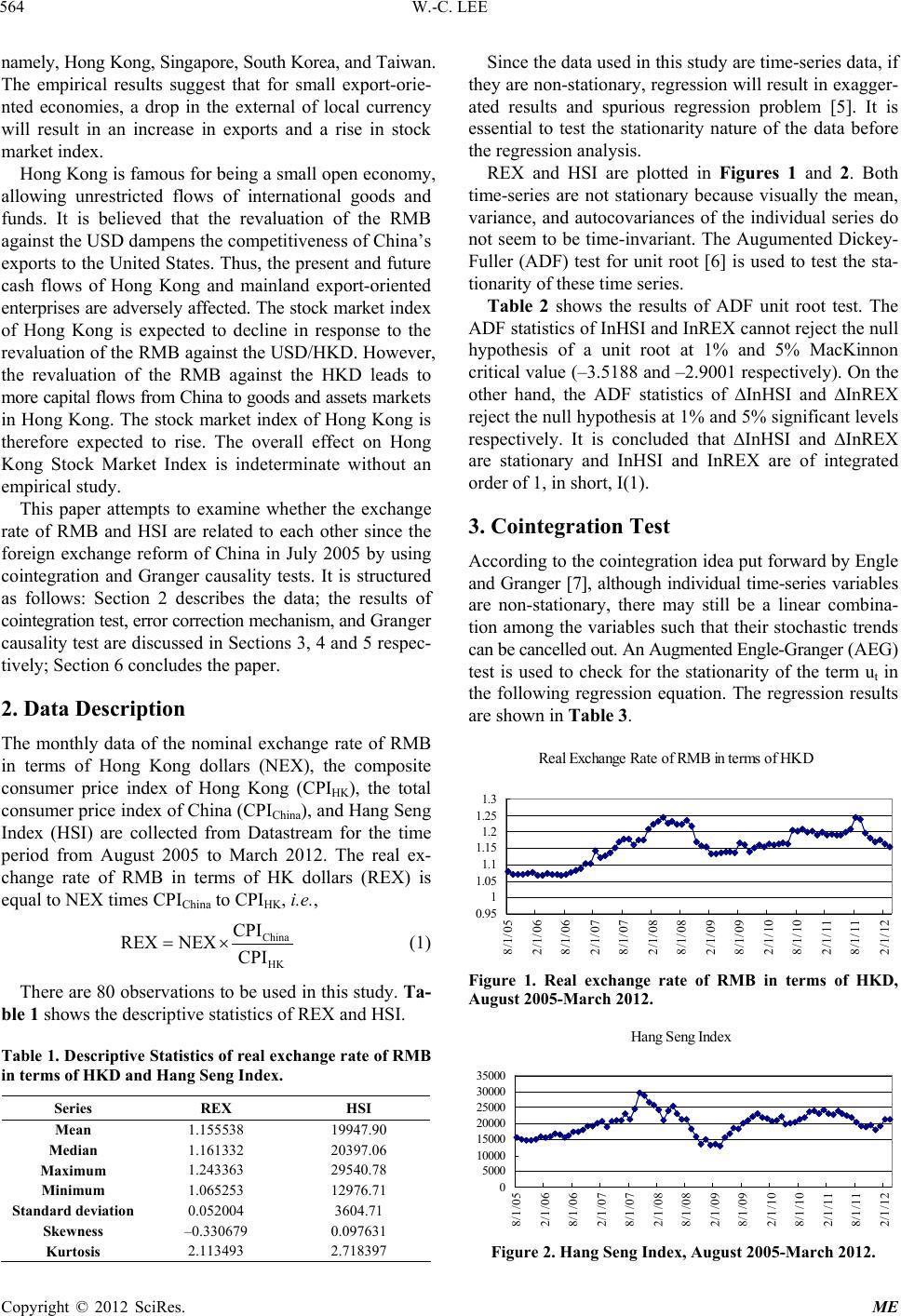

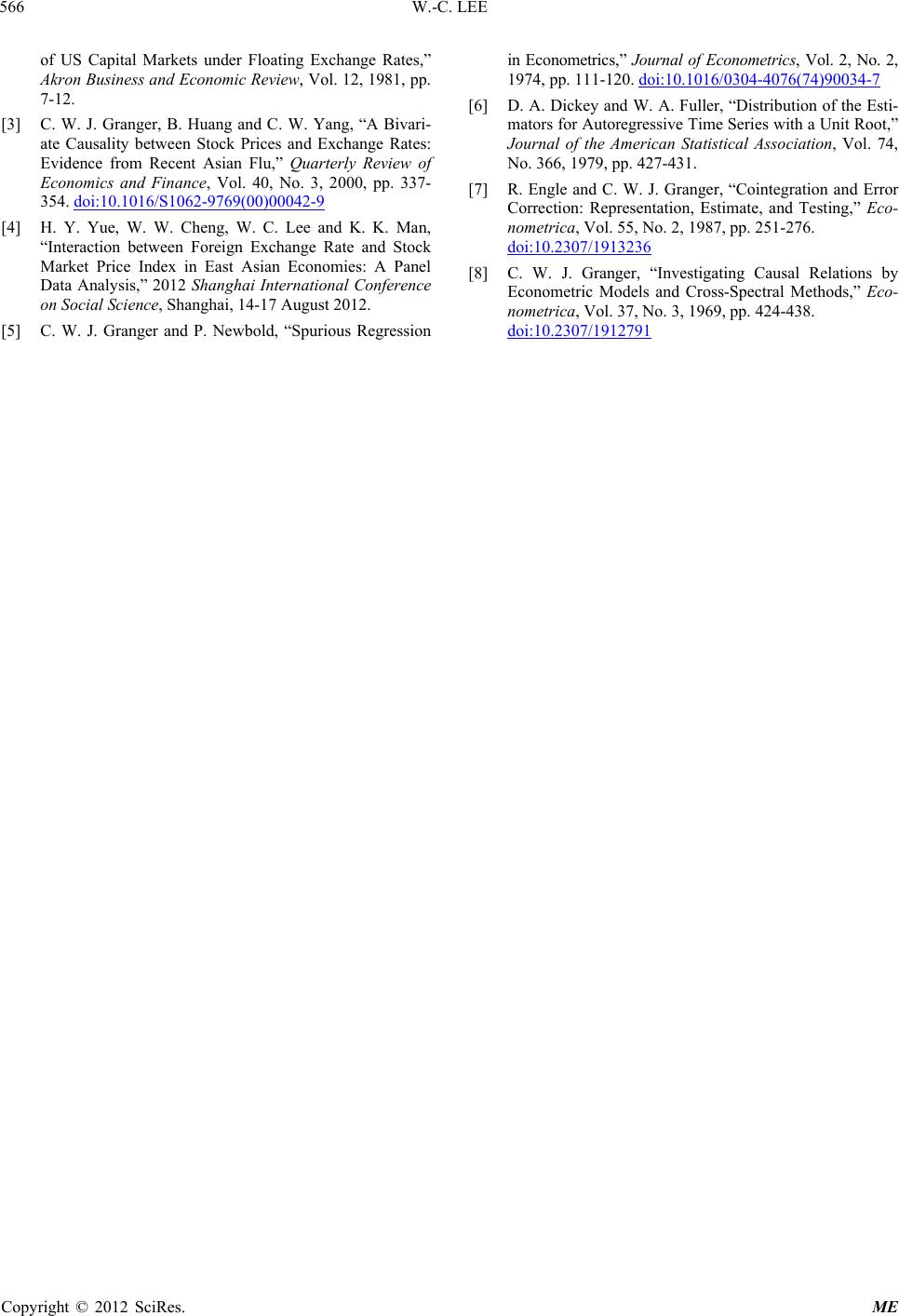

Modern Economy, 2012, 3, 563-566

http://dx.doi.org/10.4236/me.2012.35074 Published Online September 2012 (http://www.SciRP.org/journal/me)

A Study of the Causal Relationship between Real Exchange

Rate of Renminbi and Hong Kong Stock Market Index

Wai-Choi Lee1,2

1Department of Economics and Finance, Hang Seng Management College, Hong Kong, China

2School of Finance, Shanghai University of Finance and Economics, Shanghai, China

Email: wclee@hsmc.edu.hk

Received May 23, 2012; revised June 20, 2012; accepted June 28, 2012

ABSTRACT

This paper attempts to study whether the real exchange rate of Renminbi and stock market index in Hong Kong are re-

lated to each other or not. The study uses cointegration and Granger causality tests on the monthly data of the real ex-

change rate of Renmnibi (RMB) in terms of Hong Kong dollars (REX) and Hang Seng Index (HSI) since the foreign

exchange reform of China in July 2005. The major findings of the study are a) the cointegration test shows that there

exists a long-run equilibrium relationship between REX and HSI; b) the error correction mechanism further evidences

that there is an error correction between REX and HSI in the short run; c) the Granger causality test indicates that there

is causal direction from RMB to HSI but not vice versa.

Keywords: Cointegration Test; Error Correction Mechanism; Granger Causality Test; Renminbi; Hang Seng Index

1. Introduction

In July 2005, the People’s Bank of China (PBoC) aban-

doned the 11-year-old peg of the Renminbi (RMB) against

the American dollar (USD) and replaced it with a man-

aged floating exchange rate based on market supply and

demand with reference to a basket of foreign currencies.

Not surprisingly, currencies in the basket included the

currencies of three trading partners—i.e., the USD, the

euro, and the Japanese yen. Under the new system, ad-

justments in the rate of exchange fluctuation will not only

govern the relationship between RMB and USD, but also

the relationship between RMB and other main currencies

such as the euro and the Japanese yen.

At the same time, the RMB was revalued by 2.1%—

from 8.28 RMB per USD to 8.11 per USD. In September

2005, the PBoC decided to adopt a narrow band of 0.3%

on either side of the central rate within which RMB can

fluctuate against USD. Since then, the RMB has gradu-

ally been revalued against USD. As of 22 May, 2012, the

exchange rate of RMB is raised to 6.33 per USD.

Since 1983, the monetary authority of Hong Kong has

maintained currency stability, defined as a stable external

exchange value of the currency of Hong Kong, in terms

of its exchange rate in the foreign exchange market against

the USD, at around HK$7.80 to US$1. As a result, the

exchange rates of Hong Kong dollar (HKD) in terms of

foreign currencies, such as RMB, follow the exchange

rates of USD in the same direction. As the USD depreciates

against RMB, the HKD depreciates against it accordingly.

The Hong Kong Stock Exchange is Asia’s third largest

stock exchange by market capitalization, behind the To-

kyo Stock Exchange and Shanghai Stock Exchange. Hang

Seng Index (HSI), the most widely quoted gauge of the

Hong Kong stock market, includes the largest and most

liquid stocks listed on Main Board of the Stock Exchange

of Hong Kong. It is a market capitalization weighted index

and comprises 48 constituent stocks of Hong Kong and

Mainland China enterprises. The aggregate market capi-

talization of these stocks accounts for over 65 percentage

of the total market capitalization in the Hong Kong Stock

Exchange.

Classical economic theory suggests a relationship be-

tween the stock market performance and the exchange

rate behaviour. Dornbusch and Fisher [1] and Aggarwal

[2] affirm that currency movements affect international

competitiveness and the balance of trade position, and

consequently the real output of the economy, which in

turn affects current and future cash flows of companies

and their stock prices.

Granger, Huang and Yang [3] find that currency de-

preciation could either raise or lower the value of Asian

companies during the Asian Crisis of 1997, depending on

whether the company mainly imports or mainly exports.

When the stock market index is considered, the net effect

cannot be predicted.

Yue, Cheng, Lee and Man [4] perform a panel data

analysis across four small export-oriented economies,

C

opyright © 2012 SciRes. ME