Is Consumption in the United States and Japan Too Much or Too Little?

Copyright © 2012 SciRes. IB

230

three typical methods: augmented Dickey-Fuller (ADF),

Phillips-Perron (PP), and Kwiatkowski-Phillips-Schmidt-

Shin (KPSS) tests.

The ADF test is often used for empirical estimation;

however, if the series is correlated at higher order lags,

the assumption of white noise disturbances is violated.

The PP test proposes a method by which to control for

higher order serial correlation in a series than is accepted

in the equation. The test makes a nonparametric correc-

tion to the t-test statistic. The test is robust with respect

to unspecified autocorrelation and heteroskedasticity in

the disturbance process of the test equation. Finally,

KPSS time series test is stationary around a deterministic

trend. This test differs from those in common use in that

they have a null hypothesis of stationarity. The test may

be conducted under the null of either trend or nontrend

stationarity. Inference from this test is complementary to

that derived from those based on the ADF. This test is

often employed with ADF to examine the possibility that

a series is fractionally integrated [13].

This article examines the effect of changes in produc-

tion on consumption. The method employed is LS (least

squares) and VAR (vector autoregression). VAR is com-

monly used to forecast systems of interrelated time series

and to analyze the dynamic impact of random distur-

bances on the employed variables. Empirical estimation

and interface are complicated by the fact that endogenous

variables may appear on both the left and right sides of

equations. The use of VAR can avoid this issue. The

variables employed are consumption and production [13].

Also, impulse responses are examined to trace the effect

of a one-time shock to one of the innovations on current

and future values of the endogenous variables.

The sample period is from 1993:1 to 2011:4. The year

1993 was selected for data availability (for Japanese em-

ployment). The data are quarterly. All the data are from

International Financial Statistics (IMF). Around the mid-

dle of 2008, the differences in the economic situations of

both countries appear evident. Since the middle of the

1990s, the Japanese economy has been in recession and

deflation; on the other hand, the US economy has ex-

panded stably except for a few years. Moreover, it has

been said that consumption is too large for economic

conditions in the United States. Whether or not this is

true or should be examined. Also, the effect of produc-

tions shock on consumption is examined. The template is

used to format your paper and style the text. All margins,

column widths, line spaces, and text fonts are prescribed;

please do not alter them. You may note peculiarities. For

example, the head margin in this template measures pro-

portionately more than is customary. This measurement

and others are deliberate, using specifications that an-

ticipate your paper as one part of the entire proceedings,

and not as an independent document. Please do not revise

any of the current designations.

3. Empirical Results

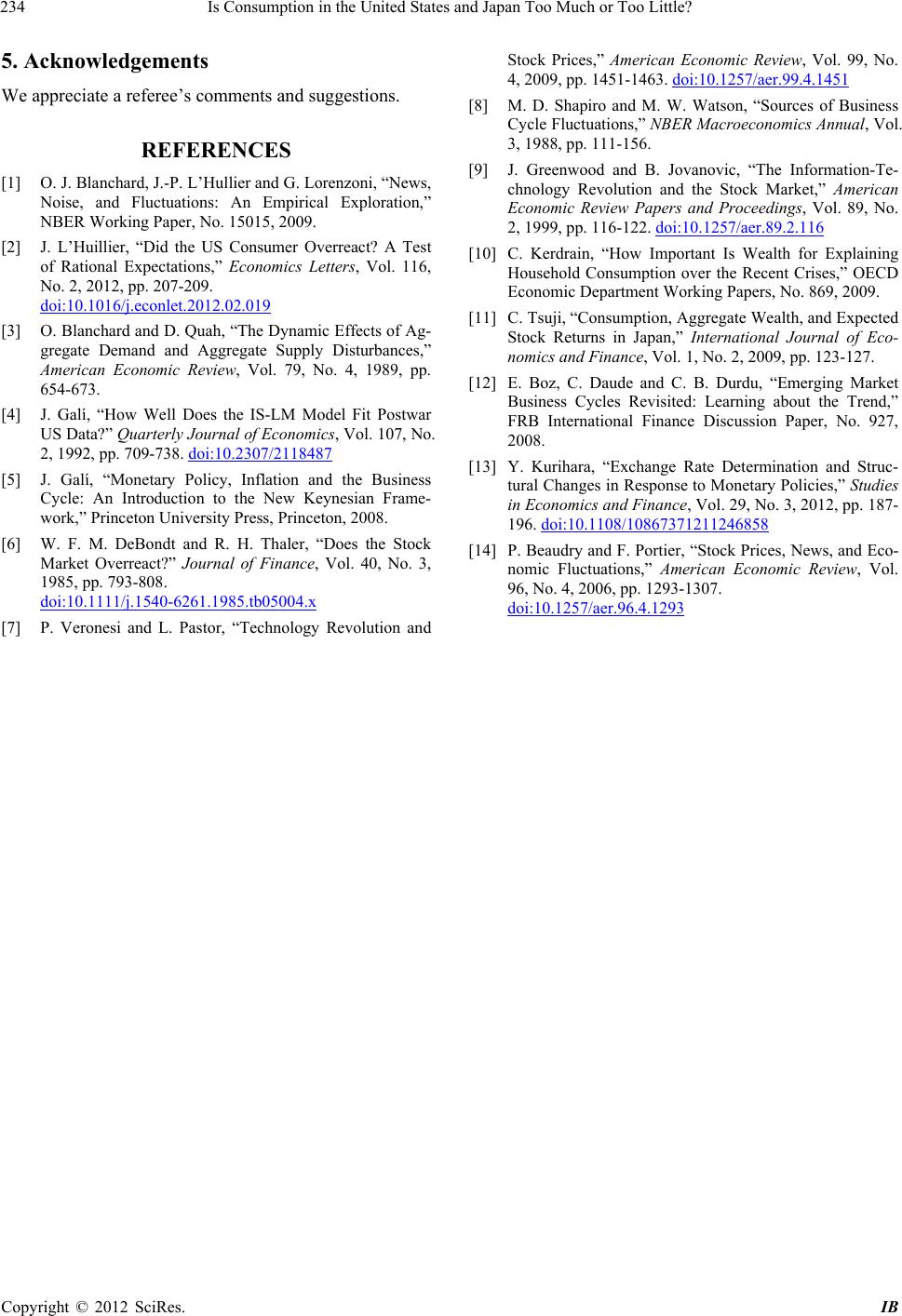

The results of the unit root tests are shown in Table 1.

In some cases, the results are not conclusive. However,

the use of each datum is not problematic especially in the

case of the PP test for empirical estimations.

The results of the regressions for Equation (9) are

shown in Table 2.

The results fit well for both the cases of the United

States and Japan. Also, it is interesting to note that the

coefficients of both countries are similar. Both countries

have common characteristics in consumption patterns de-

spite that both countries have experienced opposite eco-

nomic conditions since the middle of the 1990s. In the

past, US overconsumption has been pointed out; on the

contrary, lower Japanese consumption has been pointed

out. However, in reality, the two countries have similar

characteristics in consumptions.

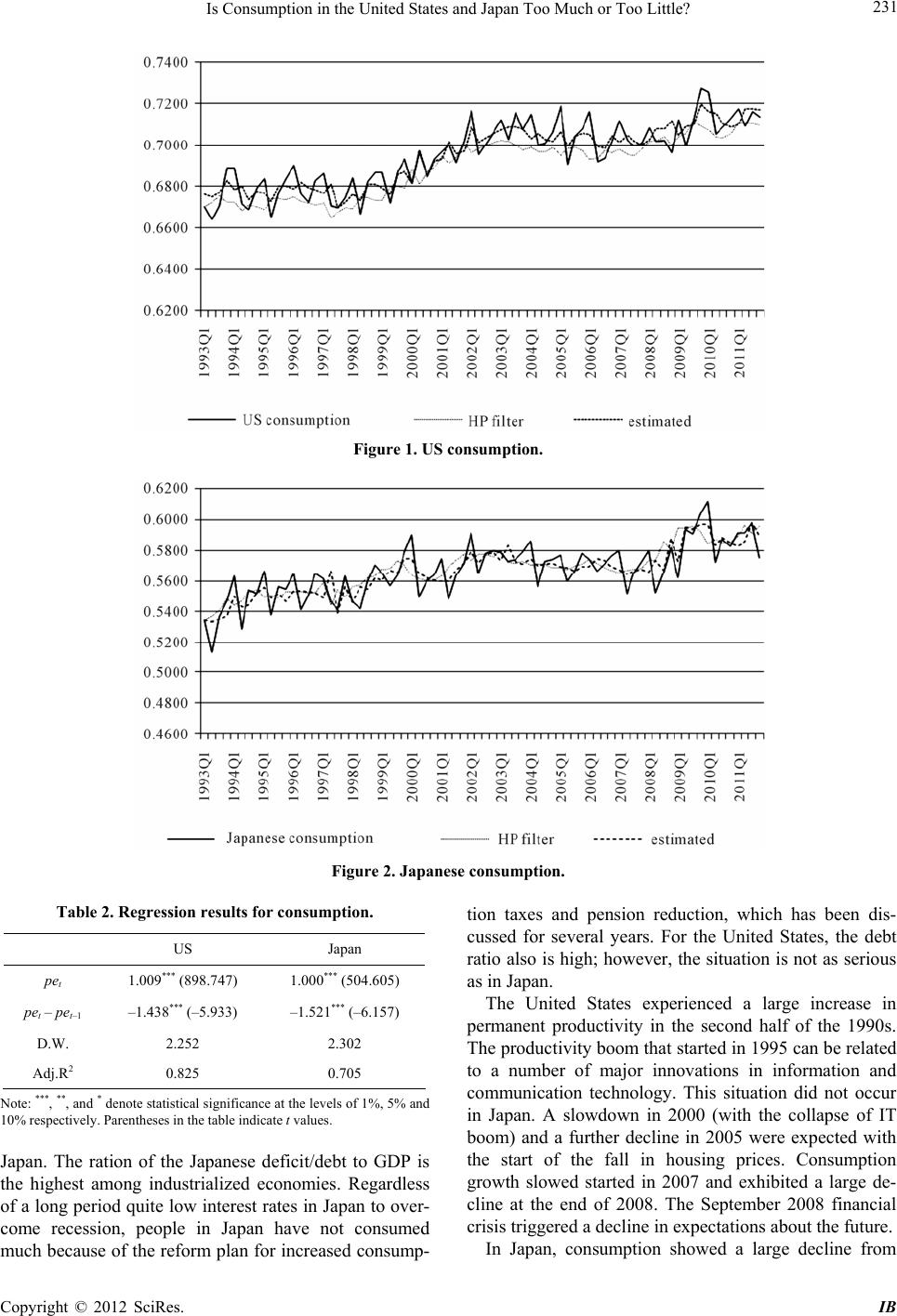

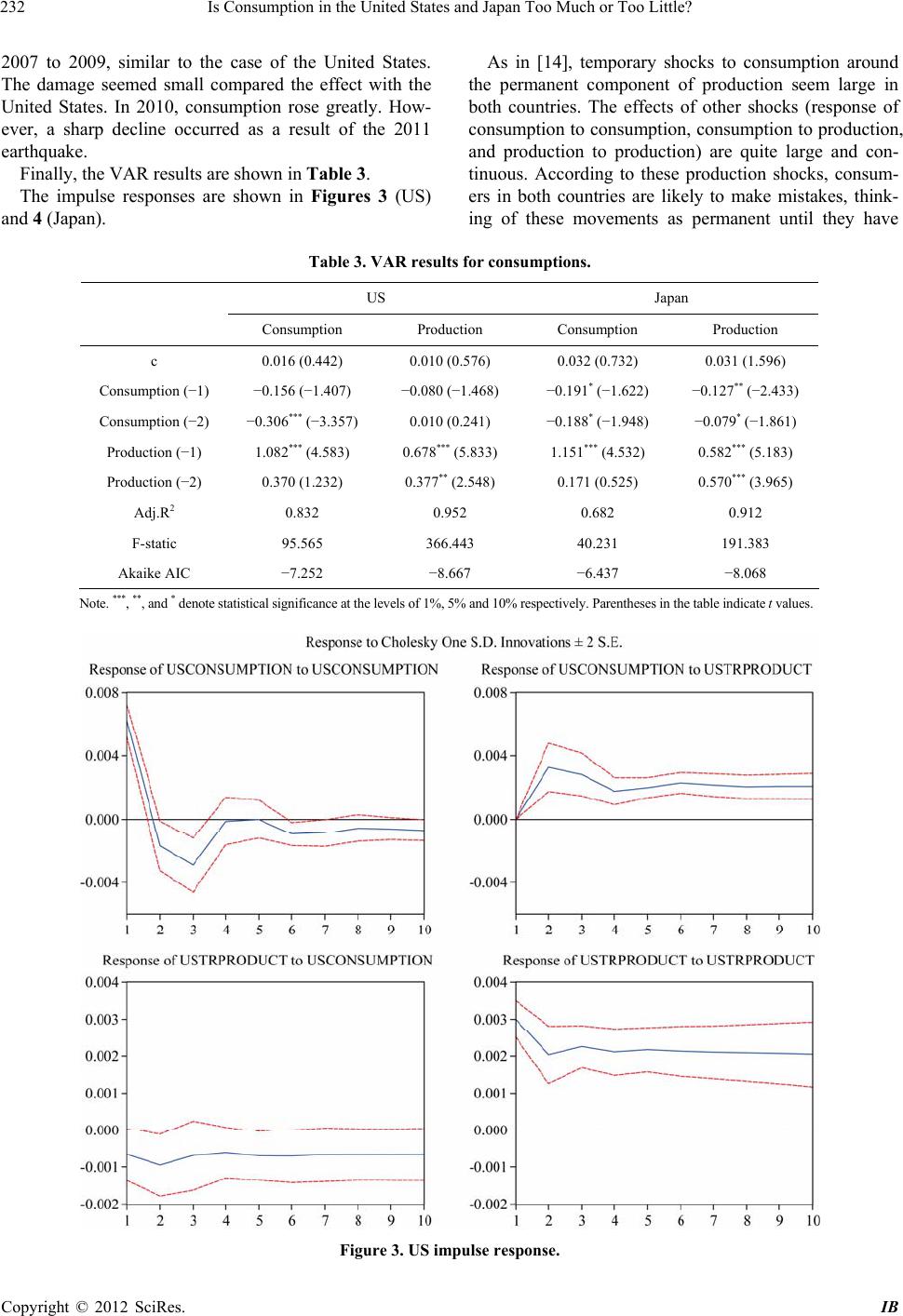

Figure 1 (US) and Figure 2 (Japan) show the con-

sumptions in reality with the HP filter and as estimated.

It should be noted that US overconsumption and lower

levels of Japanese consumption were found in general.

During the sample period, the US economy expanded at

a steady rate; however, the Japanese economy has suf-

fered recession and deflation. In Japan, reduced wages

and uneasiness about the future have both seemed to lead

to declines in consumption. From 1992 to 2011, the

Japanese average wage fell about 11%. No downward

wage rigidity has been found in the past. Also, people are

concerned about the future because of the huge deficit in

Table 1. Unit root tests.

US Japan

ADF PP KPSS ADF PP KPSS

ct –2.555* –3.546*** 1.061*** –2.011 –4.398*** 0.992***

pet –0.916 –2.695* 1.068*** –1.657 –3.512*** 1.048***

pet – pet–1 –1.737 –11.571*** 0.081*** –2.932** –11.470*** 0.065**

Note: ***, **, and * denote statistical significance at the levels of 1%, 5% and 10% respectively. For the ADF and

PP tests, the series contain a unit root under the null, whereas the KPSS test assumes stationarity under the null.