P. Juraj ET AL.

TI

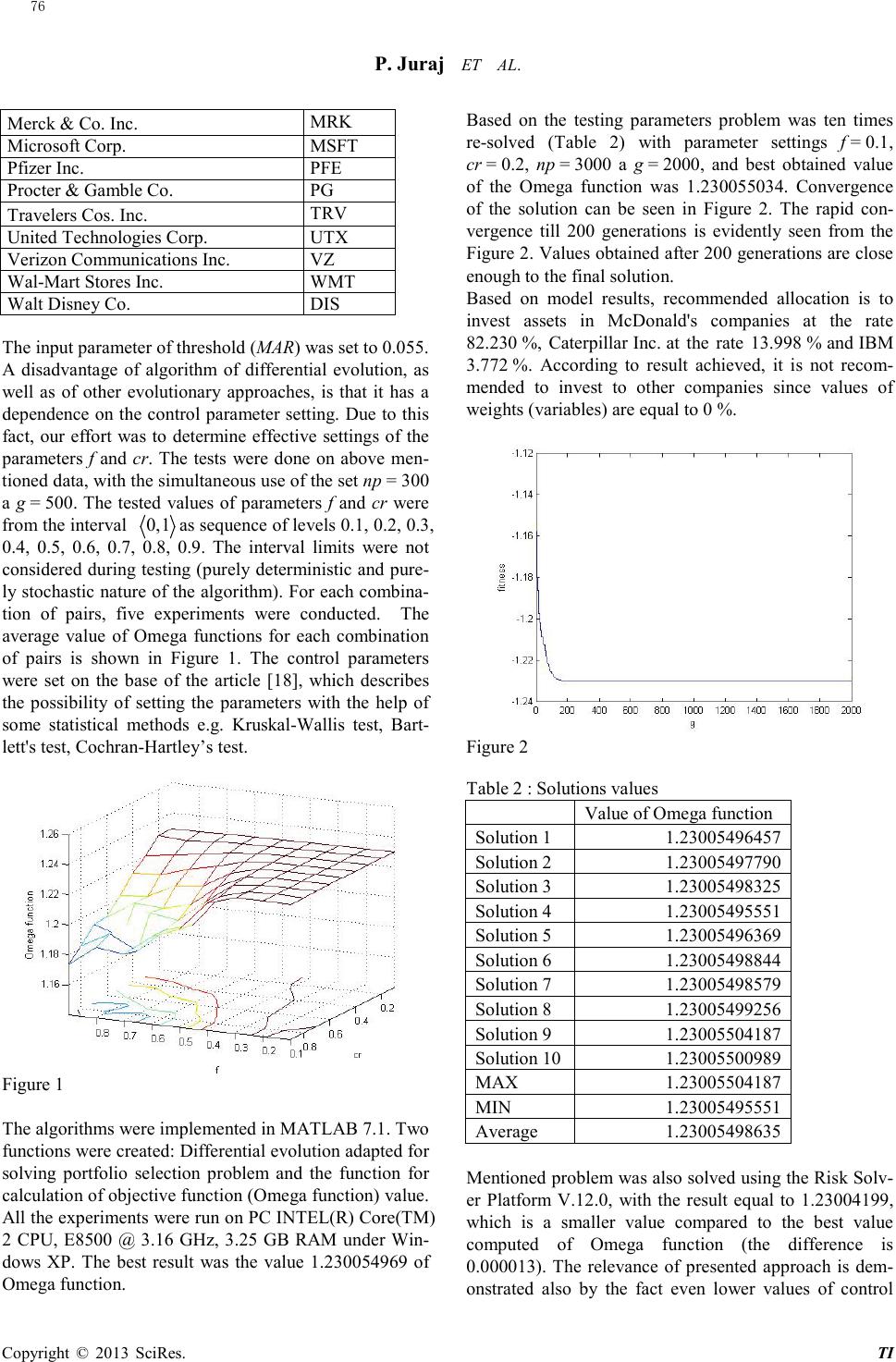

parameters (np = 300 and g = 500) provided the solution

on the level 1.230054969. Based on showed resul ts, it

can be stated the suitability of presented approach, which

enables to determine the good real time solution.

5. Conclusion

The portfolio selection problem is one of the basic prob-

lems of allocating capital over the number of assets.

Fro m differ ent sets of performance measurement tools to

assist us with our portfolio evaluations, authors chose

portfolio performance measure - Omega function, which

computability is difficult due to substandard structures

and therefore the use of standard techniques seems to be

relatively complicated. Based on it, we use one of the

evolutionary algorithms that allow solving various types

of optimization problems (differential evolution). Pre-

sented approach enables to determine good real-time

solution. The quality of results is comparable with results

obtained by professional software.

6. Acknowledgements

This paper is supported by the Grant Agency of Slovak

Republic – VEGA, grant no. 1/0104/12 „Modeling

supply chain pricing policy in a competitive

environ ment“.

REFERENCES

[1] W. F. Sharp e , “The Sharpe Ratio”, The Journal of

Portfolio Management, Vol . 21, No. 1, 1994, pp.

49–58.

[2] J. L. Treyno r , “How to Rate Management of In-

vestment Funds”, Harvard Business Review, Vol.

43, No. 1, 1965, pp. 63-75.

[3] M. C. Jensen, “The Performance of Mutual Funds

in the Period 1945-1964”, Journal of Finance, Vol.

23, 1968, pp. 389-416.

[4] F. A. Sortino and R. Meer, “Downside Risk”, The

Journal of Portfolio Management, Vol. 17, No. 4,

1991, pp. 27–31.

[5] T. H. Goodwin, “The Information Ratio”, Invest-

ment Performance Measurement: Evaluation and

Presenting Results. Hoboken, NJ: John Wiley &

Sons, 2009.

[6] C. S. Pedersen and T. Ruddholm-Alfin, ”Selecting

risk-adjusted shareholder performance meas-

ure”, Journal of Asset Management. Vol. 4, No. 3,

2003, pp. 152-172.

[7] R. Hentati-Kaffe l and J. L. Prigent , “Structured

portfolio analysis under SharpeOmega ratio”,

Documents de Travail du Centre d’Economie de la

Sorbonne, 2012.

[8] C. Keating and W. F. Shadwick, “A Universal Per-

formance Measure”, Journal of Performance Mea-

sureme nt .Vol. 6, 2002, pp. 59-84.

[9] S. Avouyi-Dovi, A. Morin and D. Neto, “Optimal

Asset Allocation with Omega Function”, Technical

report, Banque de France, 2004.

[10] R. Storn and K. Price. “Differential Evolution – A

simple and efficient heuristic for global optimiza-

tion over continuous spaces”, Journal of Global

Optimization , Vol. 11, 1997, pp. 341–359.

[11] Z. Čičková, I. Brezina and J. Pekár, “Alternative

method for solving traveling salesman problem by

evolutionary algorithm”, Management information

system s. No. 1, 2008, pp. 17-22.

[12] I. Brezina, Z. Či čková a nd J. Pekár, “Application of

evolutionary approach to solving vehicle routing

problem with time windows”, Economic review,

Vol. 38, No. 4, 2009, pp. 529-539.

[13] I. Brezina, Z. Čičko vá a nd J. Pekár, “Evolutionary

approach as an alternative method for solving the

vehicle routing problem”, Economic review, Vo l.

41, No. 2, 2012, pp. 137-147.

[14] D. Ardia, K. Boudt, P. Carl, K. M. Mullen and B. G.

Peterson, “Differential Evolution with DEoptim”,

The R Journal, Vol. 3, No. 1, 2011, pp. 27-34.

[15] I. Zelinka, “Umělá inteligence v problémech

globální optimalizace”, BEN-technická literature,

Pr aha , 2002.

[16] V. Mařík, O. Štěpánková and J. Lažanský, “Umělá

inteligence 4”, Academia Praha, 2003.

[17] G. C. Onwubolu and B. V. Babu, “New Optimiza-

tion Techniques in Engineering”, Springer-Verlag,

Berlin-Heidelberg, 2004.

[18] Z. Čičková, I. Brezina and J. Pekár, “A memetic

algorithm for solving the vehicle routing problem”,

In Mathematical methods in Economics 2011, 29th

international conference, Praha, Professional Pub-

lishing, 2011, pp. 125-128.

77

Copyright © 20 SciRes.

13