G. D. HANCOCK

Table 2.

Portfolio identities.

Symbol Description

Portfolio #1, p1 75% NASDAQ/25% VXN

Portfolio #2, p2 75% NASDAQ/25% VIX

Portfolio #3, p3 75% S & P500/25% VIX

Portfolio #4, p4 75% S & P500/25% VXN

Portfolio #5, p5 75% DJIA/25% VXD

Portfolio #6, p6 75% DJIA/25% VIX

Portfolio #7, p7 75% Russell/25% RVX

Portfolio #8, p8 75% Russell/ 25% VIX

with the implied volatility of a dissimilar equity index. It is

expected that hedging with matching volatility, as with the

natural portfolios, will outperform hedging with disparate vola-

tility, as with the constructed portfolios.

The risk-adjusted returns (RAR) of the natural portfolios

(odd numbered) are compared to the performance of the con-

structed portfolios (even numbered). When the performance of

the natural portfolio is greater than the corresponding con-

structed portfolio the conclusion is that the matched volatility

fills a unique need.

Specifically, the risk-adjusted return (RAR) is defined by

Equation (1) below and applied to each of the 8 portfolios:

,,,

tptp

RAR Rt

(1)

The portfolio returns and standard deviations are obtained as

follows:

,,

0.750.25 ,

tctvt

xR xR (2)

12

22 22

,,,,,,

0.750.2520.75 0.25

ptctvtctvt ct vt

xxxxxxx

(3)

The variables are defined as:

,

t

AR = The risk-adjusted return of the portfolio on the tth

day;

,ct

= The return on the cash index on the tth day;

,vt

= The return on the volatility index on the tth day;

,ct

= The standard deviation of returns for the cash index

over the tth time period;

,vt

= The standard deviation of returns for the volatility

index over the tth time period; and,

,ctvt

= The correlation of returns between the cash index

and the volatility index over the tth time period.

A second series of tests are performed to verify the robust-

ness of the RAR test results. This test is a simple linear regres-

sion, shown in Equation (4), designed to determine the amount

of variation in the cash index explained by volatility.

,01,2,3,4,c tvxdtrvx tvxn tvix tt

RbRbRbxRbxR

(4)

where:

,vxd t

= the return on the DJIA volatility index on day t;

,rvxt

= the return on the Russell-2000 volatility index on

day t;

,vxn t

= the return on the NASDAQ-100 volatility index on

day t;

,vix t

= the return on the S & P 500 volatility index on day t.

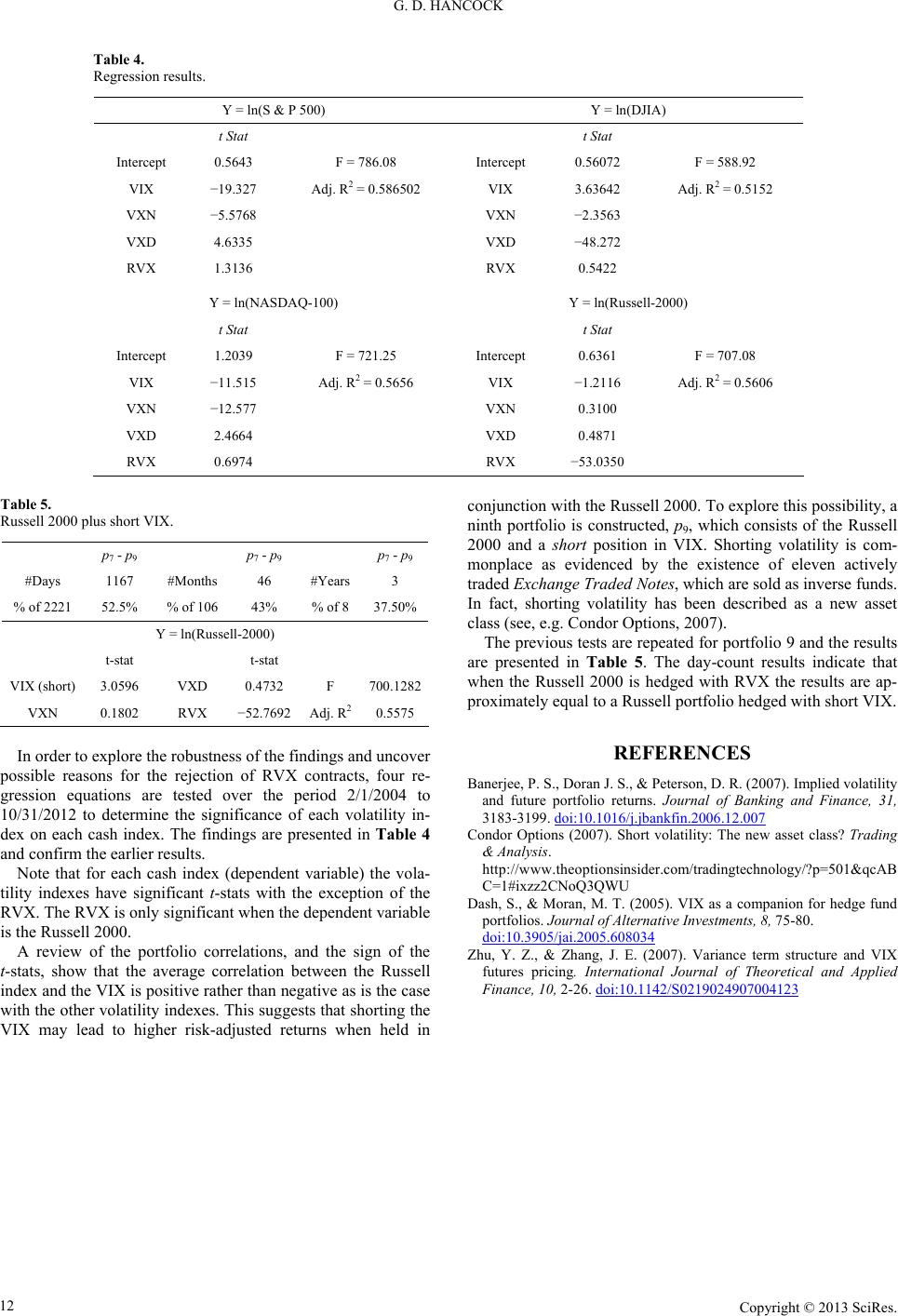

Results

Table 3 is presented as the difference between each natural

portfolio’s RAR and the corresponding RAR for the constructed

portfolio.

The first column, of the day-count results, indicates that in

49.5% of the days evaluated, the NASDAQ plus VIX portfolio

(p2) outperforms the NASDAQ plus VXN portfolio (p1). The

month-count and year-count results confirm that portfolio #1

and #2 perform almost equally over time.

The S & P 500 portfolios are shown in the second column of

the results presented in Table 3. Since the S & P natural portfo-

lio (p3) includes VIX, the comparison portfolio (p4) is com-

prised of the S & P 500 plus VXN. All three time counting

schemes indicate that the performance of the two portfolios is

approximately the same. Slightly different results are reported

for the DJIA portfolios. According to the day-count, the per-

formance of the natural DJIA portfolio is equal to the con-

structed portfolio. However, the month-count and year-count

results suggest that the natural portfolio (p5) more frequently

out performs the VIX hedged portfolio (p6).

Finally, the Russell-2000 portfolio findings diverge dramati-

cally from the others. According to all three time measures, the

natural portfolio (p7) almost always outperforms the con-

structed portfolio (p8) which suggests that option or futures

contracts offered on RVX should fill a unique need that cannot

be met using VIX. No so for the VXN and the VXD contracts

which appear to be mostly redundant and have, therefore, been

rejected by the market. Yet, the market has also rejected con-

tracts on the unique RVX.

All of the portfolio combinations produce smaller differences

in performance as the holding period is lengthened. This is

most likely a result of the well-documented mean reverting

behavior of volatility indexes (see, for e.g., Dash and Moran,

2005), Zhu and Zhang (2007) and Banerjee, Doran and Peter-

son (2007). It is the mean reversion tendency that explains at

least one of the reasons that sponsors of volatility products

recommend a very short holding period. Given the pricing be-

havior of volatility products and the recommendation of the

sponsors, more weight should be placed on the one-day results.

The monthly and annual results are best viewed as robustness

tests since, under no circumstances, are volatility products

recommended for long-term investment purposes.

Table 3.

Differences between portfolio RAR.

Count if <0 (Day-Count)

p1 - p2 p3 - p4 p5 - p6 p7 - p8

#Days 1460 1464 1493 236

%of 2950 49.50% 49.60% 50.60% 10.60%

Count if <0 (Month-Count)

p1 - p2 p3 - p4 p5 - p6 p7 - p8

#Months 66 68 57 0

% of 141 48.50% 50% 42% 0%

Count if <0 (Year-Count)

p1 - p2 p3 - p4 p5 - p6 p7 - p8

#Years 6 7 4 0

% of 12 50.00% 58% 33% 0%

Copyright © 2013 SciRes. 11