Open Journal of Business and Management

Vol.04 No.04(2016), Article ID:69896,35 pages

10.4236/ojbm.2016.44061

Intellectual Capital: An Exploratory Study from Lebanon

Hussin J. Hejase1*, Ale J. Hejase2, Hassana Tabsh3, Hassan C. Chalak4

1Faculty of Business Administration, Al Maaref University, Beirut, Lebanon

2Faculty of Economics and Business Administration, Islamic University of Lebanon, Beirut, Lebanon

3Human Resources Office, Lebanese American University, Beirut, Lebanon

4Faculty of Business and Economics, American University of Science and Technology, Beirut, Lebanon

Copyright © 2016 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/

Received: July 12, 2016; Accepted: August 19, 2016; Published: August 22, 2016

ABSTRACT

Organizations are spending quality time to build their Intellectual Capital by attracting people with talent; a caliber that has become a valuable asset in the business world, especially since talented people are difficult to find. Intellectual Capital is the knowledge that individuals put into advantage in their respective companies; as such, it is an organizational competitive advantage and helps in value creation. The Human Resources Department creates value for these organizations by coming up with effective human- resource related solutions and creative ideas for dealing with and retaining people who have the right talent. To achieve the aforementioned, employees’ qualifications have to be evaluated in terms of knowledge, skills, education, in addition to future potentials and ability to cope with change. Consequently, organizations have become interested in developing their human capital by developing their employees’ knowledge, applied experience, enterprise process, customer relationships, and professional skills. This paper discusses “Intellectual Capital” as a modern HR concept that has influenced business processes and plans. It aims at exploring and assessing the extent of awareness of such concept, current challenges it faces, its future, and also the different views and thoughts regarding it. In addition, the research focuses on how to exploit and retain Intellectual Capital and identifies the financial and non-financial organizational benefits gained by employees. The research is exploratory and explanatory, quantitative in nature using a survey questionnaire responded by 258 Lebanese employees and managers working in different business sectors. Collected data are evaluated statistically through computer software SPSS-22. Findings are used to support existing managerial practices and policies for better retention practices and management of Lebanese human resources.

Keywords:

Human Capital, HR, Intellectual Capital, Lebanon, Retention, Talent

1. Introduction

Intellectual Capital is currently a popular and extensively discussed topic. According to Huang and Liu (2005), there is a widespread recognition that Intellectual Capital is a critical force that drives economic growth [1] . In the past, enterprises were solely considered and evaluated by their physical and tangible assets, whereas now, the details of their financial or nonfinancial assets are fundamental factors in the evaluation process whereby a much accurate consideration of firms’ real value is required; this shift is a leading reason as to why Intellectual Capital has incurred a critical value for companies and nations. Lockwood (2005; cited in [2] ) contends that in “today’s global marketplace, talent management represents one of the greatest challenges for HR leaders: successful talent management requires effective alignment of human capital and business strategies to support organizational financial goals and positively impact shareholder value” (p. 1). Rappaport (2006) asserts that “companies can develop leading indicators of value, which are quantifiable, easily communicated current accomplishments that frontline employees can influence directly and that significantly affect the long-term value of the business in a positive way” [3] (Para 29).

There are several objectives that have led the researchers to choose this major topic. First of all, this research will let readers and researchers understand what Intellectual Capital is. Readers will understand how this capital contributes to the organizations’ success. Managers and businessmen will be able to assess its true value to organizations, and will know how to utilize the most valuable asset, the people, to tap into the deepest power within the organization. This paper will also show the importance of exploring employees’ skills and needs. It will majorly determine how Intellectual Capital is managed to enhance its potential to increase wealth. Organizations may be unaware of the extent and importance of their Intellectual Capital for future sustainability; accordingly, this research is designed to highlight the importance of this capital. The research explores how Intellectual Capital is perceived by an organization and how it is being managed.

2. Literature Review

Robbins and Coulter (2009) contend that, “management involves coordinating and over- seeing the work activities of others so that their activities are completed efficiently and effectively” [4] (p. 22). However, the implied meaning in this definition needs to be well clarified so as to understand its relation to Intellectual Capital. Robbins and Coulter (2009) assert that first of all, an organization is “a deliberate arrangement of people gathered to accomplish some specific purpose” [4] (p. 30). Hence, any organization, whether new or old, small or big, requires certain methods, procedures and plans in place for its efficient functioning. For this to happen, these organizations must develop and implement management concepts which help them implement their vision for the future of the organization. Each organization has a distinct purpose. Therefore, as people within the organization have become of central importance to an organization, and since the human resource function is the guardian of talent within the organization, it becomes imperative to address Human Resources management (HRM). Lockwood (2006), in a study for the Society for Human Resource Management − SHRM, encourages companies to seriously invest in human capital, whereby “HR leaders act as business partners while working closely with senior management to attract, hire, develop and retain talent” [5] (Para 1). Mondy and Mondy (2012) define Human Resources Management (HRM) as “the utilization of individuals to achieve organizational objectives. Consequently, managers at every level must concern themselves with HRM. Basically, all managers get things done through the efforts of others; this requires effective HRM. Individuals dealing with human resources matters face a multitude of challenges, ranging from a constantly changing workforce to ever-present government regulations, a technological revolution, and natural disasters as flooding, hurricanes, and tornadoes. Furthermore, global competition has forced both large and small organizations to be more conscious of costs and productivity. Because of the critical nature of human resources issues, these matters must receive major attention from upper management” [6] (p. 30).

Consequently, and based on the aforementioned interest in human resources, it is imperative for the organization to maintain a productive working environment, build positive interpersonal relationships and engage in problem solving. This can only be done effectively, with proper communication among employees. “Communication can help motivate, build trust, create shared identity and spur engagement; it provides a way for individuals to express emotions, share hopes and ambitions and celebrate and remember accomplishments. Communication is the basis for individuals and groups to make sense of their organization, what it is and what it means” [7] (Para 9).

HR practices have undergone many changes since 1950s. Jayaraman (2012) found that “driven by continuous changes in the business conditions accompanied by aggressive advancements in technology, people practices have helped in significant improvements in productivity and value creation” [8] (p. 14). In response to the aforementioned changes it became apparent that total people’s engagement and involvement at all levels of the organization is a must or a necessity. Hence, to generate organizational wealth and to secure sustainability, the HR function had to encourage people to collaborate, to align behind the vision and mission of the organization, to follow a well-es- tablished strategy, and to meet the needs and aspirations of customers [8] .

Conner and Ulrich (1996) claim that it is imperative for the HR function to undergo a large-scale transformation, and that many companies are discovering the need to reinvent the Human Resource function [9] (p. 38). Nonetheless, Lawler III (2011) declares that the “HR function has not progressed significantly in terms of its strategic role in corporations” [10] (p. 171); “Fundamental change is needed in how organizations are designed to make and implement decisions concerning Human Capital” [10] (p. 172).

Companies have the choice to either respond to change or to lead the change. Consequently, HR executives need to approach the opportunity to shape how they respond to the demands that their function entails; otherwise, HR executives who stick with the status quo and maintain a focus on transactional work will soon become obsolete. Moreover, HR professionals who meet the need for strategic expertise concerning human capital management and organizational effectiveness will contribute value that far exceeds the past contributions of the HR function. In the process, HR professionals will make themselves indispensable to their organizations [11] .

According to Adelman (2010) [12] , a key challenge today is that employees have excellent “Tacit Knowledge”, that is, knowledge about their job, the business processes, the data that supports their job and those processes, as well as knowledge of how to most effectively make things happen, and the insight into what works and what does not. Unfortunately, in most situations, the said employees have no means, or incentive to share their knowledge. Their tacit knowledge has not been captured, transferred, or made available to others. “One impact of today’s recession and unemployment situation is that this knowledge is potentially lost to the organization. HR professionals and managers have a major challenge to obtain and store information about: 1) core job knowledge of all employees, their experience, and their key skill-sets; 2) training; 3) performance review systems and measurement metrics; 4) development of effective succession planning systems; and 5) leadership and management development programs” [12] (Para 10).

Herein are some excerpts of how Intellectual Capital has been defined in literature.

2.1. Intellectual Capital

Many prominent authors have presented a general concept of Intellectual Capital (IC) ( [13] , [14] ). The term “Intellectual Capital” was first introduced by John Kenneth Galbraith in 1969 [15] (p. 1337). Kozak (2011) pointed out that the concept of Intellectual Capital is still underdeveloped, and there is no uniform definition accepted for identifying its subcomponents [16] . However, many researchers have attempted, in various ways and for over a few decades, to define the concept of Intellectual Capital.

“Intellectual capital has been considered by many, defined by some, understood by a select few, and formally valued by practically no one” (Sveiby, 1997; cited in [17] , p. 298). Intellectual Capital has been rarely understood or studied. For organizations; Intellectual Capital is considered as an essential source to gain competitive advantage [18] . IC is described by Edvinsson and Sullivan (1996, p. 358) as the knowledge assets that can be converted into value [19] ; knowledge that Stewart (1997) contends has been given by individuals to the company, which is supposed to be an organizational competitive advantage and helps in value creation [20] . Moreover, Edvinsson (1997; cited in [21] ) emphasizes that “Intellectual Capital includes all the processes and the assets which are not normally shown on the balance sheet and all the intangible assets (trademarks, patents and brands) which modern accounting methods consider” [21] (p. 82). It includes the sum of the knowledge of its members and the practical translation of their knowledge. Intellectual Capital is the difference between the book value of the firm and the amount of money someone is prepared to pay for it [22] .

In Edvinsson’s (1997) view, Intellectual Capital is a combination of Human Capital (the brains, skills, insights and potential of those in an organization) and Structural Capital (things like the processes wrapped up in customers, processes, databases, brands and systems). Intellectual Capital is the ability to transform knowledge and intangible assets into wealth-creating resources, by multiplying human capital with structural capital. This is the Intellectual Capital multiplier effect [23] .

Harrison and Sullivan (2000) [24] state that Intellectual Capital is knowledge that can be converted into profit. “Intellectual Capital” represents the main firm intangible resource that can help create opportunities for stable competitive advantage and also help create value and wealth in a Knowledge-based Economy ( [25] , [26] ).

Stralser (2004) states that “Intellectual Capital consists of the knowledge, expertise, and dedication of an organization’s workforce. The management of Intellectual Capital is necessary in order to get the most out of an organization’s material resources and achieve organizational goals” [27] (p. 19). Getting the most from employees necessitates appropriate motivational policies, for “motivation is an important driver in an organization and is crucial to the management of Intellectual Capital” [27] (p. 20). Moreover, effective and efficient utilization of Intellectual Capital constitute a primary goal of high-performance organizations. Stralser (2004) contends that “high-performance organizations focus on Employee Involvement, Teamwork, Organizational Learning, Total Quality Management (TQM), and Integrated Production Techniques” [27] (p. 33).

Intellectual Capital, in the last two decades, has been defined as a valuable intangible resource, which positively affects the firm’s economic value [28] , firm’s performance [29] , and firm’s value depicted by the difference between the market value and booked organization assets [26] . The aforementioned term “Intangible” is a concept on whose definition no consensus exists. Authors like Lev (2001) [22] , Andriessen (2004) [30] , and Cohen (2005) [31] , argue about the intangibles’ impact on businesses and on company’s value creation; thus, historically, intangibles have been treated as an aggregated amount (goodwill), without impact on national wealth, neither is included in financial statements of firms. According to Lev (2001), an intangible asset is any asset that has a future economic benefit or income for the organization but does not have physical representation, such as goodwill [22] . It could be considered as an accounting element. Blair and Wallman (2003) define “Intangibles as non-physical factors that contribute to, or are used in, the production of goods or the provision of services or that are expected to generate future productive benefits to the individuals or firms that control their use” [32] (p. 451). While Andriessen (2004) considers that intangible assets should rather be regarded as intangible resources, because the asset term implies control and ownership, while resource is more appropriate to the intangible nature [30] . As for Epstein and Mirza (2005), “goodwill, in nature, represents a residual, which incorporates all intangibles that cannot be measured separately. The researchers focus on those ones that can be identifiable and be measured under impairment approaches, having or not an indefinite lifetime” [33] (p. 234).

2.2. Knowledge and Intellectual Capital

In their definition, Carroll and Tansey (2000) state that Intellectual Capital is best conceived as the knowledge and creativity available to a firm to implement a business strategy that maximizes stakeholders’ value [34] . The definition is broad and designed in such a way that it refers to the benefits to be gained through the application of knowledge. Moreover, the importance of Intellectual Capital has seriously increased in the recent years, since the gap between market values and book values of firms is getting wider; “Especially between the late 1990s and early 2000s, firms with intangible assets enlarged tremendously. A large portion of the value of these firms was linked to their intangible assets instead of tangible and physical assets” [35] (p. 328). Furthermore, Seetharaman, Sooria, and Saravanan (2002) contend that in the new economy, knowledge is considered to be a vital production factor and is the most important competitive advantage of organizations [36] . Later on, Rastogi (2002) asserts that the Intellectual Capital of an enterprise represents its holistic capacity and prowess to create value through exploitation of knowledge as the quintessential resource [37] ; a fact supported by Foray (2004; cited in [38] , p. 15) who points out that in the knowledge-based economy, the contribution of intangible assets is greater than tangible assets. Also, as Peter Schwartz wrote in the September 2000 issue of “Red Herring” (cited in [39] ) that “in the organization of today’s economy, it is knowledge that counts more than anything, knowledge has value. Creating value is about creating new knowledge and capturing its value. The most important property is Intellectual Property. Committed employees creating new ideas, delivering value, and innovating to create growth are the key assets of the new economy” [39] (p. 2). Also, with the revolution in information technology, in the early 1990s, the global economy model has changed fundamentally. In today’s knowledge economy, knowledge is the most important capital and has replaced financial and physical capital [40] . Moreover, Mitchell (2010) asserts that to every business that exists to increase wealth, Intellectual Capital is critical to achieve greater wealth and results [41] . And finally, Pourkiani, Sheikhy, and Daroneh (2014) present Intellectual Capital as “a knowledge package that includes a set of intangible and invisible resources, principles, culture, behavior patterns, capabilities, competencies, structures, communications, processes, processes of knowledge. All knowledge is based on subjective perceptions. Entering the knowledge economy, knowledge is more preferable compared to other factors of production such as land, capital and machinery” [42] (p. 512).

However, to capitalize on the aforementioned knowledge package and to maintain competitive advantage, the company should always look for new knowledge and utilize it in new creative ways. This requires securing an organizational environment that will encourage individuals to employ and exploit this knowledge, taking into consideration that talented employees leave the organization if they are not satisfied with the total rewards, leadership and organizational policies etc. These problems occur when proper talent management practices are not in place [43] . However, to counter the impact of the aforementioned problems, organizations must guarantee the existence of proper motivation, understanding and resources. Hence, knowledge management and motivation management are key strategic elements for securing and sustaining the competitiveness of a company [44] . Moreover, Montano (2005) assert that knowledge “is one of the main organizational assets that increase the value of an organization, and that when appropriately applied can lead to the development of a new or improved products or services” [45] (p. 285). Knowledge is the bedrock that is supporting today’s corporate strategies [46] . In knowledge based economy, “Intellectual Capital is the most critical asset of the organization” (Ramezan, 2011; cited in [38] p. 15). Consequently, and as Hejase, Haddad, Hamdar, Al Ali, Hejase, and Beyrouti (2014) assert, organizations should motivate employees to learn and share knowledge to sustain the value-adding process. “Employees need to be able to associate new obtained knowledge with special rewards, such as higher job security and personal satisfaction and fulfillment. After understanding and associating cost to benefits, people will start to see the psychological costs of change and learning as being less than the value they may attain from acquiring new knowledge” [47] (p. 1554).

2.3. Process and Components

Generally, a number of classification literatures ( [20] , [26] and [48] - [50] ) divide Intellectual Capital into three categories:

1) External (Customer-Related) Capital,

2) Internal (Structural) Capital, and

3) Human Capital.

The aforementioned authors state that Intellectual Capital is based on various intangible resources, such as employees’ competence, knowledge, education, skill, intellectual agility, brand name, customer relationship and organization structure, taking into consideration that Ismail (2005) added Spiritual Capital as the fourth component of Intellectual Capital [51] , and that Bueno, Salvador, and Rodriguez (2004) [52] and Wu and Tsai (2005) [53] had extended the concept of Intellectual Capital in their research and introduced two more components, namely Social Capital and Technological Capital. However, Ramezan (2011) states that the components of Intellectual Capital are Human Capital, Organizational Capital (or Structural Capital), Technological Capital, Social Capital and Business Process Capital (or Customer Capital) [54] . Accordingly, the components of Intellectual Capital will be divided in this paper into fundamental components, Human Capital, Structural Capital, and Relational Capital; Spiritual Capital; Social Capital; and, Technological Capital. However, it is important to mention that some researches like Nemec Rudež (2005, pp. 325-326) classify Intellectual Capital into “A Two-Side Intellectual Capital Classification” and “A Three-Side Intellectual Capital Classification”. The two-side classification consists of Human Capital and Structural Capital, while the three-side classification contains Human Capital, Structural Capital, and Relational Capital. So, there are several models or classifications that might be applicable for the study of Intellectual Capital [55] .

2.3.1. Human Capital

Human Capital has been defined as the knowledge, skills, and abilities residing within and utilized by individuals [56] . Human Capital is the heart of Intellectual Capital. Human Capital (HC) is known as an organization’s combined human capability for solving different business problems. It is inherent in employees and cannot be owned by a firm [49] . As the literature has indicated, HC focuses on competencies, attitudes and intellectual agility. So, Human Capital is made of different knowledge assets of the person, such as people knowledge backlog coming from training, skills, innovation and others [57] . This capital is a part of the underpinnings core competence of the organization [58] . Human Capital has been considered as the primary element of Intellectual Capital and the most important source of sustainable competitive advantage ( [49] , [59] ). Moreover, Starovic and Marr (2004) discern that according to “guidelines produced by researchers from universities across Europe, collectively known as the Meritum Project, Human Capital is defined as the knowledge, skills and experience that employees take with them when they leave. Some of this knowledge is unique to the individual; some may be generic” [60] (p. 6). Human Capital also encompasses how effectively a firm uses its employees’ resources as measured by innovation and creativity. Human Capital includes anything associated with the people within the organization. It includes elements such as employees’ tacit knowledge, skills, experience and their attitude [61] .

Based on the aforementioned definitions, it can be deduced that Human Capital is a major source of value addition in organizations as it is based on skills, knowledge and expertise, competence, attitude, and intellectual agility of employees. The improvement of Human Capital consists of a set of competencies which are necessary for using knowledge and skill in order to access outcomes of organizational programs. These competencies include features such as creativity, flexibility, leadership ability, problem solving ability, holding constructive relationships with others, entrepreneurship, and complex skills like “the knowledge of how to learn”. “Since human capital is considered as the main stimulus for growth in this economy, it can determine the competitive status of a country. The successful development of this economy considerably depends on the quality of education and the educational system” [62] .

2.3.2. Structural Capital

Structural Capital (SC) includes codified knowledge, procedures, processes, goodwill, patents, systems, information system, databases, hardware, software and culture. Some authors declare that HC creates SC and that the quality of SC is most likely a reflection of the quality of HC [49] . In contrast to Human Capital, Structural Capital (SC) is described by OECD (1999; cited in [63] , p. 55) as “What is left after employees go home for the night”. Structural Capital of organizations represents all the nonhuman storehouses of knowledge, including databases, organizational charts, process manuals, strategies, routines and policies ( [29] , [53] ). Jamshidy et al. (2014) referred to Moon and Kym (2006) who state that SC facilitates the use of available knowledge resources as a supportive infrastructure, databases and processes of the firm that enable the manager and employee to function and run the firm in order to implement and enhance the delivery of goods and services. While firms do not own HC, Structural Capital belongs to the firm as a whole [63] .

2.3.3. Relational Capital

Several researchers [28] and [64] contend that Relational Capital comprises alliances, relationship with different stakeholders (such as customers, partners, suppliers, investors and so on) as well as franchises, trademarks, licenses, distribution networks, government bodies and agencies, image and brand, communities, public and environment. Roos, Bainbridge, and Jacobsen (2001) emphasize the importance of the relationship with customers to organizations because customers buy products or services from the enterprises [65] . This relationship is stressed by Ciemleja and Lāce (2008) as the basic principle of Customer Capital [66] ; a notion shared by Tai-Ning, Hsiao-Chen, Shou-Yen, and Chiao- Lun (2011) [67] . Such capital contains a customer base, knowledge about customers, and cooperation in terms of historical and future predictions. Customer Capital is considered a future income or cash flow from the current and potential customers. However, “it is a value that bases upon the reliable, sustainable and mutually beneficial relationships between the customer and enterprise and it is related to the investments from the enterprise. The value generation process is influenced by such elements: product or service price, quality and functionality; identification and reputation of the enterprise; interrelation position between customers and enterprise staff” [66] (p. 31).

Moreover, this kind of capital has also influence on networking and the relation function of the Board of Directors (BOD) within and outside the firm [68] . The BOD is seen as a potentially central resource for the firm, which especially plays a vital role between the firm and the different providers of resources, in particular the different resources for the operations of the firm [68] . It is very important for organizations to satisfy their customers’ needs [67] . Therefore, Customer Capital is an important component of Intellectual Capital and is based on customer satisfaction, loyalty and network. However, Nemec Rudež (2005) divided Relational Capital into two categories [55] . Her justification is based on the fact that relationships with customers are crucial for service industries; and, that Customer or Relationship Capital should be separated from Structural Capital. To Rudež, what characterizes the services is the fact that it is very difficult to repair mistakes or improve the service after it is delivered to the customer. Therefore, service industries have critical soft skills needed to guarantee fast response to customers’ complaints or customers’ concerns including reliability, courtesy, attentiveness, helpfulness, care, friendliness, understanding the customers, responsiveness, and com- munications. Thus, according to Rudež, the importance of customer care indicates that the three-part intellectual capital classification is more adequate than the two-side one in service industries. “From the view of value creation, we found necessary to divide relationship capital into two parts:

・ Customer Capital, defined as an asset shaped by relationships between the company and its customers; and,

・ Non-customer Capital, defined as an asset shaped by relationships between the company and every subject in its environment but customers” [55] (p. 329).

2.3.4. Other Components of Intellectual Capital

In addition to the previously mentioned Intellectual Capital’s components, several researchers and theorists have defined more components of IC.

2.3.5. Spiritual Capital

Jamshidy et al. (2014) referred to Zohar and Marshall (2004) and Ismail (2005) in their review about Spiritual Capital [63] . For example, Zohar and Marshall (2004) have applied the term “spiritual capital” as “the amount of spiritual knowledge and expertise available to an individual or a culture, adding that the word-spiritual-refers to meaning, values and fundamental purposes” [63] (p. 27). Spiritual Capital is identified by Ismail (2005) as “the intangible knowledge that includes faith, belief and emotion embedded in the minds and hearts of individuals and in the heart of the organization which includes vision and direction, principles, values and culture”. He believes “the individual and organization behave and act with honor, integrity, sincerity, honesty, truth, trust, love, morals and ethics” [51] (p. 9). According to Isamil, Spiritual Capital also includes motivation, self-esteem, courage, strength, commitment, teamwork, determination, desire, enthusiasm and team spirit [51] .

Spiritual Capital is considered a recent form of capital and is known as the new- found Intellectual Capital form of the firm and organization. Scholars (Verter, 2003; Zohar and Marshall, 2004; Metanexus Institute, 2006; all cited in [63] , p. 56) have stated that it has arrived through three separate paths: sociological constructs; individual spiritual intelligence at the organizational level; and, quantification of the value of spirituality and religion in economic terms. However, according to Middlebrooks and Noghiu (2010), “Despite the fact that these three paths overlap, each of them offers a diverse conceptualization of spiritual capital, particularly at the operationalization level” [69] (p. 73).

2.3.6. Social Capital

According to Requena (2002), “possessing the elements of social capital is the sole most important indicator of quality work conditions and efficiency in an organization” [70] (p. 10). While, Ekinci (2008, p. 21; cited in [71] ) contends that “the theoreticians who were influential in the conceptualization of social capital define it as a combination of trust, social networks, mutuality, values and norms, which guide people’s cooperation and have a role in economic development and social well-being” (p. 212). Referring to the aforementioned definition, Social Capital is the basis of all social organizations, ranging from interpersonal relationships, groups, institutional and organizational structures to larger social segments. Accordingly, Çelik and Ekinci (2012) assert that “Social Capital grows in relation to value-based social relationships. The formation and strengthening of these values also depends on the relations between individuals and groups” [71] (p. 213). In their research about Social Capital and schools, they found that “of the dimensions of social capital, a positive relationship was observed between ‘organizational commitment’ and success groups” [71] (p. 221).

2.3.7. Technological Capital

According to De Castro, Navas López, García Muiñac, and Sáez (2004), “Technological Capital is composed of four basic elements: research, development, and innovation (R & D & I); technological infrastructure; intellectual and industrial property, and results of innovation” [72] (pp. 10-11). Longo-Somoza, Bueno and Acosta-Prado (2015) state that Technological Capital refers to the “combination of intangibles directly linked to the development of the activities and functions of the technical systems of operations, responsible for obtaining products with a series of specific attributes” [73] (p. 5).

2.3.8. Managing Intellectual Capital

The process to reach Successful Intellectual Capital Management was discussed by several authors and theorists. Marr (2008) gives a five-step process to succeed in managing Intellectual Capital, namely, identifying, mapping, measuring, managing, and reporting Intellectual Capital as shown in Exhibit 1 [74] .

Exhibit 1. Five steps to manage Intellectual Capital, [74] .

The first step: An inventory check. It requires the identification of an organization’s Intellectual Capital. The categorization of Intellectual Capital can be used to facilitate a discussion about the current stock of intangibles. It can be used to create a template that informs people about the different categories of Intellectual Capital, and prompts them to think about their organizations’ different types of intangibles. Intellectual Capital can be identified through conducting interviews, facilitated workshops, or via mail or online surveys.

Second step: Mapping the Intellectual Capital Value Drivers: A value creation map is a visual representation of the organizational strategy. Mapping the key value drivers into a visual map has two primary functions. The first is to ensure that the strategy with all its Intellectual Capital value drivers is integrated and coherent; the second is to enable easy communication of the strategy and the role and importance of Intellectual Capital in delivering the strategy. A value creation map brings together the three key elements of an organizational strategy, namely, its value proposition, its core activities, and its enabling strategic elements or performance drivers.

Third step: Measuring Intellectual Capital: After identifying and mapping the Intellectual Capital value drivers, organizations can start measuring them. Many tools and techniques are available to measure Intellectual Capital.

Fourth step: Managing Intellectual Capital: Measures allow organizations to manage Intellectual Capital. Without relevant assessments, it is impossible to understand current performance levels, know whether the Intellectual Capital has improved or deteriorated, and understand whether any activities and initiatives have affected performance. Organizations that have meaningful performance information about its Intellectual Capital can use it to inform decision making, to test and review strategy, and to manage risks associated with Intellectual Capital.

Fifth step: Reporting Intellectual Capital: The final step is to report the Intellectual Capital. Disclosing the value of Intellectual Capital can be done for different reasons. However, they all share one key objective, which is to provide information about the Intellectual Capital of an organization to its stakeholders.

Although Intellectual Capital is similar to tangible assets in its potential for generating future cash flows, Talukdar (2008) sees that it is radically different from Tangible Capital in the following respects [75] :

・ “Intellectual Assets are non-rival assets. Unlike physical assets which can only be used for doing one thing at a time, Intellectual Assets can be multiplexed.

・ Human Capital and Relational Capital cannot be owned, but have to be shared with employees and suppliers and customers.

・ Structural Capital is an intangible asset that can be owned and controlled by managers.

・ Structural Capital, in the form of just-in-time procurement processes and real time inventory control systems can be substituted for expensive capital expenditure such as storage warehouses.

・ Firms that leverage their Intellectual Capital to do knowledge work are able to generate higher margin of profits than those who provide mass-produced solutions.

・ Human, Structural and Relational Capital often work together in judicious combinations to give rise to core competencies that assume strategic significance. Hence, it is not enough to invest in people, systems and customers separately, but in combinations that produce end value” [75] (p. 2).

2.4. Methods and Applications

Müller (2004) contends that “when evaluating available measurement methods, one will furthermore recognize that there exists a strong emphasis on the strategic aspect of Intellectual Capital. The metrics of IC that are delivered are often highly aggregated. Consequently, their capability to transport good information about the operational aspect of Intellectual Capital is rather restricted” [76] (p. 8), noting that Neely, Marr, Roos, Pike and Gupta (2003) identify in their research a third generation of measurement systems [77] . However, they offer an insight which states that first generation measurement systems, which were financially biased, were supplemented with non-fi- nancial indicators, including intangibles. These systems were static and failed to adequately illustrate the linkage between different performance measures. Later on, second generation measurement systems offered an improvement to the first by “using strategy and/or success maps to take into account the dynamic nature of performance and the transformation processes linking objectives and resources” [77] (p. 129). The proposed third generation measurement systems will build on the aforementioned developments and “seek to link, explicitly, the non-financial and intangible dimensions of business performance to the generation of free cash flow” [77] .

Measuring Intellectual Capital helps to “recognize organizational knowledge’s flows and critical knowledge issues; to accelerate the learning patterns; identify best practices; diffuse them across the firm; and, to increase innovation and collaborative activities” (Kannan and Aulbur 2004; cited in [78] , p. 340). There exist many reasons which incite an organization to measure Intellectual Capital; these reasons can be classified into two groups: internally oriented reasons and externally oriented ones [78] (p. 340). External reasons include a better public image, an increase in market value, a reduction of the difference between market and book value, and additional information for potential investors and the market. While internal reasons include decision making, overall business success, the connection between investments in intangibles and business goals as well as the necessity to manage them [78] .

Different categories of Intellectual Capital measurement methodologies can be distinguished, and all have their pros and cons. The most structured approach of presenting the available methods was developed by Sveiby (2010). The methods are classified into four groups based on the level of measurement and the way of evaluation. These are: Market Capitalization, Return on Assets, Scorecard and Direct Intellectual Capital Methods [79] .

Nowadays, many corporations around the world have found that measuring and managing Intellectual Capital can provide them with a competitive advantage. Although there are several Intellectual Capital Measurement Methods it must be considered that calculated intangible value is not precise. However, Sveiby (2010) offers the following recommendations whereby he matched measuring approaches to measuring motives:

“1) Monitor Performance (Control). Best are Baldrige award-type of performance indicators and KPIs.

2) Acquire/Sell Business (Valuation). Best are Industry rules-of-thumb ($ per click, $ per client, brand valuation).

3) Report to Stakeholders (Justification, PR). Best are IC supplements, EVA, Triple- bottom line.

4) Guide Investment (Decision). None of the intangibles approaches can beat traditional Discounted Cash Flow.

5) Uncover Hidden Value (Learning). Best are score cards and Direct IC methods” [79] (Para 17).

No one method can fulfil all purposes; one must select a method depending on purpose, situation and audience. Gogan (2014) contends that “properly using Intellectual Capital Measurement Methods can cause the creation of competitive advantage consequently create development of the whole company” [80] (p. 175).

2.5. Benefits

The role of Intellectual Capital is important inside small and medium enterprises; the main reason is their influence on formulation and implementation of strategies in these enterprises. “Companies with strong Intellectual Capital have the chance to recruit and retain higher quality personnel” [81] (p. 242). Nowadays, organizations need to utilize all their resources, both tangible as well as intangible assets, to gain competitive advantage [82] . “The importance of Intellectual Capital is highly recognized as a successful factor not only in knowledge-intensive organizations, but also for most other types of organizations” (Lonnqvist and Mettanen, 2002; cited in [83] , p. 341).

Other studies have revealed that Intellectual Capital is positively and significantly related to organizational performance ( [18] , [29] , and [84] ) and to innovation, and competitiveness ( [82] , [85] - [87] ). On the other hand, the interaction between innovation, knowledge management and Intellectual Capital has also been studied ( [88] - [91] ), and was concluded that managers have the opportunity to take necessary actions and give a better direction to their enterprises where they are informed about their organization’s Intellectual Capital. According to Guthrie, Petty, and Ricceri (2006), Intellectual Capital definitely, “enlightens investors and shareholders with a broader perspective about the growth and improvement trend as well as potential of an organization [92] . Parallel to this issue, it is stated that sharing Intellectual Capital information of companies is also advantageous for the economy of nations, since investments are allocated much better” [92] (p. 254). Also, Rexhepi, Ibraimi, and Veseli (2013) contend that Intellectual Capital provides managers with the big picture and serves as an essential part of firm strategy [93] . Rexhepi et al. (2013) refer to Wu (2005) by stating that nowadays, “competitive advantage, material and financial resources of enterprises, depend on how organizations conduct their Intellectual Capital” [93] (p. 45). Furthermore, the aforementioned authors confirm other researchers point of view that “the future of a business move is to create values of working people; business strategy, structure, systems and processes, established by the enterprise and customer community are only possible with effective management of Intellectual Capital” [93] (p. 45).

The value organizations obtain from their Intellectual Capital is the result of well- reasoned, well-planned and well-executed set of management initiatives [94] . Hamzah and Ismail (2008) assert that “different approaches to competition require different resources; and these different resources need to be managed differently to ensure that they create the desired value. Hence, the importance of intellectual capital as a resource must be managed effectively” [95] (p. 242). Laing, Dunn, and Lucas (2010) examine the relationship between IC and financial performance of Australian hotel industry and argue that IC performance is one of the strategic assets. The study concludes that the measured financial performance heavily depends on Human Capital Efficiency (HCE), which indicates efficient staff has great capability to boost the financial performance of any organization through their effective decision making [96] . The aforementioned relationship was also confirmed by Ul-Rehman, Asghar, and Ur Rehman (2013) [97] .

In their book “Managing Intellectual Capital in Practice”, Roos, Pike, and Fernström (2006) state that the proper and efficient management of Intellectual Capital will increase transparency in the financial market which may result in lower weighted cost of capital and therefore a higher market capitalization [98] . This also helps create trust among employees and other stakeholders. In addition, it will support the long-term vision of the company since Intellectual Capital reporting is about long-term perspectives. Marr (2008) shows that Intellectual Capital helps to drive success and create value [74] . Although physical and financial assets remain important, Intellectual Capital elements such as the right skills and knowledge, a respected brand and a good corporate reputation, strong relationships with key suppliers, the possession of customer and market data, or a culture of innovation, set enterprises apart. According to Andrews (2009), the Intellectual Capital component is not well understood; it is a “black hole” of strategic analysis [99] . The key challenge in Intellectual Capital Management is transforming intangible assets into something that creates value for the organization using Dynamic Capability. Dynamic Capability is the ability to achieve new forms of competitive advantage by appropriately adapting, integrating, and reconfiguring intangible assets (organizational skills, resources, and competencies). Understanding intangible assets provides new strategic insights and competitive options for supply chain design and operation.

Talukdar (2008) explains that the tangible assets can be acquired by just about any business which has enough money to buy such assets [75] . However, intangible assets have to be cultivated, nourished and nurtured in a planned manner before their yield can be fully harvested. The real differentiator between one firm and the next therefore is the readiness of the firm’s intangible assets for converting its tangible assets to cash in the most efficient manner. This readiness is more commonly known as core competency in business texts and is the chief source of competitive advantage for companies.

2.6. Constraints

Part of the problem in managing Intellectual Capital is that many organizations do not understand its underlying power. In fact, value creation results from the interaction of the components of Intellectual Capital; for example, the ability to take a human skill or expertise and transform it into a structural asset. For instance, a marketing employee who has developed a method of handling customers efficiently can be encouraged to document his/her method so that other marketers can learn it. In some cases, the method can form the basis of an expert system in which technology can be an enabler that makes the process accessible to others. Converting skills into an organizational asset in this way illustrates the dynamic potential of managing Intellectual Capital. It can be interpreted as a means of capturing the tacit knowledge of the individual and making it explicit in the organizational structure [100] . In his article, “Intellectual Capital: A Human Resources Perspective”, Adelman (2010) states that “Human Resources Professionals and Managers have a major challenge to obtain and store information about

・ Core job knowledge of all employees, their experience, and their key skill-sets.

・ Training is perhaps more important than ever.

・ Performance review systems are based upon meaningful metrics.

・ Development of effective succession planning systems.

・ Leadership and management development programs” [12] (Para 11).

3. Research Methodology

This research is exploratory in nature, using a convenient sample based on the willingness of the respondents to participate and volunteer their time to respond to the questionnaire. The research was carried out in the period extending from July 2014 to June 2015.

3.1. Questionnaire Design

The questionnaire includes a statement describing the information to be collected followed by a statement of confidentiality in which the researchers introduced themselves to the respondents. The questionnaire consists of 45 questions divided into six parts. Different styles of closed questions are used including dyadic, multiple choice, and five- level Likert scale questions. The six parts are explained herein,

・ The first part consists of seven demographic questions.

・ The second part consists of ten questions related to the technical knowledge of the subject. It helps to assess the level of employee’s awareness of Intellectual Capital Management.

・ Third part consists of six five-level Likert scale questions regarding the “Financial Benefits” and their impact on employee’s retention. It identifies the degree of the satisfaction with the level of financial benefits.

・ The fourth part consists of ten five-level Likert scale questions related to the “Non-financial Benefits”. It focuses on listing the degree of satisfaction with several benefits such as Job Security, Work Environment, Team Work, and Work-Life Balance.

・ The fifth part consists of ten questions designed to assess the employees’ awareness of the work’s roles, tasks, conditions, and responsibilities.

・ The final part consists of six questions whose aim is to assess Knowledge Management concept, and check whether employees are familiar with this concept or not. It will also identify the most effective way to gain knowledge based on employees’ response.

3.2. Sample Selection and Size

Non probability sampling is any procedure in which elements do not have the equal opportunities of being included in a sample. The set target was to collect 300 questionnaires. First, the questionnaire was published on Surveymonkey.com through the link: https://www.surveymonkey.com/s/XC5TNV9, and then shared by the researchers (to employees-people who work) through LinkedIn, Research Gate, and Personal E-mails. After this, and from the total of 286 respondents, a total of 258 questionnaires were completely filled out. 28 questionnaires were excluded due to incompleteness or due to inappropriate filling, that is, responses selected haphazardly. Thus, the response rate is 86%. It is worth mentioning that 36.82% of the people who had filled out the questionnaire are females and 63.18% are males. Their age range is mostly between 25 and 34.

3.3. Data Analysis

All responses were entered to the SPSS program “Statistical Product and Service Solutions, an IBM product acquired by IBM in 2009 [101] (p. 58). The study was performed using exploratory statistics; data tables including frequency and percentage distributions were used and supported by their respective figures. Moreover, cross tabs were performed to study relationships between variables that may add value to the findings of the research.

4. Results and Findings

This section delineates the results in the form of exploratory statistics. Results and findings are presented in the same order as that of the sections of the questionnaire.

4.1. Demographic Analysis

63.18% of the respondents are males (163 persons) and 36.82% are females (95 persons); 50.8% of the respondents are between 25 and 34 years old, 12.8% are between 18 and 24 years old, and 23.3% are between 35 and 44 years old. The remaining percentage consists of those older than 45 years. Also, 49.6% of the respondents are single, and 47.7% are married. Moreover, 43.8% of the respondents hold a Bachelor Degree (BA/BS), and 37.6% hold a Master’s Degree (MBA/MS/MA), while 8.9% hold a high school degree and 9.7% hold a PhD.

Furthermore, 13.2% of the respondents are first line managers, 31.4% are middle managers, 21.3% are senior/executive managers, 3.9% are owners, and 19.4% hold non-managerial positions. It is important to mention that there is 10.9% who are university professors and advisors. In addition, 52% of the respondents work in the service industry, including consulting, education, information technology, and pharmaceutical companies; 30% work in Retail/Wholesale business; 9% in food production; 3% in government; and, 6% in engineering. Finally, 38.8% of the respondents have been with the company for a period from 1 to 5 years, 24.8% have 6 to 10 years of experience, 15.5% are new joiners, 10.1% have 11 to 15 years of experience, and 10.8% have been for more than 16 years at the company.

4.2. Awareness about Intellectual Capital Management

The aim of this section is to identify the degree of awareness of different related concepts, such as Knowledge Management, Human Capital, and Intellectual Capital.

When respondents were asked about their awareness of the term “Intellectual Capital”, 77.52% (200/258) answered positively; and, when asked regarding their awareness of all the company’s policies and procedures, 88.37% confirmed. Also, 93.41% feel that Human Capital is considered a valuable asset at the company, and 93.02% of the respondents confirmed that their technical and soft skills have improved during their current jobs. In addition, 97.67% of the respondents (252 persons) are aware of the importance of Human Resources (HR) Management, and 92.25% of the total respondents are familiar with the roles, tasks, and responsibilities of HR Department. However, only 54.65% of the respondents (141 persons) have attended a training/conference on HR concepts.

Moreover, out of 258 respondents, 176 persons are working at a company where the HR Department is divided into divisions/sections. 220 employees (85%) have confirmed that open communication is encouraged at the company they work at, and the remaining 38 persons (14.72%) do not think this is applicable at their companies.

When employees were asked about the existence of awareness on Employee Retention methods at the company, 71.32% of them (184 out of 258) said that these methods exist; however, 28.68% of them (74 out of 258) denied such fact.

4.3. Financial Benefits

Table 1 illustrates the different questions asked regarding the importance of the Financial Benefits for employees. Responses are presented as three categories for the sake of clarity and comparability of details whereby “Strongly Agree and Agree” are labeled as “A: Agreement” and “Strongly Disagree and Disagree” are labeled as “D: Disagreement” while keeping “U: Uncertain” as is.

Table 1 shows that respondents are marginally satisfied with their financial benefits (56.20%), with their salaries as compared to their peers (60.90%), and to their counterparts in similar jobs (53.10%). A similar satisfaction is observed as to their promotion prospects (52.70%).

4.4. Non-Financial Benefits

In the questionnaire, several non-financial benefits have been evaluated in order to assess the degree of satisfaction of respondents. First of all, 67.80% of the respondents agree that “Job Security” is ensured at the company they work at. In addition, 70.90% of them confirm that the work environment of the company is healthy and positive. “Work-Life Balance” is applicable at 59.3% of the respondents’ companies/jobs. 69.80% of surveyed employees (180 out of 258 persons) agree that Team Work level is high and is encouraged by managers. The companies of 143 respondents (55.40%) have a program to show appreciation to employees. The current company’s culture and values are adaptable for 72.50% of respondents. “Non-Financial Benefits” (such as Job Security, Appreciation, Career Path and Healthy Environment) are essential and very important for (241/258) 93.40% of surveyed employees. However, only 127 out of 258 (49.20%) have stated that they will stay at the company they work at whatever the financial benefit is.

4.5. Work Roles and Responsibilities/Job Conditions

This part aims to analyze the degree of satisfaction with the work conditions as well as the degree of commitment to the company/team. In response to the sentence “I’m happy working with the members of the group”, 89.14% of the respondents answered with “Yes”. Moreover, 93.02% of the respondents like the nature of their jobs. 81.78% are satisfied with the duties and responsibilities assigned to them. Also, 72.48% of the respondents claim that the work schedules are flexible, 72.86% of the respondents believe that their workload is fair, and only 67.05% of the respondents said that they are given the sufficient training opportunities at the current company.

Table 1. Importance of the financial benefits for employees.

4.6. Knowledge Management

This section analyzes the ability to manage the employee’s knowledge within the current job. 82.6% of the respondents confirm that their jobs’ environments help them increase their knowledge. 91.10% of employees (235 out of 258) agree with the fact that having an effective Knowledge Management applied on the company’s Human Capital will give the company a competitive advantage among other companies within the same industry.

Also, 164 out of 258 surveyed people (63.56%) agree that the company they work at gives attention to Knowledge Management. Almost the same rate of respondents (63.95%) agrees that the company cares about the knowledge of the workers. Also, 84.90% of the respondents (219 persons) confirm that they are able to increase and manage their knowledge during their work.

Table 2 shows the distribution of responses when respondents were asked to choose the most effective way to increase their knowledge. Multiple responses were allowed.

Table 2 depicts several responses whereby the top three responses were: 22.70% chose “Work Experience”, 18.58% chose the “Internet”, and 15.17% “On-Job Training”.

4.7. Cross Tabulations

When conducting survey analysis, cross tabulations (also referred to as cross-tabs) are a quantitative research method appropriate for analyzing the relationship between two or more variables. Cross tabulations provide a way of analyzing and comparing the results for one or more variables with the results of another (or others) [102] .

Results show that 50.38% (130 out of 258) of the respondents like the nature of their jobs and also agree that their salaries are fair as compared to counterparts in similar jobs in other organizations; while 21.31% (55 out of 258) like the nature of their jobs but think that the salary is not fair as compared to counterparts in similar jobs in other organizations. However, when the aforementioned statements are cross tabulated, no statistical significance is obtained (see Table 3). Similar results are obtained when studying the Cross-tab “I like the nature of my job” versus “The salary is fair compared to my peers within the organization”. Results show that 58.91% (152 out of 258) of the

Table 2. Effective ways to increase knowledge.

respondents like the nature of their jobs and their salaries are fair as compared to their peers within the organization; while 17.05% (44 out of 258) like the nature of their jobs but think that the salary is not fair as compared to their peers within the organization. However, the crosstab in question has no statistical significance (see Table 3).

Furthermore, the cross-tab “I like the nature of my job” versus “I am satisfied with the company’s financial benefits” shows that 54.26% (140 out of 258) of the respondents like the nature of their jobs and are satisfied with the company’s financial benefits; while 20.15% (52 out of 258) like the nature of their jobs but are dissatisfied with the company’s financial benefits. Here, although Pearson’s R indicates a weak and negative correlation, the crosstab in question has statistical significance (see Table 3).

4.8. Other Crosstabs Lead to the Following Results

Cross-tab “I like the nature of my job” versus “The salary adjustment granted to me reflects my level of performance” show that 42.63% (110 out of 258) of respondents like the nature of their jobs and that the salary adjustment granted to them reflects their level of performance; while 26.35% (68 out of 258) like the nature of their jobs but the salary adjustment granted to them does not reflect their level of performance. Here, Table 3 shows that Pearson’s R indicates a weak and negative correlation and there is statistical significance to the cross tab in question since the calculated error is 0.009 less than 5%.

Cross-tab “I like the nature of my job” versus “The promotion prospects in the company are acceptable” shows that 51.93% (134 out of 258) of the respondents like the nature of their jobs and the promotion prospects in the company are acceptable to them; while 21.31% (55 out of 258) like the nature of their jobs but the promotion prospects in the company are not acceptable to them. In addition, Pearson’s R indicates a weak and negative correlation and one may observe that there is a statistical significance to the cross tab in question since the calculated error is 0 less than 5% (see Table 3).

Table 3. Cross-tab results.

Note: Approx. Sig. is compared to the standard error α = 5%.

Cross-tab “I like the nature of my job” versus “I’m satisfied with the duties and responsibilities assigned to me” shows that 79.06% (204 out of 258) of the respondents like the nature of their jobs and are satisfied with the duties and responsibilities assigned to them. The crosstab in question is valid since Pearson’s R = 0.304 indicates a moderate and positive correlation and the calculated error is much less than 5% (see Table 3).

Cross-tab “Human Capital is considered a valuable asset at the company” versus “Job Security is ensured at the company” shows that 64.72% (167 out of 258) of the respondents confirm that the company considers Human Capital as a valuable asset, and that the Job Security is ensured at the company; while 13.17% (34 out of 258) confirm that the company considers Human Capital as a valuable asset but does not ensure Job Security. Moreover, Pearson’s R equals to −0.155, which indicates a weak and negative correlation; however, there is statistical significance to the cross tab in the question since the calculated error is 0.013 less than 5% as shown in Table 3.

4.9. Regression Analysis

According to Hejase & Hejase (2013) a “Multiple Regression Model is needed when the researcher faces the scenario where more than one independent variable causes variations in the dependent variable under study” [101] (p. 478). Therefore, the next step is to construct possible relationships which may help analyze the impact of “Financial” and “Non-financial” benefits on either employees or organizational factors.

4.9.1. Regression Model One

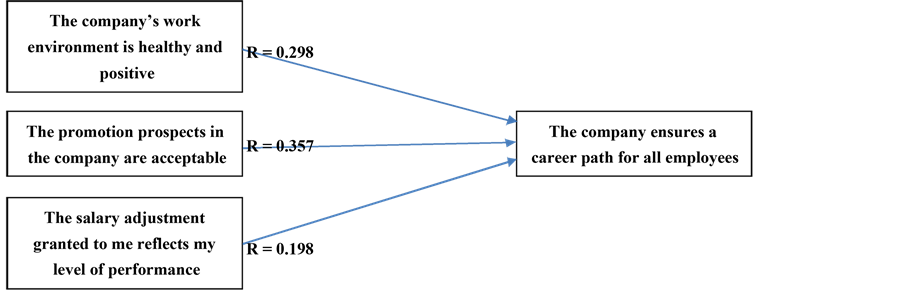

Dependent Variable: The company ensures a career path for all employees (Equal Opportunities are ensured for all).

Independent Variables: “My technical and soft skills have improved during my current job”, “The salary adjustment granted to me reflects my level of performance”, “The promotion prospects in the company are acceptable”, “The company work environment is healthy and positive”, and “Human Capital is considered a valuable asset at the company”.

Tables 4-6 provide the technical information necessary to describe the regression model. Table 4 shows the Model Summary. Results indicate that the model is quantitatively suitable due to the strong and marginal values of the coefficient of correlation (R = 0.715) and the coefficient of determination (R2 = 0.511), respectively; however, the

Table 4. Model summary.

*Predictors: (Constant), Human Capital is considered a valuable asset at the company. The salary adjustment granted to me reflects my level of performance. My technical and soft skills have improved during my current job. The promotion prospects in the company are acceptable. The company’s work environment is healthy and positive.

Table 5. ANOVA.

*Predictors: (Constant), Human Capital is considered a valuable asset at the company. The salary adjustment granted to me reflects my level of performance. My technical and soft skills have improved during my current job. The promotion prospects in the company are acceptable. The company’s work environment is healthy and positive.

Table 6. Coefficients.

Dependent Variable: The company ensures a career path for all employees (Equal Opportunities are ensured for all).

model is also qualitatively acceptable and statistically significant with F-value = 52.725 with an associated probability of Zero (which is less than α = 0.05). Table 5 shows the results of ANOVA testing which indicate that the regression equation predicts better than would be expected by chance. The F-value = 52.725 with an associated probability of Zero which is less than α = 0.01.

Table 6 shows the comparison of explanatory variables:

My technical and soft skills have improved during my current job:

This variable has a regression standardized weight of −0.069. However, is not statistically significant since sig. = 0.126 > α = 5%. Therefore, it is excluded.

The salary adjustment granted to me reflects my level of performance:

This variable has a regression standardized weight of 0.198 and is statistically significant since sig. = 0.000 < α = 5%. Therefore, it is included.

This means that for the variable “The salary adjustment granted to me reflects my level of performance”, as this variable increases by one standard deviation (SD), the dependent variable “The company ensures a career path for all employees” increases by 19.8% of a SD. This direct relation implies that the more respondents feel that their salaries are adjusted based on their level of performance, the more they will feel assured of a career path with the company.

The promotion prospects in the company are acceptable:

This variable has a regression standardized weight of 0.357 and is statistically significant since sig. = 0.000 < α = 5%. Therefore, it is included.

This means that for the variable “The promotion prospects in the company are acceptable”, as this variable increases by one standard deviation (SD), the dependent variable “The company ensures a career path for all employees” increases by 35.7% of a SD. This direct relation implies that the more respondents feel that the promotion prospects in the company are acceptable, the more they will feel assured of a career path with the company.

The company’s work environment is healthy and positive:

This variable has a regression standardized weight of 0.298 and is statistically significant since sig. = 0.000 < α = 5%. Therefore, it is included.

This means that for the variable “The company’s work environment is healthy and positive”, as this variable increases by one standard deviation (SD), the dependent variable “The company ensures a career path for all employees” increases by 29.8% of a SD. This direct relation implies that the more respondents feel that the company’s work environment is healthy and positive, the more they will feel assured of a career path with the company.

Human Capital is considered a valuable asset at the company:

This variable has a regression standardized weight of −0.048. However, is not statistically significant since sig. = 0.307 > α = 5%. Therefore, it is excluded.

4.9.2. Resultant Model

The Regression Model of results emphasizes the fact that when the company’s work environment is healthy and positive and has clear policies for salaries and promotions, it can assure equal opportunities for growth and a clear career plan for its employees. Consequently, it is the view of this study that sustained efforts to keep active work environment, clarity of responsibilities and duties, and a positive way of communication will promote organizational readiness to implement retention planning frameworks and consequently enrich human capital.

4.9.3. Summary of Major Findings

The purpose of the research is to assess the extent of employees’ awareness of the concept and applications of Intellectual Capital, and to explore the impact of financial and non-financial benefits on the “Employee Retention”. Results show that 22.48% of the surveyed employees are not aware of the term “Intellectual Capital”; a response that is considered a positive sign because companies do not really address this concept in a direct manner.93.41% of the respondents feel that Human Capital is considered a valuable asset at the company. In addition 97.67% are aware of the importance of Human Resources Management. On the other hand, 93.41% agree that Non-financial Benefits ensured by the company are very important and essential for employees to be satisfied with their job. However, only 49.22% of the surveyed employees will stay at the company mainly because of the Non-financial Benefits rather than the Financial Benefits. 56.2% of the employees surveyed are satisfied with the company’s financial benefits. Moreover, 67.05% of the respondents stated that they are given the sufficient training opportunities. Likewise, the researcher has noticed that 193 employees under survey consider “Their Work Experience” as the most effective way to increase their knowledge. “Internet” comes then with 158 votes. “On-job Training” came third with 129 answers. Fourth comes the “Books and Readings” with 121 answers. Then come “Educational Programs” and “Direct Manager/Supervisor” with 120 and 112 votes respectively. However, 84.88% of the respondents stated that they are able to increase and manage their knowledge during their work. The greatest part of the respondents are educated professionals with the age range between 25 - 34, in the beginning of career with their current employer/organization, and occupying managerial as well as non- managerial positions at companies with different industries. The majority of them (31.01%) are working with Retail/Wholesale industries.

5. Conclusions and Recommendations

In a dynamic, challenging, and fast-moving labor market, it is very important for companies to retain their Intellectual Capital. Dess, Lumpkin, and Eisner (2008) contend that “in today’s knowledge economy, it does not matter how big your stock of resources is―whether it be top talent, physical resources, or financial capital. Rather, the question becomes: How good is the organization at attracting top talent and leveraging that talent to produce a stream of products and services valued by the marketplace?” [103] (p. 124). Companies should focus on granting employees both financial and non-financial benefits. Based on the aforementioned, it is imperative to have a strong HR team at the company to set fair policies and procedures. In addition, the company’s culture should be adaptable to all the employees as this will strengthen the common view towards the vision of the company. Dess and Lumpkin (2001) contend that successful firms are well aware that the attraction, development, and retention of talent is a necessary but not sufficient condition for creating competitive advantages [104] . Also, Dess et al. (2008) stress that the talented people’s “skills and attitudes must be continually developed, strengthened, and reinforced, and each employee must be motivated and his/her efforts focused on the organization’s goals and objectives” [103] (p. 127). Furthermore, Wong and Boh (2010) assert that in the knowledge economy, it is not the stock of human capital that is important, but the extent to which it is combined and leveraged [105] .

The main objective of this research is to identify the importance of retaining and managing the Intellectual Capital. In addition, it looks into both financial and non-fi- nancial benefits for employees. The study also focuses on the big impact of having a strong and effective Human Resources Department. The survey results have revealed that 93.41% of employees are not only looking for financial benefits, but also for non-financial benefits such as job security, healthy work environment, respect, work- life balance, etc… This coincides with Pfeffer’s (2001) argument which states that paying people more is seldom the most important factor in attracting and retaining Human Capital [106] . Therefore, in order to find more ways to retain the Intellectual Capital, a question was posted on Researchgate.net (2016, a social networking site for scientists and researchers) to know what non-financial factors will retain the Human Capital at the company. The question was: “Other than good ‘Financial Benefits’, what makes an employee stay with the company he/she works at?” The question was shared with all the researchers on the site, and Exhibit 2 depicts some of the answers.

Exhibit 2. Responses collected from Resaerchgate.net.

・ Feeling the nurturing culture where support, empathy, and career plan exist.

・ Could be the feeling of belonging to a successful team and being active part of it.

・ An interesting job, great colleagues, reasonable bosses, a manageable workload, good career perspectives…

・ The more reputable the company, the longer duration and more employees stick to the company. Some of the young employees try to learn as much as they can before exploring out for better job opportunity.

・ Apart from salary, employees stay with the organizations because of working atmosphere/colleagues, Job Content, Career Opportunities, Training, Company Image, Company Culture, The Management, Internal Opportunities. Again apart from the aforementioned factors, the most important factor is the role of a supervisor or being fortunate to get a good boss because problems with the boss is the main reason why employees do not like to stay. Employee satisfaction and commitment factors are under the control of the managers, supervisors or team leaders (A Survey done by Hay Group, 1998, the sample size was half million employees over 300 companies).

・ Job Satisfaction, Superior’s Treatment, Participatory Culture, and Due Recognition.

・ Some of these factors are job security, good working conditions, loyalty, full appreciation of work, specific type of job, etc.

・ An interesting environment, kind and great colleagues and bosses, a manageable workload, and respect (among colleagues and also customers).

・ In some places or countries, it is hard to have opportunities to change for better job’s conditions and salary. People stay in the same company for their salary and the number or years of personal investment in their career despite the dissatisfaction and the frustration.

・ When a person has a personal agenda for improvement within the current job, he/ she will stick to it until objectives are achieved. From there on, the different factors mentioned in this forum are weighted against the next planned move.

・ Financial Benefits are used more to attract new people to join the company (although it will increase the level of satisfaction and employee retention). Job Security, Clear Code of Business Conducts, and a management that “LISTENS” and “ACTS” are some factors that will retain the employee within the organization.

・ “Bad Bosses” cause high turnover of employees. The problem grows further by the bosses not realizing that what they are doing is wrong.

・ The scheme of succession planning.

The collected responses shown in Exhibit 2 are but a few of what researchers and scientists have to say. Mach (2015, May 19), in her article titled, “Leadership according to Inc. Magazine’s Top 5: Jack Welch”, refers to Jack Welch’s famous quote regarding compensation: “If you pick the right people and give them the opportunity to spread their wings and put compensation as a carrier behind it, you almost don’t have to manage them” [107] (Para 2). So, it is about giving the opportunities!

This research has attempted to shed light on and explore current Lebanese “Intellectual Capital” practices as a modern HR concept that has influenced business processes and plans. Overall, findings provide support and evidence to the fact that Lebanese employers and employees bring forward a fair and positive feedback to the study and managers take the process seriously despite the fact that only 49.22% of the surveyed employees will stay at the company because of the Non-financial Benefits whatever the Financial Benefits are, and 56.2% of the employees surveyed are satisfied with the company’s financial benefits.

According to Andrews (2009), the Intellectual Capital component is not well understood [99] . The key challenge in Intellectual Capital Management is transforming intangible assets into something that creates value for the organization. Organizations of the 21st century need to have dynamic capability, that is, the ability to achieve new forms of competitive advantage by appropriately adapting, integrating, and reconfiguring intangible assets (organizational skills, resources, and competencies). Understanding intangible assets provides new strategic insights and competitive options for supply chain design and operation. The resultant model of the current research confirms what Andrews (2009) recommends when assuring that organizational sustained efforts to keep active work environment, clarity of responsibilities and duties, and a positive way of communication will promote organizational readiness to implement retention planning frameworks [99] . Furthermore, and according to Hejase, Eid, Hamdar, and Haddad (2012a), “many Lebanese companies failed to identify their employees’ talents; they should start considering anyone working for their company as a talent and should invest in it” [108] (p. 31).

Sharabati, Jawad, & Bontis (2010) contend that the “concept of intellectual capital is a newly emerging concept, and until now, it is not fully understood by most organizations in Jordan or the Arab world” [109] (p. 117). Therefore, and as Hejase, Rifai, Tabsh, and Hejase (2012b) contend, “it is urgently recommended that strategically integrated human capital programs like talent management are to be adopted to capitalize on the new generation of better prepared future employees” [110] (p. 37).