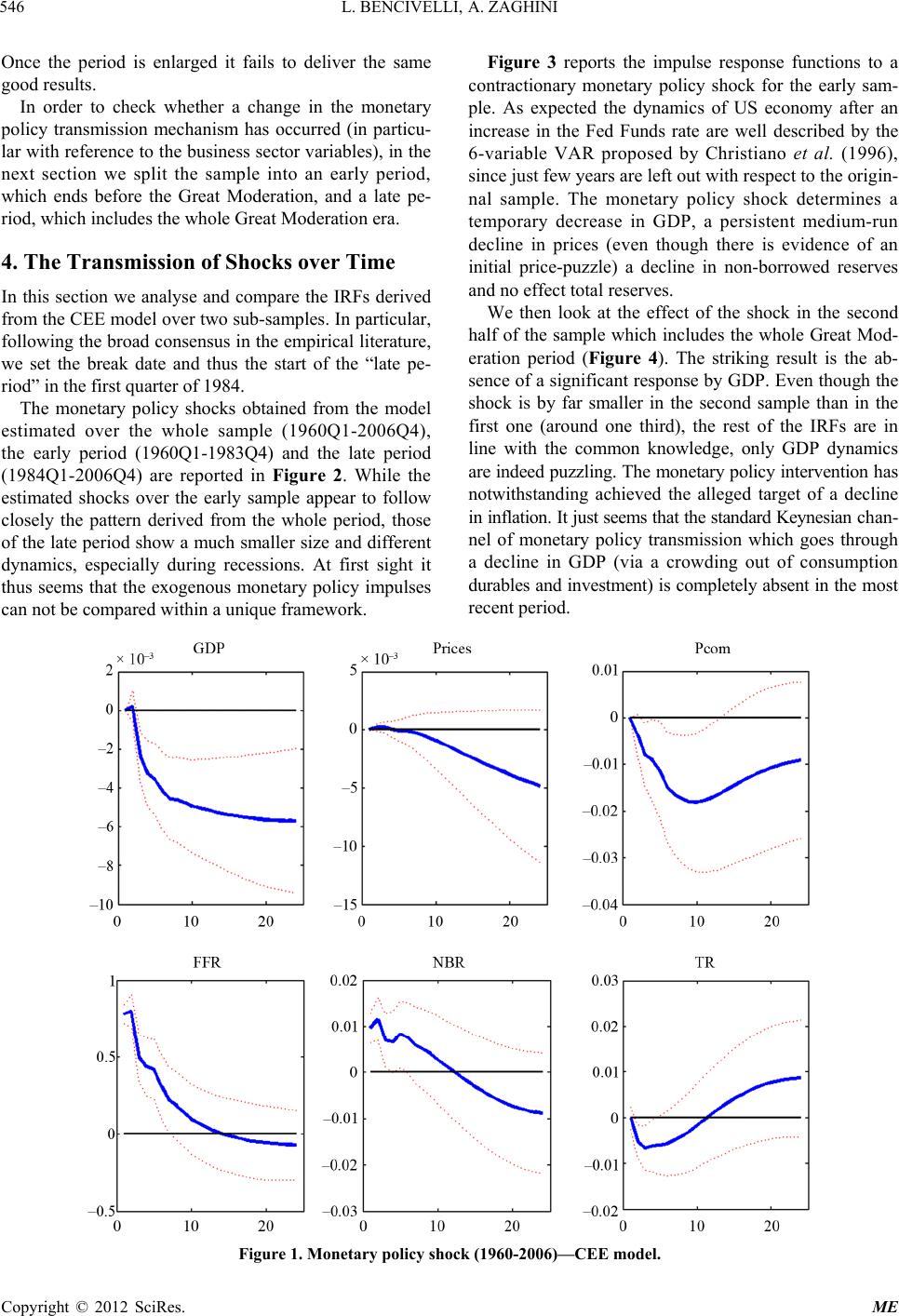

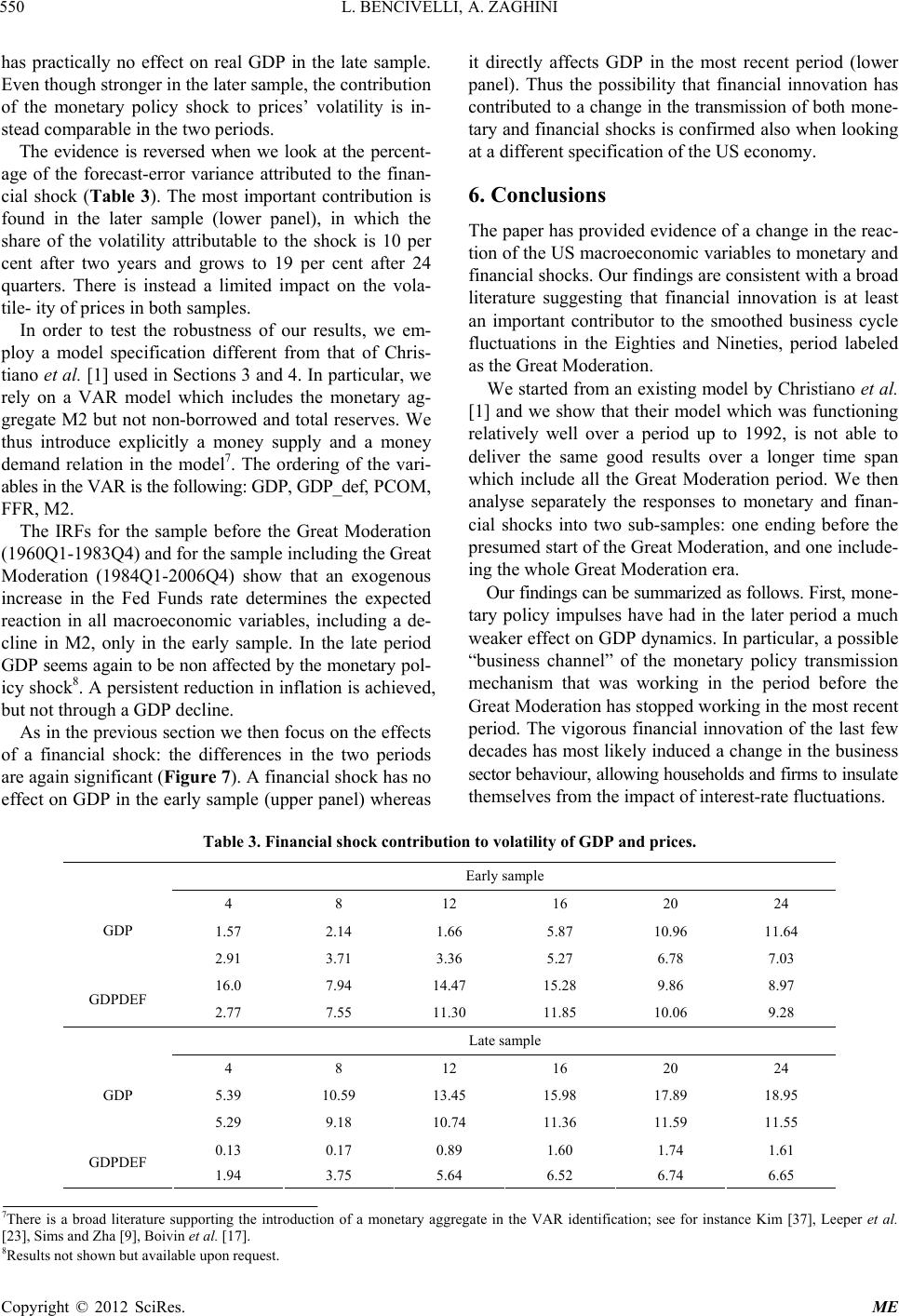

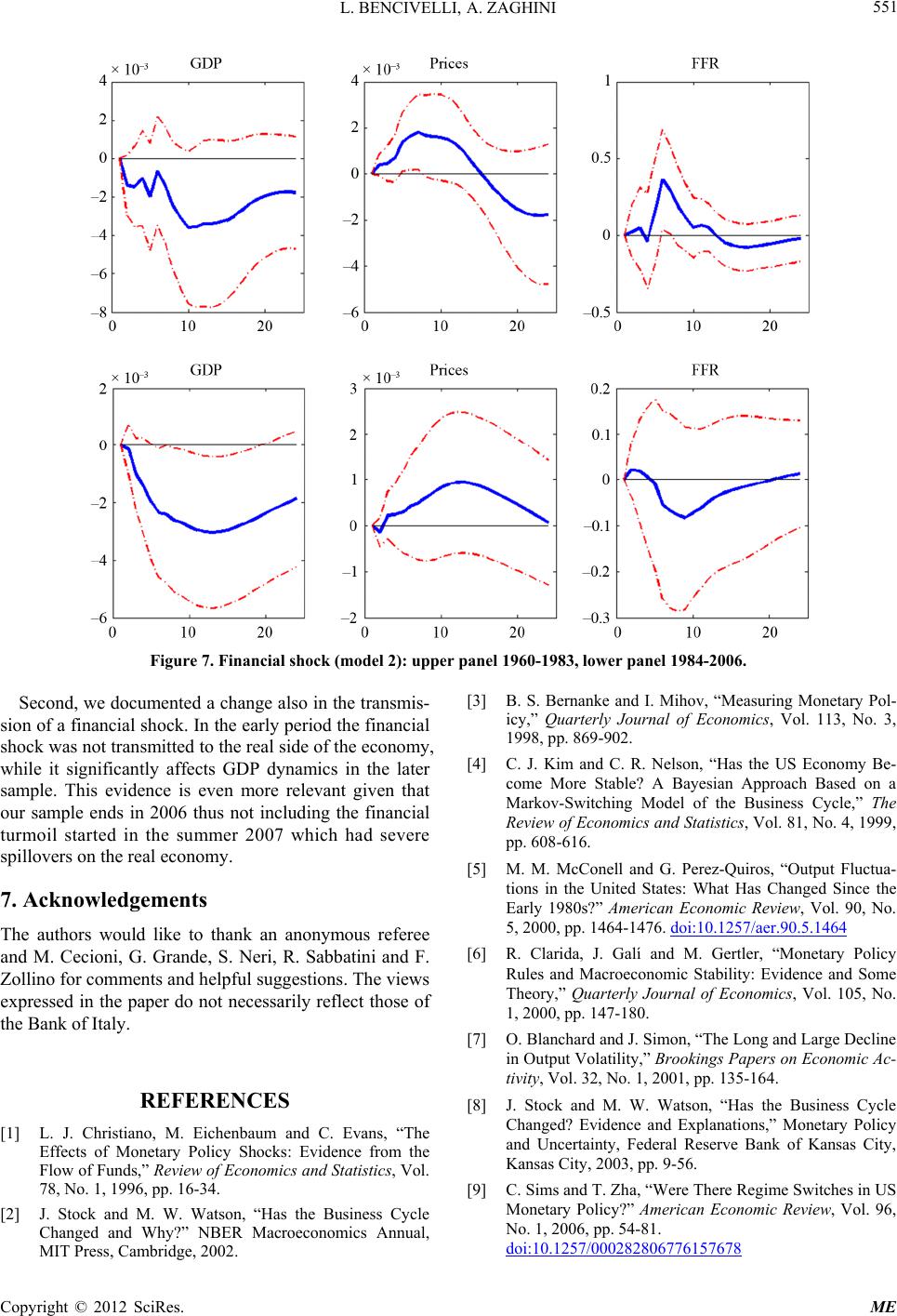

L. BENCIVELLI, A. ZAGHINI

552

[10] T. Lubik and F. Schorfheide, “Testing for Indeterminacy:

An Application to US Monetary Policy,” American Eco-

nomic Review, Vol. 94, No. 1, 2004, pp. 190-217.

doi:10.1257/000282804322970760

[11] J. Boivin and M. Giannoni, “Has Monetary Policy Be-

come More Effective?” Review of Economics and Statis-

tics, Vol. 88, No. 3, 2006 pp. 445-462.

doi:10.1162/rest.88.3.445

[12] D. Giannone, M. Lenza and L. Reichlin, “Explaining the

Great Moderation: It Is Not the Shocks,” Journal of the

European Economic Association, Vol. 6, No. 2-3, 2008,

pp. 621-633. doi:10.1162/JEEA.2008.6.2-3.621

[13] J. Gali and L. Gambetti, “On the Sources of the Great

Moderation,” American Economic Journal: Macroeco-

nomics, Vol. 1, 2009, pp. 26-57.

[14] F. S. Mishkin, “Inflation Dynamics,” International Fi-

nance, Vol. 10, No. 3, 2007, pp. 317-334.

doi:10.1111/j.1468-2362.2007.00205.x

[15] A. Calza and A. Zaghini, “Sectoral Money Demand and

the Great Disinflation in the US,” Journal of Money, Credit

and Banking, Vol. 42, No. 8, 2010, pp. 1663-1678.

[16] B. De Blas, “Can Financial Frictions Help Explain the

Performance of the US Fed?” The B.E. Journal of Mac-

roeconomics, Vol. 9, No. 1, 2009, 27 Pages.

[17] J. Boivin, M. T. Kiley and F. S. Mishkin, “How Has the

Monetary Transmission Mechanism Evolved over Time?”

NBER Working Paper 15879, 2010.

[18] F. Canova and L. Gambetti, “Structural Changes in the

US Economy: Is There a Role for Monetary Policy? ” Jour-

nal of Economic Dynamics and Control, Vol. 33, No. 2,

2009, pp. 477-490. doi:10.1016/j.jedc.2008.05.010

[19] S. Gilchrist, A. Ortiz and E. Zakrajšek, “Credit Risk and

the Macroeconomy: Evidence from an Estimated DSGE

Model,” Unpublished Manuscript, May 2009.

[20] A. Justiniano and G. Primiceri, “The Time Varying Vola-

tility of Macroeconomic Fluctuations,” American Eco-

nomic Review, Vol. 98, No. 3, 2006, pp. 604-641.

[21] S. G. Cecchetti, A. Flores-Lagunes and S. Krause, “Has

Monetary Policy Become More Efficient? A Cross-Coun-

try Analysis,” Economic Journal, Vol. 116, No. 511, 2006,

pp. 408-433. doi:10.1111/j.1468-0297.2006.01086.x

[22] F. Canova and L. Gambetti, “Do Expectations Matter?

The Great Modera tion Revisited,” American Economic Jour-

nal: Macroeconomics, Vol. 2, No. 3, 2010, No. 3, pp. 183-

205.

[23] O. Korenok and S. Radchenko, “The Role of Permanent

and Transitory Components in Business Cycle Volatility

Moderation,” Empirical Economics, Vol. 31, No. 1, 2006,

pp. 217-241. doi:10.1007/s00181-005-0042-5

[24] C. J. Kim, C. R. Nelson and J. Piger, “The Less-Volatile

US Economy: A Bayesian Investigation of Timing, Br-

eadth, and Potential Explanations,” Journal of Business &

Economic Statistics, Vol. 22, No. 1, 2004, pp. 80-93.

[25] A. B. Galvao and M. Marcellino, “Endogenous Monetary

Policy Regimes and the Great Moderation,” The Centre

for Economic Policy Research 2010, Discussion Paper

No. 7827.

[26] M. Gertler and C. S. Lown, “The Information in the

High-Yield Bond Spread for the Business Cycle: Evi-

dence and Some Implications,” Oxford Review on Eco-

nomic Policy, Vol. 15, No. 3, 1999, pp. 132-150.

[27] K. E. Dynan, D. W. Elmendorf and D. E. Sichel, “Can

Financial Innovation Help to Explain the Reduced Vola-

tility of Economic Activity,” Journal of Monetary Eco-

nomics, Vol. 53, No. 1, 2006.

[28] U. Jermann and V. Quadrini, “Macroeconomic Effects of

Financial Shocks,” American Economic Review, Vol. 102,

No.1, 2012, pp. 238-271.

[29] C. Fuentes-Albero, “Financial Frictions, the Financial

Immoderation, and the Great Moderation,” Mimeo, Uni-

versity of Pennsylvania, 2009.

[30] F. Smets and R. Wouters, “Shocks and Frictions in US

Business Cycles: A Bayesian DSGE Approach,” Ameri-

can Economic Review, Vol. 97, No. 3, 2007, pp. 586-606.

doi:10.1257/aer.97.3.586

[31] M. Kiyotaki and J. Moore, “Credit Cycles,” Journal of

Political Economy, Vol. 105, No. 2, 1997, pp. 211-248.

[32] B. S. Bernanke, M. Gertler and S. Gilchrist, “The Finan-

cial Accelerator in a Quantitative Business Cycle Model,”

In: J. B. Taylor and M. Woodford, Eds., The Handbook of

Macroeconomics, Elsevier, Amsterdam, 1999, pp. 1341-

1393.

[33] W. Den Haan and V. Sterk, “The Myth of Financial In-

novation and the Great Moderation,” Economic Journal,

Vol. 121, No. 553, 2011, pp. 707-739.

doi:10.1111/j.1468-0297.2010.02400.x

[34] L. Christiano, M. Eichenbaum and C. Evans, “Monetary

Policy Shocks: What Ha ve we Learned and to What End?”

In: J. Taylor and M. Woodford, Eds., Handbook of Mac-

roeconomics, North Holland, 1999, pp. 65-148.

[35] K. Jang and M. Ogaki, “The Effects of Monetary Policy

Shocks on Exchange Rate s: A Str uctural Vector Error Cor -

rection Model Approach,” Journal of the Japanese and

International Economies, Vol. 18, No. 1, 2004, pp. 99-

114. doi:10.1016/S0889-1583(03)00042-X

[36] H. Uhlig, “What Are the Effects of Monetary Policy on

Output? Results from an Agnostic Identification Proce-

dure,” Journal of Monetary Economics, Vol. 52, No. 2,

2005, pp. 381-419. doi:10.1016/j.jmoneco.2004.05.007

[37] S. Kim, “Do Monetary Policy Shocks Matter in the G-7

Countries? Using Common Identifying Assumptions

about Monetary Policy across Countries,” Journal of In-

ternational Economics, Vol. 48, No. 2, 1999, pp. 387-412.

doi:10.1016/S0022-1996(98)00052-X

Copyright © 2012 SciRes. ME