Paper Menu >>

Journal Menu >>

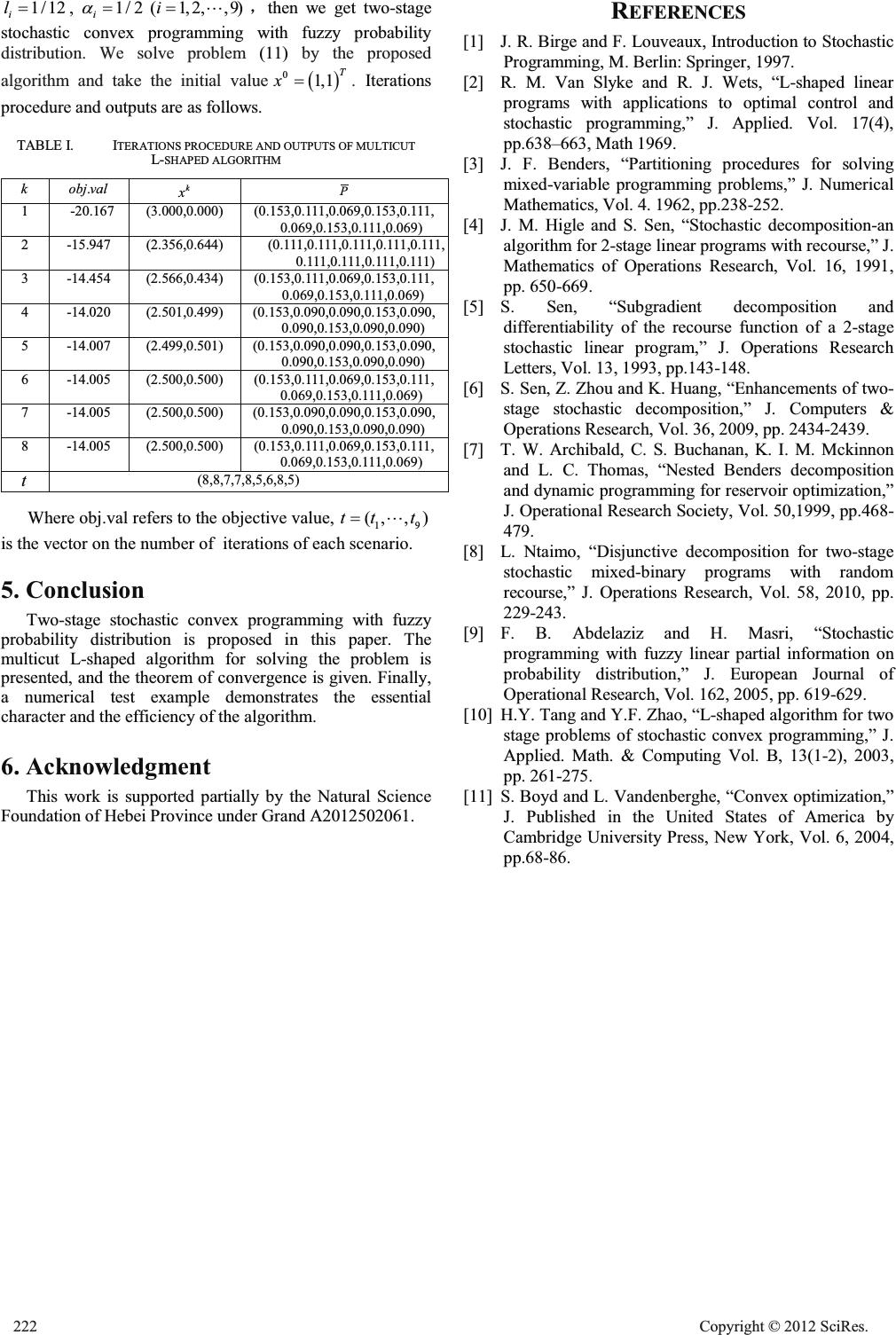

Multicut L-Shaped Algorithm for Stochastic Convex Programming withFuzzy Probability Distribution Miaomiao Han School of Mathematics and Physics North China Electric Power University Baoding, Hebei Province, China Hanmiaomiao_1@163.com Xinshun MA School of Mathematics and Physics North China Electric Power University Baoding, Hebei Province, China xsma@ncepubd.edu.cn Abstract—Two-stage problem of stochastic convex programming with fuzzy probability distribution is studied in this paper. Multicut L-shaped algorithm is proposed to solve the problem based on the fuzzy cutting and the minimax rule. Theorem of the convergence for the algorithm is proved. Finally, a numerical example about two-stage convex recourse problem shows the essential character and the efficiency. Keywords-stochastic convex programming;fuzzy probability distribution; two-stage problem; multicut L-shaped algorithm 1. Introduction Stochastic programming is an important class of mathematical programming with random parameters, and has been widely applied to various fields such as economic management and optimization control[1]. Two-stage stochastic programming is a kind of mathematical programming where the decision variables and the decision process can be decomposed into two stages based on random parameters are observed before and after the specific value. Stochastic linear programming as a basic issue has been studied widely, and many research results have been reported.In [2], two-stage problem of stochastic linear programming and the basic algorithm were first proposed and applied to the linear optimal control problem. Since then, a large variety of algorithms including Benders decomposition[2][3], stochastic decomposition[4], subgradient decomposition[5][6], nested decomposition[7], and disjunctive decomposition[8] for the two-stage stochastic linear programming had been developed. Among these methods, Benders decomposition also called the L-shaped method has become the main approach to deal with stochastic programming problems. The theories and algorithmsobtained before on stochastic linear programming all arebased on a hypothesis that the probability distributions of random parameters have completely information. However, in many situations, due to lack of the date, the probability of a random event is not fully known, and need to get an approximate range with the help of experts’ experience. Recently, model of the stochastic linear program with fuzzy probability distribution was proposed in [9], and the modified L-shaped algorithm was presented to solve the model. Stochastic convex programming is an important class of stochastic nonlinear program and has more widely application than stochastic linear programming[10].As a result, stochastic convex programming with fuzzy probability distribution will havemore useful in many practical situations. In this paper, two-stage stochastic convex programming with fuzzy probability distribution and the solving method are studied, a numerical example shows the essential character and the efficiency. 2. Two-stage stochastic convex programming under fuzzy probability distribution Let ,,P:¦ be a probability space, sample space ^` 1 ,, N ZZ : " is a finite set, and ¦ = 2 : is the V -algebra composed by power set of : , ^` . ii pP ZZ The two- stage stochastic convex programming problem is 1 ()(,) . . 0 N ii i minfxp Qx st Ax b x Z t ¦ (1) whereˈ (,) (,) . . ()() 0 ii ii Qx mingy st WyhTx y ZZ ZZ t (2) 1 n x and 2 n y are decision vectors, ()fx is convex function, Ais 11 mnu matrix, 1 m b is known vector, W is 22 mnu recourse matrix, for each i Z :,(, ) i gy Z is convex function on y , 2 () m i h Z is vector, and i T Z is Open Journal of Applied Sciences Supplement:2012 world Congress on Engineering and Technology Cop y ri g ht © 2012 SciRes.219  21 mnumatrix. Where x and y are the first stage decision variable and the second stage decision variable respectively. The mathematical expected value 1 [(,)](,) N ii i EQx pQx ZZ ¦ . When the random variable obeys fuzzy probability distribution, the scope of i pis as follows[9] ^ ` 1 |11 , 1;0,1,, N iiiiiii N ii i Pd lpd l ppi N D SDD dd t ¦ " (3) where 12 ,,, TN N Ppp p " consisted of probabilities, 1 ,, T N ll l " denotes the vagueness level, and the level value (0 1) i DD dd expresses the DM credibility degree of the partial information on probability distribution. Thefuzzy probability distributions results in that mathematical expectation [(,)]EQx Z is uncertain, here, [(,)] p P max EQx D S Z = 1 (,) N ii Pi maxp Qx D S Z ¦ will be used to instead of [(,)]EQx Z , and then (1) can be expressed as follows 1 ()(,) . . 0 N ii Pi minfxmaxpQx st Ax b x D S Z t ¦ (4) where (, ) i Qx Z is confirmed by(2). Obviously, for a given x , there exists 12 (, ,,) T N Ppp p " D S , such that 11 (, )(, ) NN ii ii P ii pQ xmaxpQ x D S ZZ ¦¦ . I. MULTICUT L-SHAPED ALGORITHM The problem(4) is equivalent to: 1 12 (), .. (,), , x N ii Pi min f x s tmaxp Qx xK KK D S T ZT d ¦ (5) where (, ) (,), . . ()(), 0, i iii y ii i i Qx min gy st WyhTx y Z Z ZZ t (6) and ` ^ 1,0,KxAxbx t ` ^ 2 , 0,.. ()(). ii iii Kxforallys tWyhTx ZZZ :t The standard L-shaped algorithm for solving above problem can be designed under outer linearization (see e.g. [9]). Suppose that 12 (, ,,) T N Ppp p " is solution of 1 (,) N ii Pi maxp Qx D S Z ¦ , problem (5) can be replaced by the following (7) 1 12 (, ) () .. , i N ii xi i Qx min f xp s tforalli xK KK Z T T d ¦ (7) because of each constrain in (5) corresponds to Nconstraints in (7). The multicut L-shaped algorithm is defined as follows: S0. Set 0,sk 0 i t for all 1, 2,,iN " , and 0 x is given. S1. Set 1kk , solve the following master problem: 1 () () ()(a1) .. ,0,(a2) ,1,2,,, (a3) ,()1,2,,, (a4) 1, 2,, N ii i ll lii lii min fxp stAxb x Dx dls Exe lit iN T T ° ° t ° ®t ° °t ° ¯ ¦ " " " (8) Let 1 ,,, kk k N x TT " be an optimal solution of problem(8). Note that if no constraint (a4) is presentfor some i , k i T is set equal to f , k i T and i parenot considered in the calculation of k x . Go to S2. S2. For 1, ,iN ", solve the following linear programming problems . . ()() (a5) 0,0,0 TT i k ii min zeueu s tWyIuIuhTx yu u ZZ ° ® °ttt ¯ (9) where 1, ,1 T e " , until, for some i , if the optimal value 0 i z!, let k V be optimal dual variables value, and define 1 1 ()() ()() kT si kT si DT dh VZ VZ ° ® ° ¯ , set 1ss , add the constraint 11 k ss Dx d t to the set (a3) and return to S1. If for all ,0 i iz , then go to S3. S3.For 1, ,iN " , anda fixed k x , solve the following convex programming problems (,) . . ()() (a6 0 (a7) ii k ii i i min g y st WyhTx y Z ZZ ° ® °t ¯ (10) 220 Cop y ri g ht © 2012 SciRes.  Let (,) i k Qx Z be the optimal value, and k i y the optimal solution. Solve the problem 1 (,) N i Pi kk i maxp Q x D S Z ¦ , and suppose 12 (,,,) kk kT N pp p" is the optimal solution, then update the objectivefunction of the master problem. Let k i v and k i u be the optimal dual variables associated withconstrain (a6) and (a7) respectively. Compute 1 1 () (), (,)()() [()()]. i i kT tii kT kkTk tiiiiiii EvT egy uyvWyh Z ZZ ° ® ° ¯ If 11 ii kk it t eEx T does not hold for any 1, ,iN " , stop, then 1 (, ,,) kk k N x TT " is an optimal solution. Otherwise, set 1 ii tt , add the constraint 11 ii kk it t eEx T t to the set (a4) , return to S1. 3. Theorem of convergence for the algorithm Proposition1. In the algorithm, constraint set(a3) is finite. Proof The proof of this proposition is the same to the standard L-shaped algorithm (see e.g. [2]). Proposition 2. For any i Z : and on all i xK Z , (, ) i Qx Z is either a finite convex function or is identically f , where ^ ` , 0,.. ()() iii iii Kx ystWyh Tx Z ZZZ :t . Proof (see e.g. [10]) Proposition3. If (, ) i Qx Z is a finite convex function for each i Z : , then the function 11 ii tt eEx islinear supporting hyper planes of(, ) i Qx Z . Proof By the duality theory (see e.g. [11]), it holds that (,( , )()()[( )()()] ) kTT k ii ii kkkkk iiiii Qxgyuy vWy hT x ZZ ZZ . We know from the convexity of (, ) i Qx Z that (, )(, )( )()[()()] ()(). TT ii i T i kkkkk iiiii k i Qxgyuy vWy h vT x ZZ Z Z t Thus (,)()()[()()] TT ii kkkkk iiiii gyuy vWy h ZZ () () T i k i vT x Z 11 ii tt eEx is a linear support of (, ) i Qx Z . Theorem. Suppose that the algorithm generates an infinite sequence of 1 (, ,,) kk k N x TT " . If 1 (, ,,) N x TT " is the limit point of an arbitrary subsequence 1 (, ,, ) jj j kk k N x TT " , and for each ,i 11 lim() 0 jj ii kk tt i j eEx T of , 1,, ,iN " then 1 (, ,,) N x TT " is an optimal solution of problem(7), x is an optimal solution of problem(4). Proof Since the number of the constraints of type (a3) is finite, we have that j k xK for j k sufficiently large. We also know K is closed convex set, then xK .By known, for each ,i 11 (,) jj j ii kk k iitt QxeEx TZ t , and 11 lim() 0 jj ii kk tt i j eEx T of Then (, ) ii Qx TZ for all 1, ,iN " . Thus, 1 (, ,,) N x TT " is a feasible solution of problem(7). On the other hand, if x is optimal solution to the minimax problem(4), but not necessarily an optimal solution in iteration j k , then * 11 () (,)() (,). jj NN kk ii ii PP ii fxmaxp Qxfxmaxp Qx DD SS ZZ d ¦¦ By continuity of the convex function we have that * 11 ()(, )()(, ) NN iii i PP ii fxmaxp Qxfxmaxp Qx DD SS ZZ d ¦¦ , then, for a certain value 12 (, ,,) T N pp p D S " * 11 ()( )( ,), NN iiii P ii fxpfxmax pQx D S TZ d ¦¦ Hence, 1 (, ,,) N x TT " is an optimal solution to problem(7), and xis an optimal solution to problem(4). 4. Numerical example Consider the following two-stage stochastic convex programming 12 22 12 12 12 12 11 122 2 112 2 1212 3 3.552 22 . . 25, , 3, 2, ,,, , 0. , x min xx yy Eminyyyy stx xyx xxyx x y yy y [ [[ °½ ° ° ®¾ °°¿ ¯ ° ° ®t d °d d ° °d ¯t d ° ° (11) where 1 [ takes the three values 3.5, 3.8 and 4.0 with probability 1/3, that2 [ takes the values 0.5, 1.0and 1.5 with probability 1/3, and that 1 [ and 2 [ are independent of each other, then 12 (,) T [[[ can take the each vector in the set 12 {(,)| T kk3 12 3.5,3.8,4.0,0.5,1.0,1.5}kk with probability 1/9. Under fuzzy probabilitydistribution, assume that [ takes the each values in 3 with probability around 1/9, i.e. i p#1/9 (1,2,,9)i "ˈit can be confirmed by(3), where 1/12 i d , Cop y ri g ht © 2012 SciRes.221  1/12 i l , 1/2 i D (1,2,,9)i "ˈthen we get two-stage stochastic convex programming with fuzzy probability distribution. We solve problem (11) by the proposed algorithm and take the initial value 0 1,1 T x .Iterations procedure and outputs are as follows. TABLE I. ITERATIONS PROCEDURE AND OUTPUTS OF MULTICUT L-SHAPED ALGORITHM k .obj val k x P 1-20.167(3.000,0.000)(0.153,0.111,0.069,0.153,0.111, 0.069,0.153,0.111,0.069) 2-15.947 (2.356,0.644)(0.111,0.111,0.111,0.111,0.111, 0. 111,0.111 ,0. 11 1,0.111) 3-14.454(2.566,0.434) (0.153,0.111,0.069,0.153,0.111, 0.069,0.153,0.111,0.069) 4-14.020(2.501,0.499) (0.153,0.090,0.090,0.153,0.090, 0.090,0.153,0.090,0.090) 5-14.007(2.499,0.501) (0.153,0.090,0.090,0.153,0.090, 0.090,0.153,0.090,0.090) 6-14.005(2.500,0.500) (0.153,0.111,0.069,0.153,0.111, 0.069,0.153,0.111,0.069) 7-14.005(2.500,0.500) (0.153,0.090,0.090,0.153,0.090, 0.090,0.153,0.090,0.090) 8-14.005(2.500,0.500) (0.153,0.111,0.069,0.153,0.111, 0.069,0.153,0.111,0.069) t (8,8,7,7,8,5,6,8,5) Where obj.val refers to the objective value, 19 (,, )tt t " is the vector on the number of iterations of each scenario. 5. Conclusion Two-stage stochastic convex programming with fuzzy probability distribution is proposed in this paper. The multicut L-shaped algorithm for solving the problem is presented, and the theorem of convergence is given. Finally, a numerical test example demonstrates the essential character and the efficiency of the algorithm. 6. Acknowledgment This work is supported partially by the Natural Science Foundation of Hebei Province under Grand A2012502061. REFERENCES [1]J. R. Birge and F. Louveaux, Introduction to Stochastic Programming, M. Berlin: Springer, 1997. [2]R. M. Van Slyke and R. J. Wets, “L-shaped linear programs with applications to optimal control and stochastic programming,” J. Applied. Vol. 17(4), pp.638–663, Math1969. [3]J. F. Benders, “Partitioning procedures for solving mixed-variable programming problems,” J. Numerical Mathematics, Vol. 4. 1962, pp.238-252. [4]J. M. Higle and S. Sen, “Stochastic decomposition-an algorithm for 2-stage linear programs with recourse,” J. Mathematics of Operations Research, Vol. 16, 1991, pp. 650-669. [5]S. Sen, “Subgradient decomposition and differentiability of the recourse function of a 2-stage stochastic linear program,” J. Operations Research Letters, Vol. 13, 1993, pp.143-148. [6]S. Sen, Z. Zhou and K. Huang, “Enhancements of two- stage stochastic decomposition,” J. Computers & Operations Research, Vol. 36, 2009, pp. 2434-2439. [7]T. W. Archibald, C. S. Buchanan,K. I. M. Mckinnon and L. C. Thomas, “Nested Benders decomposition and dynamic programming for reservoir optimization,” J. Operational Research Society, Vol. 50,1999, pp.468- 479. [8]L. Ntaimo, “Disjunctive decomposition for two-stage stochastic mixed-binary programs with random recourse,” J. Operations Research, Vol. 58,2010, pp. 229-243. [9]F. B. Abdelaziz and H. Masri, “Stochastic programming with fuzzy linear partial information on probability distribution,” J. European Journal of Operational Research, Vol. 162, 2005, pp. 619-629. [10]H.Y. Tang and Y.F. Zhao, “L-shaped algorithm for two stage problems of stochastic convex programming,” J. Applied. Math. & Computing Vol. B, 13(1-2), 2003, pp. 261-275. [11]S. Boyd and L. Vandenberghe, “Convex optimization,” J. Published in the United States of America by Cambridge University Press, New York, Vol. 6, 2004, pp.68-86. 222 Cop y ri g ht © 2012 SciRes. |