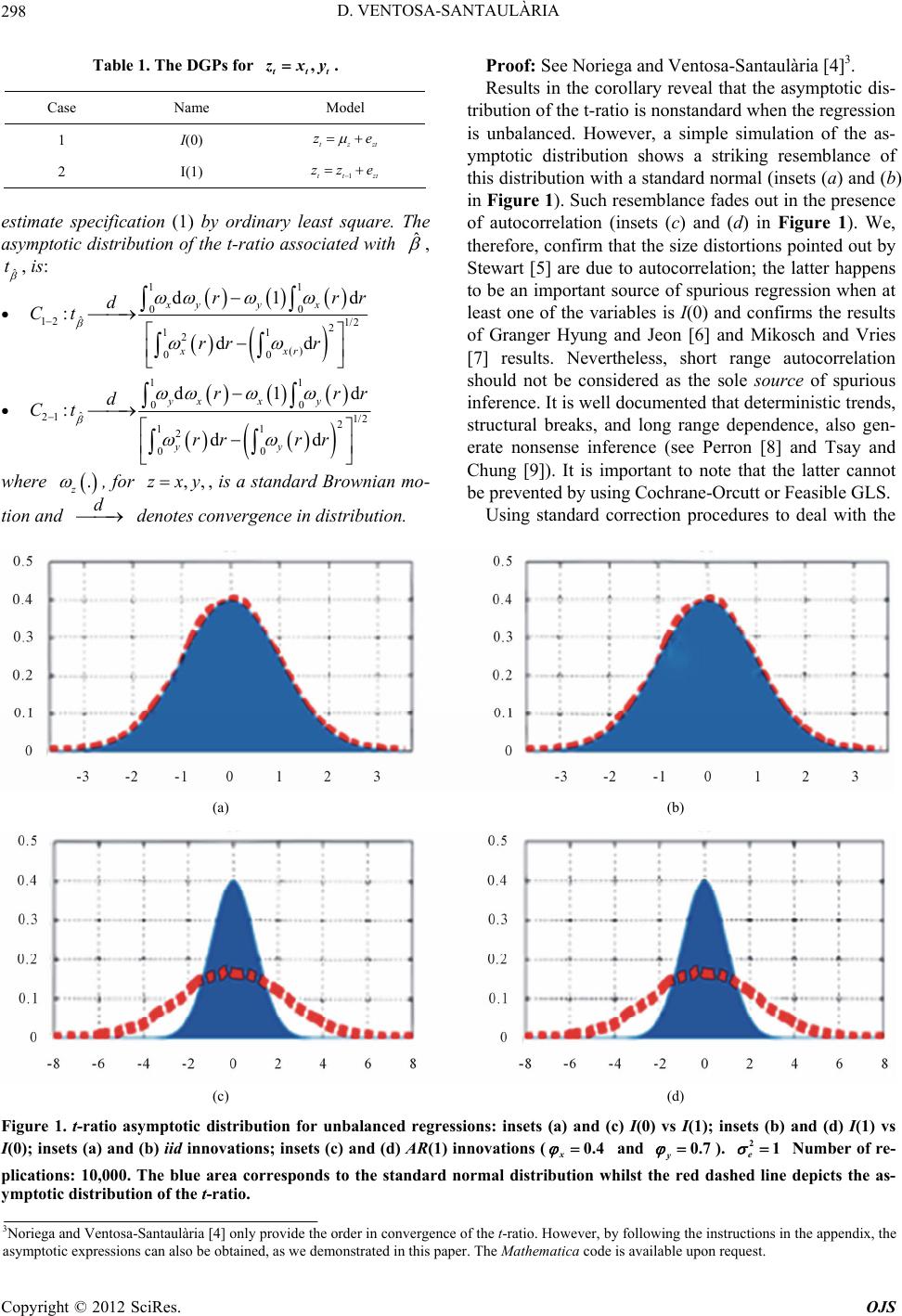

D. VENTOSA-SANTAULÀRIA 299

spurious regression phenomenon is tempting, even if such

procedures cannot always provide correct inference (see

Stewart [5] and McCallum [10], for example). Sun [11]

proposed a convergent t-statistic using modified HAC

errors with a bandwidth proportional to the sample size

when the variables are highly persistent. The author ac-

knowledges, however, that such a procedure cannot be

used in empirical applications, since the limit distribution

of the test depends on the memory parameter under the

null hypothesis and critical values cannot, therefore, be

tabulated. McCallum [10] and Kolev [12] also advocate

classical correction procedures to deal with spurious re-

gressions, such as the Cochrane-Orcutt procedure and

Feasible Generalized Least Squares. They argue that us-

ing them reduces size distortions of the t-test. However,

Martínez-Rivera and Ventosa-Santaulària [13] proved that

such methods are not always effective and remain highly

dependent on the DGP of the series4.

2. Concluding Remarks

There is finite-sample evidence showing that spurious

inference in unbalanced regressions mostly occurs when

the innovations of the DGPs are not iid. In that sense,

standard autocorrelation-correction procedures, such as

HAC errors, Feasible GLS and Cochrane-Orcutt esti-

mates, have been advanced to eliminate/reduce the size

distortions and, thus, spurious inference. This approach

should, nevertheless, be reconsidered. First, there is evi-

dence that spurious regression using stationary series

cannot always be interpreted as a short range autocorre-

lation phenomenon: long range dependence and struc-

tural breaks (level shifts, for example) also cause spuri-

ous inference; spurious regression cannot, therefore, be

always corrected using classical procedures. Second, an

unbalanced regression (in which the order of integrations

of the involved series is not the same) is an empirical

situation which remains to be proved relevant. The esti-

mation of an unbalanced regression is not intuitive, al-

though there are cases such as in the predictive equation

in the finance literature, in which the market returns

(usually, found to be stationary) is regressed against

dividend yield (stationary but highly persistent). Spurious

regression cannot be simply considered as a short-mem-

ory autocorrelation phenomenon and cannot, therefore,

be treated using standard procedures. The main conclu-

sion is, therefore, twofold: 1) practitioners should inter-

pret cautiously their results whenever they find evidence

of autocorrelation, since the inference could be spurious;

2) they should, however, be aware that spurious regres-

sions arise for many diverse reasons, autocorrelation be-

ing only one of them; standard autocorrelation correction

procedures are not to be considered as the sole solution

to prevent spurious inference; on the contrary: parameter

stability, long memory and cointegration tests should

always be also considered.

REFERENCES

[1] C. W. J. Granger and P. Newbold, “Spurious Regressions

in Econometrics,” Journal of Econometrics, Vol. 2 No. 2,

1974, pp. 111-120. doi:10.1016/0304-4076(74)90034-7

[2] P. C. B. Phillips, “Understanding Spurious Regressions in

Econometrics,” Journal of Econometrics, Vol. 33, No. 3,

1986, pp. 311-340. doi:10.1016/0304-4076(86)90001-1

[3] D. Ventosa-Santaulària, “Spurious Regression,” Journal

of Probability and Statistics, Vol. 2009, No. 1, 2009, pp.

155-182. doi:10.1155/2009/802975

[4] A. E. Noriega and D. Ventosa-Santaulària, “Spurious Re-

gression and Trending Variables,” Oxford Bulletin of

Economics and Statistics, Vol. 69, No. 3, 2007, pp. 439-

444. doi:10.1111/j.1468-0084.2007.00481.x

[5] C. Stewart, “A Note on Spurious Significance in Regres-

sions Involving I(0) and I(1) Variables,” Empirical Eco-

nomics, Vol. 41, No. 3, 2011, pp. 565-571.

doi:10.1007/s00181-010-0404-5

[6] C. W. J. Granger IV, N. Hyung and Y. Jeon, “Spurious

Regressions with Stationary Series,” Applied Economics,

Vol. 33, No. 7, 2001, pp. 899-904.

[7] T. Mikosch and C. G. Vries, “Tail Probabilities for Re-

gression Estimators,” Tinbergen Institute Discussion Pa-

pers, TI 2006-085/2, 2006.

[8] P. Perron, “The Great Crash, the Oil Price Shock, and the

Unit Root Hypothesis,” Econometrica, Vol. 57, No. 6,

1989, pp. 1631-1401. doi:10.2307/1913712

[9] W. J. Tsay and C. F. Chung, “The Spurious Regression of

Fractionally Integrated Processes,” Journal of Economet-

rics, Vol. 96, No. 1, 2000, pp. 155-182.

doi:10.1016/S0304-4076(99)00056-1

[10] B. T. McCallum, “Is the Spurious Regression Problem

Spurious?” Economics Letters, Vol. 107, No. 3, 2010, pp.

321-323. doi:10.1016/j.econlet.2010.02.004

[11] Y. Sun, “A Convergent T-Statistic in Spurious Regres-

sions,” Econometric Theory, Vol. 20, No. 5, 2004, pp.

943-962. doi:10.1017/S0266466604205072

[12] G. I. Kolev, “The ‘Spurious Regression Problem’ in the

Classical Regression Model Framework,” Economics

Bulletin, Vol. 31, No. 1, 2011, pp. 925-937.

4There are other approaches worth mentioning. In Davidson and Mac-

Kinnon [14], for example, the authors consider that the spurious re-

gression phenomenon is, at least partially due to a misspecification o

the model. The authors argue that instead of Equation (1), practitioners

should estimate yt = α + βxt + γyt-1 + μy. Using this specification makes

the null hypothesis of the t-test valid. Simulations presented in David-

son and MacKinnon [14] reveal, however, that even a correct specifi-

cation is unable to provide an adequate size of the t-test under the null

hypothesis when the variables are nonstationary.

[13] B. Martínez-Rivera and D. Ventosa-Santaulària, “A Com-

ment on ‘Is the Spurious Regression Problem Spurious?’”

Economics Letters, Vol. 115, No. 2, 2012, pp. 229-231.

[14] D. Davidson and J. G. MacKinnon, “Econometric Theory

and Methods,” Oxford University Press, New York, 2004.

Copyright © 2012 SciRes. OJS