Open Journal of Accounting, 2012, 1, 27-37 http://dx.doi.org/10.4236/ojacct.2012.12004 Published Online October 2012 (http://www.SciRP.org/journal/ojacct) Is There a Specific Accrual Basis Standard for the Public Sector? Theoretical Analysis and Harmonization of Italian Government Accounting Fabio Giulio Grandis1, Giorgia Mattei2 1Associate Professor of Public Administration Economics, Roma Tre University, Rome, Italy 2Candidate in Economy and Management, University of Urbino, Urbino, Italy Email: fg.grandis@studioferrari.com, giorgia.mattei@uniurb.it Received September 10, 2012; revised October 12, 2012; accepted October 20, 2012 ABSTRACT This paper aims to analyse the principle of accrual accounting when applied to non-business-oriented companies, in- cluding most general government bodies. The analysis is carried out by referring to concepts that are well-established and firmly anchored to the “history” of accounting and which, today, allow us to define the principle of accrual ac- counting for “non-busin ess” activities differently to that app licable to profit-oriented companies. This also gives rise to a different interpretation of the economic result. This work subsequently provid es a “fieldwo rk” analysis of how accrual accounting has been introduced in the Italian public sector through an on-going accounting harmonization project. Fi- nally, this paper offers a critical examination of the current accrual basis recognised by the International Public Sector Accounting Standards (IPSAS), as compared to its theoretical d efinition. The conclusions of this paper support the the- ory that the IPSAS can contribute to the current harmonization of Italian government accounting, but also reverse. Keywords: Public Administration Accounting; Principle of Accrual Accounting; Accounting Harmonization; International Public Sector Accounting Standards Board (IPSASB) 1. Objectives and Research Methodology Up to 2002, the work carried out by the International Public Sector Accounting Standards Board (IPSASB, formerly PSC, Public Sector Committee) was that of adapting the accounting principles of the International Accounting Standards (IAS) to the public sector. Subse- quently, IPSASB began to develop a number of specific accounting principles for cases in which the IAS prince- ples could not apply-hence the peculiarity of the public sector. For example, the IPSAS 23 principle on “Reve- nue from Non-Exchange Transactions” was published in December 2006. During this second phase, IPSASB’s strong attachment to the IAS framework conditioned its choice to extend the so-called “accrual basis” principle of accounting, applicable to private companies, to the public sector [1,2]. This paper’s first objective is to analyse whether the accrual basis principle set out in the IAS framework can be implemented in non business organization without any modifications, or whether it will have to be undergo the typical adaptations or tailoring required for the public sector. This paper’s second objective is to examine how the accrual system has been introduced in the Italian public administration over the last 20 years and, in particular, to study the recent process of accounting harmonization of public financial statements, which is provided for in the Italian Constitution. The methodology used in this paper is both deductive and inductive. A deductive analysis has been applied mainly in relation to this paper’s first objective. In that regard, this paper offers a detailed and doctrinal research on the topic, delving into the specific peculiarities of the public sector, which is characterised by its non-business- oriented nature, its specific funding regime and a fre- quent lack of a market price for the services it provides. Conversely, an inductive analysis has been applied mainly in relation to this paper’s second objective. By analysing concrete cases, the provisions on the imple- mentation of accrual systems and the effective means of implementation of such systems, one can assess to what extent the doctrinal analysis is indeed accurate. Such analysis highlig hts th e real difficu lties that public bodies and administrations face when applying the prin- ciple of accrual accounting adapted to non-business-ori- ented companies. The reasons for such difficulties are two-fold: the first reason, which can be extended to an C opyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 28 international level, relates to how the economic result isinterpreted according to the accrual accounting princi- ple adopted; the second reason is specific to all public ad- ministrations in those countries where the budget plays a strong “authorizing” role. The turbulent context in which European public ad- ministrations operate would prompt a traditional ac- counting system being implemented alongside one that can maintain economic stability over time. However, it is also true that economic stability for a profit-oriented company is very different to that of a non-business-ori- ented entity, such as general government bodies—at least the Italian ones. If we consider other international scenarios, the as- sumption that all of the most economically advanced countries have adopted, or are about to adopt, the “full accrual” accounting system, is clearly put into question. A new interpretation of the accrual accounting system aimed at the public sector is likely not only to revive the modernisation of public accounting systems, but also to avoid any regrets in switching from the current public accounting system to one with a focus on accrual basis accounting [3,4]. 2. “Historical” Relevance of the Economic Analysis of Public Administrations Nowadays, public administrations are mainly made up of non-business-oriented bodies which carry out a number of activities that are similar to those of “business-ori ented” companies. In fact, it has been observed [5] that public admini- strations also carry out business-like processes, have their own asset management activities and carry out pro- fitable corporate transactions. These activities, however, play an instrumental role with respect to the all other activities which such public bodies carry out in order to reach their institutional, political and social goals. In Italian general government bodies, economic rele- vance gained notoriety only in the 1990s, notwithstand- ing the fact that a distinguished scholar had anticipated its importance by more than a cen tury [6,7]1. In the past, management analysis was limited to finan- cial and monetary aspects, following a “kameral” ac- counting system [8]. Th is approach, ad opted due to trad i- tional public administrations, revealed its shortcomings when the public sector began to adopt increasingly com- plex production processes as a result of public economic intervention and the direct fulfillment of the collective administration n ee d s . Such an approach has given rise to a number of tech- nical and administrative difficulties, many of which are still relevant today [9,10], and the most important of which relates to corporate asset fluctuation. Net asset maintenance has therefore become the minimum requirement for a company’s “survival” and sustainability; without this condition, the public sector would suffer “a continuing pathology” [11]2 resulting from management trapped in an “irreversible coma”. Net asset conservation is to be interpreted dynamically, perhaps as a “re-conversion” of assets according to pub- lic needs, which change through time and in accordance with the main political class in power. A management analysis based solely on financial as- pects is now considered to be insufficient. In Italy, the reform of the public accounting systems introduced the requirement-for the public Administra- tion-to also carry out an economic and asset management analysis but different accounting models [12] prevailed. Such models reflect two distinct approaches, which are also found in internation al doctrine: 1) The first approach completely abandons “tradi- tional” public accounting in favour of the same economic survey models used by companies [13-17]. 2) The second approach is based on different integra- tion models for both financial and economic surveys [18,19]. The choice of one approach over the other fuels school-arly debates and clarifies the rationale behind se- veral accounting provisions applicable to the various areas of the public sector. In any case, an economic analysis of management has become both necessary and inevitable. Nonetheless, in order to understand the actual relevance of such informa- tion, it is important to examine how the accrual basis system applies to non-business-oriented companies, as opposed to the typical profit-oriented companies that are active on today’s markets. 3. The Accrual Basis in Non-Business-Oriented Companies In most public sector entities, the production cycle of a service provided only justifies costs and charges. Only rarely are adequate earnings made on a service, since the entire business process is not aimed at sales but, rather, at meeting the needs of a community. 2Amaduzzi very aptly points out: “manifestazioni numerarie, imposte dalla continuità della vita aziendale, possono anche richiedere lesioni al otere di generazione di ricchezza che l’azienda di erogazione abbia. E allora se non si verificasse una ricostruzione delle perdute forze eco- nomiche, l’azi enda sarebbe destinata alla cessazione del suo unitar io pro- cesso, o alla continuazione patologica della sua vita, quando l’azienda fosse perenne per natura”. It is assumed that he term “long-lasting company” used by the author refers to public sector companies that, as such, cannot go bankrupt.Nevertheless, in today’s reality, such public sector companies c an have their goods confiscated and a uctioned, can be laced under temporary receivership or, potentially, be absorbed by a higher-level administrative body. 1In the 19th century, the most prevalent scholar of Italian public ac- counting was definitely Giuseppe Cerboni. Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 29 Furthermore, most of the revenue which funds the factors of production is, contrary to costs and charges, entirely independent from the volume of the activity car- ried out. For example, a state or government grant or a mandatory contribution towards a public sector entity is often awarded notwithstanding the quantity and quality of the services provided. In these cases, the revenue per- ceived is not consideration for a specific service provided, but it generally falls within a general institutional objec- tive. Thus, in order to fully understand the differences be- tween the economic management of a business-oriented company and that of a non-profit-oriented one, it is nec- essary to distinguish management details taken from the economic results and based on the following points: earnings and costs, implying an underlying exchange of goods and services; revenue and charges, that do not im- ply an exchange transaction, but relate to other unilateral acts-be they casual, voluntary or compulsory; these would include, for example, obtaining a contribution in cash or in kind; an extraordinary variation in the value of assets; endowments and donations; taxes and levies, etc. If we look at needs fulfilled of services provided, we can find the different public Administration structures. These structures, in detail, are: 1) Specific and divisible services that are individually requested; Figure 1. 2) General and indivisible services that is generally requested; Figure 2. 3) Other typologies of contribution provided Figure 3. In the first category, we find the production inside public Administration. It will be necessary to sustain some costs for the acquisition of production factors. The latter will be put through the operating cycle. This pro- cesses results in individually requested services, which generate earnings. These earnings will be reused to sus- tain costs. We can identify an exchange transaction both from costs and earnings. This specific accrual basis standard is also found in business organization. In the second category, we can also find a production. It will be necessary to sustain so me costs for the acquisi- tion of production factors that will be put through the operating cycle. This processes result in collectively re- quested services. Revenues come from higher Admini- strations. The revenues will be used to sustain costs. We can identify an exchange transaction from the sector costs and non-exchange transactions from the revenue sector; in this case, we think that it is more difficult to implement the “traditional accrual basis”. In the third category, public Administration revenues come from higher Administrations, which are distributed in various modalities (for example: scholarships, unem- ployment benefit, etc.). These are charges that the public Figure 1. Specific and divisible services. Figure 2. General and indivisible services. Figure 3. Other typologies of contribution provided. Administration sustains for the community. In this case we have only non-exchange transactions and, for this reason, is more difficult to implement the “traditional accrual basis”. All administrative facts tied to the economic manage- ment of a company can be sub-divided according to by their effects on one financial year instead of another. The costs and earnings, and the charges and revenue are re- corded every calendar year on the basis of assumptions on the “causal link” between positive and negative eco- nomic elements. It is thanks to this causal link, called “accrual basis”, that we can measure asset variations and its respective economic result for the year. However, the “causal link” is not only extremely dif- Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 30 ferent, but literally inverted [20]3 when comparing the dynamics of non-business-oriented companies and profit- oriented o nes. Indeed: in profit-oriented companies, the costs are borne in order to make earnings; the company’s main goal is to increase th e margin between costs and earning s. in non-busin ess-oriented companies, th e opposite occurs: revenue is obtained, often in a compulsory manner, to bear costs and charges needed to reach social, political and institutional goals; the volume of revenue and earn- ings should represent the maximum limit of costs and charges; in the medium-to long-term, there should be no significant or stable margin between positive and nega- tive economic elements. The notion of “accrual basis” therefore takes on a par- ticular meaning when it is applied to non profit-oriented companies and, in particular, to public administrations. When the accrual basis concept was applied at the non-business organizations, this notion takes a special connotations, particularly as applied at the public Ad- ministration. Asset management and business activities find their raison d’etre in non-profit-oriented companies only in- asmuch as they generate positive net equity, which, seen as a “means”, is subsequently “used” to reach an institu- tional goal. It is absolutely clear, in fact, that a business activity carried out by a company in loss would have a negative effect on its delivery process. This is due to the fact that a public body, g iven its unitary character, should cover the losses even where this is to the detriment of the very so- cial needs for which it was created. It follows from the above that the economic analysis of the management of a public sector en tity requires that, as a preliminary step, a distinction be made between events that are directly linked to a market exchange transaction and those that are not, by virtue of their social objec- tives4. In the former, the accrual basis for income and ex- penses can be traced back to the notion used for compa- nies, i.e. income is distributed to a financial period on an accrual basis when an exchange has taken place, in other words where a transaction such as a succession, an asset or a service has been completed in all its production cycle; expenses are linked to the income for which they were incurred. The correlation can therefore be deducted ana- lytically and directly as a result of a cause and effect. When there is no such causal link, the correlation can be made by reference to the functionality or usefulness from a rational and systemic point of view (for example a time basis) or when utility and functionality of costs is lacking. In any case, were it is feasible to gain earnings, on a synallagmatic basis, notwithstanding its political price, the aforementioned principle becomes entirely applicable and must be referred to when defining the economic components of a financial period. In the latter case, and thus for most public sector enti- ties, it is necessary to consider the accrual basis directly in relation to the provision of social ben efits and services rendered “outside” market rules i.e. where there is no sales transaction. Revenue for a public sector entity is not u sually related to the volume of institutional activities carried out (take, for example, all taxes and all financial contributions from higher administrations, etc.). Rarely do these constitute consideration for the granting of goods or services. In other words, the synallagmatic connection between in- come and expenses in these context wanes, whilst reve- nues and charges follow asynchronously. This therefore implies that, while income derives from costs-as a result of the production and sales process-revenue may have nothing to do with charges: the body that provides the revenue need not be that which benefits from the provi- sion of goods or services. 3The different notions of accrual basis can be noted by the following comment s by P. ONIDA: “But the revenue and expenses of a commercial business cannot be assimilated, respectively, to earnings and costs of an roduction company for the market exchange. In this company the costs, or better still, complex data of costs—are usually borne on the assumption that they will bring about earnings [...]. However, in a service company, the provision of service s and the incu rring of expens es, i.e. the outgoings , are not stimulated by potential earnings relating to such outgoings, but rather to satisfy the needs of the entity to which the company belongs.It is also true that the volume of revenue influences expenses and that the means at a company’s d isposal affects the propensity to consume, and its increase seems to cause and stimulate needs, especially those that are more supe rfic ial” . 4The difference between services on “individual request” and on “co llec- tive request” is well-known. The former are particular and divisible ser- vices, i.e. services that satisfy specific needs and for which it is possible to quantify the service rendered to the individual beneficiary. The latter are general and indivisible services, i.e. services of collective inte rest and fo which it is not possible to quantify the benefit provided to the user. Clearly, only the services on individual request can be managed in accor- dance with a business regime, i.e. by requesting specific consid eration fo the service, regardless of whether the amount of such consideration is regul ate d by m arket pr ice s or re flec ts a po lit ical pric e. Furthermore, this highlights the public sector’s duty to redistribute nat i o na l we alth. The amount of costs and charges is closely related to the amount of institutional activities carried out, since one generates the other. Following such logic, revenue is obtained by virtue of a “formal commitment”, or by a “solemn promise” to use it to cover the costs and charges necessary to carry out the required social functions. Such “formal commitment” and “solemn promise” are contained in the annual budgets which thus become not only the legal bond which regulates the relationship be- tween individual public administrations and their gov- ernment entities, but also—on a business level-represent the main element when identifying the correlation be- tween cause and effect of revenue and management costs and charges. The legally binding requirement for public administra- Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 31 tions to budget and management forecasting can now be seen in light of its unavoidable managerial aspect, since the significance of economic analysis would be compro- mised without them. In fact, in business, management forecasting is neces- sary and appropriate, but not essential; in this context, “corporate governance” works “rationally” [21] expect- ing earnings as soon as costs are incurred; the economic result for the years is relevant regardless of whether any management planning has taken place. In public administrations, on the other hand, the ex- pected profits must be identified and agreed upon before any costs are incurred and, more importantly, before the revenue has been collected. A causal link must therefore be established in the planning phase so as to allow the economic result to be of greater informational value in indicating management progress. In this case, a net defi- cit could also be the result of a conscious and express decision [22]. Furth ermore, cos ts and charges mu st be conside red, as a rule, on an accrual basis—not when the corresponding earnings are made, as is expected for profit-oriented companies—but when the following two conditions are met: production cycle of goods and services is over; the service was allocated. There is a transfer of property rights as a result of an individual request, in the case of goods or services, or the goods or services become a public benefit in the case of social and service activities provided on the basis of a collective request. The participation of the costs and charges in the pro- duction and distribution cycles takes place when: the costs incurred in a financial year by a company relate to items which are not longer relevant by the end of that financial year, or their future relevance cannot be as- sessed or calculated; the accrual basis of costs can also be determined on the basis of cost flow forecasts or, fail- ing a more direct link, of the repartition of the long-term utility or functionality from a systematic and rationale basis (for ex. amortisation); the potential social utility of the factor of production which incurred costs in the pre- vious financial years is lower or can no longer be as- sessed; is irrelevant the relationship to the productive process or utility allocation on a rational and systematic basis. There are specific rules concerning the survey of costs concerning long-term activities, namely the production of goods and the provision of services whose productive process goes beyond a financial year. Revenue, as well as all the positive economic compo- nents provided by non-exchange transaction, must be linked to the costs and charges of that financial year. That link, which is opposite to that concerning income and expenses, represents a fundamental corollary to the principle of accrual accounting for facts of management which characterise the activities of non-profit-oriented companies. It is therefore essential that expenses in a financial period, whether definite or presumed, be set against the respective income. Such a link can be achieved: by a causal link between income, costs and charges. The link can be made analytically or directly (for example: fund-specific taxes, tied loans, en tailments, etc.); by the direct allocation of income to the financial statement of a financial period. This can be time-related (for example, year-based taxes) or disjointed in the cost/taxes correlation (for example, income from gains); by transferring, from the balance sheet to the income statement, income that was previously obtained but which is linked to one or more activities carried out in that financial period. In the last example cited above, there is a need to de- fine a specific set of rules in order to properly account for revenue provided to carry out long-term activities. These are, typically, grants given by the State and other gov- ernment entities. It becomes apparent that a proper accounting arrange- ment within a financial statement should reflect the real animus with which such grants are given [23,24]5 and, therefore, should take in to account the accrual basis used when making the effective animus assessments. The animus, intention, purpose and reasons for the grant as well as the possible recipients thereof must, in this context, be differentiated on the basis of the role they play in the management of a single public administration. We can therefore differentiate between grants intended to restore or increase net assets and those intended for “consumption” or, more precisely, for management. The animus, intention or purpose of the grant is often retraceable to the laws of the individual county or to the motivations of the governing entities that have given the funding. Thus, once the reasons for a grant has been identified: grants that represent a transfer of funds de- signed to pursue institutional goals in a lasting and sus- tainable manner are to be considered as an increase in net assets; grants “for management”, designed “for consump- tion” or covering costs and charges of the year’s man- agement will converge into the income statement, among the positive items of that financial period; grants that are to cover specific institutional services over a number of years (carrying out public works, long-term research projects, purchasing fixed assets, etc.) compensate the “social” value generated by the public administration by carrying out its activities; in this case, the grants could be 5On this point, refer to F.G. Grandis, 1996. Similarly, in the case o usinesses, it has been said: Riteniamo che il metodo più corretto per la contabilizzazione dei contributi in conto capitale debba essere scelto facendo riferimento alle finalità e alle peculiarità di ogni iniziativa agevolata, considerando anche le modalità in base alle quali tale inizia- tiva si inserisce nell’ambito dell’economia dell’impresa che ha fruito del contributo; solo in questo modo può essere valutata la validità di un determinato approccio e l’efficacia informativa del conseguente criterio contabili. Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 32 treated like deferred income i.e. “deferrals”, or accounted for as a specific liability passive entries to be linked to the cost incurred to carry out the activities for which the grant was given, by using the accounting procedure of “sterilization”6. In the latter case, the grant could represent, on an ab- stract level, a “ommitment debt” 25] taken against the community for future services to be rendered or, more precisely [26], in the form of “true accrual basis reve- nues” In this manner, the balance sheet counterbalances a specific funding source with a specific on-going in- vestment, thus highlighting the binding objective of the grant. In conclusion, a principle of accrual accounting tai- lored to public administrations does indeed exist. Such a principle, in some aspects, is the opposite of that which applies to profit-oriente d companies. Only in this manner can the economic result for the period of a “non-business” company be of relevance. 4. The Importance of the Economic Result for the Year The different notion of the accrual basis for public ad- ministrations finds a logical, strategic and managerial meeting point with “rofit-oriented” businesses. The economic result of a profit-oriented business indi- cates, when positive, that the year has closed profitably, yielding a net earning; conversely, a loss is recorded when a year is unprofitable. In public administrations, like in all “non-business” companies, the economic result of a financial period is not viewed in the same manner [27]. In fact, when a par- ticular public administration constantly generates a net surplus, it is considered not to have allocated all of its resources to reaching its institutional goals. Rather, it is considered to be making an undue pro fit and to be asking citizens to make an excessive sacrifice in light of real needs and the actual services provided. In fact, such a scenario effectively indicates that re- sources can be assigned to services through an increase of charges and of costs which relates to: an increase in the number of users and beneficiaries; an increase in the type of services o ffered; an increase in the quality of ser- vices offered. As an alternative, the net surplus could be placed in a reserve fund in order to address potential situations of short-term deficit [28]7. In fact, in public administrations, there is no payment of dividends to individual citizens. In any event, should one not want to take any of the steps described above, one could still: lower the prospective political price of the provision of the services in question; request less funding from the State, which can thus allo- cate such resources to the pursuit of oth er public policies; return the surplus to the government entities. A positive economic result of the year is not consi- dered to be a “profit” as it is understood in “business-ori- ented” companies—It rather acquires the meaning of a “saving” [5]8. Such “saving” is justifiable only in the short-term, provided it does not affect the quantity or quality of the services [29], or if it is used to cover short- term deficits or fund future services. Instead, it will be seen as a “harmful” saving if it detracts funds from the social objectives sought by the government entity, or if it requires citizens or local councils to prov ide an excessive contribution for services rendered to the community. On the other hand, the prolonging of a deficit situation 6The term “sterilization” comes from the fact that, through such an operation, the economic result from costs incurred is sterilized, driven by the same activities for which the contribution was given. For exam- ple, in the hypothesis that a contribution has been obtained to cover the entire disbursement for the purchase of fixed assets, they following accounting entries will ensue: Credits v/funding Administration Earmarked contributions 100 Fixed assets Debts v/suppliers 100 Treasurer (bank) Credit v/funding Administration 100 Debts v/suppliers Treasurer (bank) 100 When carrying out writing, adjustment and general account closing, the following entries will ensue: Fixed assets amortization Fixed assets amortization fund 20 Earmarked contributions Earmarked contributions implementation 20 Income statement Fixed assets amortization 20 Earmarked contributions implementation Income statement 20 Final net asse t Fixed assets 100 Various Earmarked contribu- tions implementation Final net asse t 100 Earmarked contributions 80 Fixed assets amortization fund 20 As stated above, the effect on the income statement and net asset is immediately d e d uc t ib l e. Naturally, in the hypothesis that the contribution of grants related to assets is not able to fully cover the purchase, the income statement write off must be calculated by applying the same amortization rate to the consistency of the contribut ion of grants related to assets. 7“Attraverso la politica del risparmio il criterio informatore del pareggio economico dei risultati di esercizio viene a tramutarsi in una politica di normalizzazione dei risultati di esercizio, che intende, mediante un accantonamento di ricavi di contributi, per fare fronte a maggiori costi di futuri esercizi, a fare sì che nei vari esercizi l’amministrazione non conduca al disavanzo economico, ma a quel pareggio o a quell’avanzo economico che esprima un normale soddisfacimento di bisogni. La politica della normalizzazione dei risultati economici dei vari eser- cizi dovrebbe perciò possibilmente consentire il soddisfacimento di ogni nuovo ed eccezionale ordine di bisogni che l'amministrazione aziendale dovesse affrontare: prevedere quelle temporanee impellenti circostanze non economiche che condurrebbero a squilibri se non fossero fronteggiabili, e dovrebbe anche provvedere a quella mutevole- zza di forze economiche dell'azienda e dell’ambiente che potrebbe condurre a ri s ul t a t i troppo vari nel tempo”. 8“L’avanzo economico è in sostanza un risparmio, che varrà a incre- mentare il patrimonio dell’azienda, e a migliorare la sua condizione economica futura.Va, tuttavia, ricordato che l’avanzo economico non deve considerarsi una méta della gestione erogativa, che è in equilibrio, se i componenti negativi sono pari ai componenti positivi, se cioè si manifes a una situazione di areggio economico”. Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 33 would indicate a serious imbalance in the allocation of resources and, rebus sic stantibus, the wish to pursue institutional goals [30]—in other words, the ability to satisfy the future needs of the community, which the lo- cal administration was set up to address [5]. In this case, the management variables with which to operate should be, in particular, “internal” ones, namely those that can be amended by means of decisions or ac- tions that are not dependent on any external influence. These relate in particular to: carrying out a radical analy- sis of efficiency, return and costs; determining the spe- cific needs to be satisfied, some of which may no longer warrant “public” assistance and can, therefore, be man- aged by the business sector; examining the effectiveness of the services provided. In some cases the fulfilment of needs could even fall below the minimum social neces- sary needs; thoroughly analysing earnings and revenue by means of, for instance, an increase in the political price of some services; increasing the output amount- only the minimum amount of such output is usually binding-by imposing a “price” that is at least greater than the unitary variable cost, without increasing fixed costs. A situation could also arise where the resources avail- able are insufficient to achieve institutional goals. The public sector entity is then compelled to obtain more funding from the State or from general government enti- ties, or if it has fiscal autonomy, to increase the tax levy on citizens, thus increasing the tax burden on the com- munity. However, obtaining greater revenue of this kind should be conditional on the State or government entity bearing this burden expressing a social, political ad macro-economic opinion on this. In brief, the scalar income statement must be read “the other way round”: once the balance statement balances out, the intermediate results, for example EBITD (Earn- ings before Interest Tax and Depreciation), must be as low as possible and not, as for companies, as high as possible. The lower the EBITD, the more income has been al- located to covering institutional costs and charges rather than facing extraordinary and unforesee n o perations. Once again the economic logic behind public admini- strations, as for all non-business organisations, is “in- verted” compared to profit-oriented businesses [31]. 5. The Implementation of Accrual Accounting in the Italian Public Sector In Italy the accounting system of every public admini- stration is characterised by the legislation applicable in its particular field and the authoritative legal bond sanc- tioned by the budget forecast. This also weighs heavily on the general principles and the framework that is set for fina n c i al reporting . As a result of accounting reforms implemented be- tween 1992 and 2003, accounting in Italy has been cha- racterised by its ambiguous rules [12] and its heterogene- ous application, even among public administrations of the same kind. Although the analysis below relates only to obligatory financial reports, accounting principles in Italy can be summarized as follows: 1) The state accounting system provides for the draw- ing up of a “balance sheet”; in 1997 a cost accounting system was introduced, but which does not, however, provide general results or an economic appraisal9; the general principles of this system were extended to re- gional level in 200010; 2) Provisions ap plicable to local authorities (provinces and councils) since 1995 enforce the mandatory “balance sheet” and “income statement” schemes, but leaves to their discretion the ways in which to introduce accrual accounting11; on analysis, there are remarkable differ- ences among the accounting systems of over 8000 local authorities, despite the fact that a specific body was set up to draft u n iform accounting principl e s12; 3) Since 1992, the accounting method to be used by bodies linked to the National Health Authority (Aziende del Servizio Sanitario Nazionale) is that set out in the provisions of the Italian civil code applicable to limited liability companies, although regional authorities the power to establish more detailed rules13; consequently, this has resulted in 21 different legal regimes (19 regions and 2 autonomous provinces) being applicable to 250 public health companies scattered throughout the coun- try; 4) Since 2003, the rules applicable to national institu- tional entities (welfare entities, research entities, Gov- ernment entities, national parks, etc.) are essentially analogous to those of local authorities; the rules in fact specify the general accounting principles, including the accrual basis principle14. Based on the analyses carried out, public administra- tions falling under points (b) and (d) use the “theoretical” accrual basis principle defined in chapter 3 of this paper. This is substantiated by: the latest version of the ac- counting principles publish ed by the National monitoring centre for the finance and accounting of local authorities 9L. 94/1997 e D.Lgs . 279/1997, Ar t i cle 10. 10L. 208/1999 and the subsequent D.Lgs. 7 6 / 2 0 00 . 11D.Lgs. 77/1995 transposed by D.Lgs. 267/2000. Concerning accrual basis accounting, see Article 232 of the D.Lgs.267/2000. 12This organization, called “Osservatorio sulla finanza e la contabilità degli enti locali”, is provided for by Article 154 of the D.Lgs. 267/ 2000. 13Lgs. 502/1992, Art. 5.Regional bodies have aligned themselves to these standard with considerable delay and, even now, there are entities ertaining to the National Health Authority that have only formally introduced accrual basis accounting. 14See addendum n.1 of the President of the Italian Republic Decree D.P.R. 97/2003. Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 34 (Osservatorio per la Finanza e la Contabilità degli enti locali), for administrations falling within point (b) [32]; both in the text of the law itself and the technical docu- mentation relating to its publication [33]. Furthermore, when analysing the liabilities in the bal- ance sheet15 of institutional bodies, local authorities16 and companies forming part of the Italian National Health Authority17, one can see how multiannual earmarked provided by government entities are recorded under a specific liability entry. Consequently, in order for such data to be used, an accounting “sterilisation” proced ure is necessary, implying the “correlation between revenue and cost” and not the “correlation between cost and earnings”. Recently, within the context of the government account- ing harmonization process provided for in the Italian Constitution18 after a 2001 amendment, public admini- strations have had to adopt accrual accounting19, in addi- tion to—and not in replacement of—traditional public accounting. Accrual accounting will only be of informa- tional value, providing support to managerial processes, but will be devoid of any legal or authoritative value. As a result of the aforementioned prescriptive provi- sions, some common principles of general accounting were set out20, Amongst these is the “accrual basis prin- ciple”, compatible with the results of the theoretical analysis discussed in chapter 3. It is in this very context that IPSAS could be particu- larly useful if they were not the result of a mere unques- tioning transposition of IAS but were able to take ac- count of the particular characteristics of public admini- strations in general and, in particular, those in which the budget still plays a strong “authorizing” role. 6. The Accrual Basis Principle in IPSAS Taking into account IPSAB’s strong attachment to the IAS framework, it seems clear how the accrual basis principle21 has also become the standard for public ad- ministrations that opt for IPSAS. Paragraph 22 of the IAS framework, entitled “accrual basis”, indicates that this basis is useful for the prepara- tion of financial reports. However, it specifies that under this basis, the effects of transactions are recognized when they occur, and not when cash or its equivalent is re- ceived or paid. Consequently, these transactions are noted and merged into their corresponding time frame in annual reports. When comparing this d efinition with the one provided for in the Italian civil provisions22, which provide for an inclusion in the budget of “[…]” period revenues and charges, irrespective of the collection or payment date’, no fundamental differences seem to exist between the two. Here we can also see that the basic idea is to estab- lish a link between costs and earnings, therefore estab- lishing that the economic effect of all the period events must be attributed to th e relevant financial period and not to that where the corresponding payments are made or received. In the light of the above, as well as the concept which was developed at length in chapter 3 relating to the im- possibility of applying the accrual basis principle tout court to the public sector, it becomes apparent that it is necessary to adapt such a standard to the particular characteristics of public administrations. The cash basis has always been taken into account by IPSAS, even though it was intended to be a transitional system though which to reach the “full accrual” system [34]. Only as from 2006 onwards [35] did the IPSASB— aware of the difficulty of extending all the “private” standards to the public sector—undertake the planning of a specific IPSAS framework in which it would have even been possible to redefine the standard of accrual ba- sis23.The last of the four documents issued by IPSASB dates back to January 2012, when the IFAC website pub- lished an Exposure Draft and a consultation paper enti- tled “Conceptual framework for general purpose finan- cial reporting by public sector entities: presentation in general purpose financial reports”. An analysis of the draft documents pertaining to the IPSAS framework illustrates the well-rooted position that the accrual basis should be used in drawing up public accounts. In fact, one can easily appreciate the main ad- vantages24 of using accrual basis for management-related issues. It therefore seems that the findings based on the cash basis provide considerably less information than 22See Article 2423 bis, Italian Civil Code, point 3. 23The expectations of the transactors find their raison d’etre in the fre- quent misapplication of certain IPSAS principles—especially the one connected to accrual basis accounting-were these may not be applicable to public Administrations. The IPSAS framework elaboration has been divided into four stages. AN exposure draft has been published for each stage: 1) Users, objectives, scope, qualitative characteristics,reportin entity; 2) Elements and recognition in financial statements; 3) Meas- urement of assets and liabilities in financial statements; 4) Pre- senta- tion and disclosure. 24This statement can be found on the 31st January 2012 IFAC website entry, which says: “ inancial statements prepared under the accrua basis of accounting inform users of those statements of past transac- tions involving the payment and receipt of cash duringthe reportin eriod, obligations to pay cash or sacrifice other re ources of the entity in the future and the resources of the entity at the reporting date. Therefore, they provide in ormation about past transactions and other events that are more usefulto users for accountability purposes and as input for decision making than is information provided by the cash basis or other bases of accounting and f inancial reporting”. 15See addendum 13 of the D.P.R. 97/2003. 16See model 20 of the D.P.R. 194/1996. 17See D.M. 13/11/2007. 18Art. 117, item n. 3of the Constitution of the Italian Republic. 19Art. 2,item n. 2, point d) of L. 196/2009. 20See addendum 1 of the D.Lgs. 91/2011. Similar regulations are con- tained in addendum 1 of the D.Lgs. 118/2011. 21Paragraph 22 of the IAS framework entitled: “Accrual basis”. Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 35 that obtainable from documents drafted on the accrual basis25. Furthermore, there is no evidence in the IPSAS stan- dards of the need to combine a cash system with accrual basis accounting. However, in Italy many authors [36-40] advocate for an integrated approach to accounting. The coupling of traditional accounting which, by its very na- ture, is suitable for the financial aspects of management, with full accrual basis which can cover also other finan- cial aspects could provide more information to stake- holders, in particular national governments that have signed international agreements on financial stability. As reiterated above, accrual basis accounting estab- lishes a correlation between costs and the income result- ing from bearing such costs. Such income is recorded under the period in which the transaction takes place. However, this begs the question whether one can apply the accrual principle to entities whose revenue derives primarily from non-exchange transactions? Can this ac- crual principle apply to entities where most of their costs are unrelated to their income? Until 2006, none of the IPSAS standards had consid- ered the possibility that income could derive from non-exchange transactions26. A non-e xchang e tran saction implies that the income is not linked to an exchange, but to a levy, to a tax or a transfer. In Italy, the financing of the management of the public sector comes mainly from taxes, transfers from other entities or from the payment of services or products rendered. The latter items fall within IPSAS 9, while the others are subject to IPSAS 23. Taxes are linked to the institutional activities of the entity and to the carrying out of functions that satisfy general societal needs. Taxes, from a legal point of view, can be seen as a forced levy on wealth, while, from an economic point of view, they constitute indirect com- pensation for providing services to society [41]. Gene- rally speaking, taxes can be collected directly by the in- dividual public entity or can be acquired indirectly by means of transfers from other entities. Based on how they are collected, they can be divided into levies and taxes. Levies are linked to income and assets—and not to the activities of the public body. Taxes, on the other hand, are linked to certain financial operations carried out by the public sector for the benefit of citizens-despite the fact that the beneficiary need not be the person having paid the tax. Transfers are a source of indirect funding because they come from a system of public relations that is established between different government levels and which varies according to the public governance model adopted. Fur- thermore, no specific correlation exists inasmuch as their entity depends on the organization and provisions which vary from country to country. The major criticism voiced in relation to IPSAS 23 is the use of the accrual basis—in its traditional sense— when having to attribute to one period rather than another income obtained from non-exchange transactions. Based on an analysis of cases in some European coun- tries where IPSAS have been implemented, the principle of accrual accounting is subject to a specific derogation for non-exchange transactions. Such derogation has re- sulted in the cash accounting principle being applicable in order to allocate all income deriving from non-ex- change transactions. Conversely, under the accrual basis principle, tailored to the public sector, as described in chapter 3, income deriving from non-exchange transactions could have been attributed not to a cash accounting system, but to the economic relevance of charges for which they were mandatorily taxed. 7. Conclusions In Italy, the public sector accounting harmonization pro- ject should have begun in 2001, as a result of the amendment of Article 117 of the Italian Constitution. However, only at the end of 2009 did the Italian Parlia- ment issue the law that marked the launching of such a project, whic h i s currently on-going. The true incentive for such accounting innovation is the fact that the Italian Government must provide EU- ROSTAT with the data necessary to check compliance with the stability parameters set by the European Coun- cil. EUROSTAT, and ISTAT in Italy, draw up the data in compliance with Regulation (EC) 2223/1996, more commonly known as “ESA 95”, which is a collection of statistical-not accounting-rules. The accounting data un- der ESA 95 pertains to cash flow and not the principle of accrual basis. As a result, the macroeconomic tendency at European level is to give increasing primacy to cash flow. Accrual accounting will gain relevance only if it can bring “added value” in terms of informational content to those who govern single public administrations, i.e. at microeco- nomic and managerial levels. 25The necessity of implementing an accrual bass system is highlighted. In fact, on page 3 of the document we find: “Under the accrual basis o accounting, transactions and other events are recognized in financia statements when they occur (and not only when cash or its equivalent is received or paid). Therefore, the tran actions and events are recorde in the accounting records and recognized in the financial statements o the periods to which they relate”. 26The absence of a IPSAS that could acknowledge non-exchange trans- actions is to be attributed to the derivation of international public sector accounting principles from the private. Due to the difficulty of compa- nies in obtaining this type of revenue, no specific IAS exists. In order to put this into effect, the principle of accrual basis ratified by IPSAS should not be implemented without question by IAS, but should reflect all the par- Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI 36 ticularities and specificities of the public administra- tion. In fact, the IPSAS’ accrual basis standard not consider non exchange transaction effect, such as revenues derive- ing from: general and indivisible services supply; other typologies of contribution provided; where the “causal link” between revenues and charges are inverted. In all likelihood a new definition of the accrual basis principle, applicable to the public sector, would be ap- propriate, not only to modernise public accounting sys- tems but also to avoid regretting having replaced the current public accounting system with the accrual basis accounting system. REFERENCES [1] S. Newberry, “The Conceptual Framework Sham and Its Support for an Even Greater Sham,” Australian Ac- counting Review, Vol. 3, No. 12, 2002, pp. 47-49. [2] S. Ellwood and S. Newberry, “A Bridge Too Far: A Common Conceptual Framework for Commercial and Public Benefit Entities,” Accounting and Business Re- search, Vol. 36, No. 1, 2006, p. 19. doi:10.1080/00014788.2006.9730004 [3] J. Perrin, “From Cash to Accruals in 25 Years,” Public Money & Management, Vol. 18, No. 2, 1998, pp. 7-10. doi:10.1111/1467-9302.00108 [4] I. Lapsley, R. Mussari and G. Paulsson, “On the Adoption of Accrual Accounting in the Public Sector: A Self-Evi- dent and Problematic Reform,” European Accounting Re- view, Vol. 18, No. 4, 2009, pp. 719-723. doi:10.1080/09638180903334960 [5] P. E. Cassandro, “Le Gestioni Erogatrici Pubbliche,” Unione Tipografico-Editrice Torinese, Torino, 1960. [6] G. Cerboni, “Quadro Di Contabilità Per Le Scritture in Partita Doppia Della Ragioneria Generale Dello Stato,” Stamperia Reale, Roma, 1877. [7] G. Cerboni, “La Ragioneria Scientifica E La Sue Relazioni Con Le Discipline Amministrative E Sociali,” E. Loescher e C., Roma, 1886. [8] J. Schrott, “Lehrbuch Der Allgemeinen Verrechnung- swissenschaf,” Friedrich Rohlicek, Prague, 1856. [9] F. G. Grandis, “Il Conto Economico Nei Documenti Con- tabili Degli Enti Pubblici,” Kappa, Roma, 1995, p. 29. [10] F. Pezzani, “L’evoluzione Dei Sistemi Di Contabilità Pubblica,” Azienda Pubblica, Vol. 18, 2005, pp. 561-565. [11] A. Amaduzzi, “Aziende Di Erogazione. Primi Problemi Di Organizzazione, Gestione E Rilevazione,” Principato, Messina-Milano, 1935, p. 130. [12] F. G. Grandis, “Le Ambiguità Nelle Riforme Dei Sistemi Contabili Pubblici,” Quaderni Monografici RIREA, Vol. 47, 2006, p. 10. [13] B. McCulloc and I. Ball, “Accounting in the Context of Financial Management Reform,” Financial Accountability and management, Vol. 8, No. 1, 1992, pp. 7-12. doi:10.1111/j.1468-0408.1992.tb00137.x [14] M. Evans, “Corporate Gove rnance,” In: P. Jackson and M. Levender, Eds., The Public Services Yearbook, Chapman and Hall, London, 1995. [15] D. Heald, G. Georgiou, “Resource Accounting: Valuation, Consolidation and Accounting Regulation,” Public Ad- ministration, Vol. 73, No. 4, 1995, pp. 571-579. doi:10.1111/j.1467-9299.1995.tb00846.x [16] T. Mellor, “Why Local Governments are Producing Bal- ance Sheets,” Australian Journal of Public Administration, Vol. 55, No. 1, 1996, pp. 78-81. [17] J. Guthrie, “Application of Accrual Accounting in the Australian Public Sector. Rhetoric or Reality,” Financial Accountability and Management, Vol. 14, No. 1, 1998, pp. 1-19. doi:10.1111/1468-0408.00047 [18] M. Aiken and C. Capitanio, “Accrual Accounting Valu- ations and Accountability in Government: A Potentially Pernicious Union,” Australian Journal of Public Admini- stration, Vol. 54, No. 4, 1995, pp. 564-576. doi:10.1111/j.1467-8500.1995.tb01169.x [19] N. Coon, “Reservation about Governments Producing Balance Sheets,” Australian Journal of Public Admini- stration, Vol. 55, No. 1, 1996, pp. 82-85. doi:10.1111/j.1467-8500.1996.tb01185.x [20] P. Onida, “Economia d’azienda,” Utet, Torino, 1971, p. 20. [21] H. A. Simon, “Il comportamento amministrativo”, Il Mu- lino, Bologna, 1958. [22] M. Paoloni and F. G. Grandis, “La Dimensione Aziendale Delle Amministrazioni Pubbliche,” Giappichelli, Torino, 2007, p. 424. [23] F. G. Grandis, “Lo Schema Di Bilancio Delle Aziende Sanitarie Pubbliche,” The Community Economic De- velopment Association of Michigan, Padova, 1996, p. 85. [24] G. Paolucci, “I Contributi in Conto Capitale Nell’Eco- nomia Dell’Impresa. Peculiarità Contabili, Prassi Inter- nazionale ed Indagini Empiriche,” Giappichelli Publisher, Torino, 2001. [25] F. Besta, “La Ragioneria”, Volume I, Seconda edizione, Vallardi, Milano, 1909. [26] P. Onida, “La Logica Ed Il Sistema Delle Rilevazioni Quantitative D’Azienda,” Giuffrè, Milano, 1970. [27] J. L. Chan, “International Public Sector Accounting Stan- dards: Conceptual and Institutional Issues,” McGraw-Hill, Milano, 2008. [28] A. Amaduzzi, “Le Aziende Di Erogazione Primi Problemi Di Organizzazione, Gestione Rilevazione,” Principato, Milano, 1936, p. 123. [29] L. Hinna, M. Meneguzzo, R. Mussari and M. Decastri, “Economia Delle Aziende Pubb liche,” M cGraw -Hill, M ilano, 2006, p. 157. [30] G. Airoldi, G. Brunetti and V. Coda, “Economia Azi- endale,” Il Mulino, Bologna, 1994, p. 125. [31] G. Marcon, “L’evoluzione Delle Teorie Sui Processi Decisionali Delle Amministrazioni Pubbliche, Premessa Per l’Interpretazione Della Riforma Della Contabilità,” Azienda Pubblica, Vol. 24, 2011, pp. 207-221. [32] M. Dell’Interno, “Osservatorio per la Finanza e la Con- Copyright © 2012 SciRes. OJAcct  F. G. GRANDIS, G. MATTEI Copyright © 2012 SciRes. OJAcct 37 tabilità Degli Enti Locali, Principio Contabile n.3. Il Rendiconto Degli Enti Locali,” 2008, Par. 111 and 134, in press. [33] M. dell’Economia e delle Finanze, “Dipartimento della Ragioneria Generale dello Stato, Principi contabili per il bilancio di previsione e per il rendiconto generale degli Enti pubblici istituzionali,” Istituto Poligrafico e Zecca dello Stato, Roma, 2001, pp. 16-17. [34] S. Pozzoli, “The International Public Sector Accounting Standards between Convergence and Conceptual Frame- work,” In: M. D’Amore, Ed., The Harmonization of Gov- ernment Accounting and the Role of IPSAS, McGraw- Hill, Milano, 2008, pp. 3-18. [35] A. Bergmann, “Public Sector Financial Management,” Pearson Education, Harlow, 2001. [36] G. Zappa and A. Marcantonio, “Ragioneria Applicata Alle Aziende Pubbliche Principi Contabili,” Giuffrè, Milano, 1954. [37] A. Amaduzzi, “Studi di Economia Aziendale,” Kappa, Roma, 1995. [38] P. Capaldo, “Il bilancio dello Stato nel sistema di programmazione economica,” Giuffrè, Milano, 1973. [39] E. Borgonovi, “Principi E Sistemi Aziendali Per Le Amministrazioni Pubbliche,” European Garage Equip- ment Association, Milano, 2005. [40] G. Farneti, S. Pozzoli, (edited by), “Principi E Sistemi Contabili Negli Enti Locali. Il Panorama Internazionale, Le Prospettive in Italia,” Franco Angeli, Milano, 2005. [41] E. Borgonovi, “Principi E Sistemi Aziendali Per Le Amministrazioni Pubbliche”, European Garage Equip- ment Association, Milano, 2002.

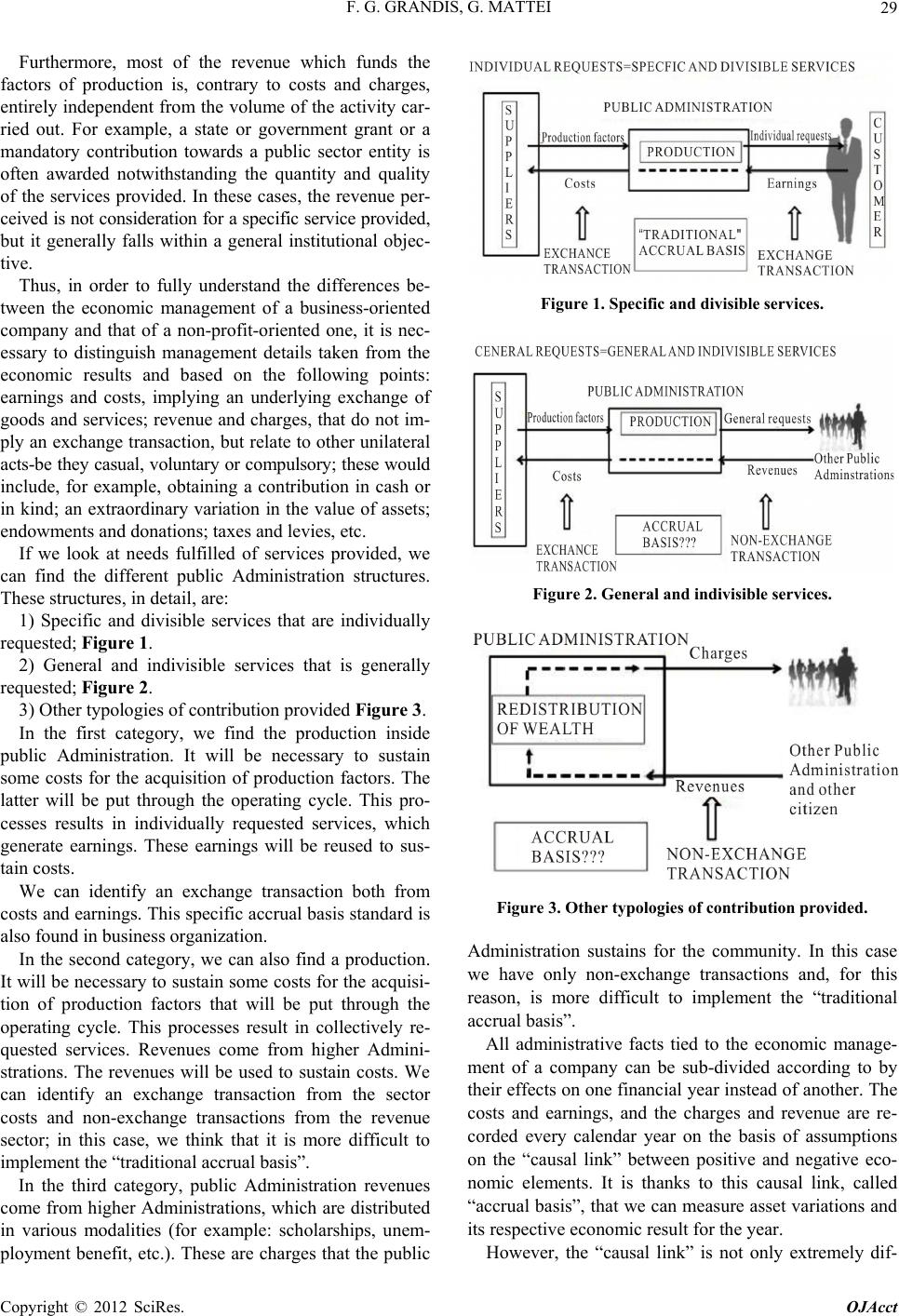

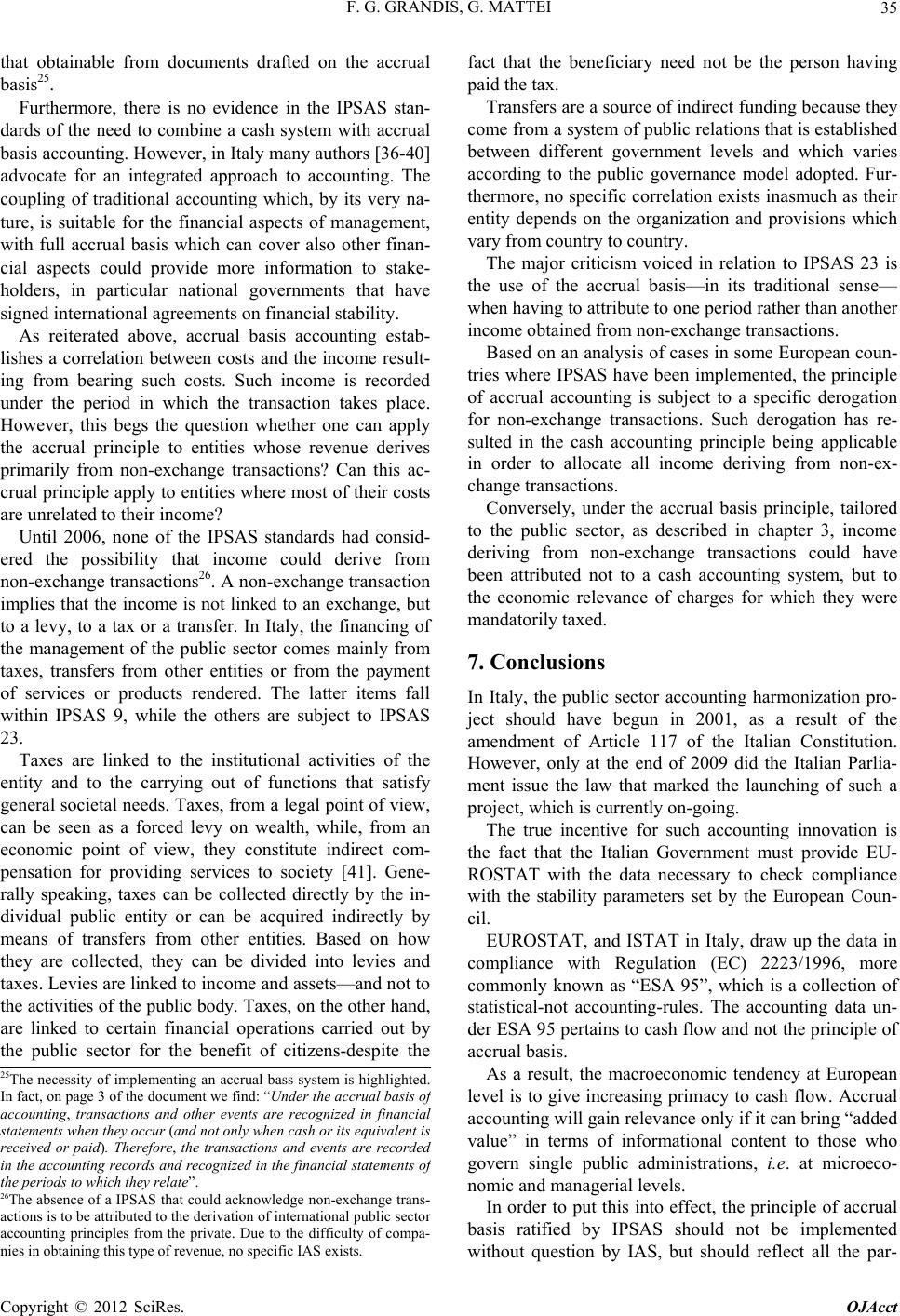

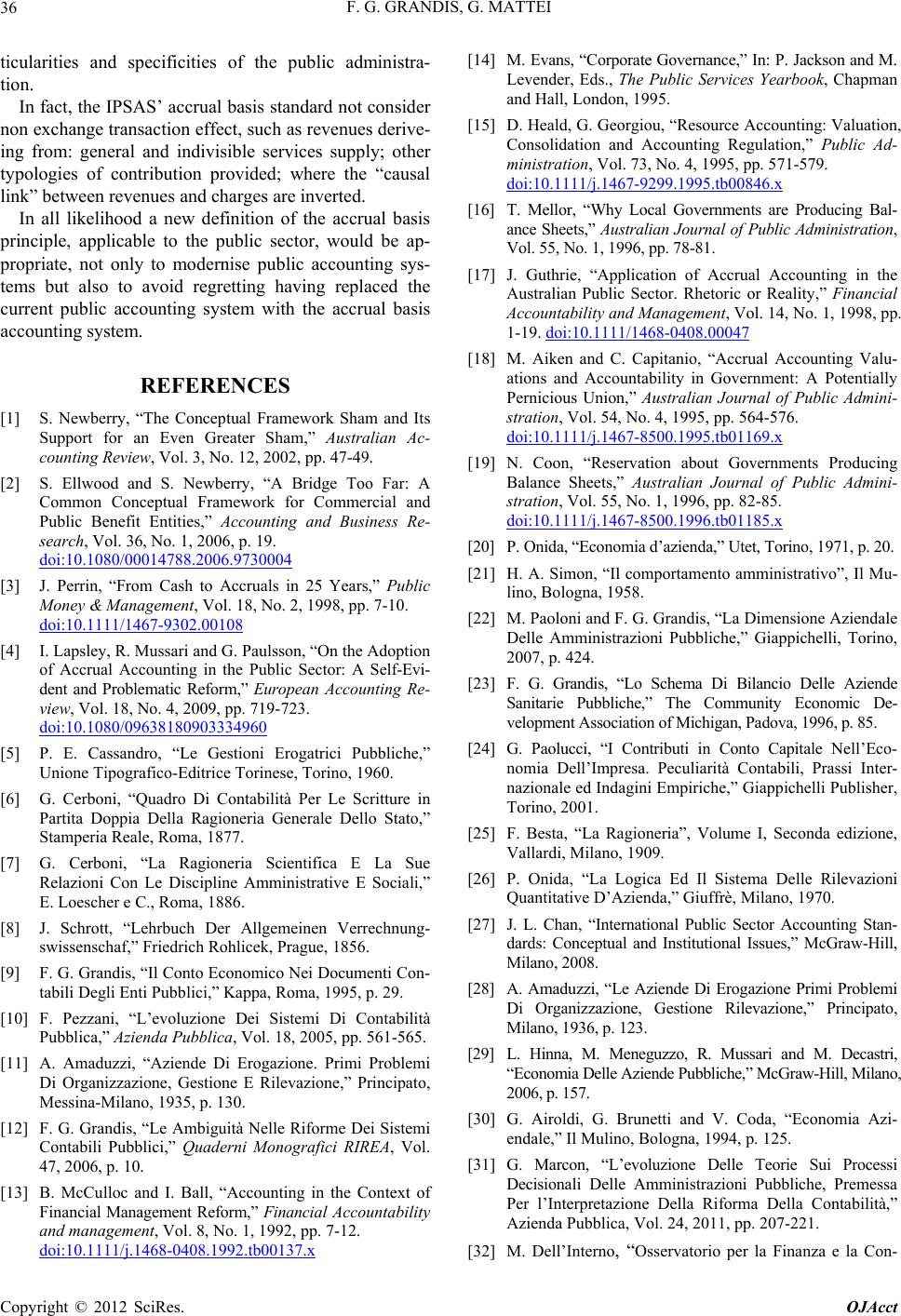

|