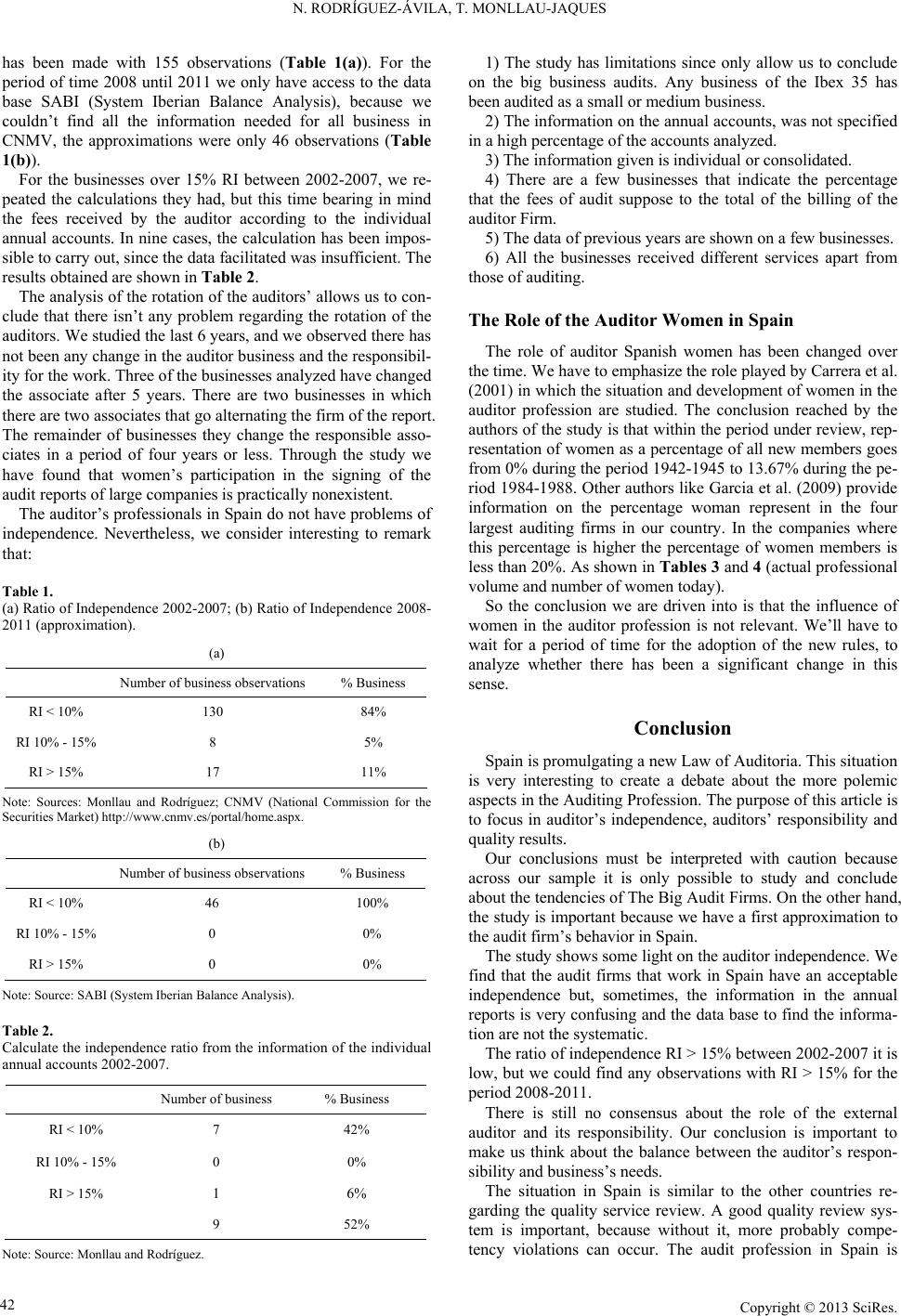

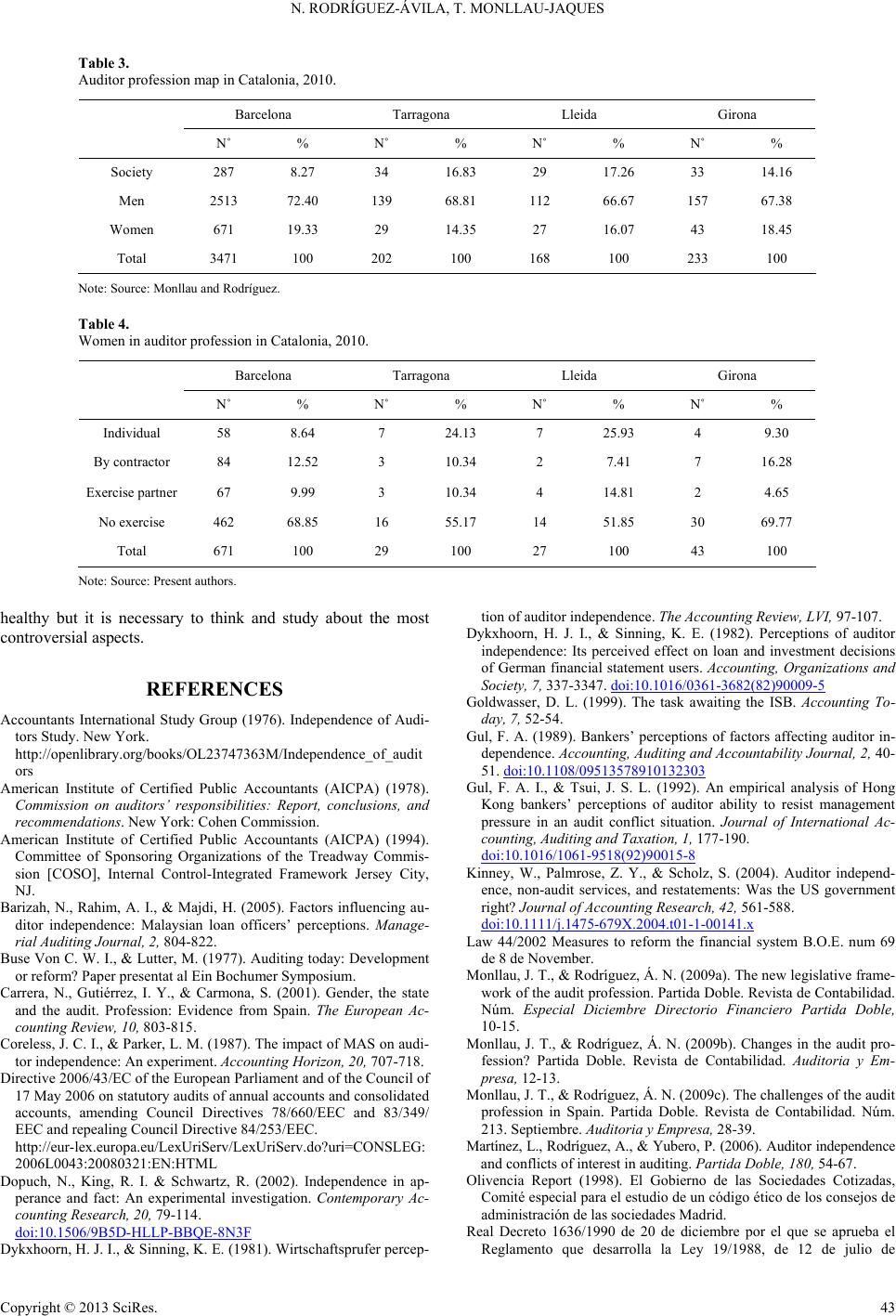

N. RODRÍGUEZ-ÁVILA, T. MONLLAU-JAQUES

make well founded opinions. Legislators say that providing

certain non-audit services increase the likelihood of financial

reporting that violates generally accepted accounting principles.

Some authors say that non-audit services can be negatively as-

sociated with restatements because non-audit services increase

the information available for the auditor (Goldwasser, 1999;

The Panel on Audit Effectiveness, 2002; Dopuch et al., 2003).

Other studies found a positive relationship between non-audit

services and the auditor’s objectivity (Goldwasser, 1999; the

Panel of Audit Effectiveness, 2002; Dopuch et al., 2003). Fi-

nally, there are studies that have shown that the provision of

non-audit services has no effect on auditor independence (Gul,

1989; Coreless & Parker, 1987).

Analyzing the situation it’s necessary to do a classification

for the services provided by audit companies. The classification

is the following:

Audit work.

Financial Information system design and implementation.

Other services like tax, internal audit services .

The conclusions for Kinney (Kinney, 2004) are:

It is not a statistically significant positive association be-

tween fees for financial information system design and im-

plementation or internal audit serv ices and restatements.

There is a statistically significant positive association be-

tween audit fees, audit-related fees, and unspecified non-

audit services fees and restatements.

Tax service fees are typically negatively associated with

restatements.

Legislators think that non-audit services impair auditor inde-

pendence (Law 19/1988; Directive 2006/43/CE). The Sarbanes-

Oxley Act (2002) says that a registered public accounting firm

may engage a non-audit service only if the activity is approved

in advance by the audit committee of the issuer.

Our opinion is that the audit company can do non-audit ser-

vice. If it is made a control of quality process and also the cli-

ents assume the responsibility, the audit firm can provide these

services.

The position of the legislator on this matter is to prohibit the

services from audit firms (Law 19/1988 of 12 of July; Manag-

ing 2006/43/CE). There are other norms that prohibit the exe-

cution of all kinds of works except advice and review on taxes

provided that this service has been approved by the committee

of audit (Sarbanes-Oxley Act, 2002).

We think that the businesses of audit can carry out different

services apart from the emission of a report. This service needs

two conditions: Firstly, the financial Law says, the “client as-

sume the responsibility of the global systems of internal control

or the service that will be carried out continuing the specifica-

tions established by the client, which it should assume the re-

sponsibility, execution, evaluation and operation of the sys-

tem” (Law 44/2002; art. 51e). Secondly, the client is not aware

that there is an adequate control of quality on the firms of audit

that includes the evaluation of the independe nce.

The Rotation of the Auditors

The analysis of the auditor rotation is clear, the all the exer-

cises during the audit of the business are made by the same

auditor, links they are created and a relationship among parties

implied in the auditors’ work a hazard in the independence of

the auditor.

Reviewing the regulations, we conclude that it is necessary a

rotation to have an efficient auditor’s system. This efficiency

comes from a double aspect; on one hand, to define a minimum

number of years, caused by economies of scale and the knowl-

edge given by the client. On the other hand, also establishes a

maximum of years, so difficult situations ar e avoided which can

put in prohibition the independence of the auditor.

We found some divergences in the regulations. On one hand,

some regulations talk about contracts with firms of audit (Law

of Audit), and about the rotation of the associates (VIII Guide-

lines). On the other hand, the Law of Audit establishes the du-

ration of audit’s contract around 9 years, the VIII Managing

talks about an average associa tes rotati on of 7 years.

From our point of view is good to have a regulation which it

establishes some limits on the number of years of the duration

of the contract of the audit firm and the rotation of the associate

responsible for the job.

Empirical Study

The first objective of the study has been to obtain informa-

tion on the independence of the audit firms in Spain. The se-

cond, the objective has been to analyze the utility of the infor-

mation facilitated in the annual accounts, in respect to the full

fees to the auditors.

The variables analyzed to derive from other studies from

Spain (Martinez et al., 2006) and International studies (Barizah

et al., 2005; Kinney et al., 2004). The ratio of independence has

been analyzed as well as the rotation of the auditors. The ratio

of independence has been used to see if the fees received from

the auditors put in prohibition its independence. The ratio of

independence has been calculated according to the following

expression:

RIHC I100

RI: Ratio of Independence.

FC: Fees received by the auditing firm from the client.

I: Total income of the auditing firm.

To calculate FC we use the information from the annual ac-

counts, which it has been obtained from a consolidated budget.

We use this data information for two reasons. First, because it

has been possible to verify that in a great number of the busi-

nesses analyzed, the same information about the auditors’ fees

on the annual accounts has been consolidated. In the individual

annual accounts is not specified, if the information facilitated is

from an individual or from a group of auditors. Second, we

worked with the information consolidated, because it is a pru-

dent criteria.

For fee calculation, we have added the fees received in audi-

tor work’s concept as the ones received i n othe r work’ s con cept .

This way we avoid the effects of the possible transfers of prices

among services.

To analyze the auditor rotation, we have evaluated: first, if it

has been any changes of the reference period in the auditor firm.

Second, if these changes are not regarding the auditors business,

we also analyzed rotation of the auditors.

The study sample has been formed by the totality of the

businesses in the Ibex 35 index in February, 2009. The period

of time analyzed was 2002 until 2007 by CNMV (National

Commission on the Securities Market). In 2002 was the first

time that the businesses were obliged to report the auditor fees.

We eliminated 6 businesses from the Ibex 35 index, because we

couldn’t find all the information needed. In this period of study

Copyright © 2013 SciRes. 41