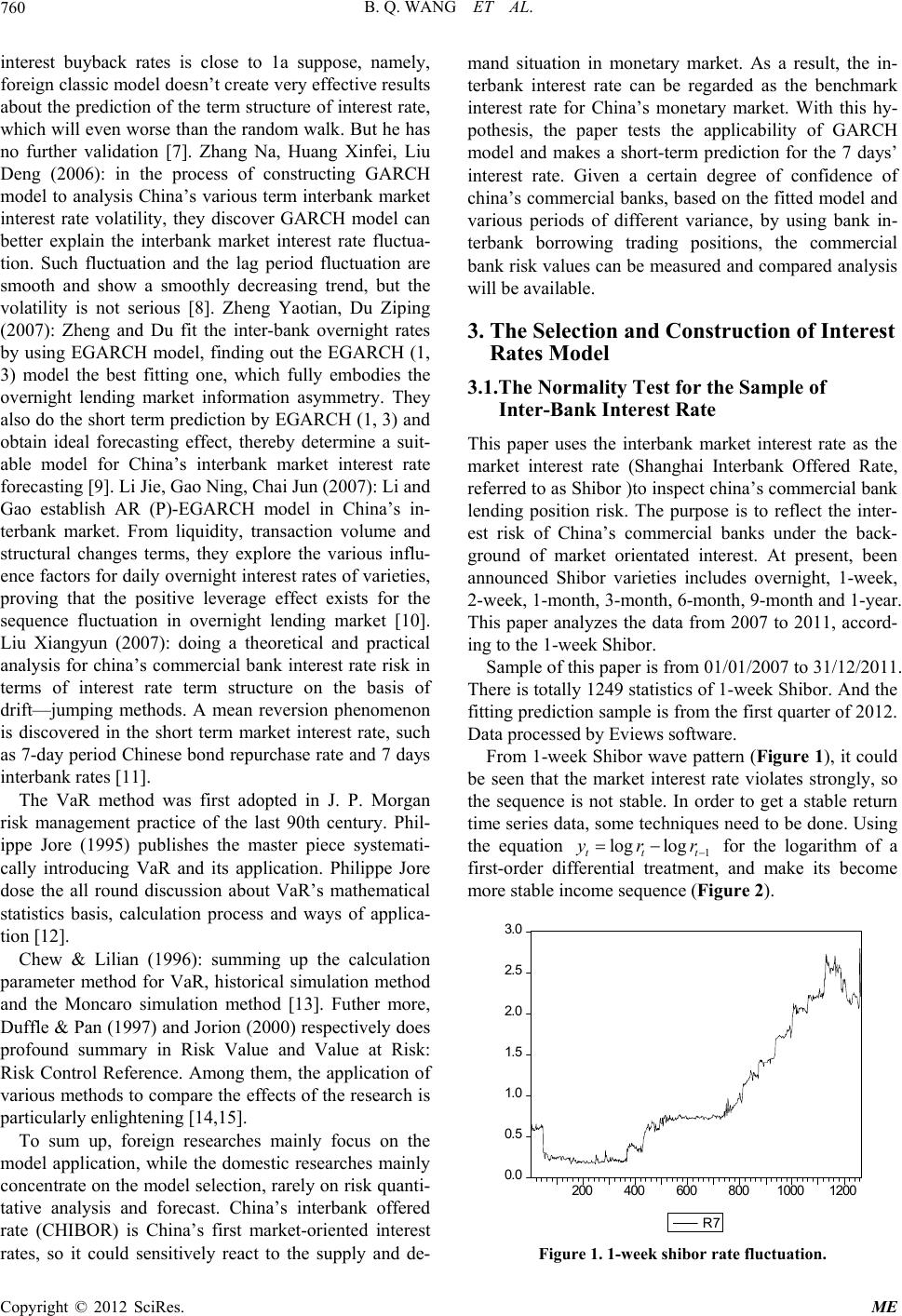

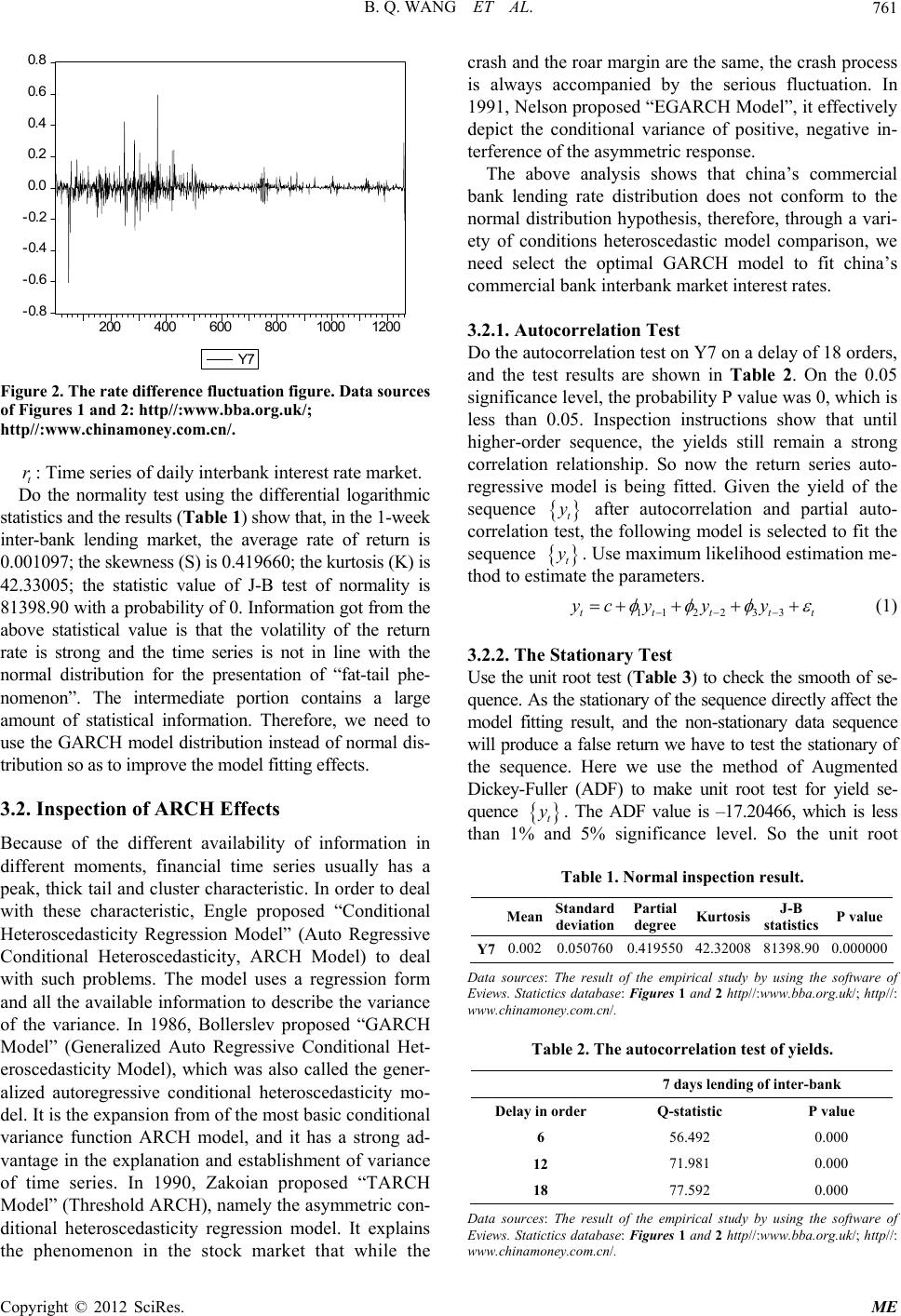

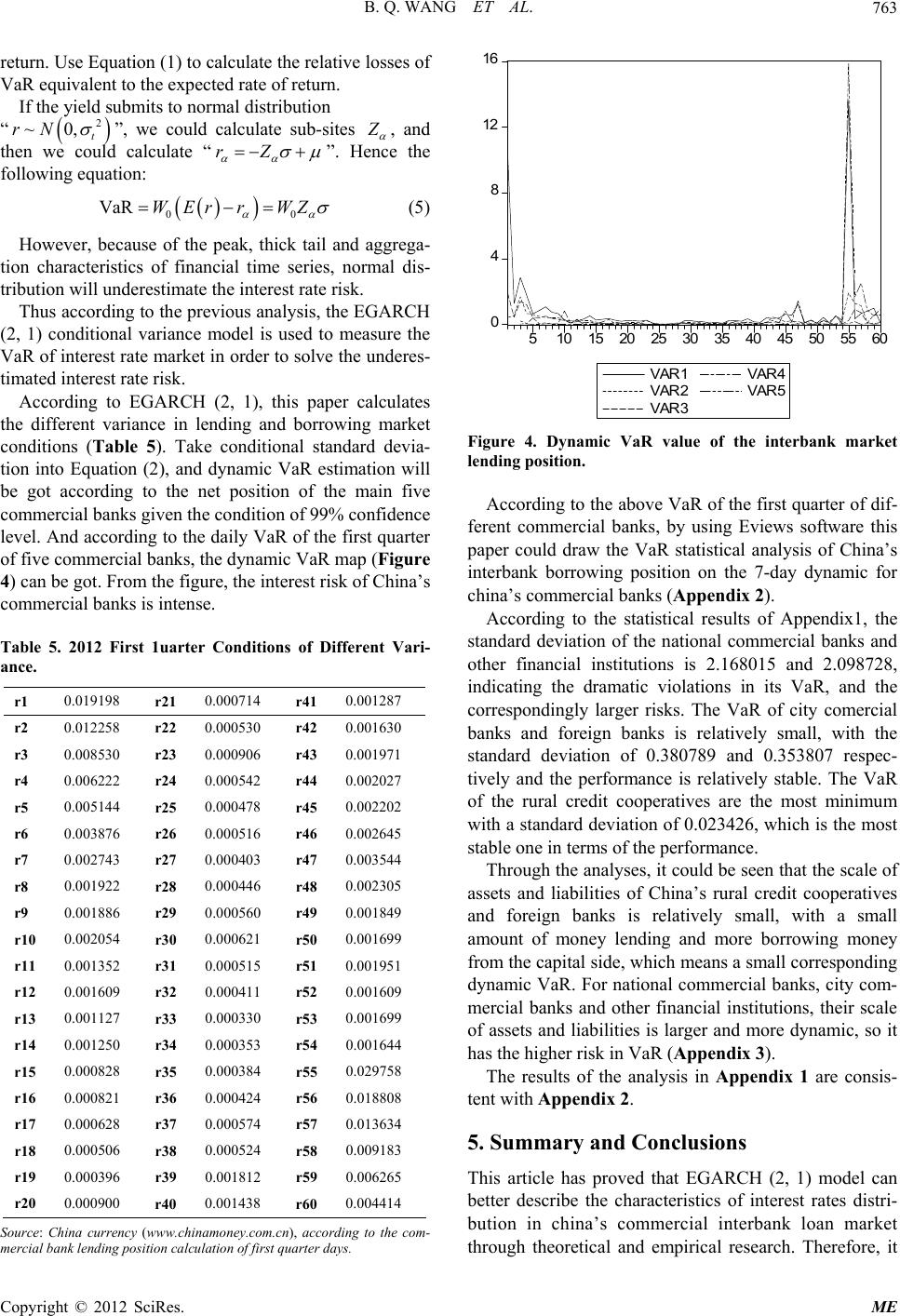

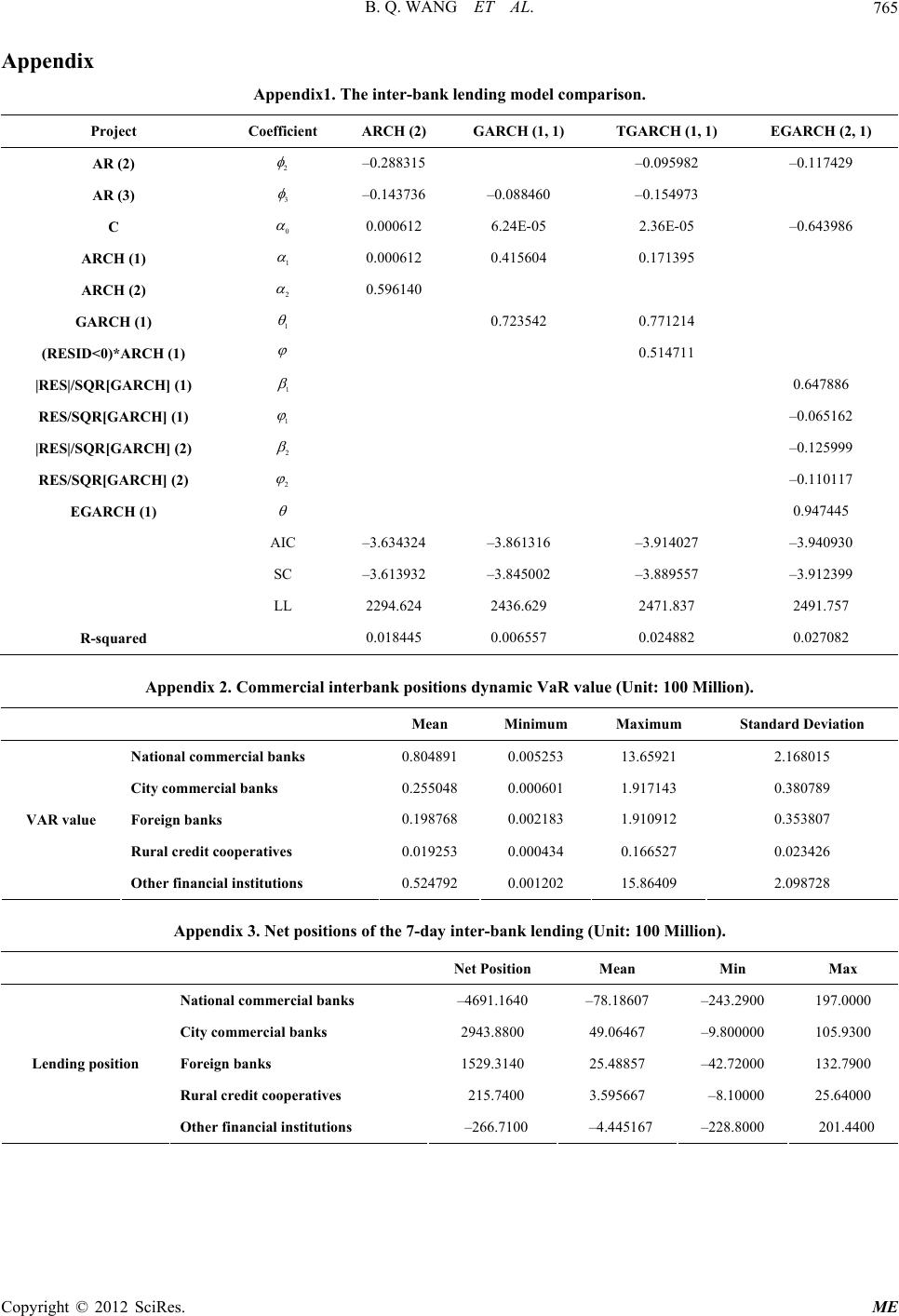

B. Q. WANG ET AL.

Copyright © 2012 SciRes. ME

764

success

si

rket conditions heteroscedastic. Take the condi-

tio

e of statistical description, it can be

th

could be a useful tool for commercial banks to undergo

the risk management by using VaR estimation.

Establish the model of ARCH (1), GARCH (1, 1),

TGARCH (1, 1) and EGARCH (2, 1) and make- [2

ve comparison. The AIC and SC of EGARCH (2, 1) is

the smallest, the LL value of TGARCH (1, 1) is smaller

than EGARCH (2, 1) but the fitting coefficient of

EGARCH (2, 1) is larger than TGARCH (1, 1). In com-

prehension, EGARCH (2, 1) can better describe the dis-

tribution of the series of the interest rate of inter lending

and borrowing market in china’s commercial banks, and

as a result, EGARCH (2, 1) could be used as the fitting

model.

Use EGARCH (2, 1) model to calculate the interest

rate ma

ns heteroscedastic into VaR model so that the dynamic

VaR estimation of night and 7-day lending position could

be figured out according to the daily net trading positions,

on the confidence level of 99%. From the final results, it

could be seen that the fluctuation of china’s interest rate

in the interbank lending and borrowing market is serious

and violate, indicating china’s interest rate in the inter-

bank lending and borrowing market has been fully mar

ket-oriented.

From the Bank lending and borrowing yields dynamic

the VaR valuseen [9] Y.-T. Cheng and Z. P. Du, “EGARCH Model in the In-

terbank Offered Rate Forecast,” Hubei Institute for Na-

tionalities, Vol. 1, No. 6, 2007, pp. 234-237.

at the risk value and the standard deviation of national

commercial Banks and other financial institutions is big-

ger, and dramatically changed. City commercial Banks

and foreign banks’ interest rate risk value is smaller, the

performance was stable. The risk of rural credit coopera-

tives is the smallest and the most stable. According to the

value, the risk of china’s state-owned commercial Banks

and other financial institutions is the largest, followed by

city commercial banks and foreign banks and finally are

the rural credit cooperatives the scale of assets and li-

abilities of China’s rural credit cooperatives and foreign

banks is relatively small, with a small amount of money

lending and more borrowing money from the capital side,

which means a small corresponding dynamic VaR. For

national commercial banks, city commercial banks and

other financial institutions, their scale of assets and li-

abilities is larger and more dynamic, so it has the higher

risk in VaR.

REFERENCES

[1] J. F. Huang, “Interest Rate Market and Commercial Bank

Interest Rates,” Machinery Industry Press, Beijing, 2001.

] Q. Ge, “US Commercial Bank Interest Rate Risk Mana-

gement,” China Economic Publishing House, Beijing,

2003.

[3] G. Q. Dai, “China’s Commercial Banks Interest Rate Risk

Management,” Management Research Group, Portland,

2005.

[4] Q. M. Tang and X. Gao, “An Empirical Study of the

Term Structure of Interbank Lending Market in China,”

Statistical Research, Vol. 1, No. 5, 2001, pp. 29-31.

[5] H. F. Xu, “Asymmetric Transfer Relationship with the

Efficiency of Interest Rate Policy Interest Rate,” The

World Economy, Vol. 1, No. 8, 2004, pp. 39-42.

[6] H. Lin and Z. L. Zheng, “The Term Structure of Interest

Rates: Theory and Application,” China Financial and

Economic Publishing House, Beijing, 2004.

[7] Y. Dong, “China’s Short-Term Interest Rates Mean Re-

version Assumption of Empirical Research,” Quantitative

& Technical Economics, Vol. 1, No. 11, 2006, pp. 151-

159.

[8] N. Zhang, H. X. Fei and T. Liu, “Statistics and Deci-

sion-making of China’s Interbank Lending Market Inter-

est Rate Fluctuations,” Statistics and Decision, Vol. 1, No.

4, 2006, pp. 121-123.

[10] J. Li, N. Gao and C. Cai, “Bank of China Inter-Bank

Market between the Basic Characteristics of Analysis and

Influencing Factors,” China Accounting Review, Vol. 1,

No. 1, 2007, pp. 249-266.

[11] X. Y. Liu, “Drift-Jump Process of Commercial Bank

Interest Rate Risk Measurement: Theory and Experience

Analysis,” Statistics and Decision, Vol. 1, No. 6, 2007,

pp. 99-101.

[12] P. Jore, “Value at Risk: The New Benchmark for Con-

trolling Market Risk,” McGraw Hill, New York, 1995.

[13] L. Chew, “Managin Derivative Risks,” John Yiley & Soas,

New York, 2002

[14] D. Duffle and J. Pan, “An Overview of Value at Risk,”

Journal of Derivatives, Vol. 4, No. 3, 1997, pp. 7-49.

doi:10.3905/jod.1997.407971

[15] P. Jorion, “Value at Risks: Then Benchmark for Control-

ling Risk,” Central Press, Amman, 2001.