F. ASGHARI ET AL.

Copyright © 2013 SciRes. 117

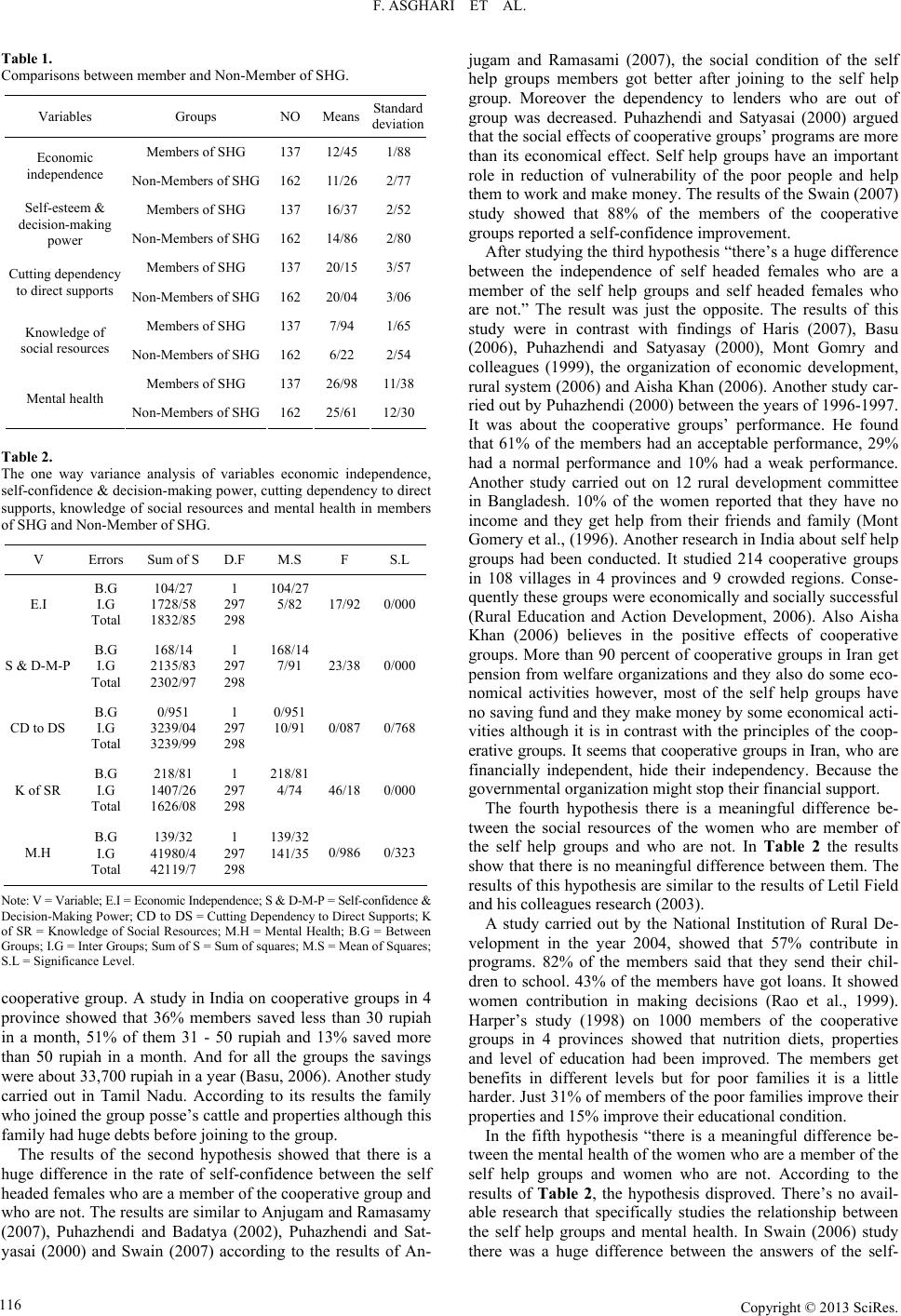

help group and control group. 88% of the respondents reported

a increased rate of reliance after joining to the group. And they

feel more positive changes in expressing their opinion. Basu

and Vastava (2010) regard the increased rate of self-respect and

welfare as the effects of the cooperative groups.

The results of the Meyer and Tankha (2002) show that the

positive effects of the self help groups on the members are:

self-confidence, communication skills, participation in social

oppositions, logical responses to problems and reduction of

aggression. Poverty reveals the story of women and their pres-

sures and endeavors. Poverty causes low self-confidence, pres-

sure and dependency and limit capacities and participation in

self help groups leads to a change. Women show the “feeling of

freedom”, increase their self-respect and self-confidence, their

understandings change and the feeling of power and motion

have its roots in limita tion and force.

We should pay attention that where the mental health of the

women is not normal. It helps to choose the women for the self

help groups. women who are under pressure because of differ-

ent reasons such as death of husband, disease, husbands break-

down, disease of other members of the family, poverty and

financial problems, lack of control in life, lack of basic skills,

lack of social and family support, feeling of loneliness, absence

of sufficient mental and physical services and absence of psy-

chologists and chronic mental and physical disease.

REFERENCES

Aisha Khan (2006). Women self-help groups in Andhra Pradesh. Pov-

erty to prosperity. Self-help groups: Use of modified roscas in micro-

finance. First draft.

Anjugam, M., & Rasmamy, C. (2007). Determinants of women’s par-

ticipation in self-help group (SHG)-Led Microfinance Programme in

Tamil Nado. The IDEAS, 20.

Baland, J. M., Somanathan, R., & Vandewal, L. (2008) Microfinance life

spans: A study of attrition and exclusion in self-help groups in India.

The IDEAS, 4, 159-210.

Basu, P. (2006). Microfinance and women empowerment—An empiri-

cal study with special to West Bengal. West Bangal: Ruje Peary Mo-

han College.

Basu, P., & Srivastava, P. ( 2010). Scaling-up microfinance for India’s

rural poor. Washington DC: World Bank Policy Research Working

Paper 3646.

Goldberg, D. P. (1972). The detection of psychiatric illness by ques-

tionnaire. London: Oxford University Press.

Goldberg, D. P., & Hillier, V. F. (1979). A scaled version of general

health questionnair e. Psychological Medicine, 9, 131-145.

doi:10.1017/S0033291700021644

Gibbons, P., Arevalo, H. F., & Monico, M. (2004). Assessing of the

factor structure and reliability of the 28 item versions of the General

Health Questionnaire (GHQ-28) in Salvador. International Journal

of Clinical Health Psychology, 4 , 389-398.

Harris, S. (2004). State of t h e M i c ro c r e d i t S um m i t C a m p ai g n Report.

Harper, M. (1998). Profit for the poor—Cases in microfinance. New

Delhi: Oxford and IBH Publishing Co., Ltd.

Israel, B. A., Checkoway, B., Schulz, A., & Zimmerman, M. (1994).

Health education and community empowerment: Conceptualizing and

measuring perceptions of individual, organizational and community

control. Health Education Quarte r ly , 21, 149-169.

doi:10.1177/109019819402100203

Kabeer, N. (2001). Conflicts over credit: Re-evaluating the empower-

ment potential of loans to women in rural Bangladesh. World De vel-

opment, 29, 63-84. doi:10.1016/S0305-750X(00)00081-4

Kabeer, N. (1999). Resources, agency, and achievements: Reflections

on the measurement of women’s empowerment. Development and

Change, 30, 435- 464. doi:10.1111/1467-7660.00125

Mayoux, L. (2000). Micro credit and the empowerment of women: A

review of the key issues. Social Finance Unit Working Paper, Gene-

va.

Mont, G. R., Bhattacharya, D., & Hulme, D. (1996). Credit for the poor

in Bangladesh. In D. Hulme, & P. Moseley (Eds.), Finance against

poverty. London: Rutledge.

NABARD (2006). National bank for agriculture and rural development.

Annual Report, 2005-2006 . Mumbai.

www.nabard.org, 2006

Palahang, H. (1997). Epidemiology of mental health in kashan urban

area. Thesis of Masters, Tehran: Iran Medical University.

Power, M. (2004). Social provisioning as a starting point for feminist

economics. Feminist Economics, 10, 3-19.

doi:10.1080/1354570042000267608

Puhazhendi, V., & Badatya, K. C. (2002). Shg-bank linkage program-

me for rural poor—An impact assessment. New Delhi: SHG-Bank

Linkage Programm e S eminar.

Puhazhendi, V., & Satyasai, K. J. S. (2000). Microfinance for Rural

People: An Impact Evaluation. Study Report, Mumbai: Nabard.

Rappaport, J. (1984). Studies in empowerment: Introduction to the issue.

Prevention in Human Services, 3, 1-7.

Rao, D. S. R. P., Satish, G. S., & Chauhan, D. S. (1999). Study or shgs

as financial intervie d i aries. Working Paper No. 15, New Delhi.

Rao, S. (2008). Reforms with a female face: Gender, liberalization, and

economic policy in Andhra Pradesh, India. World Development, 36,

1213-1232. doi:10.1016/j.worlddev.2007.06.020

Sen, A. K. (1990). Gender and cooperative conflicts. In I. Tinker (Ed.), Per-

sistent inequalities (pp. 123-149). New York: Oxford University Press.

Sen, A. (1999). Developme nt as f re e d om. New York: Alfred A Knopf.

Swain, B. S. (2006). Can microfinance empower women? Self-help groups

in India. Ada Dialogue, 37 , 37-42.

Simanowitz, A., & Walker, A. (2002). Ensuring impact: Reaching the

poorest while building financially self-sufficient institutions, and

showing improvement in the lives of the poorest women and their

families. URL (last checked 10-13 Novemb er 2002 ).

http://www.microcreditsummit.org/papers/papers.html/

Tamkha, A. (2002). Self-help groups as financial Intermediaries in India

cost of promotion, sustainability and impact. New Delhi: Sa-Dhan.

Umashankar, D. (2006). Women’s empowerment: Effect of participa-

tion in self-help groups. Dissertation Submitted in Partial Fulfill-

ments of Requirements for the Post Graduate Program in Public Pol-

icy and Management. Indi an Institute of Management Bangalore.

Yaghobi, H., Ghaedi, G., Omidi, A., Kehani, S., & Masood, Z. (2008).

Primary study of reliability and determination of GHQ-12 and GHQ-

28 on students of Shahed University. Shiraz: Seminar on Mental Health

of Students.

Zamman, H. (2001). Assessing the Poverty and Vulnerability Impact of

Microcrediting Bangladesh: A Case Study of BRAC. World Devel-

opment Report 2000-200 1, Washington DC: Wor ld Bank.

Zimmerman, M., Israel, B., Schulz, A., & Checkoway, B. (1992). Fur-

ther explorations in empowerment theory: An empirical analysis of

psychological empowerment. American Journal of Community Psy-

chology, 20, 707-727.

Zimmerman, M. (1995). Psychological empowerment: Issues and illus-

trations. American Journal of Community Psycho logy , 23, 581-599.