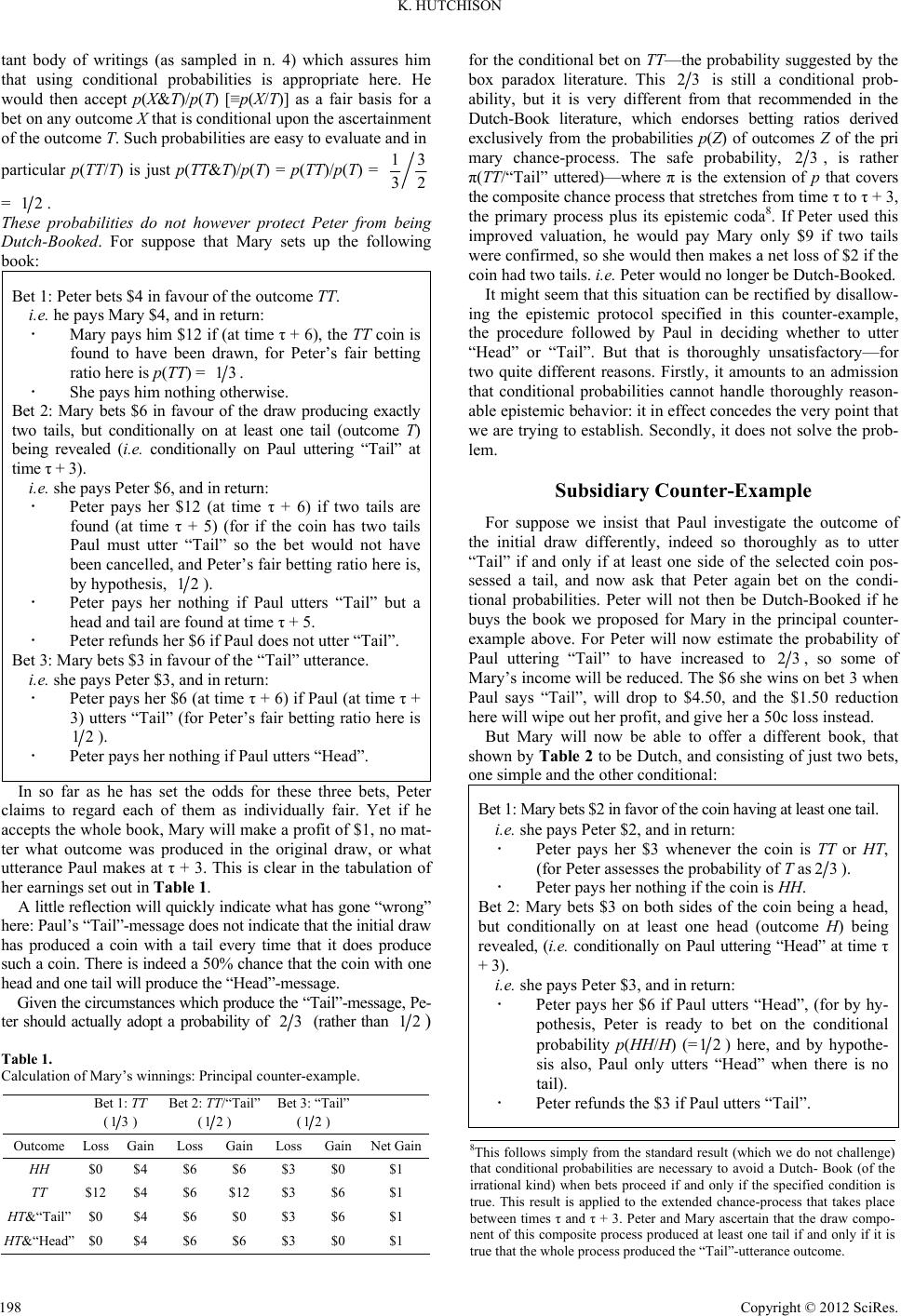

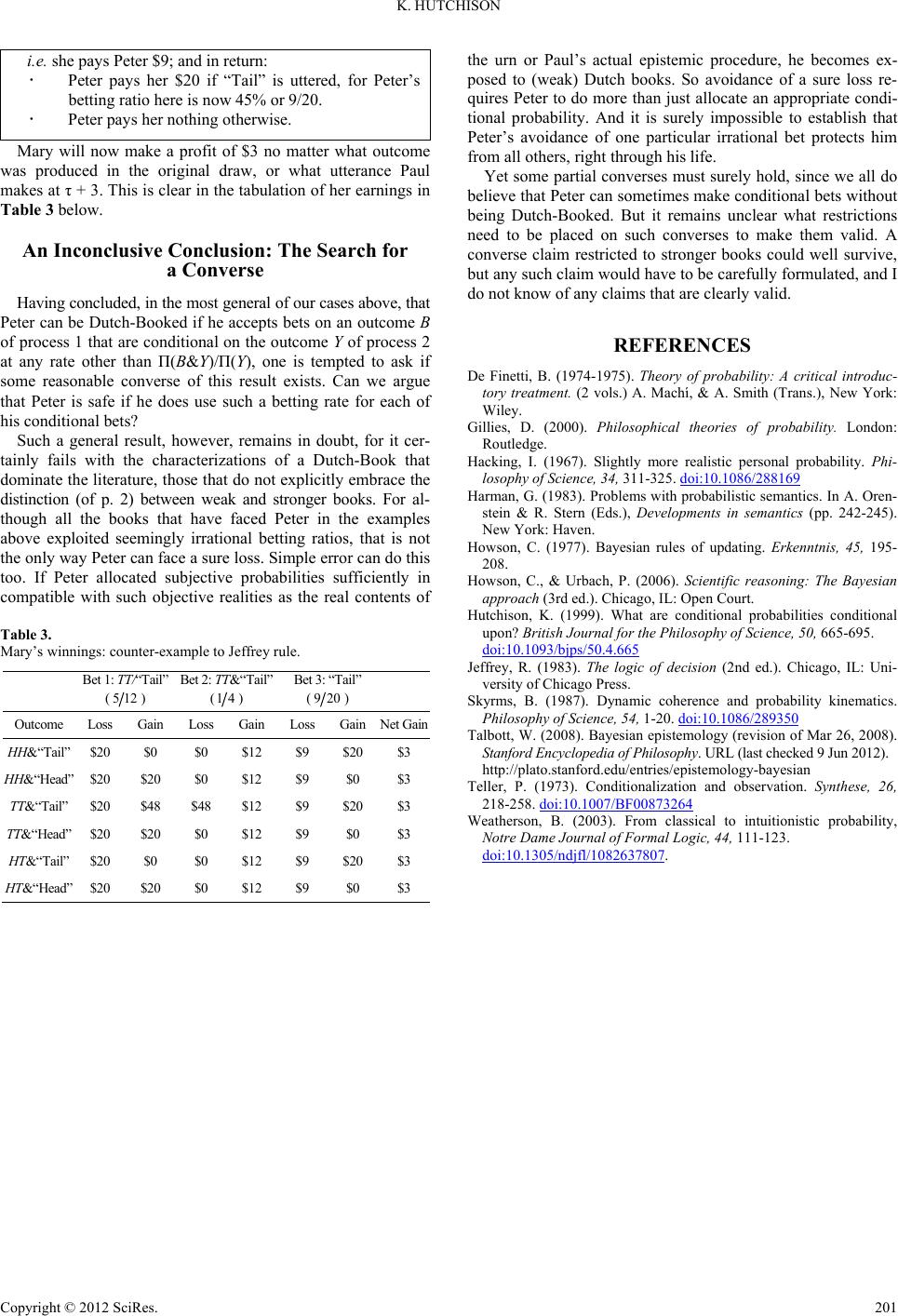

K. HUTCHISON

being ascertained and its being true3, we will observe that such

ontic bets are distinct from “epistemic” ones—which proceed if

and only if the outcome Y has been detected. Epistemic condi-

tional bets are far more realistic than the ontic ones, for ordi-

nary gamblers cannot be expected to settle a bet if its precondi-

tion is not known to be true—even if it is in fact true. They are,

too, the sort of bets that specially interest Bayesians, for the

core of Bayesianism is analysis of the effects of new informa-

tion. In many artificial situations of course (especially those

typical of the text-book, casino, or appeals to god), the truth or

falsity of the applicable condition is always ascertained, so the

distinction between the two classes of bet fades. But this is not

generally true.

There is a presumption throughout the literature that the ar-

gument which preserves a gambler from being Dutch-Booked

via ontic conditional bets, covers the epistemic ones as well4. But

that is definitely not true. Demonstrating this fact is the central

task undertaken in the present essay—which thus supplements an

earlier piece of mine (Hutchison, 1999), that demonstrated the

inadequacy of conditional probability as a procedure for updat-

ing probabilities in the light of supplementary evidence.

The core of the present argument is the simple counter-ex-

ample set out with pedantic care below. It quickly shows that

various Dutch-Books (of the irrational kind) can be set up

against Peter, if Peter adopts the strategy of betting on an out-

come X at the rate p(X&Y)/p(Y) when bets are settled if and

only if the outcome Y is detected. Peter, indeed, will not be able

to rely on a calculation that (like the traditional formula) uses

only the probabilities he attributes to the outcomes of the

chance-process under observation. For protection against Dutch-

Books, he needs to supplement these probabilities with some-

thing else: those associated with the gamblers’ finding out that

the outcome was Y.

To establish the alternative calculation that Peter needs to use,

our discussion (following the initial presentation of the main

counter-example) becomes distinctly more complicated, but

only superficially so, in that we have to juggle a multiplicity of

probabilities. We then extend this key result even further, show-

ing that our alternative formula applies when bets are made con-

ditional upon the receipt of evidence for Y, and that evidence falls

short of providing knowledge that the outcome Y has been

achieved. This situation is sometimes supposed to be covered

by Jeffrey’s extended rule of conditioning (see n. 9), but we

show that this rule advises Peter to use rather different betting

ratios, and that these do not suffice to exclude a Dutch-Book.

As befits the fact that I am arguing against a received claim,

my focus will be almost exclusively on the “synchronic” books

used in the literature that I target, those in which all bets are

placed at the one time. Diachronic books (i.e. those composed

of bets placed at different times) generate dramatic complica-

tions for the Dutch-Book approach—see e.g. n. 5—and accord-

ingly are given only passing mention below, though I have

discussed the inadequacy of conditional probability in their

context elsewhere (see Hutchison, 1999).

The Betting Scenario for the Main Example

To make the case, we consider a very simple urn model.

(Many readers will recognize this to be an adaption of Ber-

trand’s box paradox, but that fact is not important to following

the analysis below). We will be supposing that (at some time

we shall call τ) an honest (etc.) coordinator Paul places three

unbiased coins in an urn: one normal coin (with a head and a

tail face); one with two head faces; and one with two tail faces.

Later, at time τ + 1, Paul randomly selects one of these coins

from the urn, and Peter and Mary bet against each other on

(inter alia) the various outcomes of this draw. These bets can be

simple; or conditional upon information released by Paul.

3As evidenced by the citations in n. 4 below, there is remarkable little atten-

tion to this distinction in the probability literature. It is, fleetingly, recog-

nised as being a problem in the subjective interpretation, but seemingly

tolerated. Hacking, 1967: pp. 316, 324 treats it as a “trifling idealization”

typical of those made in philosophical analysis; while Weatherson, 2003

and Harman, 1983 note that the blurring creates an affinity with intuitionist

logic, without however observing the dramatically disruptive consequences

within more standard logics. Howson & Urbach, 2006: p. 54 avoid the issue

y presuming (in one particularly sensitive context) that bets are settled by

an “omniscient oracle”.

4Because the literature on probability is reluctant to distinguish the two

types of bets (and more generally, to accommodate the distinction

between truth and ascertainment), we know of no overt declaration that

the one argument covers both cases. But it is routine to find an

equivocation in the interpretation of the result at issue in the context o

discussions of the Dutch-Book defence of conditionalization. See, e.g.:

De Finetti, 1974-1975, v.1: p. 135 (“if H does not turn out to be true”;

“if I know H is true”; brief cryptic reference to Dutch-Book); Gillies,

2000: pp. 36-37 (where conditional probabilities are introduced as i

they refer to what is ascertained) and p. 62 (where the Ramsey-De

Finetti theorem is stated in terms of truth—with bets being called off i

a condition “does not occur”—then defended via a Dutch-Book argu-

ment); Talbott, 2008: p. 2 (where conditionalization is characterised

epistemically) and p. 3 (where the Dutch-Book argument is phrased in

terms of a bet called off if a condition is not true); Howson, 1977: p. 63

(middle paragraph, where the conclusion of the Dutch-Book argument

is summed up in terms of both truth and verification); Teller, 1973: p.

220 (where the problem is phrased in terms of ascertainment), p. 222

(where the reference class singled out by ascertainment is identified

with that provided by truth), p. 224 (where the circumstances in which

bets are called off is characterised via truth); Skyrms, 1987: p. 2

(where the problem is phrased in terms of ascertainment), p. 3 (where

the circumstances in which bets are called off is characterised via

truth

.

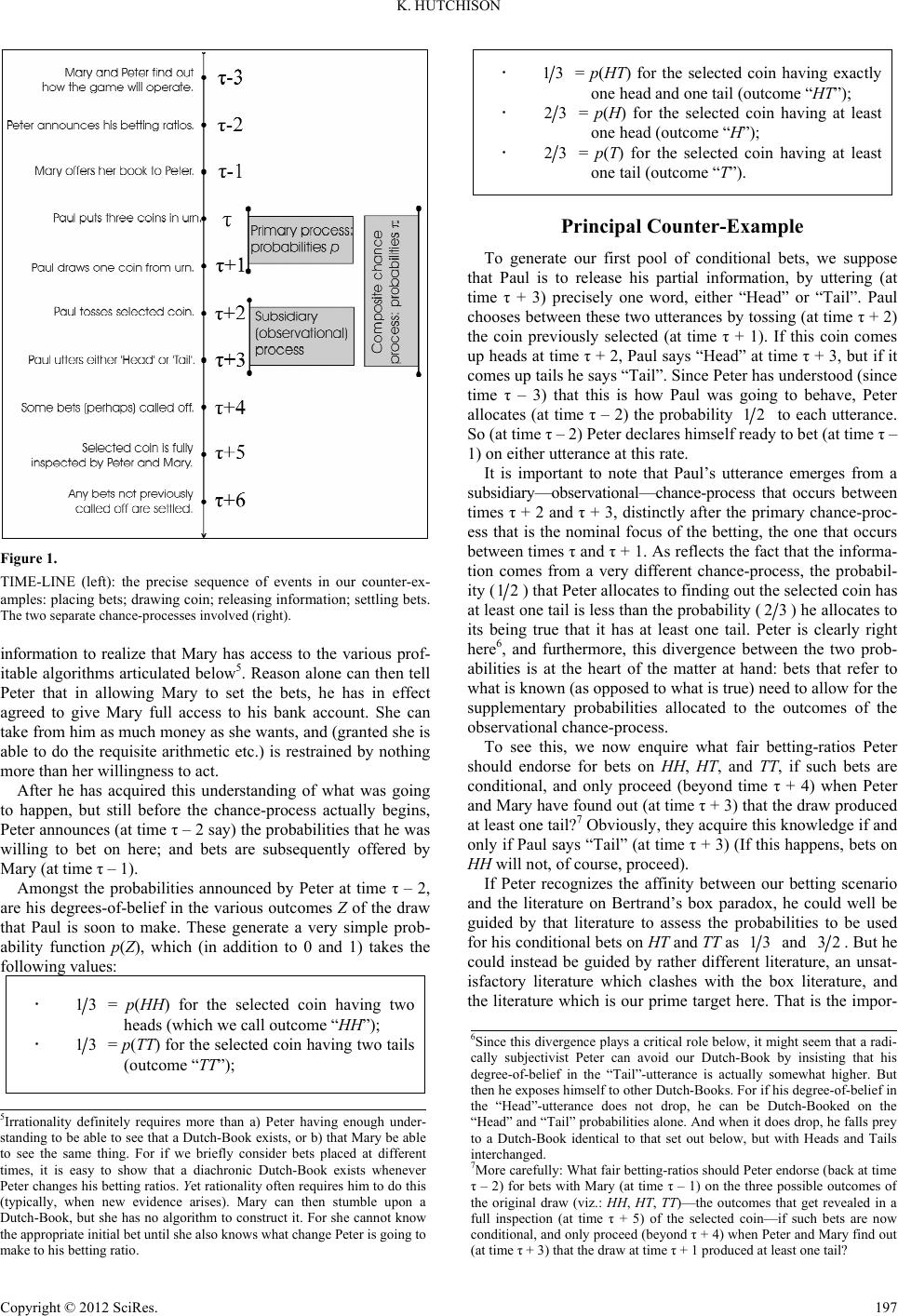

For after he makes the draw, Paul is to release information to

Paul and Mary, via a two-stage process (summarized in the

time-line depicted below). The second stage is rather trite and

takes place at time τ + 5, when Paul reveals full details of the

selected coin, so that bets can be settled (at τ + 6). The first stage

is far more significant here, for this takes place earlier (at time τ +

3), when Paul provides the partial information about the draw

that allows epistemic conditional betting. Paul inspects the coin

that has been drawn, and reveals something about it via proce-

dures specified in the individual examples below.

We suppose that Peter and Mary have both understood all

Paul’s proposed actions since well before they were actually

carried out, and that each of them also understands that the other

possesses the same comprehension of the processes. So all that

they later discover is the results of those activities. To avoid all

irrelevant confusion about the temporal sequence of events, we

suppose that this understanding of the process was in place at

time τ – 3, and we shall be irritatingly careful to stress the tim-

ings of all later activity (as summarized in our time-line, Figure

1). In the end, these timings are not very important, but it is vital

that there be no room for confusion about them.

It may not be important here that Mary know that Peter shares

her understanding of the betting process, but Peter’s realization

that Mary understands what is going on does seem vital to the

logic—because this, in the end, is what makes the Dutch-Books

below evidence of Peter’s irrationality in agreeing to bet on stan-

dard conditional probabilities. For it means that Peter has enough

Copyright © 2012 SciRes.

196