university cooperation and attracting returnees’ entrepreneurship. Strong host technology resources could support update of industrial sophistications. For instance, [62] shows that returnees entrepreneurs in Beijing Zhongguancun Science Park create a significantly positive spillovers on innovation activities in local high-tech firms, and local firm’s absorptive capacity is essential for benefiting spillovers through cooperation with foreign firms.

Besides, [63] finds that when host country offers a large market but with high wages, unproductive firms are unlikely to choose FDI and high productive firms will choose FDI and then re-import by home, depending on fixed costs of establishing a plant in host. In reality, with increasing of skilled labors in China, which in turn augment labor costs, only productive firms, namely high quality FDI from biggest MNCs, can produce positive firm operation profits, thus, local government needs to control FDI quality, aiming at engendering economic profits through cooperation with local firms.

Export ratio: we find that higher export ratio attracts more FDI and MNCs use “exporting” strategy in HT and MHT industries. [61] calculate industrial Trade competition index ( ) of electronic communication industry by eliminating the competitiveness created by FDI firms. They detect that domestic firms in this industry have very poor performance in international competiveness (

) of electronic communication industry by eliminating the competitiveness created by FDI firms. They detect that domestic firms in this industry have very poor performance in international competiveness ( varies from –0.352 to 0.205 over recent 11 years). However, when foreign firms’ contribution is added,

varies from –0.352 to 0.205 over recent 11 years). However, when foreign firms’ contribution is added,  arrived at 0.592 in 20063. We deduce that HT and MHT industries, such as electronic communication, have high FDI dependence, and the autonomous development capability in these industries are not sufficient. As a result, China’s welfare from export is not increased.

arrived at 0.592 in 20063. We deduce that HT and MHT industries, such as electronic communication, have high FDI dependence, and the autonomous development capability in these industries are not sufficient. As a result, China’s welfare from export is not increased.

We take processing of iPad as example [6]. The average production cost of an ipad is 260 US $ (market price is 499 US $). In production value chain, the most expensive accessory of Ipad is the display outsourced from LG Inc. and Samsung Inc, and the weakest profit procedure is assembly line work, which is charged by several Taiwanese MNCs’ production affiliates in mainland of China (e.g. Foxconn). In iPad’s global value chain, Apple Inc. holds the highest profit due to original R & D and core technology, the two Korean firms also get generous profits because of key accessory, Taiwanese firms gain assembly fee, and however, their affiliates in mainland of China only have tiny profit. Neither R&D nor key parts production is taken by Chinese firms. Although statistics from U.S. Custom declare that export of iPad from China to the U.S. created 1900 millions U.S.$ surplus in the year of 2009, in reality, if we take into account import costs of high value intermediate products, the real trade volume was 481 millions US $ deficit for China. MNCs’ re-export strategies in HT and MHT don’t bring China real profits.

[6] points out that international specialization of China in a number of high technology industries is strongly dependent on imports from developed countries and China’s market share of high quality (measured by unit value of export) in technology industries still lags behind developed countries. The independent innovation capability in HT and MHT industries needs to be improved unceasingly in China.

China’s huge domestic consumption market: it is an attractive factor for FDI in all sample industries. In the meanwhile, higher productivity and scale of economies in HT and MHT industries favor locations of newly FDI. The central government should establish a series of policies aiming at stimulating domestic consumption and improve consumption quality and level. In order to satisfy with increasing domestic demand, local firms can establish cooperation with foreign firms in R & D and producing of new products. Through such kind of cooperation, local firms can learn advanced technology and management experience. In long term, local firms’ international competitiveness will be improved. A group of empirical studies have proved positive spillover effects from foreign invested firms to China’s local firms in R & D works [47]. In practice, with efforts of foreign experts and local human capital, Zhangjiang High-tech Park has applied 17620 patents until the end of 2009. In Bio-Tech and Pharmaceutical industry, in 2006, the cooperation of 141 local firms and 99 foreign invested firms has created 6.4 billion RMB revenues and R & D intensity (R & D inputs divided by sales revenues) has arrived at 10%.

6. Conclusion and Perspectives

In this research, we study empirically in depth the determinants of newly inward FDI across twenty manufacturing industries (2-digit) in China, over the period 2001- 2008, and we are particularly interested in 9 high-tech (HT) and mediumhigh-tech (MHT) industries. We obtain the main results as follow: firstly, host technology resources are significantly positive determinants for newly inward FDI at industrial level; secondly, HT and MHT industries are more attractive for MNCs than lower technology industries; thirdly, MNC’s “newly oligopolistic reactions” play important roles for FDI in technology industries, namely, foreign firms’ concentration and agglomeration effects encourage industrial FDI; however, local protection prevents newly FDI; fourthly, in technology industries, FDI are both market and export seeking, moreover, high productivity and large economies of scale are also centripetal forces for attracting industrial FDI.

While we believe that our estimated results are reasonably representative of the determinants of industrial FDI in China’s manufacturing sectors, there is, however, a simple bias since we have only considered twenty industries (2-digit), due to statistical limitation. In future studies, we will investigate industrial FDI determinants at finer industrial level and take into account more technological resources variables, such as patent application and strategic R & D alliance.

7. References

[1] R. E. Caves, “Causes of Direct Investment: Foreign Firms’ Shares in Canadian and United Kingdom Manufacturing Industries,” The Review of Economics and Statistics, Vol. 56, No. 3, 1974, pp. 279-293. doi:10.2307/1923965

[2] S. Lall and N. S. Siddharthan, “The Monopolistic Advantages of Multinationals: Lessons from Foreign Investment in the US,” The Economic Journal, Vol. 92, No. 367, 1982, pp. 668-683. doi:10.2307/2232556

[3] S. H. Hymer, “The International Operations of National Firms: A Study of Direct Foreign Investment,” PhD Thesis, MIT Press, Cambridge, 1976.

[4] H. Flam and E. Helpman, “Vertical Product Differentiation and North-South Trade,” American Economic Review, Vol. 77, No. 5, 1987, pp. 810-822.

[5] P. K. Tharakan and B. Kerstens, “Does North-South Horizontal Intra-industry Trade Really Exist? An Analysis of the Toy Industry,” Weltwirtschaftliches Archiv, Vol. 131, No. 1, 1995, pp. 86-105. doi:10.1007/BF02709073

[6] Organization for Economic Co-operation and Development, “Export Competition: Price or Quality,” OECD Working Party on Globalization of Industry Working Paper, 27 April 2011.

[7] Y. Chen, “Agglomeration and Location of Foreign Direct Investment: The Case of China,” China Economic Review, Vol. 20, No. 3, 2009, pp. 549-557. doi:10.1016/j.chieco.2009.03.005

[8] L. K. Cheng and Y. K. Kwan, “What Are the Determinants of the Location of Foreign Direct Investment? The Chinese Experience,” Journal of International Economics, Vol. 51, No. 2, 2000, pp. 379-400. doi:10.1016/S0022-1996(99)00032-X

[9] J. P. Walsh and J. Yu, “Determinants of Foreign Direct Investment: A Sectoral and Institutional Approach,” IMF Working Paper, WP/10/187, 2010.

[10] T. Horst, “Firm and Industry Determinants of the Decision to Invest Abroad: An Empirical Study,” The Review of Economics and Statistics, Vol. 54, No. 3, 1972, pp. 258-266. doi:10.2307/1937986

[11] F. Knikerbocker, “Oligopolistic Reaction and Multinational Enterprise,” Harvard University Press, Cambridge, 1973.

[12] R. E. Caves, “American Industry: Structure, Conduct, Performance,” Prentice-Hall, Englewood Cliffs, 1982.

[13] P. R. Krugman, “Geography and Trade,” The MIT Press, Cambridge, 1991.

[14] P. R. Krugman, “Increasing Returns and Economic Geography,” The Journal of Political Economy, Vol. 99, No. 3, 1991, pp. 483-499. doi:10.1086/261763

[15] M. Fujita and J. F. Thisse, “Economics of Agglomeration Cities, Industrial Location, and Regional Growth,” Cambridge University Press, Cambridge, 2002.

[16] J. L. Mucchielli and F. Puech, “Internationalisation et Localisation des Firmes Multinationales: L’Exemple des Entreprises Françaises en Europe,” Economie et Statistique, No. 363-365, 2003, pp. 129-144.

[17] M. Crozet, T. Mayer and J. L. Mucchielli, “How do Firms Agglomerate? A Study of FDI in France,” Regional Science and Urban Economics, Vol. 34, No. 1, 2004, pp. 27-54. doi:10.1016/S0166-0462(03)00010-3

[18] S. Cheng and R. Stough, “Location Decisions of Japanese New Manufacturing Plants in China: A Discrete-Choice Analysis,” The Annals of Regional Science, Vol. 40, No. 2, 2006, pp. 369-387. doi:10.1007/s00168-005-0052-4

[19] J. L. Mucchielli and P. Yu, “MNC’s Location Choice and Agglomeration: A Comparison between US and European Affiliates in China,” Asia Pacific Business Review, Vol. 17, No. 4, 2011, pp. 1-24.

[20] J. L. Mucchielli and P. Yu, “Do MNCs Engage in Hierarchical Location Choice? Evidence from US and European FDI in China,” Cahiers de Recherche de PRISM-Sorbonne, No. CR-10-37, 2010.

[21] C. Batisse and S. Poncet, “Protectionism and Industry Localization in Chinese Provinces,” The 43rd European Congress of the Regional Sciences Association Working Paper, 2003.

[22] C. Bai, Y. Du and Z. Tao, “Local Protectionism and Industrial Concentration in China: Overall Trend and Important Factors,” Economic Research Journal, Vol. 4, 2004, pp. 29-40.

[23] E. Ryšavá and E. Gaelotti, “Determinants of FDI in Czech Manufacturing Industries between 2000-2006,” IES Working Paper, No. 17, 2009.

[24] B. Ramasamy and M. Yeung, “The Determinants of Foreign Direct Investment in Services,” World Economy, Vol. 33, No. 4, 2010, pp. 573-596. doi:10.1111/j.1467-9701.2009.01256.x

[25] Y. Chen, “Upgrading Industrial Structure by Controlling FDI,” Qiu Shi, Vol. 11, 2010, pp. 8-10.

[26] J. H. Dunning, “Trade, Location of Economic Activity and the MNE: A Search for an Eclectic Approach,” In: B. Ohlin, P. O. Hesselborn and P. M. Wijkman, Eds., The International Allocation of Economic Activity, Macmillan, London, 1977.

[27] J. H. Dunning, “International Production and the Multinational Enterprise,” George Allen & Unwin, London, 1981.

[28] J. H. Dunning, “Multinational Enterprises and the Global Economy,” Addison-Wesley Publishing Company, Wokingham, 1993.

[29] J. R. Markusen, “Multinational Firms and the Theory of International Trade,” MIT Press, Cambridge, 2002.

[30] F. Noorbakhsh, A. Paloni and A. Yousseff, “man Capital and FDI Inflows to Developing Countries: New Empirical Evidence,” World Development, Vol. 26, No. 7, 2001, pp. 1593-1610. doi:10.1016/S0305-750X(01)00054-7

[31] Q. Liang, “Theory of Industrial Agglomeration,” The Commercial Press, Beijing, 2004.

[32] S. Lall and Z. Shalizi, “Location and Growth in the Brazilian Northeast,” Journal of Regional Science, Vol. 43, No. 4, 2003, pp. 663-681. doi:10.1111/j.0022-4146.2003.00315.x

[33] Y. Weng and B. J. Liu, “The Determinants of FDI in US Manufacturing by Asian MNFs,” In: J.-R. Chen, Ed., Foreign Direct Investment, Macmillan Press, London, 2000, pp. 55-74.

[34] K. M. Modén, “Foreign Acquisitions of Swedish Companies: Effects on R & D and Productivity,” ISA Working Paper, February 1998.

[35] P. Karpaty and A. Poldahl, “The Determinants of FDI Flows. Evidence from Swedish Manufacturing and Service Sector,” Örebro University Working Paper, 2006.

[36] J. H. Dunning and S. Lundan, “Multinational Enterprises and the Global Economy,” 2nd Edition, Edward Elgar, Cheltenham, 2008.

[37] M. Fujita and H. Ogawa, “Multiple Equilibrium and Structural Transition of Non-monocentric Urban Configurations,” Regional Science and Urban Economics, Vol. 12, No. 2, 1982, pp. 161-196. doi:10.1016/0166-0462(82)90031-X

[38] D. C. James and H. J. Vernon, “Agglomeration of Headquarters,” Regional Science and Urban Economics, Vol. 38, No. 5, 2008, pp. 445-460. doi:10.1016/j.regsciurbeco.2008.05.002

[39] M. Brülhart and N. A. Mathys, “Sectoral Agglomeration Economies in a Panel of European Regions,” Regional Science and Urban Economics, vol. 38, No. 4, 2008, pp. 348-362. doi:10.1016/j.regsciurbeco.2008.03.003

[40] E. Helpman, M. Melitz and S. Yeaple, “Export versus FDI with Heterogeneous Firms,” American Economic Review, vol. 94, No. 1, 2004, pp. 300-316. doi:10.1257/000282804322970814

[41] M. Kotabe, “International Marketing: An Annotated Bibliography,” Journal of International Marketing, vol. 1, No. 3, 1993, pp. 110-114.

[42] T. Wilkinson and L. E. Brouthers, “Trade Shows, Trade Missions and State Governments: Increasing FDI and High-Tech Exports,” Journal of International Business, vol. 31, No. 4, 2000, pp. 725-734.

[43] C. He, H. Wei and F. Pan, “Geographical Concentration of Manufacturing Industries in China: The Importance of Spatial and Industrial Scales,” Eurasian Geography and Economics, vol. 48, No. 5, 2007, pp. 603-625. doi:10.2747/1538-7216.48.5.603

[44] J. Lu and Z. Tao, “Determinants of Industrial Agglomeration in China: Evidence from Panel Data,” China Economic Quarterly, Vol. 6, No. 3, 2007, pp. 801-816.

[45] J. Lu and Z. Tao, “Trends and Determinants of China’s Industrial Agglomeration,” Journal of Urban Economics, Vol. 65, No. 2, 2009, pp. 167-180. doi:10.1016/j.jue.2008.10.003

[46] Y. Ge, “Globalization and Industry Agglomeration in China,” World Development, Vol. 37, No. 3, 2009, pp. 550-559. doi:10.1016/j.worlddev.2008.07.005

[47] H. Yang, Y. Sun and A. Wu, “Research on Changing Trend of China’s Manufacturing Industrial Agglomeration Degree and Its Affecting Factors,” China Industrial Economics, vol. 4, No. 241, 2008, pp. 64-72.

[48] R. Resmini, “The Determinants of Foreign Direct Investment in the CEECs: New Evidence from Sectoral Patterns,” Economics of Transition, Vol. 8, No. 3, 2000, pp. 665-689. doi:10.1111/1468-0351.00060

[49] J. H. Dunning, “Trade, Location of Economic Activity and the Multinational Enterprise: Some Empirical Tests,” Journal of International Business Studies, vol. 11, No. 1, 1980, pp. 9-31. doi:10.1057/palgrave.jibs.8490593

[50] N. Kumar, “Foreign Direct Investments and Technology Transfers among Developing Countries,” In: V. R. Panchamukhi, et al., Eds., The Third World and the World Economic System, Radiant, New Delhi, 1987, pp. 139-165.

[51] F. Noorbakhsh, A. Paloni and A. Yousseff, “man Capital and FDI Inflows to Developing Countries: New Empirical Evidence,” World Development, vol. 26, No. 9, 2001, pp. 1593-1610. doi:10.1016/S0305-750X(01)00054-7

[52] D. Kyrkilis and P. Pantelidis, “Macroeconomic Determinants of Outward Foreign Direct Investment,” International Journal of Social Economics, Vol. 30, No. 7-8, 2003, pp. 827-836. doi:10.1108/03068290310478766

[53] G. Ellison and E. L. Glaeser, “Geographic Concentration in US Manufacturing Industries: A Dartboard Approach,” Journal of Political Economy, vol. 105, no. 5, 1997, pp. 889-927. doi:10.1086/262098

[54] J. H. Love and F. Lage-Hidalgo, “Analyzing the Determinants of US Direct Investments in Mexico,” Applied Economics, vol. 32, No. 10, 2000, pp. 1259-1272. doi:10.1080/000368400404416

[55] R. E. Lucas, “On the Determinants of Direct Foreign Investment: Evidence from East and Southeast Asia,” World Development, vol. 21, No. 3, 1993, pp. 391-406. doi:10.1016/0305-750X(93)90152-Y

[56] A. Chakrabarti, “The Determinants of Foreign Direct Investment: Sensitivity Analyses of Cross-Country Regressions,” Kyklos, vol. 54, No. 1, 2001, pp. 89-114.

[57] Organization for Economic Co-operation and Development, “Handbook on Economic Globalization Indicators,” OECD Press, Paris, 2005.

[58] J. A. Hausman, “Specification Tests in Econometrics,” Econometrica, vol. 46, No. 6, 1978, pp. 1251-1271. doi:10.2307/1913827

[59] M. Arellano and O. Bover, “Another Look at the Instrumental Variable Estimation of Error-Components Models,” Journal of Econometrics, Vol. 68, No. 1, 1995, pp. 29-51. doi:10.1016/0304-4076(94)01642-D

[60] R. Blundell and S. R. Bond, “Initial Conditions and Moment Restrictions in Dynamic Panel Data Models,” Journal of Econometrics, vol. 87, No. 1, 1998, pp. 115-143. doi:10.1016/S0304-4076(98)00009-8

[61] J. Lv and W. Zhang, “FDI’ Impacts on International Competitivity of Electronic Communication Industry in China,” Northern Economy, vol. 11, 2008, pp. 82-84.

[62] I. Filatotchev, X. Liu, J. Lu and M. Wright, “Knowledge Spillover through man Mobility across National Borders: Evidence from Zhongguancun Science Park in China,” Research Policy, vol. 40, No. 3, 2011, pp. 453-462. doi:10.1016/j.respol.2011.01.003

[63] K. Head and J. Ries, “Heterogeneity and the Foreign Direct Investment versus Exports Decision of Japanese Manufacturers,” Journal of Journal of the Japanese and International Economies, vol. 17, No. 4, 2003, pp. 448-467. doi:10.1016/j.jjie.2003.09.003

NOTES

1The 9 HT and MHT industries include Pharmaceuticals, Electronicscommunication, Office equipment, Special Machine and equipment, Chemical products, Chemical fiber products, Motor vehicles, Electrical machinery and equipment, Machinery and equipment.

2Refer to official site of Zhangjiang Hi-Tech Park (http://www.zjpark.com/Second.aspx?infoitem_id=7&infoitem_pid=1).

3Refer to Table 2 in p. 82 of [61].