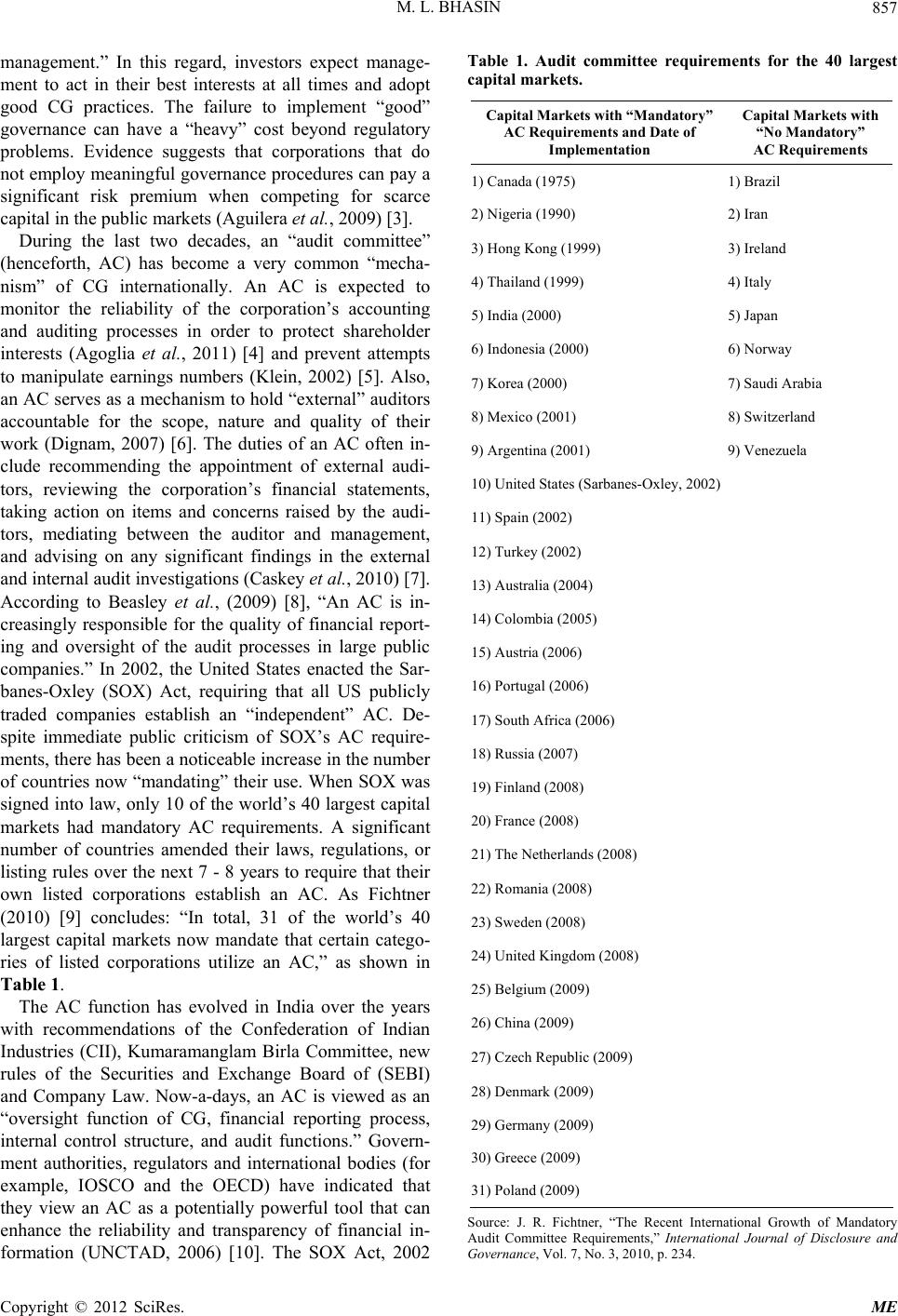

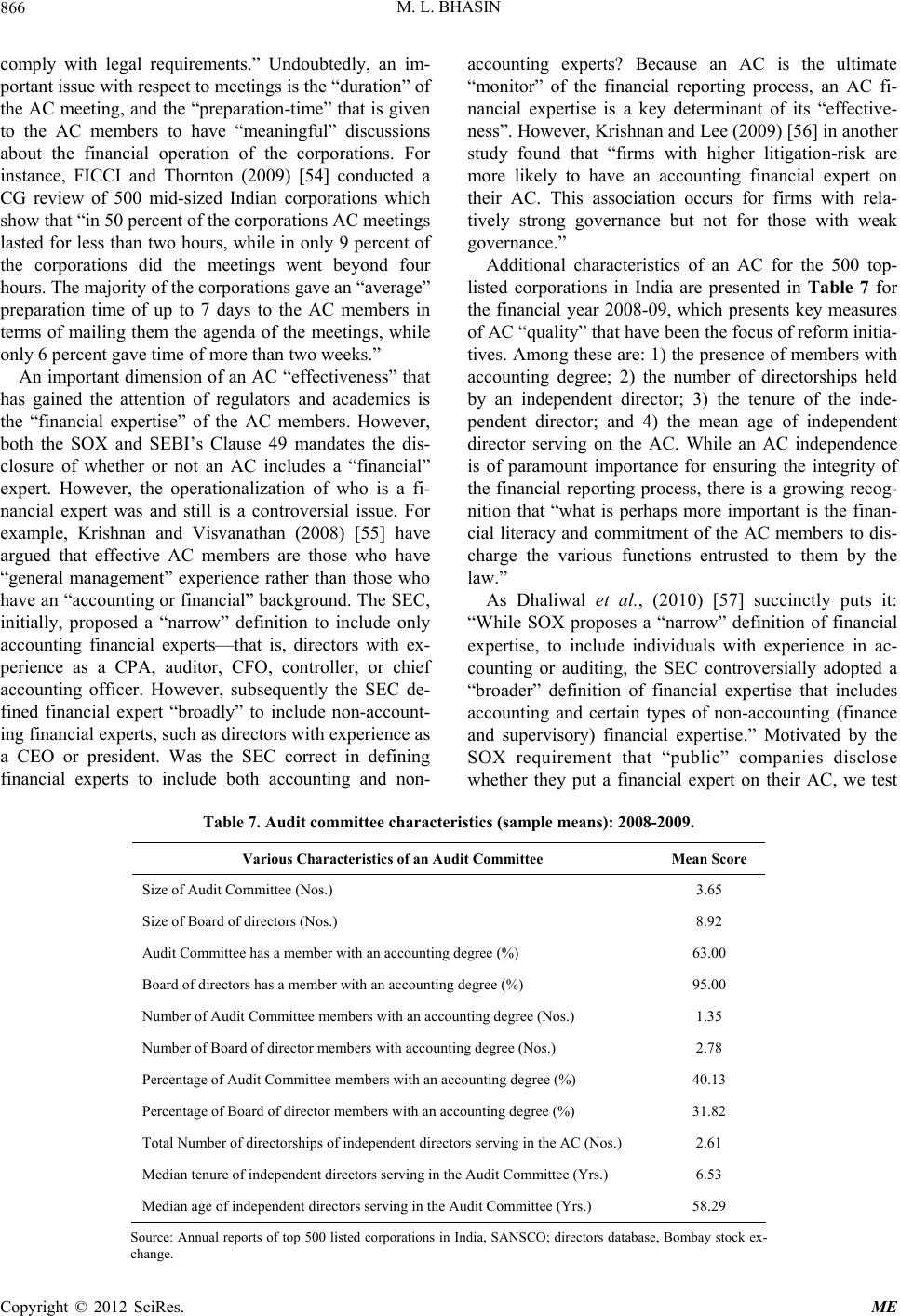

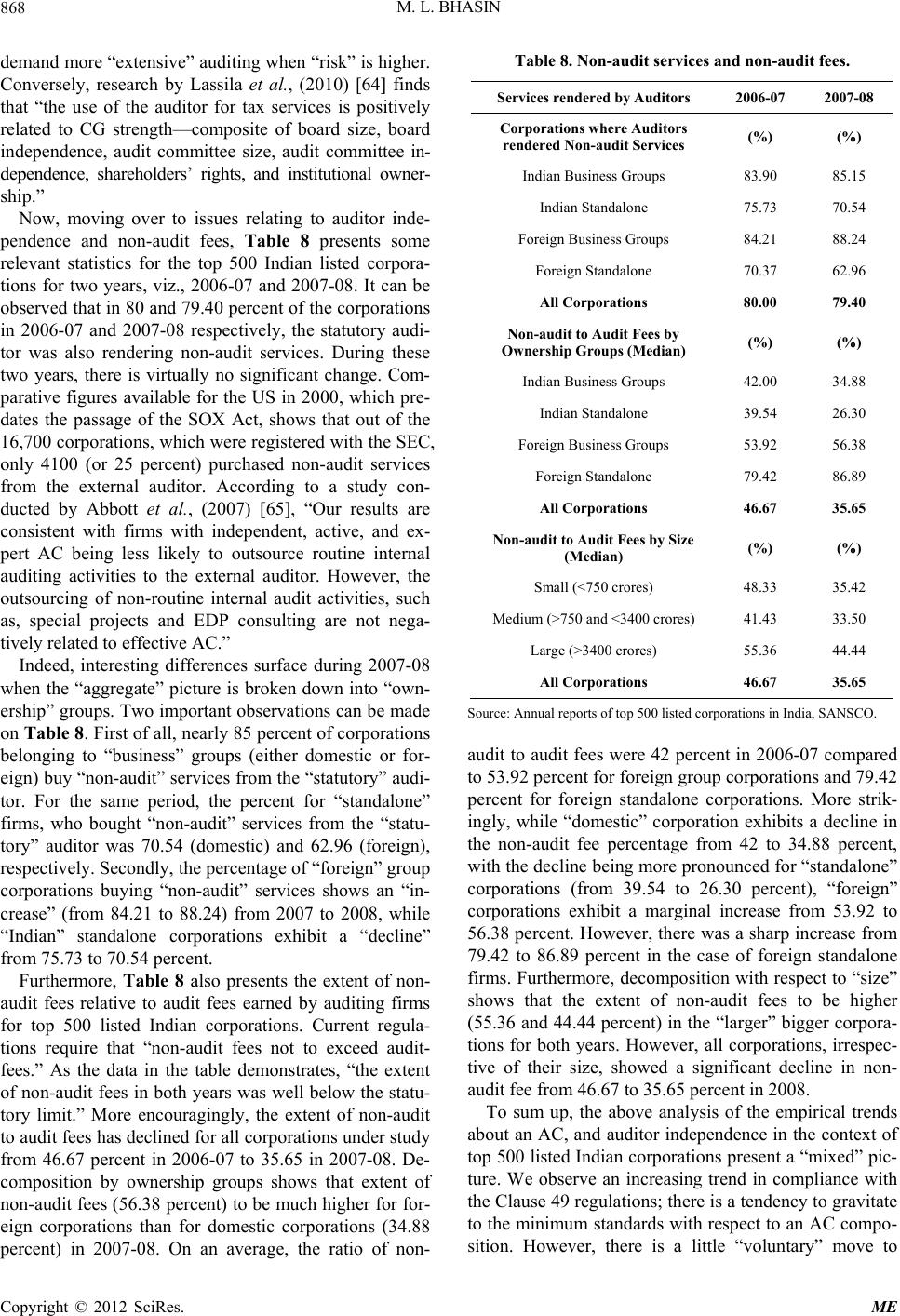

Modern Economy, 2012, 3, 856-872 http://dx.doi.org/10.4236/me.2012.37109 Published Online November 2012 (http://www.SciRP.org/journal/me) Audit Committee Mechanism to Improve Corporate Governance: Evidence from a Developing Country Madan Lal Bhasin Bang College of Business, KIMEP University, Almaty, Republic of Kazakhstan Email: madan.bhasin@rediffmail.com Received June 19, 2012; revised July 22, 2012; accepted August 10, 2012 ABSTRACT Nowadays, an audit committee (AC) is being looked upon as a distinct culture for CG and has received a wide-pub- licity across the globe. Government authorities, regulators and international bodies all have indicated that they view an AC as a potentially powerful tool that can enhance the reliability and transparency of financial information. Being mandatory under Security Exchange and Board of India (SEBI’s) Clause 49 of the Listing Agreement, an AC can be of great help to the board in implementing, monitoring and continuing “good” CG practices to the benefit of the corpora- tion and all its stakeholders. This study performs a “content” analysis on the AC reports of the top 500 listed companies in India during 2005 to 2008 to determine the information content of these reports and the extent to which these reports conform to the Clause 49 requirements of the SEBI. Also, discussed are the various trends about an AC characteristics viz., size, composition, activity, as well as, the extent of non-audit services provided by auditors in the top 500 listed Indian companies. No doubt, it is essential for the Indian corporations to accept and continue with the CG reforms that are “demarcated” by the challenges of the “new” millennium. Keywords: Corporate Governance; Audit Committee; SEBI Clause 49; Sarbanes-Oxley Act; Listing Agreement; Board of Directors; Financial Reporting; India 1. Introduction A corporation is a “congregation” of various stake- holders, namely, customers, employees, investors, ven- dor-partners, government and society. The relationship between shareholders and corporate managers is fraught with “conflicting” interests that arise due to the sepa- ration of ownership and control, divergent management and shareholder objectives, and information “asymme- try” between managers and shareholders. Due to these conflicting interests, managers have the incentives and ability to maximize their own utility at the expense of corporate shareholders. As a result, corporate governance structures evolve that help in mitigating these agency conflicts (Dey 2008) [1]. Simply stated, “Corporate go- vernance (henceforth, CG) is the system by which busi- nesses are directed and controlled.” In fact, CG deals with conducting the affairs of a corporation in such a way that there is “fairness” to all stakeholders and that its actions benefit the “greatest” number of stakeholders. CG is the acceptance by management of the inalienable rights of shareholders as the “true” owners of the corpo- ration, and of their own role as “trustees” on behalf of the shareholders. This has become imperative in today’s globalized business world where corporations need to access “global” pools of capital, need to attract and retain the “best” human capital from various parts of the world, need to “partner” with vendors on mega collaborations, and finally, need to live in “harmony” with the commu- nity. CG is beyond the realm of law; it stems from the cul- ture and mindset of management and cannot be regulated by legislation alone (Cohen et al., 2008) [2]. Corpora- tions, therefore, need to recognize that their growth re- quires the cooperation of all the stakeholders; and such cooperation is enhanced by the corporation adhering to the “best” CG practices. In this regard, the management needs to act as “trustees” of the shareholders at large and prevent “asymmetry” of information and benefits be- tween various sections of shareholders, especially be- tween the owner-managers and the rest of the sharehold- ers. While large profits can be made taking advantage of the asymmetry between stakeholders in the short-run, balancing the interests of all stakeholders alone will en- sure survival and growth in the long-run. Thus, CG is a key element in improving the economic “efficiency” of a firm. Indeed, corporations pool capital from a large in- vestor base, both in the “domestic” and in the “interna- tional” capital markets. In this context, “investment is ultimately an act of faith in the ability of a corporation’s C opyright © 2012 SciRes. ME  M. L. BHASIN 857 management.” In this regard, investors expect manage- ment to act in their best interests at all times and adopt good CG practices. The failure to implement “good” governance can have a “heavy” cost beyond regulatory problems. Evidence suggests that corporations that do not employ meaningful governance procedures can pay a significant risk premium when competing for scarce capital in the public markets (Aguilera et al., 2009) [3]. During the last two decades, an “audit committee” (henceforth, AC) has become a very common “mecha- nism” of CG internationally. An AC is expected to monitor the reliability of the corporation’s accounting and auditing processes in order to protect shareholder interests (Agoglia et al., 2011) [4] and prevent attempts to manipulate earnings numbers (Klein, 2002) [5]. Also, an AC serves as a mechanism to hold “external” auditors accountable for the scope, nature and quality of their work (Dignam, 2007) [6]. The duties of an AC often in- clude recommending the appointment of external audi- tors, reviewing the corporation’s financial statements, taking action on items and concerns raised by the audi- tors, mediating between the auditor and management, and advising on any significant findings in the external and internal audit investigations (Caskey et al., 2010) [7]. According to Beasley et al., (2009) [8], “An AC is in- creasingly responsible for the quality of financial report- ing and oversight of the audit processes in large public companies.” In 2002, the United States enacted the Sar- banes-Oxley (SOX) Act, requiring that all US publicly traded companies establish an “independent” AC. De- spite immediate public criticism of SOX’s AC require- ments, there has been a noticeable increase in the number of countries now “mandating” their use. When SOX was signed into law, only 10 of the world’s 40 largest capital markets had mandatory AC requirements. A significant number of countries amended their laws, regulations, or listing rules over the next 7 - 8 years to require that their own listed corporations establish an AC. As Fichtner (2010) [9] concludes: “In total, 31 of the world’s 40 largest capital markets now mandate that certain catego- ries of listed corporations utilize an AC,” as shown in Table 1. The AC function has evolved in India over the years with recommendations of the Confederation of Indian Industries (CII), Kumaramanglam Birla Committee, new rules of the Securities and Exchange Board of (SEBI) and Company Law. Now-a-days, an AC is viewed as an “oversight function of CG, financial reporting process, internal control structure, and audit functions.” Govern- ment authorities, regulators and international bodies (for example, IOSCO and the OECD) have indicated that they view an AC as a potentially powerful tool that can enhance the reliability and transparency of financial in- formation (UNCTAD, 2006) [10]. The SOX Act, 2002 Table 1. Audit committee requirements for the 40 largest capital markets. Capital Markets with “Mandatory” AC Requirements and Date of Implementation Capital Markets with “No Mandatory” AC Requirements 1) Canada (1975) 1) Brazil 2) Nigeria (1990) 2) Iran 3) Hong Kong (1999) 3) Ireland 4) Thailand (1999) 4) Italy 5) India (2000) 5) Japan 6) Indonesia (2000) 6) Norway 7) Korea (2000) 7) Saudi Arabia 8) Mexico (2001) 8) Switzerland 9) Argentina (2001) 9) Venezuela 10) United States (Sarbanes-Oxley, 2002) 11) Spain (2002) 12) Turkey (2002) 13) Australia (2004) 14) Colombia (2005) 15) Austria (2006) 16) Portugal (2006) 17) South Africa (2006) 18) Russia (2007) 19) Finland (2008) 20) France (2008) 21) The Netherlands (2008) 22) Romania (2008) 23) Sweden (2008) 24) United Kingdom (2008) 25) Belgium (2009) 26) China (2009) 27) Czech Republic (2009) 28) Denmark (2009) 29) Germany (2009) 30) Greece (2009) 31) Poland (2009) Source: J. R. Fichtner, “The Recent International Growth of Mandatory Audit Committee Requirements,” International Journal of Disclosure and Governance, Vol. 7, No. 3, 2010, p. 234. Copyright © 2012 SciRes. ME  M. L. BHASIN 858 has expanded the formal responsibilities of an AC. The status of an AC report has evolved from non-existence to voluntarily and now mandatory for publicly traded com- panies under the SEBI and Companies Act jurisdiction in India. Therefore, this paper seeks to “contribute to our understanding of the value and potential of an AC as a CG mechanism in a developing country like India.” It seeks to examine the structure and functions that are cur- rently performed by an AC in the Indian corporate world. 2. Literature Review Both, an AC and auditor “independence” have been im- portant areas of research in the accounting literature. In the past, various studies on an AC have focused on the independence, activity and on the financial expertise of an AC member. Recently, the research on auditor inde- pendence have focused on the extent of “non-audit” ser- vices provided by the “external” auditor as well audit- firm tenure, both of which are generally seen as “hin- drances” to auditor independence. In fact, renewed inter- est on CG and an AC have emerged in light of the “new” regulations that were enacted in the wake of the major corporate “scandals”, and the consequent enactment of the SEBI’s Clause 49 in India and SOX regulations in the US and in other parts of the world. A significant number of researchers, primarily from the Western and European countries, have studied vari- ous dimensions of an AC and its “effectiveness”. These studies have led to a lively debate as to the proper com- position of the membership of an AC. For example, Romano (2005) [11] argues that an AC composed solely of independent directors, or even a majority of inde- pendent directors, do not limit the occurrence of ac- counting “improprieties”, while Prentice and Space (2007) [12] refutes this argument by citing numerous studies confirming that an “independent” AC improves the financial reporting. Despite the continuing “hot” debate as to whether “in- dependent” directors are a necessary component of an AC, an overwhelming number of studies establish that the mere formation of an AC results in substantial bene- fits. For example, Knapp (1987) [13] concluded that an AC can improve auditing because “an AC member tend to support auditor, rather than management, when audit disputes occur.” On the other hand, Beattie (2007) [14] in his research found that the presence of an AC is a very significant factor in enhancing the third-party perceptions of auditor independence. However, Wild (1996) [15] found evidence that establishment of an AC enhances earnings quality, and Goodwin-Stewart and Kent (2006) [16] found that an AC is associated with “higher-quality” audits. Similarly, De Fond et al., (2005) [17] study re- vealed that “over-statements of earnings are less likely among firms that have an AC,” while Dechow et al., (1996) [18] study found that “corporations manipulating earnings are more likely to have boards of directors dominated by managers and less likely to have an AC.” Williams and Tower (2004) [19], however, conducted a comprehensive simultaneous analysis of the association between five AC composition and operational character- istics features and earnings management based on a sam- ple of 485 Singapore publicly traded organizations. Moreover, in a study undertaken by McMullen (1996) [20], the author concluded that “firms with an AC are associated with fewer shareholder lawsuits alleging fraud, fewer quarterly earnings restatements, fewer SEC en- forcement actions, fewer illegal acts and fewer instances of audit turnover when there is an audit-client disagree- ment.” By and large, while a vast majority of the studies conclude that an AC provides substantial benefits to the corporation, a handful of studies question their “true” value. In particular, Beasley (1996) [21] study disputes whether an AC actually reduces the likelihood of fraud. Likewise, in a study of an AC in Spain, Pucheta-Marti- nez and de Fuentes (2007) [22] determined that “the mere presence of an AC does not reduce the occurrence of error and non-compliance qualifications.” However, the same study also determined that other factors, such as the size and independence of an AC did have a signifi- cant impact on certain aspects of financial reporting. Unfortunately, very little research work has been done, both in India and abroad, on the role of an AC in im- proving CG. For example, Al-Mudhaki and Joshi (2004) [23] examined the composition, focus and functions of an AC and the effects of the meetings and the criteria used in the selection of members by the Indian listed corpora- tions based on 73 “questionnaire” responses in 2002. Similarly, Agarwal (2006) [24] stated that “an AC of the board is today seen as a key fulcrum of any corporation. Being mandatory under Clause 49, an AC can be of great help to the board in implementing, monitoring and con- tinuing good CG practices to the benefit of the corpora- tion and its stakeholders.” Moreover, Cohen et al., (2010) [25] expressed that CG issues have grown more salient in the light of the alleged corporate accounting scandals. Sandra (2005) [26] conclude by saying that “comprehen- sive regulatory changes, brought on by recent CG re- forms, have broadly redefined and reemphasized the roles and responsibilities of all the participants (espe- cially the AC) in a public corporation’s financial report- ing process.” Researchers recently have deepened the study of gov- ernance and auditing outcomes with more recent evi- dence on auditor selection and retention, findings that governance characteristics influence auditors’ risk as- sessments and planning decisions, some conflicting re- sults related to governance and auditor fees (audit and Copyright © 2012 SciRes. ME  M. L. BHASIN 859 non-audit), and evidence that internal audit budgets are associated with governance characteristics (Carcello et al., 2011) [27]. Other recent insights include the impor- tance of an AC accounting expertise over broader finan- cial expertise; the apparent potential for an AC compen- sation methods to influence an AC member judgments; the existence of substantive, ceremonial, and informal AC processes; a deeper understanding of an AC member evaluation of accounting disagreements and adjustments; and the serious consequences to directors when a com- pany experiences accounting trouble. Over the past two decades, the CG literature in ac- counting and auditing has grown rapidly. In the present study, our CG focus is primarily on the various “dimen- sions” of an AC. Documented evidence on effectiveness of an AC in enhancing “good” CG has focused on vari- ous aspects, but the issue of interest in this study is the support of an AC in enhancing “auditor” independence. Hinzpeter et al., (2009) [28], for example, found that “an AC is more likely to support across members of an AC. This is true regardless of whether the member is in a full-time (or part-time) position, such as corporate man- agers, academicians, and retired partners of certified public accounting firms.” Similarly, Pearson (1980) [29], and Dockweiler et al., (1986) [30] showed that “an audi- tor’s reliance on management is reduced due to the direct communication with an AC.” However, Lam (2000) [31] found that “the appearance of independence of an AC would enhance auditor independence and improve trans- parency in financial reporting.” Beattie et al., (1999) [32] also reported that “audit partners, finance directors, and financial journalists believed that an AC with independ- ent non-executive directors strongly encourages auditor independence. Independent directors of an AC are ex- pected to increase the quality of monitoring because they are not associated with the corporation either as an offi- cers or employees; thus, they would act as the share- holder’s watchdog.” Similarly, Raghunandan and Rama (2007) [33] revealed that “an AC that consists of quail- fied independent directors is better able to contribute towards auditor independence.” To sum up, the extant literature provides “strong” empirical support that both an independent AC and higher-levels of audit independ- ence have a significant beneficial effect on enhancing the quality of disclosures, in reducing discretionary earnings management, increasing the informativeness of earnings, and in general enhancing the value of the firm. From the above description, it is amply clear that India (being a developing country) presents an ideal case for the analysis of improving CG through making an effect- tive use of an AC practices followed by the corporate- sector because the economy has been undergoing rapid economic transformation in the financial services, tour- ism, information-technology sectors, and the “niche” manufacturing gaining momentum too. In the Indian- context, there has been very limited number of AC stud- ies, as compared to its Western and European counter- parts. However, just two studies are available on the theme of an AC in India, which were done by Al-Mud- haki and Joshi and Agarwal, as stated above. The fore- going discussion suggests that the literature on the de- terminants of an AC disclosure in the Indian CG context is very “limited and inconclusive”. Thus, our present study builds on the previous literature of an AC practice and overall CG scenario in the Indian corporate-sector. The scope of this study has been confined to top 500 In- dian “listed” corporations, and a “content” analysis was performed on their annual reports for four years, namely, 2005-06 and 2008-09 respectively. The present study also contributes to the literature in an important sense that it analyzes data from a developing country and an emerging capital market, which has not been widely studied before on the role of an AC in the context of CG requirements. 3. Corporate Governance and Audit Committee Initiatives in India : An Overview During the last two decades, an AC has become a com- mon “mechanism” of CG internationally. Originally, “non-mandatory” structures used by a “minority” of cor- porations, more recently numerous “official” profess- sional and regulatory committees in many countries have recommended their more “universal” adoption and have advocated “expanded” roles for an AC. Often, increased attention on CG is a result of “financial” crisis. For in- stance, the Asian financial crisis brought the subject of CG to the “surface” in Asian countries. To quote Lin et al., (2009) [34], “Recent scandals disturbed the otherwise placid and complacent corporate landscape in the US. These scandals, in a sense, proved to be serendipitous. They spawned a new set of initiatives in CG in the US, and triggered a fresh debate in the European Union, as well as, in the Asian countries.” Long renowned for their opaque business practices, Asian corporations have undergone a dramatic transformation on the CG front. Jamie Allen (2008) [35], for example, states that “most of the countries/markets in the Asian region had taken the initiative long-back in 1990s by formulating and im- plementing an official code of CG,” which is summa- rized in Table 2. Beginning in the late 1990s, the Indian government started implementing a significant “overhaul” of the country’s CG system. As described by Afsharipour (2009) [36], “These CG reforms were aimed at making boards and AC more independent, powerful and focused moni- tors of management, as well as, aiding shareholders, in- Copyright © 2012 SciRes. ME  M. L. BHASIN Copyright © 2012 SciRes. ME 860 Table 2. Development of CG codes in the Asian countries. Country Date of Main Code(s)Are Independent Director’s required? Are Audit Committees Required? China 2002/2005 Yes Yes Hong Kong 1993/2004 Yes Yes India 1999/2005/2007 Yes Yes Indonesia 2001/2006 Yes Yes Japan 2003/2004 Optional Optional South Korea 1999/2003 Yes Yes (Large Firms) Malaysia 2001/2007 Yes Yes Philippines 2002 Yes Yes Singapore 2001/2005 Yes Yes Taiwan 2002 Yes (Certain Firms) Yes (Certain Firms) Thailand 1999/2006 Yes Yes Source: Jamie allen, Asian Corporate Governance Association: Corporate Governance Seminar, Organized by Chubb Insurance and Solidarity, Bahrain, 16 April 2008, p. 10. cluding institutional and foreign investors, in monitoring management.” There have been several leading CG ini- tiatives launched in India since the mid-1990s. The first was by the Confederation of Indian Industry (CII), which came up with the first “voluntary” code of CG in 1998 (www.ciionline.org). In 1996, the CII took a special ini- tiative on CG—the first institutional initiative in Indian industry. In April 1998, the country produced the first substantial code of best practice on CG after the start of the Asian financial crisis in mid-1997. Titled “Desirable Corporate Governance: A Code”, this document was written not by the government, but by the CII (1997) [37]. It is one of the few codes in Asia that explicitly discusses domestic CG problems and seeks to apply best-practice ideas to their solution. In the late 1999, a government- appointed committee, under the leadership of Kumar Mangalam Birla (Chairman, Aditya Birla Group), re- leased a draft of India’s first “national” formal code on CG for listed companies. The committee’s recommenda- tions (many of which were “mandatory”) were closely aligned to the international “best” practices on CG—and set “higher” standards than most other parts of the region at that time. However, the code was approved by the Se- curities and Exchange Board of India (SEBI) in early 2000, and was implemented in stages over the following two years (applying first to “newly” listed and “large” companies). It also led to changes in the BSE and NSE stock exchange listing rules. The next move was also by the SEBI, now enshrined as Clause 49 (very similar to US Sarbanes-Oxley Act, 2002) of the listing agreement. The Naresh Chandra Committee and Narayana Murthy Committee reports followed it in 2002. Based on some of the recommenda- tion of these two committees, SEBI revised Clause 49 of the listing agreement in August 2003. The SOX has re- ceived mixed (and increasingly “negative”) response in the US. However, Clause 49 and SOX share “similarities but different responses by market.” Perhaps, only some CG changes valuable and some CG changes positive in one environment and not others (Balasubramanian et al., 2008) [38]. Also, genesis of changes differs: Clause 49 was introduced by “industry” initiative in India, but SOX was introduced in US due to Enron like scandals. While SEBI proceeded to adopt considerable CG reforms, the implementation and enforcement of such reforms in fact, have lagged behind. Reform of “central” public-sector enterprises (CPSEs) is also high on the Indian government’s agenda. Strong PSEs would be better prepared to enter the capital market to raise funds, which means practices must be in place to ensure accountability. The push by the government has resulted in some guidelines, which were issued by the Department of Public Enterprises (2007) [39] (www. dpe.nic.in) in June. Even though these guidelines are voluntary, all CPSEs (both listed and non-listed) are meant to follow them, with compliance of these guide- lines to be referred to in the Directors’ report, Annual report and the chairman’s speech during the Annual General Meeting. The Department will grade the corpo- rations on the basis of their compliance with the guide- lines. Issued on an experimental basis for a year, they will be revised “in the light of experience gained”. Thus, in CG practices, India can be proud of what it has achieved so far, initially voluntarily and later under guidance of various regulators, while recognizing that obviously much more needs to be done.  M. L. BHASIN 861 4. Audit Committee Mechanism in India There has been growing recognition in recent years of the importance of CG in ensuring sound financial reporting and deterring fraud. The audit serves acts as a monitoring device and is thus, part of the CG mosaic (Kaushik, 2009) [40]. It is claimed that the auditing system in India is “comprehensive and well supported by law, which en- sures that impartiality, objectivity and independence of statutory auditors are maintained” (Giridharan, 2004) [41]. However, experience has shown that certain weak- nesses and lacunae do exist in the Indian system. In this context, Ganguly (2001) [42] asserts, “Various types of accounting manipulations, irregularities and leakages go unnoticed to the detriment of the public and sharehold- ers.” However, over the years, this arrangement was felt inadequate in view of the changing business scenario and it is felt that a greater interaction and link between the auditors and the top echelon of management is needed. The series of accounting “scandals” have intensified “pressure” from the stakeholders and the regulators on an AC to do the jobs, for which they were hired. Even though most corporations have an AC, “their role has been limited due to the lack of expertise and time.” An “active” AC is important because it indicate the com- mitment to the issues of interest because of the reports it release about the activities undertaken during the finan- cial year and the efforts made to ensure adequate internal control (Chatterjee, 2011) [43]. In addition, an AC must be given the role to approve and review audit fees, thus neutralizing the bias of management influence on the negotiations with the auditors. Of equal importance, auditor “independence” can be safeguarded if an AC is composed of a majority of independent and non-execu- tive directors and this might indicate that their inde- pendent status would contribute to auditor independence through bridging communication networks and neutral- izing any conflict between the management and the auditor (Puri et al., 2010) [44]. Indeed, an AC can go a long-way in “enhancing the credibility of the financial disclosures of a corporation and promoting transpar- ency.” Thus, it is essential for the Indian corporations to accept and continue with the reforms that are “demar- cated” by the challenges of the “new” millennium. 4.1. Legal Framework for an Audit Committee Public corporations in India face a “fragmented” regula- tory structure. The Companies Act, 1956 is administered by the Ministry of Corporate Affairs (MCA) and is cur- rently enforced by the Company Law Board (CLB). The MCA, the SEBI, and the stock exchanges jointly share jurisdiction over the “listed” corporations, with the MCA being the “primary” government body charged with ad- ministering the Companies Act, while SEBI has served as the securities market “regulator” since 1992. Likewise the CG standards in the US and the UK, India’s CG re- forms followed a “fiduciary and agency cost model.” With a focus on the agency model of CG, the Clause 49 reforms included detailed rules regarding the role and structure of the corporate board and internal control sys- tems. An AC has been prescribed as a part of CG mecha- nism to be followed by the “listed” corporations, under clause 49 of the Listing Agreement, and by certain “pub- lic” corporations under the Companies Act, 1956. Now- a-days, an AC is an important tool to consider and decide on all financial parameters and policies, internal controls, review of auditing, project implementation, reconstruct- tion, merger and amalgamation, and any financial ir- regularities. It is noteworthy to know “how the constitu- tion of an AC generally takes place and the so called di- rectors being members of an AC are really independent and discharge their fiduciary duties entirely in an unbi- ased and unobtrusive manner.” 4.1.1. The Indian Companies Act, 1956 Section 292A was inserted in the Companies Act, 1956 with effect from December 13, 2000, providing that “every public corporation having a paid-up capital of not less than Rs. 5 crore shall constitute a committee of the board of directors known as an AC.” Further, it provides an AC should have discussions with the auditors peri- odically about internal control systems, the scope of audit including the observations of the auditors and review of half-yearly and annual financial statements before sub- mission to the board, and also ensure compliance of in- ternal control systems. The supremacy of an AC is rec- ognized in the manner that recommendations of an AC on any matter relating to financial management including audit report shall be binding on the board and, if the board does not accept the recommendations of an AC, it shall record the reasons therefore, and communicate such reasons to the shareholders. In the event of default of the provisions of Section 292A, the corporation and every officer in default shall be punishable with imprisonment for a term up to one year or with fine up to Rs. 50,000 or with both. The offence is compoundable under section 621A of the Act. A non-banking financial corporation (NBFC) having assets of Rs. 50 crore and above as per its last audited balance sheet is required to constitute an AC, consisting of not less than 3 members of its Board of Directors. The AC constituted by an NBFC under section 292A of the Companies Act, 1956 shall be the AC for this purpose. 4.1.2. SEBI Cl ause 4 9 of Li st i ng Agreement Based on the recommendations of the Committee headed by Mr. Kumarmangalam Birla on CG in “listed” corpo- Copyright © 2012 SciRes. ME  M. L. BHASIN 862 rations, the SEBI amended the Listing Agreement on February 21, 2000 by providing therein Clause 49 on CG. On October 29, 2004a “revised” Clause 49 was intro- duced, which was finally made effective from December 31, 2005. All existing listed-corporations having a paid- up share capital of Rs. 3 crore and above or net worth of Rs. 25 crore or more at any time in the history of the corporation, have to comply with the same. The corpora- tions seeking listing for the “first” time have to comply at the time of seeking “in-principle” approval for such list- ing. The clause 49 provides for appointment of inde- pendent directors, AC and several other parameters for disclosure to and for protection of interest of sharehold- ers. 5. Research Methodology Annual reports are an ideal place to apply an AC frame- work because they allow us to compare AC positions and trends across different corporations, industries and coun- tries. They are an instrument for “communicating issues comprehensively and concisely, and they are produced regularly, so they can be used to analyze management attitudes and policies across reporting periods.” The main objective of the present research study is “to survey the prevailing practices of an AC disclosure made by the corporate-sector in India over a four year period from 2005-06 to 2008-09.” Accordingly, the sample-size of this study consists of top-500 listed corporations from India in terms of their market capitalization, as on March 31, 2008. The annual reports and other relevant informa- tion of the selected corporations were obtained from the two databases, first one provided by SANSCO—Annual Reports Library Services (www.sansco.net), and second by Directors Database—a CG initiative of Bombay Stock Exchange prepared in association with Prime Database (www.directorsdatabase.com). Reports on the AC were subjected to a “content” analysis to identify the title and format of such reports. The content analysis of annual reports involves “codifi- cation” of qualitative and quantitative information into “pre-defined” categories in order to derive “patterns” in the presentation and reporting of information. The “cod- ing” process also involved reading the annual report of each corporation and coding the AC information accord- ing to pre-defined categories. Over the last decade, con- tent analysis has been used by several leading researchers to study the performance and reporting (Beattie, 2007) [14]. Therefore, as part of the present study, “content” analysis has been used to analyze the extent of an AC disclosures made by the top 500 listed companies in In- dia. By looking at the disclosures made within their an- nual reports, one can examine the extent to which Indian corporations “publicly” document the presence (or im- portance) of an AC. Specifically, the paper covers the following aspects related to an audit committee: 1) The structure and composition of an AC; 2) The criteria used to select an AC members; 3) Examining the importance of functions currently performed by an AC and also to analyze any differences in the practices of corporations in this regard; 4) The areas of an AC review focus; and 5) The effects of meetings on an AC functions. Finally, as part of this study, an attempt will be made to examine and analyze the trends about various characteristics of an AC, such as, their size, composition and activity, as well as, extent of non-audit services provided by the auditors in the top 500 listed Indian corporations. 6. Findings of Study and Analysis of Results The SEBI’s Clause 49 (2004) [45] and other regulatory changes have put tremendous demands on an AC. Hav- ing the right directors on an AC—with mandated inde- pendence and financial literacy combined with integrity, healthy skepticism and judgment, knowledge of the cor- poration and industry, and the courage to challenge deci- sions—is an important driver of an AC “effectiveness”. The AC members must learn “how to work smarter and to allow enough time to complete their ever-lengthening list of duties.” In fact, given their “pumped-up” workload, they are struggling to know what to put at the top of the list. As Heffes (2007) [46] lucidly puts it: “The AC has a lot on their plates and so they need help to ensure they see the forest, not just the trees. While they should re- view information carefully and challenge management when necessary; they should not be resolving everyday issues or making management decisions.” This section presents detailed trends about various characteristics of an AC, such as, their size, composition and activity, as well as, extent of non-audit services pro- vided by the auditors in the Indian corporations. These trends are presented for the top 500 listed corporations in India, based on their market capitalization as on March 31, 2008, for four years covering the financial years 2005-06 to 2008-09. As stated earlier under the research methodology, all the required annual reports and other secondary sources of information in respect of the top 500 listed corporations were outsourced and extracted from the private database maintained by SANSCO ser- vices (www.sansco.net) and Directors Database (www. directorsdatabase.com). Moreover, Tables 3-8 are con- structed based on the disclosures made in the “Corporate Governance Reports” filed by these corporations. In fact, the year 2006 marks the year when all the listed firms were required to comply with the revised provisions of the SEBI’s Listing Clause 49, which were first notified on October 29, 2004 but came into effect from January 1, 2006. Table 3 summarizes distribution of corporations Copyright © 2012 SciRes. ME  M. L. BHASIN Copyright © 2012 SciRes. ME 863 Table 3. Distribution of corporations according to size of audit committee. Size of Audit Committee (AC) 2005-06 2006-07 2007-08 2008-09 2 0.30 2.19 0.51 1.25 3 57.19 50.27 51.39 49.87 4 29.64 33.61 34.43 36.84 5 7.78 9.02 9.87 8.02 6 2.99 3.83 3.04 3.26 7 2.10 0.55 0.51 0.50 8 0.00 0.27 0.00 0.25 9 0.00 0.27 0.25 0.00 Average Size of AC 3.62 3.66 3.66 3.62 No. of Corporations 334 336 395 399 Source: Annual Reports of Top 500 Listed Corporations in India, SANSCO. according to size of an AC. According to Carcello et al., (2002) [47], “The AC plays an important role overseeing and monitoring the financial reporting process, internal controls, and the external audit. They provide a communication bridge between management and the internal and external audi- tors.” No doubt, to maintain integrity of their monitoring functions, an AC is required to perform their response- bilities “diligently”. As per Clause 49, “A qualified and independent AC shall be set up. The AC shall have minimum three directors as members. Two-thirds of the members of AC shall be independent directors.” Judged in the context of Clause 49 regulations requiring listed corporations to have an AC with a minimum of 3 mem- bers, Table 3 shows that nearly all (98.75 percent) cor- porations have complied with this regulation. However, a large majority of the corporations have already consti- tuted their AC, with the minimum size required under the regulations; however, with one-third (36.84) of the cor- porations adding one “extra” member. In fact, there are very few Indian corporations (just 4 percent) that have an AC with more than 5 members in 2008-09. In fact, an AC has been formed to act both as a “con- duit” of information supplied by the management to the auditors, and at the same time to “insulate” the auditor from the pulls and pressures of the management (Sharma, 2007) [48]. An AC is, therefore, required to be “inde- pendent” of the management and has the “key” response- bility of deciding the scope of work, including the fixa- tion of audit fees and the determination of the extent of non-audit services. As Sarkar and Sarkar (2010) [49] very aptly pointed out, “The basic idea is to make the auditor not to be dependent on “inside” management, both in terms of discharge of its functions as well as in terms of its survival.” Tables 5 and 6 summarize the trends regarding a AC independence in the Indian cor- porate-sector. Recalling that Clause 49 require an AC to have at least 2 to 3 of its members as “independent” di- rectors, Table 4 shows that the “mean” of independent directors to be 79 over these four years from 2005-06 to 2008-09. Surprisingly, 15.32 percent of the Indian listed corporations did not comply with Clause 49 regulations in 2006. However, by and large, corporations in India seem to be making a serious effort to comply with the regulations, with the extent of non-compliance signify- cantly decreasing from 15.32 percent in 2006-07 to 10.35 percent in 2008-09. A striking observation with regard to independence of an AC is “the steady decline in the percentage of corpo- rations with fully independent AC.” While during 2005- 06 more than half of the corporations (54.98) had “vol- untarily” chosen to have a fully independent AC, this percentage has steadily declined, surprisingly, to just over one-third (37.88) by 2008-09. What is instead ob- served is a very steady move to have an AC, which are just in accordance with the minimum independence re- quirement that is prescribed under the law. Given the size distribution of an AC, a fraction between 2/3 and less than 1 implies a “mandatory” compliance under the Clause 49 regulations. This is further borne out by the steady “increase” in the proportion of corporations that have an “executive” (or management) director present in an AC from 2006 to 2008. Recall that until 2006, when the revised Clause 49 came into effect, an AC was required to consist only of non-executive directors, with majority of them being independent. The revised Clause 49, shockingly removed the non-executive director requirement and instead specified that an AC to have a minimum of three mem- bers, with two-thirds of themeing independent. Given b  M. L. BHASIN 864 Table 4. Trends in audit committee indepe nde nce: distribution of corporations. Year Fraction of Independent Directors 2005 2006 2007 2008 f < 2/3 8.16 15.32 12.76 10.35 2/3 ≤ f < 3/4 18.43 18.11 22.45 23.48 3/4 ≤ f < 1 18.43 22.84 25.51 28.28 f = 1 54.98 43.73 39.29 37.88 No. of Corporations 334 366 395 399 Fraction of Independ en t Di re ctors (ID) 0.85 0.78 0.78 0.79 Fraction with Managing Director (MD) in the Audit Committe e (AC) (%) 19.51 19.70 19.90 22.47 Source: Annual reports of top 500 listed corporations in India, SANSCO. the specification of a minimum size of three, however, the move from the majority to two-thirds rule did not impose any extra independence burden. The only effect of the revised Clause 49 regulations was that “manage- ment directors could now be part of an AC.” Unfortu- nately, what we observe since then is a change in AC composition that seems to be a direct response to the change in the regulation. The steady decline in fully in- dependent AC is also consistent with this change in regulation, as non-executive directors are more likely to be also “independent” directors. Moreover, “non-ex- ecutive” directors could be “independent” directors, or “gray” directors. “Gray” directors are those who are re- lated to the executive directors or have a financial inter- est in the corporation. It should be noted that corpora- tions belonging to “business groups very often have fam- ily members serving as “gray” directors on corporation boards.” After the CG scandals of early 2000, policy-makers all around the world have responded by creating “codes” to improve “ethical” standards in business. A common theme in these guidelines is the “independence of the boards of directors that oversee corporate managers.” For example, in 2002, the NYSE and NASDAQ submitted proposals that required boards to have a majority of in- dependent directors with no material relationships with the corporation (Magilke et al., 2009) [50]. An “inde- pendent” director is defined as someone who has never worked at the corporation or any of its subsidiaries or consultants, is not related to any of the key employees, and does not/did not work for a major supplier or cus- tomer. The rationale for this “policy” recommendation is that board members with close business relationships with the corporation or personal ties with high-ranking officers may not assess its performance dispassionately, or may have vested interests in some business practices. To quote Ravina and Sapienza (2009) [51], “Some criti- cize the emphasis on independent board members, claiming that while they are independent in their scrutiny, they have much less information than insiders. If the ex- ecutives want to act against the interest of the sharehold- ers, they can simply leave outsiders in the dark. Thus, since the independent board members have very limited information, their monitoring could be extremely inef- fective.” Table 5 describe the “fraction” of independent direc- tors on the AC of corporations in India as a measure of AC independence, and how this has changed over the 4 years time period from 2005-2009 for the Indian corpo- rations. This is shown for corporations with different sizes of audit corporations, where the size is 3, 4, 5, or 6. The trends in independence presented in Table 5 for dif- ferent sizes of AC confirms that “the decline in fully in- dependent AC is true for of all sizes, though the decline is more pronounced for an AC which is bigger in size.” Unfortunately, the bigger-size AC has higher “non-com- pliance” with the Clause 49 requirements. For example, in 2008, almost one-third (31.25) of the AC with size of 5 did not have the requisite number of independent di- rectors required under Clause 49. Undoubtedly, an AC plays a “vital” role in ensuring the independence of the audit process. In a recent study conducted by Sharma et al., (2011) [52], the author con- cludes as: “This study is the first to demonstrate that an AC can moderate threats to auditor independence thus, protecting the quality of financial reporting.” To main- tain integrity of their monitoring function, an AC is re- quired to perform their responsibilities “diligently”. Be- cause diligence is extremely difficult to observe directly, research uses an AC meeting “frequency” as a proxy for diligence (Raghunandan and Rama, 2007) [37]. Prior research by Vineeta Sharma et al., (2009) [53], however, focuses on the consequences of an AC meetings and very clearly demonstrates “greater” meeting frequency is usu- Copyright © 2012 SciRes. ME  M. L. BHASIN 865 ally associated with a “reduced” incidence of financial reporting problems, and “greater” external audit quality. SEBI’s Clause 49 requires the AC “to have, at least, 4 meetings per year with not more than four months of gap between two successive meetings.” Accordingly, Table 6 (shown below) presents the distribution of corporations according to the number of meetings held. It can be very clearly observed that “there is a steady improvement in compliance with this requirement; only 6.28 percent of the corporations holding less than 4 meetings in 2008- 09.” Moreover, the “average” number of meetings held is nearly five (4.82) in the last two years, namely 2007-08 and 2008-09 respectively. It appears that many corpora- tions are “more” frequently holding their meetings, as per their individual requirements, and were not simply fol- lowing the “dictates” of the law. As per the “spirit” of the SEBI’s listing requirements, an AC needs to meet at appropriate times throughout the year, thus, ensuring that they have enough time to discuss various issues fully. While AC meetings are “occurring more frequently and for longer periods, chairs should ensure the AC has time to reflect on issues and not just Table 5. Trends in audit committee indepe nde nce: distribution of corporations. Size = 3 Size = 4 Fraction of Independent Directors 2005 2006 2007 2008 2005 2006 2007 2008 f < 2/3 7.41 7.73 8.50 6.53 6.06 15.97 10.29 9.72 2/3 ≤ f < 3/4 28.04 32.04 39.50 42.21 0.00 0.00 0.00 0.00 3/4 ≤ f < 1 0.00 0.00 0.00 0.00 48.48 52.10 61.76 62.50 f = 1 64.55 60.22 52.00 51.26 45.45 31.39 27.94 27.78 No. of Firms 189 181 200 199 99 119 136 144 Size = 5 Size = 6 2005 2006 2007 2008 2005 2006 2007 2008 f < 2/3 23.08 30.30 38.46 31.25 11.11 28.57 16.67 15.38 2/3 ≤ f < 3/4 0.00 0.00 0.00 0.00 33.33 35.71 58.33 61.54 3/4 ≤ f < 1 50.00 51.52 38.46 59.38 0.00 21.43 8.33 15.38 f = 1 26.92 18.18 23.08 9.38 55.56 14.29 16.67 7.69 No. of Firms 26 33 39 32 9 14 12 13 Source: Annual reports of top 500 listed corporations in India, SANSCO. Table 6. Meetings held by an audit committee (AC)—distribution of corporations. Year No. of Meetings Held 2005 2006 2007 2008 0 0.93 0.56 1.03 0.50 1 0.62 3.36 1.28 0.25 2 2.17 1.96 1.28 1.01 3 11.46 6.16 3.59 4.52 4 39.94 43.14 44.10 45.23 5 24.46 23.81 25.13 26.88 6 9.91 11.48 12.31 11.31 7 10.53 9.52 11.28 10.30 Average No. of Meetings Held 4.67 4.62 4.83 4.82 Number of Corporations 323 357 390 398 Source: Annual reports of top 500 listed corporations in India, SANSCO. Copyright © 2012 SciRes. ME  M. L. BHASIN 866 comply with legal requirements.” Undoubtedly, an im- portant issue with respect to meetings is the “duration” of the AC meeting, and the “preparation-time” that is given to the AC members to have “meaningful” discussions about the financial operation of the corporations. For instance, FICCI and Thornton (2009) [54] conducted a CG review of 500 mid-sized Indian corporations which show that “in 50 percent of the corporations AC meetings lasted for less than two hours, while in only 9 percent of the corporations did the meetings went beyond four hours. The majority of the corporations gave an “average” preparation time of up to 7 days to the AC members in terms of mailing them the agenda of the meetings, while only 6 percent gave time of more than two weeks.” An important dimension of an AC “effectiveness” that has gained the attention of regulators and academics is the “financial expertise” of the AC members. However, both the SOX and SEBI’s Clause 49 mandates the dis- closure of whether or not an AC includes a “financial” expert. However, the operationalization of who is a fi- nancial expert was and still is a controversial issue. For example, Krishnan and Visvanathan (2008) [55] have argued that effective AC members are those who have “general management” experience rather than those who have an “accounting or financial” background. The SEC, initially, proposed a “narrow” definition to include only accounting financial experts—that is, directors with ex- perience as a CPA, auditor, CFO, controller, or chief accounting officer. However, subsequently the SEC de- fined financial expert “broadly” to include non-account- ing financial experts, such as directors with experience as a CEO or president. Was the SEC correct in defining financial experts to include both accounting and non- accounting experts? Because an AC is the ultimate “monitor” of the financial reporting process, an AC fi- nancial expertise is a key determinant of its “effective- ness”. However, Krishnan and Lee (2009) [56] in another study found that “firms with higher litigation-risk are more likely to have an accounting financial expert on their AC. This association occurs for firms with rela- tively strong governance but not for those with weak governance.” Additional characteristics of an AC for the 500 top- listed corporations in India are presented in Table 7 for the financial year 2008-09, which presents key measures of AC “quality” that have been the focus of reform initia- tives. Among these are: 1) the presence of members with accounting degree; 2) the number of directorships held by an independent director; 3) the tenure of the inde- pendent director; and 4) the mean age of independent director serving on the AC. While an AC independence is of paramount importance for ensuring the integrity of the financial reporting process, there is a growing recog- nition that “what is perhaps more important is the finan- cial literacy and commitment of the AC members to dis- charge the various functions entrusted to them by the law.” As Dhaliwal et al., (2010) [57] succinctly puts it: “While SOX proposes a “narrow” definition of financial expertise, to include individuals with experience in ac- counting or auditing, the SEC controversially adopted a “broader” definition of financial expertise that includes accounting and certain types of non-accounting (finance and supervisory) financial expertise.” Motivated by the SOX requirement that “public” companies disclose whether they put a financial expert on their AC, we test Table 7. Audit committee characteristics (sample means): 2008-2009. Various Characteristics of an Audit Committee Mean Score Size of Audit Committee (Nos.) 3.65 Size of Board of directors (Nos.) 8.92 Audit Committee has a member with an accounting degree (%) 63.00 Board of directors has a member with an accounting degree (%) 95.00 Number of Audit Committee members with an accounting degree (Nos.) 1.35 Number of Board of director members with accounting degree (Nos.) 2.78 Percentage of Audit Committee members with an accounting degree (%) 40.13 Percentage of Board of director members with an accounting degree (%) 31.82 Total Number of directorships of independent directors serving in the AC (Nos.) 2.61 Median tenure of independent directors serving in the Audit Committee (Yrs.) 6.53 Median age of independent directors serving in the Audit Committee (Yrs.) 58.29 Source: Annual reports of top 500 listed corporations in India, SANSCO; directors database, Bombay stock ex- change. Copyright © 2012 SciRes. ME  M. L. BHASIN 867 whether the market reacts favorably to the appointment of directors with financial expertise to the AC. We find a positive market reaction to the appointment of account- ing financial experts assigned to an AC but no reaction to non-accounting financial experts assigned to AC, consis- tent with accounting-based financial skills, but not broader financial skills, improving the AC ability to en- sure high-quality financial reporting (Firth and Rui, 2007) [58]. According to SEBI’s Clause 49, “All members of an AC shall be financially literate and at least one mem- ber shall have accounting or related financial manage- ment experience.” For example, Bindal (2011) [59] very appropriately pointed out, “While Clause 49 does not require all AC members to possess accounting degrees, it can be hardly imagined that an AC will be able to do justice to its role without any of its members having a formal training on the complexity of the accounting process and the various accounting and auditing stan- dards that confront today’s corporations.” There is no doubt that all “fresh-appointed” AC members need a “robust” orientation-program, allowing them to under- stand their role and the corporation’s financial reporting process, so that they can “add” value to the AC sooner. In addition, Johnstone et al., (2011) [60] very strongly observes as: “Internal controls have long been recognized as important in ensuring high-quality financial report- ing.” The AC is formed to regularly review processes and procedures to ensure the effectiveness of internal control systems so that the accuracy and adequacy of the reporting of financial results is maintained at high-level at all times. To discharge their responsibility, it is impor- tant for the members of an AC to have “formal” knowl- edge of accounting and financial management, or ex- perience of interpreting financial statements. The Listing Agreement (Clause 49) requires “all members of an AC shall be financially literate and at least one member shall have accounting or related financial management exper- tise.” Clause 49, by way of explanation, defined the term “financially” literate as “the ability to read and under- stand basic financial statements, e.g., balance sheet, profit and loss account and statement of cash flows. Fur- ther, a member will be considered to have accounting or related financial management expertise if he/she pos- sesses experience in finance or accounting, or requisite professional certification in accounting, or any other comparable experience or background which results in the individual’s financial sophistication, including being or having been a chief executive officer, chief financial officer or other senior officer with financial oversight responsibilities.” Unfortunately, the explanations given above are not free from some ambiguity. Table 7 shows that 63 percent (about two-thirds) of the top 500 Indian listed corporations had an AC with at least one member with an accounting degree. However, where an AC did not have a member with an accounting knowledge, it was very likely the board had one such a member. On an av- erage, 40.13 percent of the AC members had an ac- counting degree. Similarly, percentage of board members with an accounting degree was 31.82. However, “me- dian” tenure and “age” of independent directors serving in the AC during 2008-09 was 6.63 and 58.29 years, re- spectively. Another fundamental condition which needs to be ful- filled by all AC members is their ability to devote “suffi- cient-time” to effectively discharge all the functions as- signed to them by law (Ward, 2009) [61]. For instance, Emmerich et al., (2006) [62] advises as: “To be sure, prospective AC members must understand that more will be required of them—more time and more efforts—than may have been demanded in the past. It seems clear that all aspects of the “legal” system are likely to place a heavier emphasis on independence and to demand greater attention and involvement (that is, greater commitment) from corporate directors in general, but especially from AC members, than in the past.” The legal standards for measuring the independence and the duties of an AC member, by-and-large, have not changed. As we have seen, the current SEC regulations discourage directors with more than three directorships to be members of an AC because “over the commitment that comes with too many directorships might hamper the ability of the di- rectors to dutifully carry out all the functions expected of him/her.” In this context, it is encouraging to note from Table 7 that the “average” number of directorships held by the independent directors in the top 500 listed Indian corporations during 2008-09 was 2.61, less than three. This is a welcome development and will hopefully per- sist in the coming years. In this context, Zabihollah et al., (2003) [63] states: “Having the right directors on the AC—with mandated independence and financial literacy combined with integrity, healthy skepticism, knowledge of the corporation and industry, and the courage to chal- lenge decisions—is an important driver of AC effective- ness.” In the past, some Western researchers have examined the relation between CG characteristics and the audit fees. Strong governance could increase the demand for audit- ing (thereby increasing fees) and/or reduce auditors’ as- sessments of risk (thereby reducing fees). For example, Krishnan and Visvanathan (2009) [55] in their study found that “audit fees are negatively associated with ac- counting expertise on the AC but only in corporations with strong governance. Audit fees increase with board size, board meetings, AC meetings, and CEO duality. Also, the relation between audit fees and AC accounting expertise is negative, when earnings management risk is low, but positive when the earnings management risk is high.” Thus, an AC with accounting experts appears to Copyright © 2012 SciRes. ME  M. L. BHASIN 868 demand more “extensive” auditing when “risk” is higher. Conversely, research by Lassila et al., (2010) [64] finds that “the use of the auditor for tax services is positively related to CG strength—composite of board size, board independence, audit committee size, audit committee in- dependence, shareholders’ rights, and institutional owner- ship.” Now, moving over to issues relating to auditor inde- pendence and non-audit fees, Table 8 presents some relevant statistics for the top 500 Indian listed corpora- tions for two years, viz., 2006-07 and 2007-08. It can be observed that in 80 and 79.40 percent of the corporations in 2006-07 and 2007-08 respectively, the statutory audi- tor was also rendering non-audit services. During these two years, there is virtually no significant change. Com- parative figures available for the US in 2000, which pre- dates the passage of the SOX Act, shows that out of the 16,700 corporations, which were registered with the SEC, only 4100 (or 25 percent) purchased non-audit services from the external auditor. According to a study con- ducted by Abbott et al., (2007) [65], “Our results are consistent with firms with independent, active, and ex- pert AC being less likely to outsource routine internal auditing activities to the external auditor. However, the outsourcing of non-routine internal audit activities, such as, special projects and EDP consulting are not nega- tively related to effective AC.” Indeed, interesting differences surface during 2007-08 when the “aggregate” picture is broken down into “own- ership” groups. Two important observations can be made on Table 8. First of all, nearly 85 percent of corporations belonging to “business” groups (either domestic or for- eign) buy “non-audit” services from the “statutory” audi- tor. For the same period, the percent for “standalone” firms, who bought “non-audit” services from the “statu- tory” auditor was 70.54 (domestic) and 62.96 (foreign), respectively. Secondly, the percentage of “foreign” group corporations buying “non-audit” services shows an “in- crease” (from 84.21 to 88.24) from 2007 to 2008, while “Indian” standalone corporations exhibit a “decline” from 75.73 to 70.54 percent. Furthermore, Table 8 also presents the extent of non- audit fees relative to audit fees earned by auditing firms for top 500 listed Indian corporations. Current regula- tions require that “non-audit fees not to exceed audit- fees.” As the data in the table demonstrates, “the extent of non-audit fees in both years was well below the statu- tory limit.” More encouragingly, the extent of non-audit to audit fees has declined for all corporations under study from 46.67 percent in 2006-07 to 35.65 in 2007-08. De- composition by ownership groups shows that extent of non-audit fees (56.38 percent) to be much higher for for- eign corporations than for domestic corporations (34.88 percent) in 2007-08. On an average, the ratio of non- Table 8. Non-audit services and non-audit fees. Services rendered by Auditors 2006-07 2007-08 Corporations where Auditors rendered Non-audit Services (%) (%) Indian Business Groups 83.90 85.15 Indian Standalone 75.73 70.54 Foreign Business Groups 84.21 88.24 Foreign Standalone 70.37 62.96 All Corporations 80.00 79.40 Non-audit to Audit Fees by Ownership Groups (Median) (%) (%) Indian Business Groups 42.00 34.88 Indian Standalone 39.54 26.30 Foreign Business Groups 53.92 56.38 Foreign Standalone 79.42 86.89 All Corporations 46.67 35.65 Non-audit to Audit Fees by Size (Median) (%) (%) Small (<750 crores) 48.33 35.42 Medium (>750 and <3400 crores) 41.43 33.50 Large (>3400 crores) 55.36 44.44 All Corporations 46.67 35.65 Source: Annual reports of top 500 listed corporations in India, SANSCO. audit to audit fees were 42 percent in 2006-07 compared to 53.92 percent for foreign group corporations and 79.42 percent for foreign standalone corporations. More strik- ingly, while “domestic” corporation exhibits a decline in the non-audit fee percentage from 42 to 34.88 percent, with the decline being more pronounced for “standalone” corporations (from 39.54 to 26.30 percent), “foreign” corporations exhibit a marginal increase from 53.92 to 56.38 percent. However, there was a sharp increase from 79.42 to 86.89 percent in the case of foreign standalone firms. Furthermore, decomposition with respect to “size” shows that the extent of non-audit fees to be higher (55.36 and 44.44 percent) in the “larger” bigger corpora- tions for both years. However, all corporations, irrespec- tive of their size, showed a significant decline in non- audit fee from 46.67 to 35.65 percent in 2008. To sum up, the above analysis of the empirical trends about an AC, and auditor independence in the context of top 500 listed Indian corporations present a “mixed” pic- ture. We observe an increasing trend in compliance with the Clause 49 regulations; there is a tendency to gravitate to the minimum standards with respect to an AC compo- sition. However, there is a little “voluntary” move to Copyright © 2012 SciRes. ME  M. L. BHASIN 869 compose a “fully” independent AC. Instead, what we observe is “an increasing trend of “inside” management being present in the AC. Compared to this, the trends in auditor independence are better. The data with respect to non-audit services and extent of non-audit fees tend to suggest that domestic standalone corporations, which are also likely to be relatively smaller in size, are very stead- ily moving towards the notion of auditor independence envisaged under the regulations. 7. Conclusions With the rapidly growing instances of corporate failures and the rising dissatisfaction with the functioning of the corporations gave rise to the need of reassuring the stakeholders. As a result, the emphasis was laid on im- proving the CG practices across the globe. Post-Satyam scandal in India, however, the investors’ confidence in the CG system is VERY low. Undoubtedly, in India the concept of CG has already been embedded in the statutes, viz., Company Act, 1956 and SEBI’s Clause 49 of the listing agreement. However, the listing agreement is “a weak instrument, as its penal provisions are not hurting enough.” Several “regional” stock exchanges, where a large number of corporations are listed, lack effective organization and skills to monitor effective compliance with CG requirements as stipulated by SEBI. Moreover, a vast majority of corporations, which are not listed on any of the stock exchanges, will remain outside the pur- view of SEBI’s measures. It is, therefore, desirable that the Companies Act needs to be amended suitably for enforcing “good” CG practices in India. Being “manda- tory” under Section 292A of the Company Act, 1956 and Clause 49 of the listing agreement, “an AC can be a fa- cilitator of board to implement, monitor and continue good CG practices for the benefit of the corporation and its stakeholders.” Moreover, an AC is empowered to function, on behalf of the board of directors, by assuming an important “oversight” role in the CG intended to pro- tect investors and thereby ensure corporate accountability. Besides, an AC has “oversight” responsibility over the CG, the financial reporting process, internal control structure, internal audit functions, and external audit ac- tivities. Over the past 70 years, the AC concept has grown from a committee designed to nominate and arrange the deal of engagement with the auditor to a committee re- sponsible for overseeing the integrity of the corporation’s financial reporting process. As the responsibilities of an AC grew, so did the number of countries “mandating” the use of an AC in corporate boardrooms. No doubt, after the passage of the Sarbanes-Oxley in July of 2002, the number of major capital market countries requiring an AC has more than tripled. Even though the member- ship requirements for an AC vary, it is very clear that the majority of major capital market countries view an AC as a critical component of the financial reporting process. As part of this research study, we examined top 500 listed corporations in India in terms of market capitalize- tion as on March 31, 2008. Accordingly, we summarized the trends about various characteristics of an AC, their size, composition, activity, as well as, the extent of non- audit services provided by the auditors in the Indian cor- poration sector from 2005-06 to 2008-09. Results of this study indicate that all corporations examined have adopted AC charters that are published at least once every three years. In addition, an AC should have in their charters the oversight of “disaster” planning. All studied corporations currently include a report of an AC in their annual report or proxy statement. The majority of an AC composition, structure, meetings, and qualification are in compliance with the requirements of the SEBI and or- ganized stock exchanges. The report of an AC is in- tended to ensure that financial statements are legitimate, the audit was thorough, and the auditors have no flagrant conflicts of interest that may jeopardize their objectivity, integrity, and independence. It is expected that more ef- fective AC disclosures in conformity with the provisions of the Clause 49 of listing rules and Sarbanes-Oxley Act of 2002 (e.g. charter, report) improve the trust and con- fidence in CG, the financial reporting process, and audit functions. However, the above analysis of the empirical trends regarding an AC, and auditor independence presents a “mixed” picture. On the one hand, we observe an “in- creasing” trend in compliance with the Clause 49 regula- tions. However, at the very same time, we also observe a tendency to gravitate to the “minimum” standards with respect to an AC composition. Moreover, there is a little “voluntary” move to compose a fully-independent AC. Instead, what we observe is an increasing trend of “in- side” management being present in an AC. Compared to this, the trends in auditor independence are far better. The data with respect to non-audit services and extent of non-audit fees tend to suggest that “domestic standalone corporations, which are also likely to be relatively smaller in size, are very steadily moving towards the notion of auditor-corporation independence envisaged under the regulations.” Without any hesitation, we per- sonally feel this is a very welcome development on the front of AC and auditor independence in the Indian cor- porate sector. These results should be of direct interest to policy makers and stock exchange regulators throughout the world, who seek to enhance auditor independence by means of general regulatory change. Currently auditor independence in India, especially with respect to rendering non-audit services and presence of conflict of interest, is largely dependent on “self- Copyright © 2012 SciRes. ME  M. L. BHASIN 870 regulation”. The Companies Act of 1956 has little to of- fer in this regard. Under the existing regulations, there are many unresolved CG issues with respect to auditor and AC independence in India. The Companies Bill (2009) has incorporated many of these recommendations. For investors to have confidence in the independence of the auditor, the Bill needs to be enacted quickly into law. However, notwithstanding the passage of the Corpora- tions Bill, some issues that have not been incorporated into the Bill will remain as a matter of concern. Unfortu- nately, there is a lot of resistance from industry circles for further reforms as evidenced from dropping of the Bill and revision of clause 49 on their demand. If this trend continues, the useful contributions from recent committees and the time spent by their expert members in this regard will not reap any benefits. It is essential for the Indian corporate-sector to accept and continue with the reforms that are demanded by the challenges of the new millennium. If it is operationally difficult to do fur- ther modifications to the statutes in the immediate future, then the respective Stock Exchanges should explore the possibility of incorporating these additional standards of independence in their Listing Agreement. The series of accounting scandals have intensified pressure from stakeholders and regulators on an AC to do the jobs for which they were hired. Though most corpo- rations have an AC, their role has been “limited” due to “lack of expertise and time.” An “active” AC is impor- tant because it indicate the commitment to the issues of interest because of the reports it release about the active- ties undertaken during the financial year and the efforts made to ensure adequate internal control. Of equal im- portance, auditor independence can be safeguarded if an AC were composed of a majority of independent and non-executive directors and this might indicate that their independent status would contribute to auditor inde- pendence through bridging communication networks and neutralizing any conflict between the management and the auditor (Cohen et al., 2007) [66]. Thus, an AC “mechanism” can go a long-way in enhancing the credi- bility of the financial disclosures of a corporation and promoting transparency. Those who do not require an AC in listed corporations are in a “shrinking” minority. As a result, corporate managers in “developing” coun- tries (like India), who are considering a move into a “lar- ger” capital market will most likely need to establish an AC before their stock may be traded on a listed market. To sum up, adequate, relevant and high-quality dis- closures are one of the most powerful tools available in the hands of “independent” directors, shareholders, regu- lators, and outside investors to monitor the performance of a corporation. This is particularly important for an emerging economy like India, where there is “insider” dominance. To this extent, “measures that strengthen auditor independence and enhance the powers, functions, and the independence of an AC will be crucial in the governance of the Indian corporations.” Governance “risk” is a key determinant of market-pricing of “listed” securities. A high perceived “independence quotient” of a corporation’s auditing process can be reassuring to out- side shareholders that can help reduce the risk premium of raising capital, thereby providing a strong business case for strengthening both an auditor and the AC inde- pendence. No doubt, it is essential for the Indian corpo- rations to accept and continue with the CG reforms that are “demarcated” by the challenges of the “new” millen- nium. REFERENCES [1] A. Dey, “Corporate Governance and Agency Conflicts,” Journal of Accounting Research, Vol. 46, No. 5, 2008, pp. 1143-1181. [2] J. Cohen, G. Krishnamoorthy and A. Wright, “Form ver- sus Substance: The Implications for Auditing Practices and Research of Alternative Perspectives on Corporate Governance,” Auditing: A Journal of Practice & Theory, Vol. 27, No. 2, 2008, pp. 181-198. [3] R. Aguilera and A. Cuervo-Cazurra, “Codes of Good Governance,” Corporate Governance: An International Review, Vol. 17, No. 3, 2009 pp. 376-387. doi:10.1111/j.1467-8683.2009.00737.x [4] C. P. Agoglia, T. S. Doupnik and G. T. Tsakumis, “Prin- ciple-Based versus Rules-Based Accounting Standards: The Influence of Standard Precision and Audit Commit- tee Strength on Financial Reporting Decisions,” The Ac- counting Review, Vol. 86, No. 3, 2011, pp. 747-767. doi:10.2308/accr.00000045 [5] A. Klein, “Audit Committee, Board of Director Charac- teristics and Earnings Management,” Journal of Account- ing and Economics, Vol. 33, No. 3, 2002, pp. 375-400. doi:10.1016/S0165-4101(02)00059-9 [6] A. Dignam, “Capturing Corporate Governance: The End of the UK Self-regulating System,” International Journal of Disclosure and Governance, Vol. 4, No. 1, 2007, pp. 24-41. doi:10.1057/palgrave.jdg.2050046 [7] J. Caskey, V. Nagar and P. Petacchi, “Reporting Bias with an Audit Committee,” The Accounting Review, Vol. 85, No. 2, 2010, pp. 447-481. doi:10.2308/accr.2010.85.2.447 [8] M. Beasley, J. V. Carcello, D. R. Hermanson and T. L. Neal, “The Audit Committee Oversight Process,” Con- temporary Accounting Research, Vol. 26, No. 1, 2009, pp. 65-122. doi:10.1506/car.26.1.3 [9] J. R. Fichtner, “The Recent International Growth of Man- datory Audit Committee Requirements,” International Journal of Disclosure and Governance, Vol. 7, No. 3, 2010, pp. 227-243. doi:10.1057/jdg.2009.29 [10] United Nations Conference on Trade and Development, “Guidance on Good Practices in Corporate Governance Disclosure,” New York, 2006. [11] R. Romano, “The Sarbanes-Oxley Act and the Making of Copyright © 2012 SciRes. ME  M. L. BHASIN 871 Quack Corporate Governance,” Yale Law Journal, Vol. 114, No. 7, 2005, pp. 1521-1611. [12] R. A. Prentice and D. B. Space, “Sarbanes-Oxley as Quack Corporate Governance: How Wise Is the Received Wisdom?” Georgetown Law Journal, Vol. 95, No. 6, 2007, pp. 1843-1909. [13] M. Knapp, “An Empirical Study of Audit Committee Support for Auditors Involved in Technical Disputes with Client Management,” Accounting Review, No. 62, No. 3, 1987, pp. 578-588. [14] V. Beattie, “Lifting the Lid on the Use of Content Analy- sis to Investigate Intellectual Capital Disclosures,” Ac- counting Forum, Vol. 31, No. 2, 2007, pp. 129-163. doi:10.1016/j.accfor.2007.02.001 [15] J. J. Wild, “The Audit Committee and Earnings Quality,” Journal of Accounting, Auditing and Finance, Vol. 11, No. 2, 1996, pp. 247-276. [16] J. Goodwin-Stewart and P. Kent, “Relation between Ex- ternal Audit Fees, Audit Committee Characteristics and Internal Audit,” Accounting & Finance, Vol. 46, No. 3, 2006, pp. 387-404. doi:10.1111/j.1467-629X.2006.00174.x [17] M. L. DeFond, R. N. Hann and X. Hu, “Does the Market Value Financial Expertise on Audit Committees of Boards of Directors?” Journal of Accounting Research, Vol. 43, No. 2, 2005, pp. 153-195. doi:10.1111/j.1475-679x.2005.00166.x [18] P. Dechow, R. Sloan and A. Sweeney, “Causes and Con- sequences of Earnings Manipulation: An Analysis of Firms Subject to Enforcement Actions by the SEC,” Con- temporary Accounting Research, Vol. 13, No. 1, 1996, pp. 1-36. doi:10.1111/j.1911-3846.1996.tb00489.x [19] S. M. Williams and G. Tower, “Audit Committee Fea- tures and Earnings Management: Further Evidence,” Conference Proceedings 25th McMaster World Congress, Hamilton, 2004. [20] D. A. McMullen, “Audit Committee Performance: An Investigation of the Consequences Associated with Audit Committee,” Auditing: A Journal of Practice & Theory, No. 15, 1996, pp. 87-103. [21] M. Beasley, “An Empirical Analysis of the Relations between the Board of Director Composition and Financial Statement Fraud,” Accounting Review, Vol. 71, No. 4, 1996, pp. 443-465. [22] M. C. Pucheta-Martinez and C. de Fuentes, “The Impact of Audit Committee Characteristics on the Enhancement of the Quality of Financial Reporting: An Empirical Study in the Spanish Context,” Corporate Governance: An International Review, Vol. 15, No. 6, 2007, pp. 1394- 1412. doi:10.1111/j.1467-8683.2007.00653.x [23] J. Al-Mudhaki and P. L. Joshi, “The Role and Functions of Audit Committees in the Indian Corporate Governance: Empirical Findings,” International Journal of Auditing, Vol. 8, No. 1, 2004, pp. 33-47. doi:10.1111/j.1099-1123.2004.00215.x [24] S. Agarwal, “Corporate Governance through Audit Com- mittees,” The Chartered Accountant, November, 2006, pp. 733-742. [25] J. Cohen, G. Krishnamoorthy and A. Wright, “Corporate Governance in the Post-Sarbanes-Oxley Era: Auditors’ Experiences,” Contemporary Accounting Research, Vol. 27, No. 3, 2010, pp. 751-786. doi:10.1111/j.1911-3846.2010.01026.x [26] C. S. Vera-Munoz, “Corporate Governance Reforms: Re- defined Expectations of Audit Committee Responsibili- ties and Effectiveness,” Journal of Business Ethics, Vol. 62, No. 2, 2005, pp. 115-127. doi:10.1007/s10551-005-0177-5 [27] J. V. Carcello, D. R. Hermanson and Z. S. Ye, “Corporate Governance Research in Accounting and Auditing: In- sights, Practice Implications, and Future Research Direc- tions,” Auditing: A Journal of Practice & Theory, Vol. 30, No. 3, 2011, pp. 1-31. [28] R. Hinzpeter, R. Zimerman and K. Piddo, “Getting the Deal through Corporate Governance,” Law Business Re- search, London, 2009, pp. 43-47. [29] M. A. Pearson, “A Profile of the ‘Big Eight’ Independ- ence Position,” Baylor Business Studies, Vol. 11, No. 3, 1980, pp. 7-27. [30] R. C. Dockweiler, L. A. Nikolai and J. E. Holstein, “The Effect of Audit Committees and Changes in the Code of Ethics on Public Accounting,” Proceedings of Midwest Annual Meeting, American Accounting Association, Sara- sota, 1986, pp. 45-60. [31] W. P. Lam, “The Development and Significance of Cor- porate Audit Committees,” The CA Magazine, 2000, pp. 3-40. [32] V. Beattie, R. Brandt and S. Fearnley, “Perceptions of Auditor Independence: UK Evidence,” Journal of Inter- national Accounting, Auditing and Taxation, Vol. 8, No. 1, 1999, pp. 67-107. doi:10.1016/S1061-9518(99)00005-1 [33] K. Raghunandan and D. Rama, “Determinants of Audit Committee Diligence,” Accounting Hori zons, Vol. 21, No. 3, 2007, pp. 265-280. doi:10.2308/acch.2007.21.3.265 [34] J. W. Lin, G. Kang and A. Roline, “The Effects of the Blue Ribbon Committee and the Sarbanes Oxley Act of 2002 on the Characteristics of the Audit Committees and the Board of Directors,” Advances in Accounting, Fi- nance and Economics, Vol. 2, No. 1, 2009, pp. 54-70. [35] J. Allen, “Asian Corporate Governance Association: Cor- porate Governance Seminar,” Organized by Chubb Insur- ance and Solidarity, Bahrain, 2008, p. 10. [36] A. Afsharipour, “Corporate Governance Convergence: Lessons from the Indian Experience,” Northwestern Jour- na l of Internati onal Law & Business, Vol. 29, No. 2, 2009, pp. 335-402. [37] Confederation of Indian Industry, “Desirable Corporate Governance: A Code 1997,” 2010, pp. 1-12. www.ciionline. org [38] B. N. Balasubramanian, B. S. Black and V. S. Khanna, “Firm-Level Corporate Governance in Emerging Markets: A Case Study of India,” Northwestern Law & Eco Re- search Paper No. 09-14, 2008, pp. 1-50. [39] Department of Public Enterprises, “Guidelines on Corpo- rate Governance for Central Public Sector Enterprises,” Copyright © 2012 SciRes. ME  M. L. BHASIN Copyright © 2012 SciRes. ME 872 Government of India, New Delhi, 2007. dpe. nic. in/newsite/gcgcpse. pdf [40] M. Kaushik, “How Good Are Company Boards?” Busi- ness Today, 2009. [41] P. T. Giridharan, “The Audit Committee: A Global Per- spective,” The Chartered Accountant, 2004, pp. 621-627. [42] A. Ganguly, “Provisions of Audit Committees in Compa- nies Act Listing Agreement: Need Re-Look,” India Info- line, 2001. www.indiainfoline.com/leggal/feat/prov.html [43] D. Chatterjee, “Audit Committee Observation/Recommen- dations versus Practices as a Compliance of Corporate Governance in India,” DLSU Business & Economics Re- view, Vol. 20, No. 2, 2011, pp. 67-78. doi:10.3860/ber.v20i2.1914 [44] R. Puri, R. Trehan and H. Kakkar, “Corporate Govern- ance through Audit Committee: A Study of the Indian Corporate Sector,” The IUP Journal of Corporate Gov- ernance, Vol. 9, No. 1-2, 2010, pp. 47-56. [45] Securities and Exchange Board of India, “Corporate Go- vernance in Listed Corporations: Clause 49 of the List- ing Agreement,” 2004. http://www. sebi-gov. in/circulars/2004/cfdcir0104. pdf [46] E. M. Heffes, “Audit Committee to CFO: Can We Talk?” Financial Executive, 2007, pp. 29-32. [47] J. Carcello, D. Hermanson and T. L. Neal, “Disclosure in Audit Committee Charters and Reports,” Accounting Ho- rizons, Vol. 16, No. 4, 2002, pp. 291-304. [48] D. Sharma, “When Audit Committees Do Not Stack Up?” New Zealand Management, Vol. 54, No. 4, 2007, pp. 16- 17. [49] J. Sarkar and S. Sarkar, “Auditor and Audit Committee Independence in India,” Working Paper Series under Fi- nancial Sector Regulatory Reforms Project at Indira Gandhi Institute of Development Research, 2010. [50] M. J. Magilke, B. W. Mayhew and J. E. Pike, “Are Inde- pendent AC Members Objective?: Experimental Evi- dence,” The Accounting Review, Vol. 84, No. 6, 2009, pp. 1959-1981. doi:10.2308/accr.2009.84.6.1959 [51] E. Ravina and P. Sapienza, “What Do Independent Di- rectors Know?: Evidence from Their Trading,” Published by Oxford University Press on Behalf of the Society for Financial Studies, 2009, pp. 962-1003. [52] V. D. Sharma, D. S. Sharma and U. Ananthanarayanan, “Client Importance and Earnings Management: The Mod- erating Role of Audit Committees,” Auditing: A Journal of Practice & Theory, Vol. 30, No. 3, 2011, pp. 125-156. [53] V. Sharma, N. Naiker and B. Lee, “Determinants of Audit Committee Meeting Frequency: Evidence from a Volun- tary Governance System,” Accounting Horizons, Vol. 23, No. 3, 2009, pp. 245-263. doi:10.2308/acch.2009.23.3.245 [54] FICCI Grand Thornton Report, “Corporate Governance Review 2009: India 101-500 Technical Report”. http://www.wcgt.in/html/publications/ficci_gt_cgr.php [55] G. V. Krishnan and G. Visvanathan, “Does the SOX Definition of an Accounting Expert Matter?” Contempo- rary Accounting Research , Vol. 25, No. 3, 2008, pp. 827- 857. doi:10.1506/car.25.3.7 [56] J. Krishnan and J. E. Lee, “Audit Committee Financial Expertise, Litigation Risk and Corporate Governance,” Auditing: A Journal of Practice & Theory, Vol. 28, No. 1, 2009, pp. 241-261. [57] D. Dhaliwal, V. Naiker, and F. Navissi, “The Association between Accruals Quality and the Characteristics of Ac- counting Experts and Mix of Expertise on Audit Com- mittees,” Contemporary Accounting Research, Vol. 27, No. 3, 2010, pp. 787-827. doi:10.1111/j.1911-3846.2010.01027.x [58] M. Firth and O. Rui, “Voluntary Audit Committee For- mation and Agency Costs,”’ International Journal of Ac- counting, Auditing and Performance Evaluation, Vol. 4, No. 2, 2007, pp. 142-160. doi:10.1504/IJAAPE.2007.015231 [59] C. M. Bindal, “Audit Committee: Highly Integral to Cor- porate Governance,” Chartered Accountant in Practice, Manupatra Publications, 2011, pp. 1-9. [60] K. Johnstone, C. Li, and K. H. Rupley, “Changes in Cor- porate Governance Associated with the Revelation of In- ternal Control Material Weaknesses and Their Subsequent Remediation,” Contemporary Accounting Research, Vol. 28, No. 1, 2011, pp. 331-383. doi:10.1111/j.1911-3846.2010.01037.x [61] R. D. Ward, “Audit Committee Leaders Face Increasing Workload,” Financial Executives International, Morris- town, 2009, pp. 28-31. [62] A. O. Emmerich, G. N. Racz and J. Unger, “Composition of the Audit Committee: Ensuring Members Meet the New Independence and Financial Literacy Rules,” Inter- national Journal of Disclosure and Governance, Vol. 2, No. 1, 2005, pp. 67-80. [63] R. Zabihollah, O. Kingsley and M. George, “Improving Corporate Governance: The Role of Audit Committee Disclosures,” Managerial Auditing Journal, Vol. 18, No. 6-7, 2003, pp. 530-537. doi:10.1108/02686900310482669 [64] D. R. Lassila, T. C. Omer, M. K. Shelley and L. M. Smith, “Do Complexity, Governance and Auditor Independence Influence Whether Firms Retain Their Auditors for Tax Services?” Journal of the American Taxation Association, Vol. 32, No. 1, 2010, pp. 1-23. doi:10.2308/jata.2010.32.1.1 [65] L. J. Abbott, S. Parker, G. F. Peters and D. V. Rama, “Corporate Governance, Audit Quality and the SOX Act: Evidence from Internal Audit Outsourcing,” The Ac- counting Review, Vol. 82, No. 4, 2007, pp. 803-835. doi:10.2308/accr.2007.82.4.803 [66] J. Cohen, L. M. Gaynor, G. Krishnamoorthy and A. Wright, “Auditor Communications with the AC and the Board of Directors: Policy Recommendations and Op- portunities for Research,” Accounting Horizons, Vol. 21, No. 2, 2007, pp. 165-187. doi:10.2308/acch.2007.21.2.165