American Journal of Operations Research

Vol.05 No.06(2015), Article ID:60989,12 pages

10.4236/ajor.2015.56040

When to Sell an Asset Where Its Drift Drops from a High Value to a Smaller One

Pham Van Khanh

Institute of Economics and Corporate Group, Hanoi, Vietnam

Copyright © 2015 by author and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

Received 28 June 2015; accepted 8 November 2015; published 11 November 2015

ABSTRACT

To solve the selling problem which is resembled to the buying problem in [1] , in this paper we solve the problem of determining the optimal time to sell a property in a location the drift of the asset drops from a high value to a smaller one at some random change-point. This change-point is not directly observable for the investor, but it is partially observable in the sense that it coincides with one of the jump times of some exogenous Poisson process representing external shocks, and these jump times are assumed to be observable. The asset price is modeled as a geometric Brownian motion with a drift that initially exceeds the discount rate, but with the opposite relation after an unobservable and exponentially distributed time and thus, we model the drift as a two-state Markov chain. Using filtering and martingale techniques, stochastic analysis transform measurement, we reduce the problem to a one-dimensional optimal stopping problem. We also establish the optimal boundary at which the investor should liquidate the asset when the price process hit the boundary at first time.

Keywords:

Optimal Stopping Time, Posterior Probability, Threshold, Markov Chain, Jump Times, Martingale, Brownian Motion

1. Introduction

In this paper we consider the following problem: How to find the optimal stopping time to sell a stock (or an asset) when the expected return of a stock is assumed to be a constant larger than the discount rate up until some random, and unobservable, time τ, at which it drops to a constant smaller than the discount rate.

An investor wants to hold the position as long as the inertia is present by taking advantage of the drift which is exceeding the discounted rate (or interest rate). On the other hand, when the inertia disappears the investor would like to exit the position by selling the asset.

The under study problem in this paper was also addressed in [1] where the buying problem with the same assumption was solved. The results of [1] showed that the optimal buying time was the first passage time over some unknown level for the a posteriori probability process

defined below and by simulating it was found that the optimal time to buy an asset was the time which the asset price process had just passed the trough.

defined below and by simulating it was found that the optimal time to buy an asset was the time which the asset price process had just passed the trough.

The author of [2] studied a problem of finding an optimal stopping strategy to liquidate an asset with unknown drift; more exactly he wanted to find the best time to sell a stock when its drift was a discrete random variable which took the given values. The first time the posterior mean of the drift passes below a non-decreasing boundary that is the unique solution of a particular integral equation is shown to be optimal.

Some classical optimal stopping time problem has been considered in [3] . These are applied in mathematical finance but these are basic problem, and it is difficult to apply in real world.

For related studies of stock selling problems, see [4] [5] and for studies of basic optimal stopping problems see [3] . The method we use to study in this paper is the martingale theory, the transformation theory of measuring and the optimal stopping time is referenced in the literature [3] [6] [7] .

In this paper, the asset price is modeled as a linear Brownian motion with a drift that drops from one constant to a smaller constant at some unobservable time. This drift is modeled as a Markov chain with two states which are denoted by 0 and 1 where 0 is denoted for price decrease and 1 is denoted for price increase.

We define the asset price model in Section 2, and the optimal selling problem is set up. In Section 3, we study the simulation to examine our studies and finally, Section 4 is conclusion.

2. The Model

We take as given a complete probability space . On this probability space, let the change-point τ be a random variable with distribution

. On this probability space, let the change-point τ be a random variable with distribution

where λ is the intensity of the transition from state 1 to state 0 and assume that λ is positive and that belongs to [0; 1). Denote the drift of the price process at, t ≥ 0, can be modeled as a Markov chain with two states al denoted by state 0 and ah denoted by state 1 such that ;

;

at time 0, al < r < ah where r is discounted rate which is a given constant and process at, t ≥ 0 can only transit from state 1 to state 0

at time 0, al < r < ah where r is discounted rate which is a given constant and process at, t ≥ 0 can only transit from state 1 to state 0

with transition density matrix as follows

Next, let W be a Brownian motion which is indepen-

Next, let W be a Brownian motion which is indepen-

dent of τ. The asset price process X is modeled by a geometric Brownian motion with a drift that drops from ah to al at time τ. More precisely,

and , where

, where

i.e.

i.e.

if

if

and

and

if

if

the volatility

the volatility

is a constant.

is a constant.

At the time of

we define the a posteriori probability process

we define the a posteriori probability process

by

by

where

is a filter generated by X and τ. The process

is a filter generated by X and τ. The process

indicate the probability of event that the price process decreases. We consider the optimal stopping problem:

indicate the probability of event that the price process decreases. We consider the optimal stopping problem:

Find

-stopping time

-stopping time

such that:

such that:

(2.1)

(2.1)

Similar the buying problem, posterior probability process

satisfying the following stochastic differential (see theorem 9.1, [6] ):

satisfying the following stochastic differential (see theorem 9.1, [6] ):

or

where

is a P-Brownian motion with respect to

is a P-Brownian motion with respect to

given by

given by

Moreover, in terms of

we have

we have

Processes

and

and

satisfy the following system equations:

satisfy the following system equations:

Put

and Ito’s formula gives that:

and Ito’s formula gives that:

We define new process

as follow:

as follow:

and a new measure

satisfying:

satisfying:

By Girsanov theorem,

is a

is a

-Brownian motion. Furthermore,

-Brownian motion. Furthermore,

where

.

.

The price process

satisfying the following stochastic differential

satisfying the following stochastic differential

or in term of

The solution of this stochastic equation is

Now we consider the process:

then

is a

is a

-martingale and

-martingale and

where

where

Let

is a process which defined by

is a process which defined by , we have

, we have

Put

and according to Itô’s formula:

and according to Itô’s formula:

From this we have

(a.s.), thus:

(a.s.), thus:

Denote

then

To solve the problem (2.1) we solve the following auxiliary problem:

(2.2)

(2.2)

Put

The optimal stopping time is the first hitting time of the process

to the area

to the area

with some B. Moreover pairs

with some B. Moreover pairs

satisfying the flowing free boundary problem:

satisfying the flowing free boundary problem:

(2.3)

(2.3)

where

is infinitesimal generated operator.

is infinitesimal generated operator.

Differential equation in (2.3) has the general solution as follows:

where

where

Changing variables and using some analytic transformations we obtain:

then

and

and

We also have

as

since

since

and

and

We have

since

therefore

therefore

and

and

is an increasing function.

is an increasing function.

Moreover

since

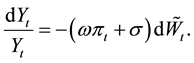

These mean that the function

is increasing and convex on

is increasing and convex on .

.

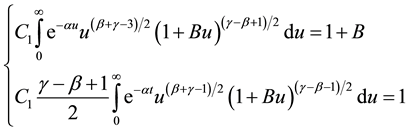

Figure 1 shows the graph of function , we can check the increase and convex properties of it. The graph of

, we can check the increase and convex properties of it. The graph of

is shown in Figure 2, we can see that it tends to infinite when z as 0+.

is shown in Figure 2, we can see that it tends to infinite when z as 0+.

But

therefore

therefore

and

and

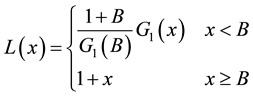

According to (2.3) we have

Figure 1. Graph of the function .

.

Figure 2. Graph of the function .

.

So B is the solution of the following equation:

(2.4)

(2.4)

Lemma 2.1. The free boundary Equation (2.4) has unique positive solution B.

Proof: The Equation (2.4) is equivalent to

Denote:

The graph of

is shown in Figure 3. We shall prove that the function

is shown in Figure 3. We shall prove that the function

satisfying

satisfying ,

,

and

and

is decreasing and therefore the equation

is decreasing and therefore the equation

has unique solution on

has unique solution on .

.

We have

Figure 3. Graph of the function .

.

It follows that

Because

and

we obtain

We will prove that . Indeed, with the large enough x we have

. Indeed, with the large enough x we have

so

so

since

Consequently,

and

and

is decreasing so the equation

is decreasing so the equation

has unique

has unique

solution on . The theorem is proved.

. The theorem is proved.

Theorem 2.2. Stopping time

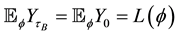

is the optimal stopping time for (2.1).

is the optimal stopping time for (2.1).

Proof: Let

and we will prove that

, indeed

, indeed

Now, we examine the function

Take the derivative we obtain

This follows

.

.

Using the Dynkin’s formula to the process

we have:

we have:

.

.

Because B satisfying

so the drift of Y is positive and therefore Y is super martingale and

so the drift of Y is positive and therefore Y is super martingale and

is martingale. By optional theorem we have:

is martingale. By optional theorem we have:

.

.

By

we have

we have

moreover

moreover

. So

. So .

.

We will show that B satisfy the condition: . Indeed, by general optimal stopping theory all points satisfy the form

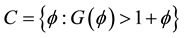

. Indeed, by general optimal stopping theory all points satisfy the form

with positive value will be in continuation area

.

.

The optimal stopping time is the first hitting time of

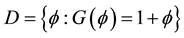

to the area:

to the area:

or

or

Thus function G satisfy the following condition:

.

.

We define the function:

Now, we assume , because

, because

is a decreasing function so

is a decreasing function so . Then the left derivative of

. Then the left derivative of

. Specially,

. Specially,

with some

with some . This follows

. This follows

is super martingale and

is super martingale and

martingale. For the stopping time

martingale. For the stopping time

satisfying

satisfying

we have:

we have:

.

.

This contradicts to the existence of

such that

such that

when

when

. Finally, we achieve

. Finally, we achieve .

.

The optimal stopping time

is the first hitting time of

is the first hitting time of

to the area

to the area

.

.

But

therefore

therefore

,

,

by this, we have finished the provement.

3. Simulation Study

To make visual for the above theory we simulate the asset price process, the posterior probability process

process

(notice that

(notice that

is an increasing function of

is an increasing function of ) and the selling threshold B. Some

) and the selling threshold B. Some

parameters is used in our simulating are ;

; ;

; ;

; ;

;

and the time interval is [0, 1].

and the time interval is [0, 1].

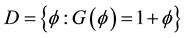

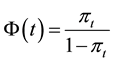

As can be seen in the figures from 4 to 8 if the price is increasing then the

and

and

are decreasing and conversely.

are decreasing and conversely.

Figure 4 shows the price process has increased since the time 0.2 so the

decreased from the respective time and it can not hit the red line denoted the threshold, therefore the optimal selling time in this case is 1.

decreased from the respective time and it can not hit the red line denoted the threshold, therefore the optimal selling time in this case is 1.

Figure 5 simulate a price process which is fluctuated from time 0 to 0.14 and decrease dramatically at the time 0.14 so the process

increase sharply from this and crossover the threshold, it follows that the optimal time to liquidate the asset is about 0.17. At this time the price of the asset is lower than the origin but if we hold it we will sell it at a much more loss in the future.

increase sharply from this and crossover the threshold, it follows that the optimal time to liquidate the asset is about 0.17. At this time the price of the asset is lower than the origin but if we hold it we will sell it at a much more loss in the future.

Another simulation is shown in Figure 6. Clearly, whenever the price process is increasing, the

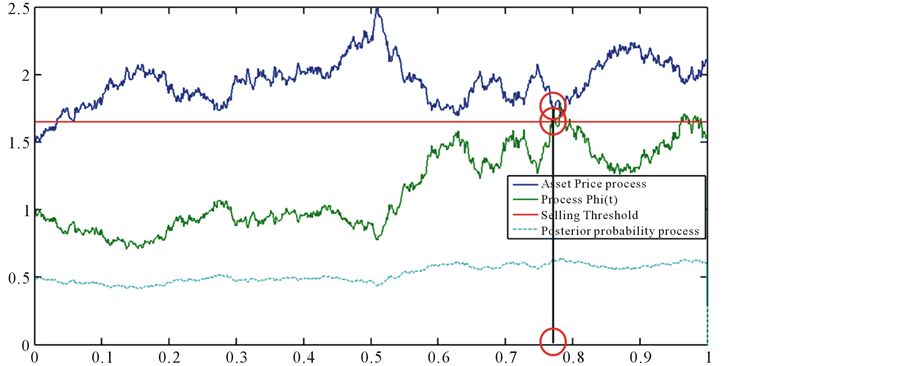

and the posterior probability process are decreasing and the liquidated time is 0.77. At this time the price is not the highest but it is significantly higher than the original value which is 1.5.

and the posterior probability process are decreasing and the liquidated time is 0.77. At this time the price is not the highest but it is significantly higher than the original value which is 1.5.

Figure 4. A simulation of asset price process, the posterior probability process, process Φ(t), the threshold probability and the optimal stopping time. In this case, the process Φ(t) always under the threshold probability so the optimal stopping time is the final time 1.

Figure 5. A simulation of asset price process, the posterior probability process, process Φ(t), the threshold probability and the optimal stopping time. In this case, the first time that the process Φ(t) over passes the threshold probability at the time 0.17 so the optimal stopping time is 0.17.

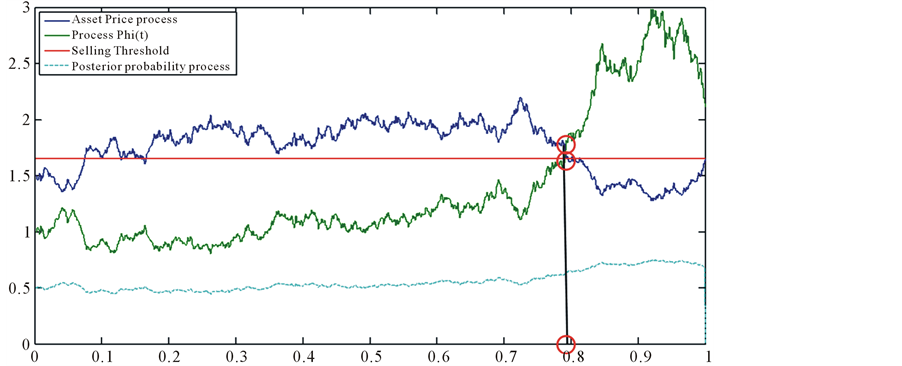

In Figure 7, we can see the same scenario with the simulation in Figure 6. The time to liquidate in this case is 0.795, the price is about 1.75 whereas the started price was 1.5. We can see

it means that we benefit by this trade affair.

it means that we benefit by this trade affair.

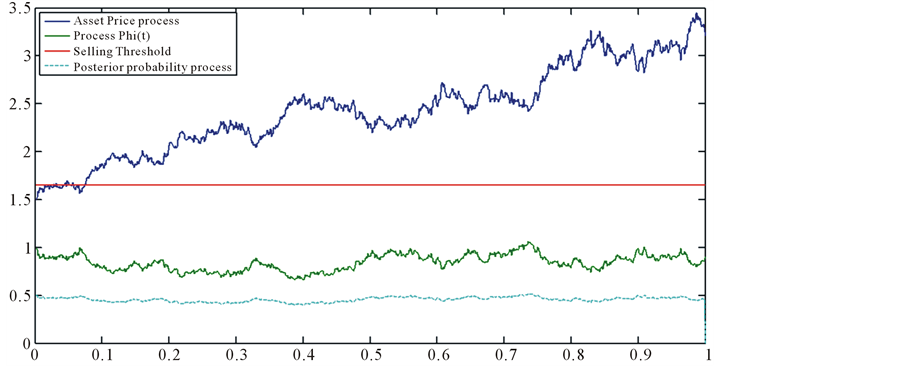

The same scenario with the simulation in Figure 1, the simulation results in Figure 8 show the price illustrates an uptrend from time 0 to the end that the process

can not pass over the selling threshold B, consequently, the optimal time to sell in this situation is 1.

can not pass over the selling threshold B, consequently, the optimal time to sell in this situation is 1.

4. Conclusion

This research considers the problem of how to find the optimal time to liquidate an asset when the asset price is modeled by the geometric Brownian motion which has a change point. In particular, the drift of the process drops from a high value to a smaller one and this drift process can be modeled as two-state Markov process. The results of this research indicate that a optimal selling decision is made when the probability of downtrend surpassed some certain threshold. We also simulate the price process with a number of parameters and conduct

Figure 6. A simulation of asset price process, the posterior probability process, process Φ(t), the threshold probability and the optimal stopping time. In this case, the first time that the process Φ(t) over passes the threshold probability at the time 0.77 so the optimal stopping time is 0.77.

Figure 7. A simulation of asset price process, the posterior probability process, process Φ(t), the threshold probability and the optimal stopping time. In this case, the first time that the process Φ(t) over passes the threshold probability at the time 0.795 so the optimal stopping time is 0.795.

Figure 8. A simulation of asset price process, the posterior probability process, process Φ(t), the threshold probability and the optimal stopping time. In this case, the process Φ(t) always under the threshold probability so the optimal stopping time is the final time 1, the same with the case in Figure 4.

numerical solution to the experimental selling threshold. In next studies, we will consider problems in which the price growth rate is a Markov process which has more than 2 states and establish some properties as well as distribution of stopping time.

Acknowledgements

This research is funded by Vietnam National Foundation for Science and Technology Development (NAFOSTED) under grant number 10103-2012.17.

Cite this paper

PhamVan Khanh, (2015) When to Sell an Asset Where Its Drift Drops from a High Value to a Smaller One. American Journal of Operations Research,05,514-525. doi: 10.4236/ajor.2015.56040

References

- 1. Khanh, P. (2014) Optimal Stopping Time to Buy an Asset When Growth Rate Is a Two-State Markov Chain. American Journal of Operations Research, 4, 132-141.

http://dx.doi.org/10.4236/ajor.2014.43013 - 2. Khanh, P. (2012) Optimal Stopping Time for Holding an Asset. American Journal of Operations Research, 4, 527-535.

http://dx.doi.org/10.4236/ajor.2012.24062 - 3. Peskir, G. and Shiryaev, A.N. (2006) Optimal Stopping and Free-Boundary Problems (Lectures in Mathematics ETH Lectures in Mathematics. ETH Zürich (Closed)). Birkhäuser, Basel.

- 4. Shiryaev, A.N., Xu, Z. and Zhou, X.Y. (2008) Thou Shalt Buy and Hold. Quantitative Finance, 8, 765-776.

http://dx.doi.org/10.1080/14697680802563732 - 5. Guo, X. and Zhang, Q. (2005) Optimal Selling Rules in a Regime Switching Model. IEEE Transactions on Automatic Control, 9, 1450-1455.

http://dx.doi.org/10.1109/TAC.2005.854657 - 6. Lipster, R.S. and Shiryaev, A.N. (2001) Statistics of Random Process: I. General Theory. Springer-Verlag, Berlin, Heidelberg.

- 7. Shiryaev, A.N. (1978) Optimal Stopping Rules. Springer Verlag, Berlin, Heidelberg.