Open Journal of Social Sciences

Vol.03 No.10(2015), Article ID:60789,17 pages

10.4236/jss.2015.310025

Fostering Regional Integration in Africa: Lessons from Sasol Natural Gas Project between South Africa and Mozambique

Albert-Enéas Gakusi1, David Sartori2, Joe Asamoah3

1Independent Development Evaluation (IDEV), African Development Bank, Abidjan, Côte d’Ivoire

2Center for Industrial Studies, Milan, Italy

3 EnerWise Africa, Accra, Ghana

Email: a.gakusi@afdb.org, sartori@csilmilano.com, joasa2@yahoo.com

Copyright © 2015 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 6 October 2015; accepted 26 October 2015; published 30 October 2015

ABSTRACT

This paper contains the results of a case study aiming at assessing the extent to which the public- private Sasol Natural Gas Project between South Africa and Mozambique contributes to fostering regional cooperation and integration and to identifying operational challenges that are specific for multinational operations. The core objective of the project is to develop the previously untapped natural gas resources available in Mozambique in order to supply and convert Sasol’s coal-burning petrochemical plants to natural gas. This objective fits both governments’ goals to develop gas market for Mozambican and to diversify the energy supply mix for South African market. Also, the project serves broader development objectives of strengthening the bilateral economic ties between Mozambique and South Africa; thus, contributing to regional cooperation and integration. The paper draws on project documentation including project completion report and supervision reports carried out by donors, as well as on results of a field mission in South Africa and Mozambique between 26 November and 9 December 2011.

Keywords:

Case Study, Regional Cooperation and Integration, Effectiveness, Efficiency, Impacts, Sustainability

1. Introduction

The case study aims to assess the extent to which the Sasol Natural Gas Project (hereafter the project) is relevant and effective in fostering the cooperation and integration of the economies of Mozambique and South Africa. It looks at the sustainability of the benefits of the project and it assesses if these are equitably shared. The study also assesses the project efficiency. It seeks to understand the factors of the success and the lessons that can be learnt from this experience. The study draws on a review of project documents including the appraisal reports, supervision mission reports and the project completion report, as well as other documents available including reports by different donors. It is also based on the results of a field mission undertaken in the Republic of South Africa and in Mozambique between 26 November and 9 December 2011.

The mission team carried out individual interviews with the senior management of the project sponsor, Sasol Ltd., and other stakeholders including senior officials of the Development Bank of Southern Africa, one South African and two Mozambican governmental agencies operating in the field of petroleum and gas, and the senior staff of the Extractive Industries Transparency Initiative in Mozambique. Interviews were backed by a checklist of evaluation questions (Appendix 3).

The mission team visited the project site in Temane, Mozambique, and three social projects for local communities in the province of Inhassoro in Mozambique: a school, a clinic and a borehole. It carried out a discussion with the employees to gather their opinions on the effects of these projects on local communities. For reasons of confidentiality, some information could not be accessed including those concerning profits of the private shareholders.

The paper describes the project’s context including its regional cooperation and integration dimension, its objectives, institutional arrangements, cost and management. It then assesses the project’s performance against the evaluation criteria of relevance, quality at entry, effectiveness, efficiency and sustainability. Finally, it concludes and draws the main lessons.

2. Regional and Country Context of the Energy Sector

While Mozambique has vast energy resources―hydropower, gas and coal―which have considerable potential for domestic energy-intensive industry and export, only about 15% of households have a power connection. This is in part a consequence of the difficulty in exploiting its natural resources, especially, the high cost of generation and distribution [1] . More specifically, Mozambique faces four critical challenges:

- Lack of human resource capacity at senior managerial level in the oil and gas extractive industry.

- Lack of an energy market due to very limited domestic demand.

- Absence of private investors on the supply side.

- Thin financial markets with difficult access to credit.

For South Africa, much of the manufacturing sector is still linked to mining activities, mineral extraction and metal production, which are energy-intensive and rely on the availability of comparatively cheap electricity generation from coal [2] . Today, South Africa faces the challenge of the non-sustainability of using coal for power generation in the long term, and the need to rethink its energy supply mix by shifting to more diversified sources and cleaner forms of energy [3] .

Both countries have developed significant initiatives to reform and regulate their energy sectors. Mozambique has put in place a modern legislative framework for the power sector. The Energy Policy (1998) and the Energy Sector Strategy (2000) encourage more efficient management of energy resources. Today, the country’s upstream oil industry is controlled by the parastatal agency Empresa Nacional de Hidrocarbonetos de Moçambique (ENH), which has exclusive rights to explore and develop oil and gas in Mozambique, and is permitted to exercise these rights in association with foreign investors [4] .

Mozambique has adhered to the Extractive Industries Transparency Initiative (ITIE) launched in October 2008. The ITIE is a voluntary multi-stakeholder initiative that sets global standards for companies to publish what they pay and for governments to disclose what they receive from extractive industries, thus promoting greater transparency and accountability (see www.itie-mozambique.org). This also reflects the country’s efforts to improve governance in the extractive sector. While the legislative framework is considered largely in place, the implementation and enforcement of the policy to achieve the expected development goals appear to lag behind [5] .

In 1998, the White Paper on Energy Policy advocated the South African Government’s commitment to develop a gas industry to ensure security of supply [6] . A legislative framework was further developed to catalyse the establishment of a gas industry, which is underpinned by the Gas Act of 2001. From the Gas Act, and through the National Energy Regulator Act of 2004, the National Energy Regulator of South Africa (NERSA) was created. Regulations associated with the Gas Act were finally established in 2007.However, the development of the legislative framework has not yet been translated in corresponding evolutions in the gas industry [7] [8] .

Source: http://www.nersa.org.za/

The piped-gas industry in South Africa is dominated by Sasol Ltd., which is the only gas distributor. Sasol is an integrated energy and chemicals company predominantly based in South Africa, but with manufacturing and marketing operations worldwide, using coal, oil and gas as feedstock in the production of liquid fuels, fuel components and chemicals. In 2003, about 40% of South Africa’s demand for liquid fuel from coal, crude oil and gas was supplied by Sasol [9] . The Sasol Group comprises the South African Energy cluster made up of Sasol Mining, Sasol Gas, Sasol Oil and Sasol Synfuels, and the Sasol International Energy cluster comprising Sasol Petroleum International and Sasol Synfuels International.

In the late 1990s, while the legislation for the regulation of the piped-gas industry was still under discussion, Sasol entered into negotiations with the governments of South Africa and Mozambique to source natural gas from Mozambique. As a result, a special regulatory dispensation was issued, making Sasol the only major supplier of gas in South Africa [10] .

3. Project Objectives and Description

The core objective of the project is to develop the previously untapped natural gas resources available in Mozambique in order to supply Sasol’s petrochemical plants. The project consists of two distinct, but integrated components:

- The upstream component: gas field development and gas production;

- The transmission component, comprising a gas pipeline from Mozambique to the Republic of South Africa.

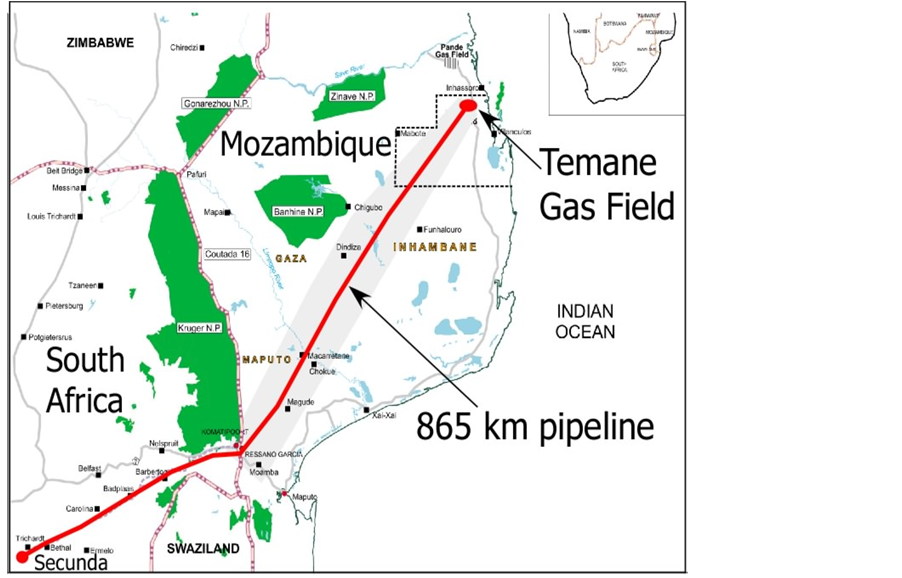

The upstream component entailed developing the gas fields of Temane and Pande, in Mozambique’s Inhambane province, and the associated processing facilities (see the map in Appendix 1). A Central Processing Facility (CPF) has been constructed at Temane. The natural gas is gathered through a 177 km network and processed at the CPF, before transportation to downstream customers (Figure 1). The CPF consists of gathering networks linked to the wells, drying, compression and condensate removal facilities. The project is designed to recover electricity and heat so that the facilities are self-sustaining, including a potential for electricity generation to supply the local market. The upstream component includes associated infrastructures, such as roads, utilities, workshops, accommodation units and offices. The project comprises different development phases and is currently under expansion.This entails installing additional equipment at the CPF to process increased gas volumes and to manage pollution, including a new incinerator, landfill site and sewage treatment plant [11] .

The transmission component consisted in developing an865km 26-inch diameter high-pressure steel pipeline between the gas fields and Sasol’s petrochemical complex at Secunda, South Africa. The pipeline is buried one metre below the ground surface and has a design capacity to deliver 120Million Giga Joules per year (MGJ/year) of gas. The 525 km Mozambican section starts at the CPF and crosses the Mozambican-South African border near the town of Ressano Garcia; the South African portion then continues to Secunda, where it feeds into Sasol’s gas distribution network and plants [12] .

The project includes Corporate Social Responsibility (CSR) investments, financed by a Social Development Fund initially set at about US$ 6 million, and designed to provide development assistance to local communities. The stated objective of the CSR investments is to promote human capital within the project catchment areas [13] .

Figure 1. Central processing facility: process flow diagram. Source: AfDB (2003), project appraisal report.

The project is integrated into a broader investment plan, which involves the conversion of Sasol’s petrochemical plants in Sasolburg and Secunda from using coal as a feedstock to natural gas―manufacturing component and the extension and adaptation of Sasol’s gas distribution network to end-users in South Africa― downstream component. Also, thanks to increased gas availability, Sasol plans to develop a 700 MW gas-fired plant in Secunda for electricity generation to supplement its power supply.

Sasol was responsible for the project construction and took 100% of the risks related to the investment. Sasol commenced construction of the facilities in 2001 with its own funds, because it agreed with the Governments of Mozambique and South Africa to fast track the project development. The objective to supply Sasol’s petrochemical plants fits within a more comprehensive framework of public goals in the energy sector, as well as broader development impact objectives including regional integration, as illustrated in Table 1 [14] .

4. Costs and Financing

At appraisal, the total cost of the project up to initial production in 2004 was estimated at about US$856.2 million including a sum of US$96.7 million of sunk costs incurred by Sasol prior to the signature of the Petroleum Production Agreement (see below). This amount covers gas field development, the design and engineering of the CPF, pipeline material, route engineering, construction and commissioning.

Project financing was structured through two unincorporated joint ventures?i.e. joint ventures where the parties do not form a corporation―Sasol Petroleum Temane (SPT) and Republic of Mozambique Pipeline Investment Company (ROMPCO) set up by Sasol to manage the upstream facility and the pipeline respectively. In the upstream facility, Sasol Petroleum International owns 70% of SPT, while Companhia Mozambicana de Hidrocarbonetos (CMH), a subsidiary of the Mozambique national agency ENH, responsible for oil and gas exploration and development, owns 25%. The remaining 5% is owned by International Finance Corporation (IFC) [15] .

Similarly, ROMPCO is a joint venture between Sasol, Companhia Mozambicana de Gasoduto (CMG)―an- other subsidiary of ENH, and iGas―a subsidiary of the Central Energy Fund of South Africa controlled by the Minister of Minerals and Energy of South Africa. Sasol owns 50% of ROMPCO, while CMH and iGas share the remainder with 25% each (Figure 2) [16] .

Each entity was responsible to raise the funds for its share of investment. Both SPT and ROMPCO were financed through equity provided by Sasol and IFC and debt from external lenders. The Development Bank of Southern Africa (DBSA) was the Lead Arranger appointed by Sasol on 23 February 2003 to underwrite a debt facility of Rand 1.5 billion. In the selection of the potential funding partners, DBSA gave due consideration, among others, to the Borrowers’ political risk mitigation strategy. Other lenders include the European Investment Bank (EIB) and the African Development Bank (AfDB, the Bank thereafter). Deutsche Investitions und Entwicklungsgesellschaft (DEG), PROPARCO and Dutch government-backed Facility Emerging Markets (FOM―Faciliteit Opkomende Markten) were also brought into funding to further reduce the political risk. The Standard Bank of South Africa (STBSA) provided risk insurance policies and guarantees.

Total capital expenditure funded by external lenders amounted to US$ 505.7 million.Considering the actual project cost of US$ 714.5 million, this corresponds to a 70.8:29.2 debt-to-equity ratio, as opposed to the 48.0:52.0 debt-to-equity ratio at appraisal. The change is due to the significant cost under-run by the pipeline project com- ponent, as well as gains from foreign exchange rates for loans denominated in Euro and converted into Rand.

Table 1. Logical framework of the project.

Source: AfDB (2003) Project Appraisal Report and World Bank (2003) Project Appraisal Document.

Figure 2. Project ownership and implementation structure. ROMPCO was initially 100% owned by Sasol gas and only subsequently have iGas and CMG exercised their options to purchase up to an aggregate of 50% of the shares in ROMPCO. Source: World Bank (2003), Project appraisal document.

Figure 3 shows the shares of senior debt financing by the lenders. Each shareholder has its own separate agreements with the lenders and can earn dividends according to its board’s dividend policy and subject to the lenders’ covenants [17] .

5. Governance Arrangements

The choice of resorting to unincorporated joint ventures required to set up complex governance arrangements on how the joint ventures would function, and to define ex ante roles, responsibilities, rights and duties of the parties. A series of contractual agreements on institutional, commercial and operational aspects were signed forming the project’s governance architecture (box 3).

Figure 3. Shares of senior debt financing (million US$). Source: AfDB, project completion report, 2009.

The key institutional agreements, including the Regulatory Agreement, the Petroleum Production Agreement and the Pipeline Agreement, regulate the mutual obligations; and provide Sasol with dispensations and guarantees against market uncertainties. The commercial agreements, including the Gas Sales Agreement and the Gas Transportation Agreement, regulate trade transactions, while the Joint Operating Agreement regulates the operation and maintenance of the project’s various components.

An aspect not touched upon by the agreements was the harmonization of the different legislations. Currently, payments related to gas transportation are made in compliance with two different regulatory systems and principles, as the pipeline is partly in Mozambique and partly in South Africa. For example, the South African regulator has proposed a new tariff regime for gas transportation, distribution and marketing for the additional production volumes expected from on-going expansion works at the CPF. However, this regime is not the same as that applied by the Mozambican regulator. This situation―according to Sasol staff―causes administrative and cost burden of complying with two systems. Sasol is in discussions with Mozambican authorities to harmonize the principles of gas pricing.

Given the characteristics of the piped-gas market dominated by Sasol, which holds strong bargaining power, Sasol occupies a privileged position in the governance framework. Under these arrangements, Sasol became the primary sponsor of the project, holding exclusivity from gas field development to end-user sales in South Africa with protection from any potential competitor. Although, jointly owned with other shareholders, Sasol is one of the sellers (through SPT), as well as the operator of the upstream fields and CPF (through ROMPCO). It is the transporter and the operator of the pipeline (through Sasol Gas) and the buyer as well (again through Sasol Gas) [18] .

Overall, these arrangements helped define a clear framework within which entities operate in accordance with the law. Overall, this governance structure was adequate and solid, as confirmed by the fact that it is still in place after eleven years and has never been revisited. This shows that unincorporated joint venture is a suitable structure for transnational project finance.

6. Project Management

Three committees composed of representatives from each shareholder, were formed to streamline and enhance project management and coordination. At the operational level, a Technical Committee was in charge of all the technical aspects of the project and made resolutions that were ratified by the Operational Committee at the management level, and the Managing Committee at the strategic level. Decision making was a bottom-up process because the issues to be discussed were usually of a technical engineering nature.

Project operations were carried out in compliance with the Sasol Business Development & Implementation (BD&I) model, which defines the principles of optimal business generation and management. The model is a systematic approach to the development and implementation of business opportunities. The methodology is based on the traditional stage gate process associated with project life cycles, and includes a collection of best practices and lessons learnt (box 4). By using the principles of the BD&I model, a suitable business opportunity, identified in the idea generation stage, turns into a business development project as it becomes more focused through the application of the model. During the execution phase, a system of monitoring and evaluation activities, and risk reviews is applied to ensure that the project meets the objectives and to optimize operations, maintenance, and products along the way [11] .

The standardization of the project decision-making process and the adoption of the BD&I model proved to be a positive factor that mitigated risks during implementation and operation.

7. Relevance

Given the increasing demand for fuel products in South Africa and the fact that the existing coal mine in Sasol burg was exhausted, Sasol was looking for an alternative source of energy to increase its production. At the same time, the Government of Mozambique was looking for a way to monetize its untapped natural gas resources, discovered in the 1960s, but not yet exploited due to their location in a remote area without basic infrastructures and lack of technical skills. Also, the long lasting political conflicts in the country did not allow the exploitation of these resources. The project has benefited from the support of both governments of Mozambique and the Republic of South Africa, who participated in the investment as shareholders and set up institutional and commercial agreements to foster the project development [19] .

The project responds to the Bank’s priority to promote regional integration by financing projects or programmes, which by their nature or scope concern several members. The project is also aligned with the Bank’s country strategies for both Mozambique and South Africa. On the one hand, it is consistent with the central goal for private sector interventions in Mozambique to promote accelerated and sustainable economic growth; on the other hand, it is in line with the Country Strategy for South Africa of “Enhancing Private Sector Competitiveness, Partnership for Regional Integration and Development, as well as Knowledge Management” [20] - [22] .

8. Quality at Entry

The project design and preparation process benefited from the following factors.

Good quality of information and data generation. The preparation of the project was carried out over a long period during which all relevant information was collected and analysed. A preliminary appraisal of the gas fields carried out by a Russian company in the 1990s was used as the basis for the acquisition and generation of new data. Various project alternatives were considered and different business plans evaluated. Institutional and economic partners were identified and addressed. The quantity and the quality of gas available in the reservoirs, on which Sasol had to take an entrepreneurial risk, was the main unknown element.

Option analysis and selection of the best alternative. The project was the best alternative for Sasol, compared to other options including opening a new coal mine near Secunda. The latter possibility was abandoned owing to its likely negative environmental impact. The project was also the best alternative for the Government of Mozambique as compared to the option of developing the steel andiron industry in Matola near Maputo. This alternative was considered not feasible, because it would have required the construction of a cross-border pipeline for iron transportation crossing the Krueger National Park in South Africa, which was not desirable because of environmental and cultural reasons. The adopted solution proved to be both financially and economically viable for this capital intensive project, as shown by the performance indicators including the Financial Rate of Return (FRR) and the Economic Rate of Return (ERR), calculated separately for the two components (Table 2).

Political commitment. Sasol entertained high level relationships with the two Governments of South Africa and of Mozambique. The Government of South Africa was interested in supporting a South African company to invest abroad in a strategic sector. The Government of Mozambique was interested in a partnership to exploit its natural resources.

Strong sponsorship and financial underpinning. Sasol could count on strong sponsors and was able to mobilize all the funds necessary for the project’s various components, including the financing shares of the Mozambican shareholders (CMH and CMG).

Flexibility of infrastructure design. Although the pipeline was designed for a capacity of 120 MGJ/year, the designed wall thickness enables the capacity to be doubled up to 240 MGJ/year, in case that market demand and availability of reserves justify it. Also, the design allows other investors/projects to link to the pipeline, through five take-off points in Mozambique (Figure 4).

Detailed risk assessment. At each stage of the design process, from project concept to detailed engineering study, a risk review was carried out to re-adjust the design and identify risk mitigation measures, in compliance with the methodology of Sasol BD&I’s model (see above).

Participation of local stakeholders. According to Sasol senior staff [23] , the preparation period was used to mobilize all stakeholders and inform them about the project, with a focus on the rural communities located around the gas field and the pipeline sites. Stakeholders, in particular, were kept notified about the progress and reports were made available to the public. In both Mozambique and South Africa, announcements were made on the radio, in national and local press regarding access to reports and venues for public meetings. Notices were posted along the pipeline route and messages got around by word of mouth.

Table 2. Summary of base case financial and economic evaluation results.

Social discount rate applied 11%. Source: AfDB (2003) Appraisal Report.

Figure 4. Temane-Secunda pipeline and take off points. Source: www.enh.co.mz.

9. Outputs: Gas Production and Corporate Social Responsibility Investments

Project effectiveness is satisfactory. The planned outputs of the project were met and surpassed. Outcomes and impacts have materialized, although with some limitations. The project delivers higher capacity than expected. Compared to the target of shipping 120 MGJ/year, the project is currently shipping about 150 MGJ/year. In June 2011, the cumulative sales volume of gas had reached 735.7 MGJ, while condensate shipments from the CPF in Temane had reached some 3,579,652 barrels (Appendix 2). In the near future, up to 180 MGJ/year are expected to be shipped, thanks to the current upstream expansion works.

Expenditure for Corporate Social Responsibility was almost twice larger than planned. Between 2001 and 2010, Sasol undertook investments in human capital for more than 150 projects implemented in three provinces, accounting for US$11.5 million and impacting about 450,000 people, as compared to the US$6 million planned. Main investments included clinics, schools, sink boreholes for drinking water and other facilities for local communities (Table 3). However, the mission team could not gather evidence about whether these projects responded to priorities identified in relevant national strategies [24] .

10. Outcomes: Conversion of Sasol Production, Profit Generation and Employment

Sasol’s industrial objective was met, since the project has allowed the introduction of natural gas as complementary feedstock to coal for the production of synthetic fuels and chemicals, such as waxes, ammonia, solvents, etc. About two thirds of gas from Mozambique is processed in Sasol’s gas-to-liquid facilities for both domestic market and export. The remaining one third is delivered to about 550 individual and commercial customers in South Africa.

Shareholders’ profit expectations were met despite some limitations related to the distribution of dividends. The diversification of Sasol’s energy production mix has increased its financial performance since project completion in 2004 as indicated Table 4.

Expectations of the Government of Mozambique were met as the project has generated revenues in the form of royalties and higher corporate taxes. Royalties in cash accrued by the government on gas and condensate sales between 2004 and June 2011 amounted to US$24.15million with the following breakdown: US$15.07 million from gas sales and US$9.05 million from condensate sales. This is in addition to royalties for 14.3 MGJ of gas supplied to ENH and Matola Gas Company (see below). Corporate taxes paid to the government since project inception amount to US$ 7.97 million.

Table 3. Corporate social responsibility investments 2000-2010.

Source: Sasol Monitoring Data up to December 2010.

Table 4. Financial performance (ZAR million).

Source: Sasol, Project Completion Report.

The project had a positive effect on local employment, although limited to the operation of the infrastructure. The number of Mozambican workers at the CPF increased from 61 at the opening of the facility in 2004 to 92 in August 2011, over a total of 210 employees. The objective is to reach in the next future, a level where up to 80% of the work force are made up of Mozambicans, according to the so-called “localization plan”. In addition, new jobs were created for the provision of some basic ancillary services, such as catering and security, which were contracted to Mozambican firms. The evaluation team, however, noted that the project did not induce indirect employment, i.e. the creation of news mall business (e.g. bars, restaurants, shops and transport services), to supply the workers of the CPF with goods and services.

11. Impacts: Sectoral Goals and Development Impacts

The goals of the governments concerning the energy sector were met, although with some limitations. In Mozambique, the project has contributed to initiate the development of a domestic gas market for industrial and household consumption, which is, however, still very limited. Currently, piped-gas is only used by Matola Gas Company, a private company holding a concession to supply vehicle fuels and electricity in the Matola industrial area, near Maputo, and by ENH to supply domestic users in the province of Inhassoro.

These projects receive gas by using the pipeline’s take off points at the border in Ressano Garcia and in Temane. According to ENH estimates, only 5% of the natural gas produced in Mozambique is used for domestic consumption, the remaining95%is exported to South Africa. Table 5 presents the actual data.

Through the increase in natural gas exports due to Sasol project, the two primary energy and mineral based products, aluminium and natural gas, account for about two thirds of Mozambique’s total export revenue. This leads to a high vulnerability to shocks, given the volatility of natural resources price. In this regard, the prospect currently under discussion of developing a new electricity generation plant in Ressano Garcia is expected to contribute to rebalancing the share of Mozambican consumption of gas.

In South Africa, the realisation of NERSA’s objective to foster the diversification of the energy supply mix on the country market, shifting to alternative and cleaner energy sources, is still an on-going process. In fact, only one third of imported natural gas is used for domestic consumption, where as the remaining two thirds are transformed by Sasol into other products for exportation. Thus, the contribution of the project to the objective of meeting the domestic demand of gas from industrial users is limited. According to NERSA estimates, piped-gas provided by Sasol represents only 2% - 3% of the country’s overall energy requirements.

The broader development impacts of promoting new investments and strengthening the economic and bilateral ties between the countries were partially met. The experience of Sasol gas project has played a catalytic role in attracting other world-class companies to invest in Mozambique. In recent years, there have been large offshore natural gas discoveries in Mozambique by Anadarko Petroleum Corporation, Canada, and Ente Nazionale Idrocarburi (ENI), Italy, with estimated development cost of over USD 30 billion. The two fields hold between

Table 5. Natural gas production & export in Mozambique.

Source: www.enh.co.mz.

25 trillion and 45 trillion cubic feet of natural gas with potential for 25 million to 45 million tons of liquefied natural gas (LNG) for the next twenty years. Negotiations between the government and the oil and gas companies are expected to start in 2013, and the plan is to start producing liquid natural gas in 2018. Both companies’ reserves warrant the establishment of liquefied gas plants in Mozambique. If these discoveries are developed, it is expected to cover the energy needs of both Mozambique and South Africa inducing a significant economic development effect in the region. Admittedly, the successful experience of Sasol has played a key role in creating confidence among multinational companies and in attracting Foreign Direct Investments in Mozambique.

As far as regional cooperation and integration is concerned, being a cross-border pipeline between Mozambique and South Africa, the project de facto links both economies in different ways. To operate and maintain the CPF and the pipeline, people, goods and services have to move across the countries. According to data for the 2008 financial year, Sasol’s spending on goods produced in Mozambique represented about 45% of the total outlays, and spending on locally supplied services accounted for 55% of the total. This excludes original equipment manufactured spares, which are sourced internationally.

The main factors determining the positive achievements of Sasol’s Natural Gas Project included:

- The long experience of Sasol in the sector, with in-depth knowledge of the business and of the market potential. This mitigated the risk associated with the high pre-investment required to develop upstream activities for Brownfield gas.

- A robust management model (BD&I), based on risk reviews and the identification of mitigation measures at each step of the project. This limited the risk associated to hasty decisions and underestimation of problems.

- An efficient human resources management, in which great consideration is given to staff and to safety. This minimised the risks related to workers’ motivation and low productivity rates. The “loyalty” to Sasol is evidenced by the fact that once the newly recruited people have joined Sasol, they stay and embrace the values of the company. Sasol applies a sort of ‘Loyalty and Value’ model explaining how loyalty determines high productivity, solid profits, and steady expansion [25] .

In the face of these positive points, the project contributes only marginally to the transformation of the industrial sector of Mozambique and to the development of new businesses and services along the project’s area. Such economic “transformative capacity” and technological spill-over are still limited.

This limitation comes from the nature of the investment, characterized by capital intensity and a high technology bias production process, which does not translate per se into local development, unless a “diffusion process” is adequately managed by governments [26] . With the management of an important domestic natural asset such as gas in the hands of an international company, there is the risk for the Government of Mozambique to be relegated to the simple role of “transmission belt for transnational capital, which means that the State acts just as a facilitator to attract for foreign capital rather than promoting people-centred development [27] .

12. Environmental Impact

The conversion from coal to natural gas at Sasol’s Synfuel plants is expected to contribute to improving air quality in the industrial area, with decreases in air pollutant emissions such as sulphur dioxide, nitrogen oxide and carbon dioxide. However, no quantitative evidence exists to measure this benefit. According to Sasol (2008), using natural gas instead of coal as a feedstock for power generation, cuts CO2 emissions by more than half, but again no evidence is available in this respect.

That said, the project is compliant with its social and environmental obligations and it is environmentally sustainable. These obligations are contained in a number of legal authorizations, management plans and documents, such as the Regional Environmental and Social Assessment (RESA), the Environmental Management Plan (EMP) and the Resettlement Planning and Implementation Programme (RPIP). Sasol Petroleum Temane (SPT) was awarded ISO 14001 and 9001 certifications in November 2004 and has maintained them in subsequent annual surveillance audits. SPT was also awarded OHSAS 18001 certification in January 2006 and the available audit and monitoring reports carried out on a yearly basis are generally satisfied about Sasol’s continuous commitment to the project’s environmental management and the efforts being made to continuously improve the environment and safety performance.

13. Efficiency

The implementation time schedule was adhered to and cost savings were recorded. Construction of the CPF and the pipeline started in 2002 and was completed in February 2004 as planned. Both infrastructures were constructed as initially designed and within the forecasted time schedule. The first supply of natural gas through the pipeline reached Sasol’s Secunda plants on 23 February 2004 and the project was declared commercially operational on 26 March 2004. The official commissioning took place in June 2004.

The project was implemented within budget, except for a cost over run in the upstream component of US$48.3 million that was borne by Sasol. This was, however, more than counterbalanced by a cost under-run of US$189.9 million in the pipeline component. The net effect was a cost saving of US$141.6 million. The actual project cost of US$714.5 million was well below the US$856.2 million forecasted at appraisal. Table 6 summarizes the cost by project component at completion compared to the appraisal.

Given the time schedule adherence and the cost savings, the project shows an overall better-than-forecast financial and economic viability (Table 2 above). The unavailability of updated financial data prevents, however, to recalculate the indicators.

The project efficiency is explained by a number of factors including:

- Favourable exchange rates.

- Good quality of the design, which obviated the occurrence of predictable adverse events during construction.

- Knowledge of the construction context, which helped implement activities efficiently. In particular, the flood that occurred in 2003, just before work commenced, provided a lesson on how to deal with heavy rainfall and to adapt the construction activities accordingly.

- Setting up of a liaison committee composed of different institutions, including Sasol, INP, NERSA and the relevant ministries of both countries, to facilitate the implementation of the project by mitigating institutional and legal constraints. This committee was active from construction up to commissioning.

14. Sustainability

Sasol Petroleum International is responsible for the operation and maintenance of the CPF, as well as for the maintenance of the infrastructures developed through the CSR investments. Cumulative capital expenditure from inception up to June 2011 for maintaining and expanding the upstream component amounted to US$ 714.7 million. Operation and maintenance of services not belonging to Sasol’s core business (such as security, camp services, etc.) is provided by Mozambican suppliers. On the pipeline side, Sasol Gas is the entity responsible for operation and maintenance. As was the case at the CPF, some services (e.g. pigging, helicopter checking, etc.) were out sourced to South African and Mozambican contractors. No financial data was made available on the maintenance and expansion of the pipeline.

At institutional level, the fiscal benefits that both countries obtain from the project provide a strong incentive for the continued support to the project’s implementation and operation.

Since the beginning of the project, exploration and development activities have taken place systematically to prospect for new sources. Five licences were obtained for the project over a 25-year basis, three of which are off-shore. Given the prevailing problem of piracy, the Governments of Mozambique and of South Africa agreed to work together in developing a common strategy to secure SADC waters in order to carry out economic activities, including gas and petroleum off-shore exploration. In parallel with the project execution, Sasol developed a strategy to prospect for new sources of gas, as per the agreement with the Government of Mozambique for new on-shore and off-shore explorations, as well as through drilling campaigns in the Temane and Pande fields (Table 7). Exploration and development activities, if successful, will improve the profitability and thus the sustainability of the business [28] .

Table 6. Project cost by component (million).

Source: Sasol, Project Completion Report.

Table 7. On-shore exploration and development activities since project inception.

Sasol (2011) Annual integrated disclosure report.

According to the opinions gathered from Sasol managers, CSR investments, while formally aimed to promote human capital, were also used “as a way of sustaining results in the long term by associating local communities to the benefits of the project. This was done to pre-empt negative behaviours, such as vandalism and theft, and it worked since we had only a few episodes in this sense”. The mission team, however, could not gather further evidence from other stakeholders on this issue.

15. Conclusions

The Sasol Natural Gas Project is considered as a successful private public partnership. The project is fully integrated in a value chain that benefits stakeholders in both Mozambique and South Africa. The project is contributing to regional cooperation and integration dynamics between the economies of both countries. It has promoted institutional cooperation, involving governments whose objective is to set up regulatory framework agreements in order to proceed with the project. Also, the central processing facility and pipeline operations require flows of people, goods, services that move across the border between the two countries.

The project is marginally contributing to the national-level goals in the energy sector. In Mozambique, the project has contributed to initiating the development of a domestic gas market for industrial and household consumption even if this market is still very limited, absorbing only 5% of the total national production of gas. In South Africa, the contribution of the project to meet the existing demand of natural gas from industrial users is still marginal. In fact, there is a huge unmet demand that is not satisfied by Sasol’s supply.

The experience of the project has opened new frontiers to business opportunities in the gas sector, especially at upstream level, where intensified on-shore and off-shore explorations and the new prospected FDIs are likely to secure additional resources to sustain the gas business in the region in a long-term perspective. At the level of gas manufacturing and distribution, the impact seems to be lower, although some evidence of stimulation of entrepreneurship does exist. The project, however, failed to induce economic spill-over through the development of small businesses for provision of goods and services in the areas of influence of the project, and thus it has a limited impact on local employment.

The project was a response to a business opportunity for Sasol but it also corresponded to a convergence of objectives and priorities for both concerned governments: generating revenues from natural resources for the Government of Mozambique and securing the provision of gas to South Africa. Other success factors were: flexibility of the project design; Sasol’s long experience and knowledge of the sector; efficient project management, with efforts put in promoting safety and mitigation of environmental externalities. The main limitations include:

- The nature of the project, which is highly capital intensive and thus does not guarantee spill-over per se, unless specific measures are taken to set up the conditions for local development.

- The strong bargaining position of Sasol, which explains, for example, some issues as far as the distribution of dividends to shareholders is concerned.

- The risk of dependence on external shocks, because almost all the produced gas is exported and domestic demand is still very limited.

- The two legislations in place to regulate payments related to gas transportation, which cause administrative and cost burden to comply with two different systems.

In sectors with high profit potential such as energy, public-private partnerships are highly relevant. In the case of Sasol, the unincorporated joint venture legal form is proved to be particularly adequate. To ensure fair distribution of benefits and to secure the convergence of objectives of the participating public and private stakeholders, public-private partnership requires balanced bargaining power of partners. The development of a cross- border infrastructure de facto generates cross-border movements of people, goods and services. To maximise regional integration effects, it is required to set up a legal framework facilitating institutional cooperation and business process.

Acknowledgements

This paper has benefited from very useful comments from: a) Tesfaye Dinka, John Eriksson, and Fredrik Söder- baum, external peer reviewers; b) private sector experts of the African Development Bank, especially Yusuf Hussein Iman and Grace Kyokunda; and c) comments of anonymous referees. The findings, interpretations, and conclusions presented in this paper are the sole responsibility of the authors.

Cite this paper

Albert-EnéasGakusi,DavidSartori,JoeAsamoah, (2015) Fostering Regional Integration in Africa: Lessons from Sasol Natural Gas Project between South Africa and Mozambique. Open Journal of Social Sciences,03,187-204. doi: 10.4236/jss.2015.310025

References

- 1. Winkler H., et al. (2006) Energy Policies for Sustainable Development in South Africa Options for the Future. Energy Research Centre, University of Cape Town, Cape Town.

- 2. AfDB (2011) Mozambique: Country Strategy Paper 2011-2015.

- 3. Cambray, G. (2007) Peak Oil and South African Synfuels—A Positive Lesson for the World.

- 4. Bossel, A. (1998) Renewable Energy in Mozambique: Country Report. AFREPREN/FWD, Working Paper N. 380.

- 5. AfDB (2011) Energy Strategy of the African Development Bank Group. Memo, 3 November.

- 6. Republic of South Africa (2002) Gas Act (48/2001). Government Gazette Vol. 440, No. 23150, Cape Town.

- 7. Republic of South Africa (2007) Gas Act 2001. Piped Gas Regulations. Department of Minerals and Energy. No. R. 321.

- 8. Republic of South Africa (2009) Gas Act (48/2001): National Energy Regulator: Rules. Department of Energy, Government Gazette Vol.534, Pretoria 31 December 2009, No. 32849, Government Notice. R. 1251.

- 9. Republic of South Africa (2001) Regulatory Agreement. Agreement Concerning the Mozambican Gas Pipeline between the Republic of South Africa and Sasol Limited.

- 10. Government of the Republic of South Africa and Government of the Republic of Mozambique (2000) Agreement between them, concerning Natural Gas Trade between South Africa and Mozambique.

- 11. Sasol (2011) Sasol Petroleum International Temane CPF Development Project. Welcome African Development Bank. Presentation Delivered on 1st December 2011.

- 12. AfDB (2003) South Africa/Mozambique: Loan to Sasol Petroleum Temane Limitada (SPT) and Republic of Mozambique Pipeline Company (ROMPCO) to Finance the Sasol Natural Gas Project. Board Resolution No. P/ZZZB/ 2003/05.

- 13. Sasol (2003) Natural Gas Project. Consolidated Executive Summary and Update.

- 14. ROMPCO ADB Facility Agreement (2004) Credit Facility for Republic of Mozambique Pipeline Investments (Proprietary) Limited, Development Bank of Southern African Limited, African Development Bank and Standard Corporate and Merchant Bank.

- 15. World Bank (2003) Project Appraisal Document. International Bank for Reconstruction and Development and International Finance Corporation. Report No. 26757-MOZ.

- 16. World Bank (2005) World Bank Provides Enclave IBRD Guarantee to Cross-Border Gas Project. The Southern Africa Regional Gas Project. Project Finance and Guarantees.

- 17. AfDB (2009) Republic of South Africa and Republic of Mozambique. Sasol Natural Gas Project. Project Completion Report (PCR).

- 18. AfDB (2003) South Africa/Mozambique—Proposal for an ADB Loan of ZAR 550 Million to Finance the Sasol Natural Gas Project. Revised Version.

- 19. Davidson, O. and Winkler, H. (2003) South Africa’s Energy Future: Visions, Driving Factors and Sustainable Development Indicators. Energy and Research Development Centre, University of Cape Town, Cape Town.

- 20. AfDB (2003) Mozambique: 2002-2004 Country Strategy Paper. Memo to the Board of Directors, 25 September 2003. http://dx.doi.org/10.1787/aeo-2003-16-en

- 21. AfDB (2011) Energy Strategy. http://www.afdb.org/en/blogs/energy-strategy/information-communication-technology/

- 22. AfDB (2003) South African Country Strategy Paper. Memo. 17 April 2003.

- 23. Mateus, Z.G. and Haan, E. (2010) Case Study: Mozambique Natural Gas Project. World Economic Forum on Africa- Tanzania, Dar es Salaam, 5-7 May 2010.

- 24. Sasol (2003) Natural Gas Project Temane and Pande Gas Field Development Mozambique/Secunda Pipeline. Volume 1 of 4. Resettlement Planning and Implementation Programme—Final.

- 25. Rieccheld, F.F. and Teal, T. (2011) The Loyalty Effect. The Hidden Force behind Growth, Profits, and Lasting Values. Harvard Business School Press, Boston.

- 26. Power, J.H. (1995) Capital Intensity and Economic Growth. The American Economic Review, 45, 197-207.

- 27. Soderbaum, F. and Taylor, I. (2003) Regionalism and Uneven Development in Southern Africa. The Case of the Ma- puto Development Corridor. Ashgate Publishing, Ltd., Farnham.

- 28. Sasol (2011) Integrated Annual Report. Sasol Reaching New Frontiers, 30 June..

Appendix 1. Map of the Site

Appendix 2. Production and Sales Volumes ? 30 June 2011

Appendix 3. Research Check List