The Method of Real Options to Encourage the R & D Team239

5.2 Real Option Incentive Program

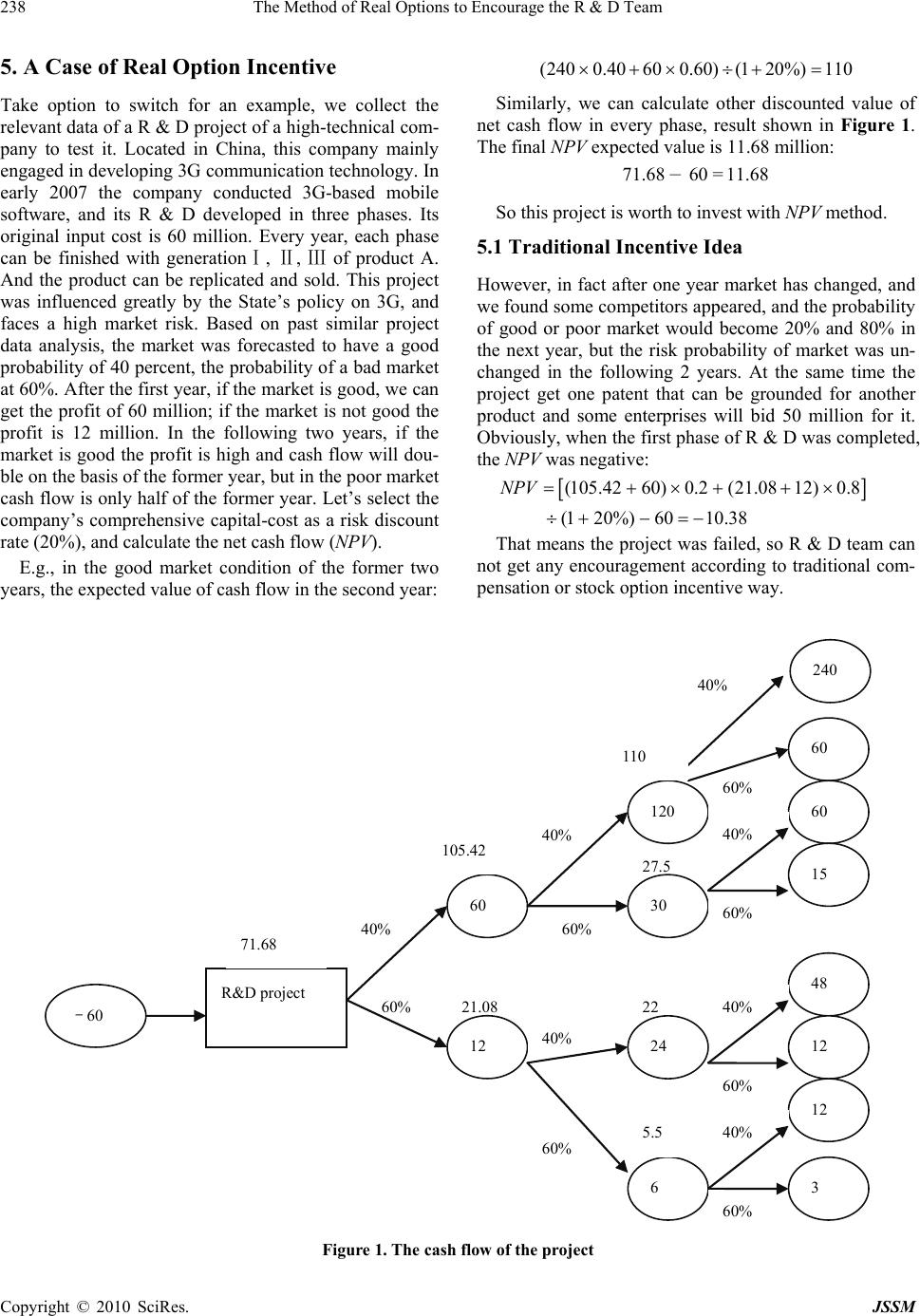

Now if we consider real option, the evaluation to the

project is entirely different. When R & D in the first

phase was completed, cash flow was only 33.08 million

in the poor market (that is, cash flow expected value after

one year in poor market: ), if we

switched to another product at this time, the value of the

previous R & D was 50 million. Obviously, such a con-

version opportunity is valuable. Actually it is option to

switch: the agreed price is 50 million, maturity period is

1 year, the current price of the subject is 49.62 million

(hat is, expected value of current cash flow, [(

21.08+12=33.08

105.42 60)

), maybe

rise to 165.42 million (that is, expected value of cash flow

after one year in good market: 105 )

or drop to 33.08 million due to date (that is, expected

value of cash flow after one year in poor market:

). We can use

0.221.08 120.8] ()

21.08+12=33.08

(1 20%)49.62

.42 + 60 =165.42

binomial tree model

[16] and set up the probability of price raise is “P”. With

the hypothesis of symmetric information and risk-neutral,

we can get the value of this real option at risk-free inter-

est rate of 3.87%, which is bank interest rate for

one-year.

0.0387

165.4233.08(1) 49.62PPe

0.1398P

That is to say, the probability of the call option is

13.98% of which value is 55.8 million (165.42 50

). And the probability equals 1 - P when the

value of the call option is zero, that is 86.02%.

115.42

Expected cash flow of the option to switch is:

115.42 13.98%086.02%16.13

Discount at the risk rate of 20%, get current value of

option to switch:

16.13 / (120%)13.44

Therefore, project team will be able to share a part of

this value as an incentive with real option incentive ap-

proach when finished the first phase. The firm can de-

termine the proportion αi as 10% based on strategic ob-

jective and current industry competition. So, R & D team

may get 1.344 million as a reward. It is reasonable for the

both because this project can build foundation for an-

other product’s R & D and contribute to the company’s

development. Considering that being start-up period and

need more liquidity for more follow-up R & D projects,

the company decided not to use bonus but share the value

of latter project in the future.

5.3 Comparative Analysis about Advantage of

Real Option

The high-risk project is common for any firm. Real op-

tion incentive put forwarded in this paper is one of ways

to solve how to encourage R & D team in such project,

which advantages include: 1) to avoid short-term goal-

oriented, companies can determine benchmarks of team

incentive based on the follow-up value of high-risk pro-

ject; 2) To design more flexible incentive methods,

companies can use different types of real option or de-

sign different exercise methods; 3) If we combine real

option incentive with other motivation methods, the ef-

fect will be more targeted-oriented and more comprehen-

sive.

6. Conclusions

This article discusses the method of real options to en-

courage R & D team when the enterprises can not

achieve the desired economic benefit in the case of

high-risk project or the immature market. The steps of

method include: identify the real option type of high-risk

projects, design the incentive mechanism and design

specific exercise ways. In fact, real option presented in

this paper can be applied not only to high-risk project,

but also to other technical project. In addition, some

non-material incentives, such as honor or job promotion,

will bring more opportunities for R & D team, which

itself can be regarded as one of real options. How to

quantify the value of these non-material incentives ap-

proach and combine with other materials will be our next

research direction and focus.

REFERENCES

[1] F. Hu, “Incentive Compensation Study on R & D Team,”

South China Normal University, Guangzhou, 2004.

[2] T. J. Englander, “Casey at the Bank,” Incentive, Vol. 167,

No. 2, 1993, p. 20.

[3] R. J. Doyle, “Caution: Self-Directed Work Teams,” Hu-

man Resource Magazine, Vol. 37, No. 6, 1992, pp.

153-155.

[4] B. Geber, “The Bugaboo of Team Pay,” Training, Vol. 32,

No. 8, 1995, pp. 25-34.

[5] J. R. Hoffman and S. G. Rogelberg, “A Guide to Team

Incentive Systems,” Team Performance Management, Vol.

4, No. 1, 1998, pp. 23-32.

[6] S. Y. Chen, X. W. Tang, D. B. Ni et al., “Value Analysis

on Non Material Incentive in Combination Incentive to

Managers,” Chinese Journal of Management Science, Vol.

13, No. 1, 2005, pp.122-126.

[7] W. J. Zhang and J. F. Li, “Motivation System in Chinese

Knowledge-Enterprises,” Science Research Management,

V

ol. 22, No. 6, 2001, pp. 90-96.

[8] X. Li and G. S. Zhang, “The Effect of Stock Option In-

centive for Manager from the Team Theory,” Business

Ti m e s , Beijing, 2007.

[9] L. Yin, Z. Y. Zhao et al., “The Theory and Practice of

Stock and Option Incentive for High-tech Enterprise,”

Copyright © 2010 SciRes. JSSM