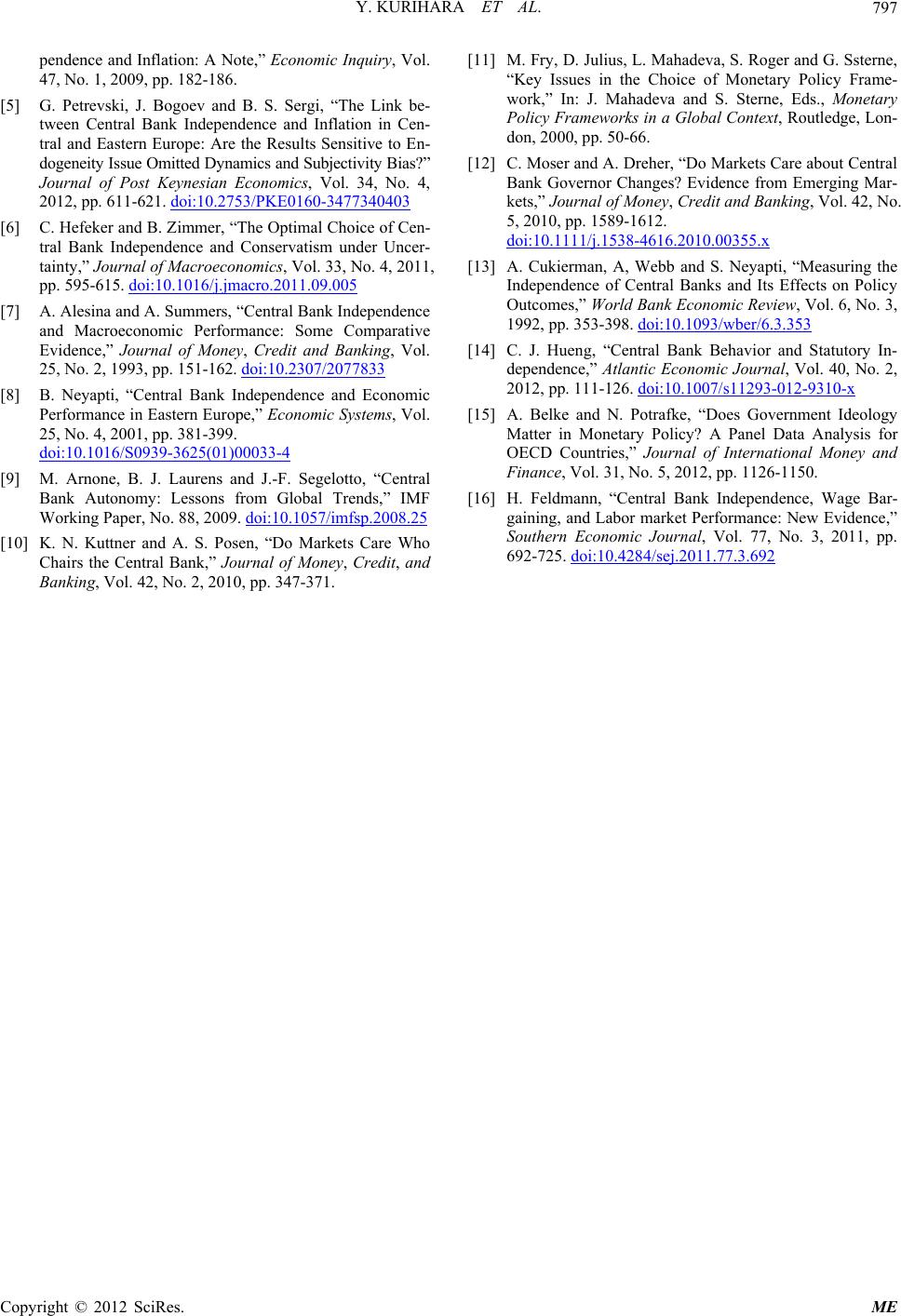

Y. KURIHARA ET AL.

794

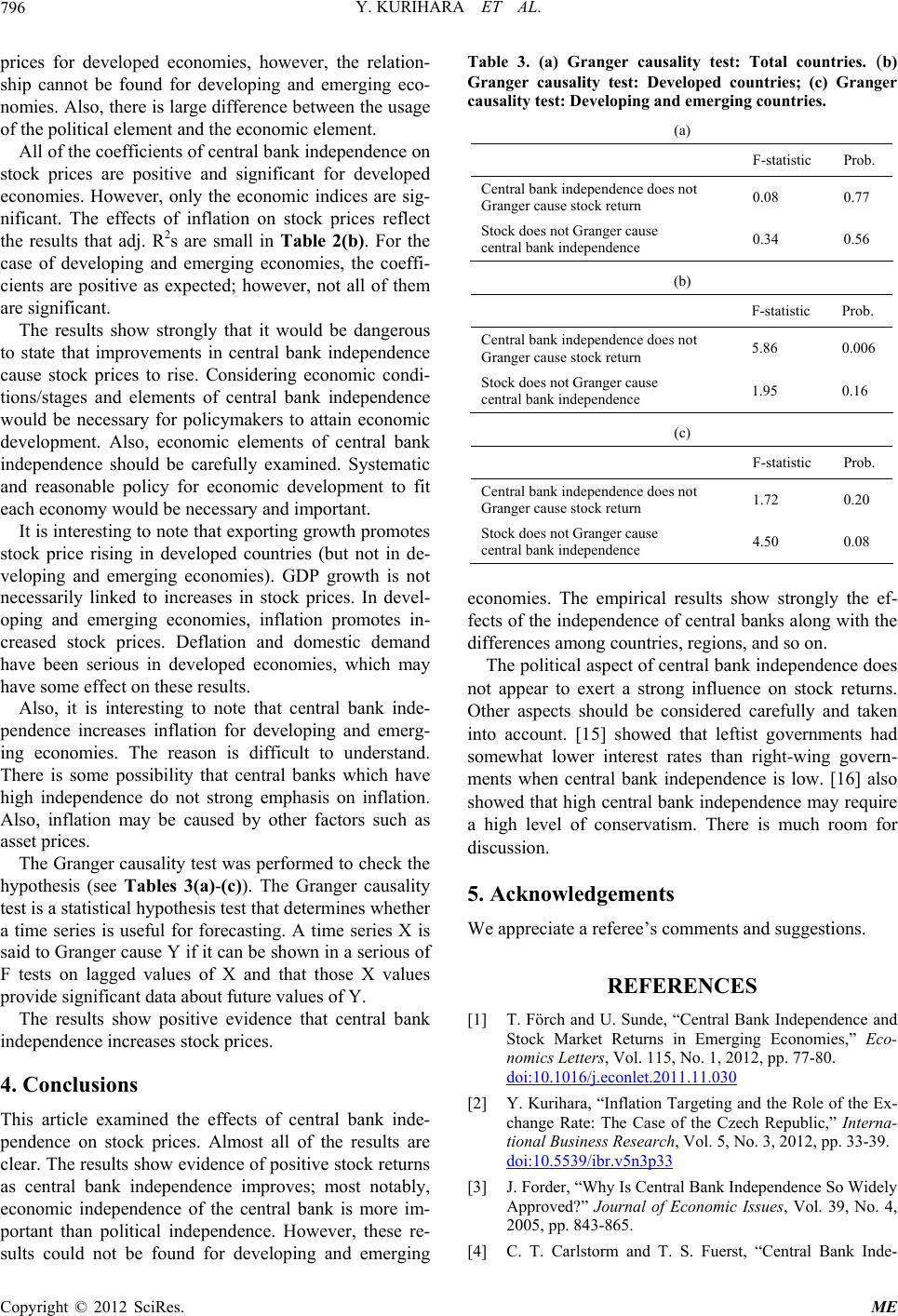

bank independence on stock prices as well as the effects

of some macroeconomic variables on stock prices. The

central bank independence index is drawn from two fa-

mous ones [1,13], which have been cited frequently. Two

groups of countries area used for this analysis: dev eloped

economies and developing/emerging economies. A com-

parison of these categories seems very important for the

conduct of monetary policy and for stable growth. Al-

though the ideal would be to use a reliable central bank

index, it is difficult to collect this type of data. Two reli-

able data [9,13] are employed in this article. However,

political and economic elements of the two indices are

distinguished to analyze the effects of the central bank

independence and some economic variables on stock

prices.

2. Theoretical Analysis

This article empirically examines the effect of central

bank independence and economic variables on stock

market prices. The equation for the empirical analysis is

as follows:

STOCKit = Const + αCBIit + βXit + εit (1)

STOCK means year-to-year p ercentage change of stock

prices. CBI denotes central bank independence index. X

means four macroeconomic variables related to stock

prices (explained in 3-1 in detail). i denotes country and t

means time. This equation is orthodox and not new as

based on [1]. Both the effect of CBI effect on stock

prices and some related macroeconomic variables with

stock prices and goals of central banks are added as ex-

planation variables for empirical estimation. This equa-

tion is orthodox and not new as based on [1].

The effect of CBI on stock prices is the main focus of

this article; it cannot be omitted. Second, almost all of

the central banks conduct their policies to attain stable

inflation rates. Inflation rate should be examined. Third,

interest rate is the most important factor for determina-

tion of stock prices. It is added as an explanation variable.

Fourth, as most central banks are interested in economic

growth, GDP growth is used as an explanation variable.

Finally, export growth is added as an explanation vari-

able as per [1], because not only the cases of developed

but also those of emerging and developed countries are

employed for estimation. Some developing and emerging

economics depend on exports for economic growth, na-

mely, in stock prices.

The main interest is in the effects of CBI on stock

prices. The CBI indices used here are the Cukierman and

Arnone index of the subindices for political independ-

ence and economic independence, together and in total.

All measures of CBI are measured for the period for

which the returns are calculated. Changes do not always

represent permanent shifts in the level of the CBI proxy.

3. Empirical Method and Results

3.1. Empirical Method

The data are yearly. For central bank independence, the

data derived from [9,13] are both used. The two papers

provided data regarding central bank independence; all

data are fixed. The sample periods are from 1989 to 1992

for the index of [13] and from 2005 to 2007 for the index

of [9]. These indices are based on information about cen-

tral bank independence across 10 dimensions. [9,13] are

combined with different weights in an economic and

political independence index. Both economic and politi-

cal factors are taken into account.

[14] found that the differences in behaviors among

central banks are consistent with the economic measure

of independence, which measures how easy it is for the

government to finance its deficits by direct access to

credit from the central bank. For example, one of the

economic differences is whether or not the central bank

is obliged to finance government debt, and one of the

political differences is the relationship between the cen-

tral bank and the government in determining monetary

policy. Both economic and political elements should be

considered in determining the central bank index.

This article divides the countries into two groups: 1)

developed countries and 2) developing or emerging

countries. For developed countries, the countries esti-

mated are Australia, Austria, Belgium, Korea, Nether-

lands, New Zealand, Norway, Portugal, Singapore, Spain,

Sweden, Switzerland, the United Kingdom, and the Uni-

ted States. Developing and emerging economies include

Barbados, Columbia, Israel, Malta, Peru, Philippines,

South Africa, Turkey, and Venezuela. Only the countries

selected were examined in this analysis due to the data

available.

The stock market prices are percentage year-to-year

change and are used for dependent variables. Explana-

tory variables include the index of central bank inde-

pendence, inflation, GDP growth, export growth, and in-

terest rate. All of the data except the index of central

bank independence are percentage year-to-year change

and are from International Financial Statistics (Interna-

tional Monetary Fund). Three indices are used for central

bank independence: total, economic, and political.

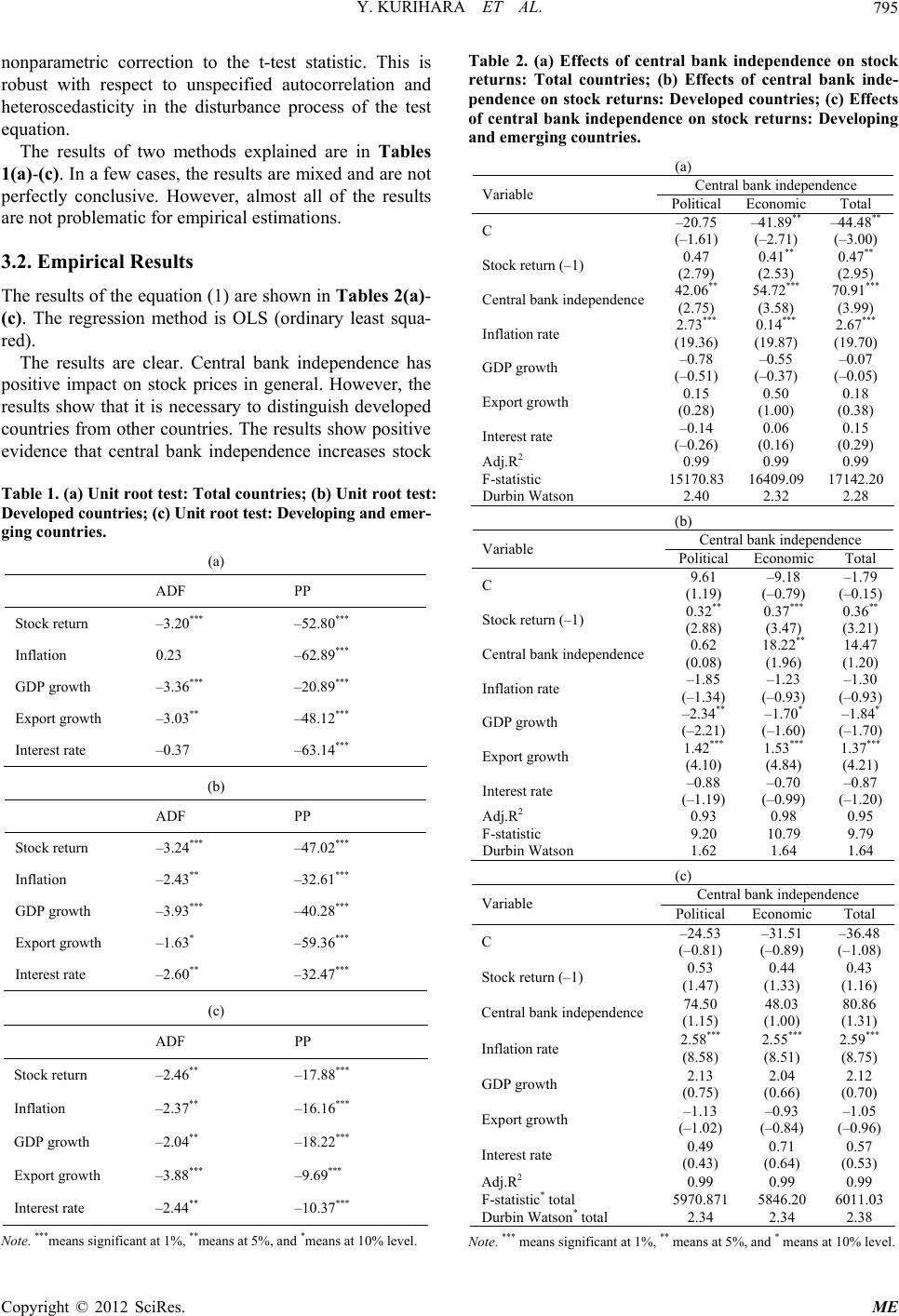

It is necessary to check unit root tests for estimation.

This paper uses two typical methods: augmented Dickey-

Fuller (ADF) and Phillips-Perron (PP). ADF is most used

for empirical estimation; however, if the series is corre-

lated at higher order lags, the assumption of white noise

disturbances is violated. The PP test proposes a method

by which to control for higher order serial correlation in

a series than is accepted in the equation. The test makes a

Copyright © 2012 SciRes. ME