Journal of Mathematical Finance

Vol.06 No.01(2016), Article ID:63372,6 pages

10.4236/jmf.2016.61003

Transfer Policies with Discontinuous Lorenz Curves

Johan Fellman

Hanken School of Economics, Helsinki, Finland

Copyright © 2016 by author and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 28 June 2015; accepted 2 February 2016; published 5 February 2016

ABSTRACT

In earlier papers, classes of transfer policies have been studied and maximal and minimal Lorenz curves  obtained. In addition, there are policies belonging to the class with given Gini indices or passing through given points in the

obtained. In addition, there are policies belonging to the class with given Gini indices or passing through given points in the  plane. In general, a transformation

plane. In general, a transformation  describing a realistic transfer policy has to be continuous. In this paper the results are generalized and the class of transfer policies

describing a realistic transfer policy has to be continuous. In this paper the results are generalized and the class of transfer policies  is modified so that the members may be discontinuous. If there is an optimal policy which Lorenz dominates all policies in the class, it must be continuous. The necessary and sufficient conditions under which a given differentiable Lorenz curve

is modified so that the members may be discontinuous. If there is an optimal policy which Lorenz dominates all policies in the class, it must be continuous. The necessary and sufficient conditions under which a given differentiable Lorenz curve  can be generated by a member of a given class of transfer policies are obtained. These conditions are equivalent to the condition that the transformed variable

can be generated by a member of a given class of transfer policies are obtained. These conditions are equivalent to the condition that the transformed variable  stochastically dominates the initial variable X. The theory presented is obviously applicable in connection with other income redistributive studies such that the discontinuity can be assumed. If the problem is reductions in taxation, then the reduction for a taxpayer can be considered as a new benefit. The class of transfer policies can also be used for comparisons between different transfer-raising situations.

stochastically dominates the initial variable X. The theory presented is obviously applicable in connection with other income redistributive studies such that the discontinuity can be assumed. If the problem is reductions in taxation, then the reduction for a taxpayer can be considered as a new benefit. The class of transfer policies can also be used for comparisons between different transfer-raising situations.

Keywords:

Lorenz Dominance, Stochastic Dominance, Tax Policy, Transfer Policy

1. Introduction

Lorenz curves were initially introduced for comparison and analysis of income distributions in a country in different times or in different countries in the same era. Later it has been widely applied in different contexts. Especially, classes of transfer and tax policies have been studied and maximal and minimal Lorenz curves  obtained. In addition, there are policies with given Gini indices or passing through given points in the

obtained. In addition, there are policies with given Gini indices or passing through given points in the  plane. Furthermore, the conditions (stochastic dominance) for attainable Lorenz curves have been obtained ([1] , [2] ). These findings have been found under the assumption that the transformation is continuous. In this paper we generalize the results for discontinuous transformations.

plane. Furthermore, the conditions (stochastic dominance) for attainable Lorenz curves have been obtained ([1] , [2] ). These findings have been found under the assumption that the transformation is continuous. In this paper we generalize the results for discontinuous transformations.

2. Notations

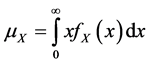

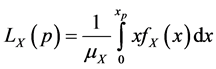

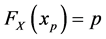

We use similar notations as in my previous papers. Let the income be X with the distribution function ,

,

density function , mean

, mean , and Lorenz curve

, and Lorenz curve . The basic formulae are

. The basic formulae are  and

and , where

, where .

.

We introduce the transformation , where

, where  is non-negative and monotone-increasing. Since the transformation can be considered as a tax or a transfer policy, the transformed variable Y is either the post-

is non-negative and monotone-increasing. Since the transformation can be considered as a tax or a transfer policy, the transformed variable Y is either the post-

tax or post-transfer income. The mean and the Lorenz curve for the variable Y are  and

and .

.

A general theorem concerning Lorenz dominance ( [3] [4] ) is:

Theorem 1. Let X be an arbitrary non-negative, random variable with the distribution , mean

, mean  and the Lorenz curve

and the Lorenz curve . Let

. Let  be a non-negative, monotone-increasing function, let

be a non-negative, monotone-increasing function, let  and let

and let  exist. The Lorenz curve

exist. The Lorenz curve  of Y exists and the following results hold:

of Y exists and the following results hold:

1)  if and only if

if and only if  is monotone-decreasing;

is monotone-decreasing;

2)  if and only if

if and only if  is constant;

is constant;

3)  if and only if

if and only if  is monotone-increasing.

is monotone-increasing.

3. Results

Classes of transfer policies. The class of transfer policies

H: (1)

(1)

where  is non-negative, monotone-increasing and continuous was introduced in ( [5] [6] ). This class was defined in order to compare policies yielding the same transfer effect. Now we modify this class of transfer policies and allow

is non-negative, monotone-increasing and continuous was introduced in ( [5] [6] ). This class was defined in order to compare policies yielding the same transfer effect. Now we modify this class of transfer policies and allow  to be discontinuous. Define

to be discontinuous. Define

H*:  (2)

(2)

where  is non-negative and monotone-increasing. If

is non-negative and monotone-increasing. If  is discontinuous, it can have only a countable number of positive finite steps ( [4] [6] ). A discontinuous transformation

is discontinuous, it can have only a countable number of positive finite steps ( [4] [6] ). A discontinuous transformation  is sketched in Figure 1.

is sketched in Figure 1.

If an optimal policy exists which Lorenz dominates all policies in H*, then according to Theorem 1, it must be continuous because  has to be monotonically and decreasing, but of every discontinuity point the ratio

has to be monotonically and decreasing, but of every discontinuity point the ratio

Figure 1. A sketch of a transformation  with a finite positive jump within the interval

with a finite positive jump within the interval  (c.f. [4] , Figure 1).

(c.f. [4] , Figure 1).

cannot be monotonically decreasing. The ratio

cannot be monotonically decreasing. The ratio  is outlined in Figure 2.

is outlined in Figure 2.

Consequently, although class (2), also contains discontinuous policies in comparison with initial class H, the policy

(3)

(3)

being optimal among all continuous policies, is still optimal, having the Lorenz curve

The inferior Lorenz curve can be obtained from the sequence [7]

(4)

(4)

These policies give no benefits to the poorest sector of the population ( ), but positive benefits to the richest (

), but positive benefits to the richest ( ). We construct the sequence so that HS Í H* and that their Lorenz curves converge towards an

). We construct the sequence so that HS Í H* and that their Lorenz curves converge towards an

inferior Lorenz curve. If we define  so that

so that , then every

, then every  is continuous

is continuous

and monotone increasing:  and

and . Hence, HS Í H* and the corresponding Lorenz curve is

. Hence, HS Í H* and the corresponding Lorenz curve is

(5)

(5)

where  ( [7] [8] ).

( [7] [8] ).

Assume that ,

,  and

and  are chosen so that

are chosen so that  for all

for all . Consider a sequence

. Consider a sequence , such that

, such that ,

,  and hence,

and hence, . We obtain the limit Lorenz curve [7]

. We obtain the limit Lorenz curve [7]

(6)

(6)

Figure 2. A sketch of the function  within the interval

within the interval  (c.f. [4] , Figure 3).

(c.f. [4] , Figure 3).

The Lorenz curve is inferior because we can prove [8] .

Theorem 2. The Lorenz curve  is inferior to the Lorenz curves for the whole class H*.

is inferior to the Lorenz curves for the whole class H*.

Proof. Consider an arbitrary, continuous or discontinuous policy  in H*. Using the condition

in H*. Using the condition , we can evaluate

, we can evaluate  in the following way:

in the following way:

(7)

(7)

This inequality holds for all . Consequently, the class H* of transfer policies containing discontinuous policies satisfies the same properties as the initial class discussed in [5] and [6] . Figure 3 includes a Lorenz curve with a cusp and the Lorenz curves

. Consequently, the class H* of transfer policies containing discontinuous policies satisfies the same properties as the initial class discussed in [5] and [6] . Figure 3 includes a Lorenz curve with a cusp and the Lorenz curves  and

and .

.

A policy with a given Lorenz curve. In Fellman [6] we obtained necessary and sufficient conditions under which a given differentiable Lorenz curve  can be generated by a member of a given class of transfer policies. These conditions are equivalent to the condition by which the transformed variable

can be generated by a member of a given class of transfer policies. These conditions are equivalent to the condition by which the transformed variable  stochastically dominates the initial variable X.

stochastically dominates the initial variable X.

Now we generalise the results, for discontinuous transformations as well. We have stressed above that  can only have a countable number of positive finite steps and that every jump in the transformation

can only have a countable number of positive finite steps and that every jump in the transformation  results in a cusp in the Lorenz curve.

results in a cusp in the Lorenz curve.

One has to assume that the Lorenz curve  considered is convex and that it is differentiable everywhere

considered is convex and that it is differentiable everywhere

with the exception of a countable number of cusps. The corresponding distribution , in which

, in which

is the inverse function to

is the inverse function to , with the mean

, with the mean  [5] . If

[5] . If  has a cusp, then the derivative

has a cusp, then the derivative  and the function

and the function  have jumps. The cumulative distribution functions are outlined in Figure 4.

have jumps. The cumulative distribution functions are outlined in Figure 4.

In general, when the Lorenz curve  and the mean are given, the corresponding income distribution is unique. Now we will prove that the conditions already obtained for classes of continuous transformations still hold for class H*; that is, we will characterise attainable Lorenz curves, although they are not universally differentiable.

and the mean are given, the corresponding income distribution is unique. Now we will prove that the conditions already obtained for classes of continuous transformations still hold for class H*; that is, we will characterise attainable Lorenz curves, although they are not universally differentiable.

The crucial part of this proof is to show that  still holds for the distribution

still holds for the distribution  [6] . The class H* of transfer policies containing discontinuous policies satisfies the same properties as the initial class dis-

[6] . The class H* of transfer policies containing discontinuous policies satisfies the same properties as the initial class dis-

cussed in [5] and [6] . Following [6] , we obtain the transformation . If

. If

has a cusp for , then

, then  has a jump for

has a jump for . The proof in [6] can be applied as such to

. The proof in [6] can be applied as such to  whenever it is continuous but the discontinuous points need special attention. Consider a neighbourhood

whenever it is continuous but the discontinuous points need special attention. Consider a neighbourhood

, where

, where  is the only discontinuity point of

is the only discontinuity point of  in the interval

in the interval  and

and

choose a δ > 0 so small that . Let

. Let  and

and .

.

Figure 3. A sketch of the Lorenz curves  and

and , when

, when  is discontinuous for

is discontinuous for  and

and . Note the cusp of

. Note the cusp of  at the point

at the point . The figure also includes the maximum and minimum Lorenz curves

. The figure also includes the maximum and minimum Lorenz curves  and

and  for the transfer policies in H*.

for the transfer policies in H*.

Figure 4. Sketch of cumulative distribution function for X and . Note the stochastic dominance

. Note the stochastic dominance  for all p and the jump in the distribution function

for all p and the jump in the distribution function  for q.

for q.

Now, the transformation  is continuous for all

is continuous for all , and

, and . When

. When

, the inequality holds for the limits and we obtain

, the inequality holds for the limits and we obtain . Similarly, we obtain

. Similarly, we obtain

and, when

and, when , the inequality holds for the limits and we obtain

, the inequality holds for the limits and we obtain

. Hence,

. Hence,  for all p, and

for all p, and  stochastically dominates the initial variable X.

stochastically dominates the initial variable X.

4. Discussion

We have studied the effects of transfer policies in this paper. In general, a transformation describing a realistic transfer policy has to be continuous. However, the theory presented is obviously applicable in connection with other income redistributive studies such that the discontinuity cannot be excluded. If the problem is reductions in taxation, then the tax reduction for a taxpayer can be considered as a new benefit [7] . The class of transfer policies H* can consequently be used for comparisons between different tax-reducing policies. If changes of transfers are of interest, then the transfer policies can also be applied in transfer-raising situations. If transfers are increased, the effect of increases on a receiver can be considered through transfer policies belonging to H*. In general, the changes may be mixtures of several different components and discontinuity cannot be excluded. The continuity assumption can be dropped and the class H* of transfer policies containing discontinuous policies satisfies the same properties as the initial class discussed in ( [5] [6] ). Analogously, tax increases and transfer reductions can be considered as new tax policies [7] . One main result is still that continuity is a necessary condition if one pursues the notion that income inequality should remain or be reduced.

Empirical applications of the optimal policies among a class of tax policies and the class of transfer policies considered here have been discussed in ( [2] [9] ), where we developed “optimal yardsticks” to gauge the effectiveness of given real tax and transfer policies in reducing inequality.

5. Conclusion

We have studied the effects of discontinuous transfer policies. The theory presented is applicable in connection with income redistributive studies such that the discontinuity cannot be excluded. A tax reduction for a taxpayer or a transfer increase on a receiver can be considered as new benefits. In general, such changes may be mixtures of different policy components and discontinuity cannot be excluded. However, one main result is still that continuity is a necessary condition if income inequality should remain or be reduced.

Acknowledgements

This work was supported in part by a grant from the Magnus Ehrnrooths Stiftelse foundation.

Cite this paper

JohanFellman, (2016) Transfer Policies with Discontinuous Lorenz Curves. Journal of Mathematical Finance,06,28-33. doi: 10.4236/jmf.2016.61003

References

- 1. Fellman, J. (2013) Properties of Non-Differentiable Tax Policies. Theoretical Economics Letters, 3, 142-145.

http://dx.doi.org/10.4236/tel.2013.33022 - 2. Fellman, J. (2014) Mathematical Analysis of Distribution and Redistribution of Income. Science Publishing Group, 166 p.

http://www.sciencepublishinggroup.com/book/B-978-1-940366-25-8.aspx - 3. Jakobsson, U. (1976) On the Measurement of the Degree of Progression. Journal of Public Economics, 5, 161-169.

http://dx.doi.org/10.1016/0047-2727(76)90066-9 - 4. Fellman, J. (2009) Discontinuous Transformations, Lorenz Curves and Transfer Policies. Social Choice and Welfare, 33, 335-342.

http://dx.doi.org/10.1007/s00355-008-0362-4 - 5. Fellman, J. (1980) Transformations and Lorenz Curve. Swedish School of Economics and Business Administration Working Paper 49, 19 p.

- 6. Fellman, J. (2003) On Lorenz Curves Generated by a Given Class of Transfer Policies. In: Höglund, R., Jäntti, M. and Rosenqvist, G., Eds., Statistics, Econometrics and Society: Essays in Honour of Leif Nordberg, Statistics Finland, Research Reports Number 239, 27-40.

- 7. Fellman, J. (2001) Mathematical Properties of Classes of Income Redistributive Policies. European Journal of Political Economy, 17, 195-209.

http://dx.doi.org/10.1016/S0176-2680(00)00035-5 - 8. Fellman, J. (1995) Intrinsic Mathematical Properties of Classes of Income Redistributive Policies. Working Papers, No. 306, Hanken School of Economics, Helsinki, 26 p.

- 9. Fellman, J., Jäntti, M. and Lambert, P.J. (1999) Optimal Tax-Transfer Systems and Redistributive Policy. Scandinavian Journal of Economics, 101, 115-126.

http://dx.doi.org/10.1111/1467-9442.00144