American Journal of Industrial and Business Management

Vol.07 No.06(2017), Article ID:76862,19 pages

10.4236/ajibm.2017.76053

Examining Factors Influencing E-Banking Adoption: Evidence from Bank Customers in Zambia

Bruce Mwiya, Felix Chikumbi, Chanda Shikaputo, Edna Kabala, Bernadette Kaulung’ombe, Beenzu Siachinji

School of Business, Copperbelt University, Kitwe, Zambia

Copyright © 2017 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/

Received: April 26, 2017; Accepted: June 11, 2017; Published: June 14, 2017

ABSTRACT

This paper contributes to the electronic banking (e-banking) literature by applying the modified Technology Acceptance Model (TAM) in an under-re- searched Zambian context. Specifically, it examines the influence of e-banking technology’s perceived usefulness, perceived ease of use and trust (safety and credibility) on e-banking adoption. Based on a quantitative correlational design, primary sample data were collected from 222 bank customers from two of Zambia’s largest cities. The findings indicate that the modified TAM model is applicable in the Zambian context and that perceived usefulness, ease of use and trust each significantly positively influences attitude to e-banking. In turn attitudes to e-banking influence intention and actual adoption of e-banking services. For scholars, practitioners and policy makers, the study shows that improving perceptions of trust (safety, security and credibility), usefulness and ease of use of e-banking systems would result in increased adoption. This paper is the first to extend the modified TAM model into the under-re- searched developing country context of e-banking in Zambia.

Keywords:

E-Banking, Adoption, Intention, Attitudes, Modified TAM

1. Introduction

The global economy has experienced tremendous transformation over the last three decades, to a certain extent galvanised by developments in information and communication technology (ICT). For example, retailing is being disrupted tremendously because out of 23,000 shoppers surveyed in 25 countries in Europe, USA, Asia and Africa, 54% of shoppers are not only buying products online on a weekly or monthly basis but they are also willing to buy off shore if the price is better [1] . This is part of electronic commerce developments facilitated by the internet-based capabilities of firms. ICT innovations have become the de-facto drivers of key sectors of the economies in developing and developed nations. This has also resulted in the interconnectedness and interdependence of countries on one another across the globe. The financial sector, more particularly the banking sector, is one key economic sector that has embraced the ICT diversifications. The current paper focuses on exploring factors influencing electronic banking (e-banking) adoption as evidenced from retail bank customers in Zambia.

Banks are important in every country because of their crucial role in supporting economic development through efficient financial services [2] . A bank is necessary for trade and industry. A bank is a financial institution that deals with deposits, advances, loans, payment and other related financial services. It receives money from those who want to save (savings-surplus units) in the form of deposits and lends money to those who need it i.e. savings-deficit units [3] . E-banking comprises the systems that enable financial institutions, customers, individuals or businesses, to access accounts, transact business, or obtain information on financial products and services through a public or private electronic network, including the internet [4] . E-banking services would include electronic funds transfers, automated teller machines (ATMs), point of sale machines (POS) in shops and mobile banking and money. In addition, e-banking services would include e-mails and e-statements from banks sent through secure lines, texts, phone calls, transaction alerts etc. [5] .

The banked population in Zambia has not fully embraced technology [5] as an alternative cheap form of banking [6] . This is so because of two major challenges: Firstly, Zambia is still growing its internet infrastructure and accessibility; only 20.4% of the population has access to internet, way below the 28.7% average for Africa and 54.2% average globally [7] . It could be argued that e-banking can only be embraced well with clear laws regulating it and a developed secure telecommunication network. Secondly, the FinScope surveys show a slight increase from 13.9% to 24.8% of adults that were formally banked between 2009 and 2015. One reason for the low level of financial inclusion is the high cost of providing financial services [8] . E-banking offers an opportunity to increase the proportion of the population that accesses formal banking services as it does not require every individual customer to physically enter the banking hall for most bank services. Therefore, it should be of great concern to policy makers, practitioners and scholars that e-banking has not been fully embraced in Zambia.

Banks that want to offer their services electronically must first ensure that all necessary infrastructure, workforce, and banking functions are in place and working at maximum efficiency [9] . This is important because the successful implementation of information systems is dependent on the extent to which such a system is used and eventually adapted by the potential users [10] . Therefore, there is a need for banks to assess their readiness to offer e-banking services to their clients [11] . It is important to understand the factors influencing customers to use bank services and how they can be attracted to use both the online and offline services.

Based on the theory of planned behaviour i.e. TPB [12] and the technology acceptance model i.e. TAM [13] , studies have been conducted in many parts of the world to explore and determine factors influencing the adoption of e-banking amongst bank customers. For example, in UK [14] , Lebanon [15] , India [16] and Saudi Arabia [17] , scholars establish that perceptions of usefulness, ease of use, trust, self-efficacy in using the systems and social norms positively influence the attitude and intentions to adopt e-banking services. However, in many developing countries, these models have not been tested, thus limiting generalisability of prior research conclusions because of context differences in terms of culture, level of education, access to internet and banking services [18] (p. 314). In Zambia, for example, with the exception of one study [5] which used time series data to assess aggregate trends in ATM, electronic funds transfer and mobile money transactions, there has not been a study exploring factors influencing the adoption of e-banking services. This study seeks to fill this contextual knowledge gap.

Therefore, the study seeks to contribute to the e-banking adoption literature by applying the modified Technology Acceptance Model (TAM) model in the under-researched developing country context of Zambia. Specifically, the study examines the influence of perceptions of usefulness, ease of use and trust (security and safety) not only on attitudes but also on intention to adopt e-banking services among Zambian bank customers. The rest of the paper is structured as follows: the next section reviews literature and develops hypotheses before research methods are highlighted. Thereafter, results are reported and discussed in relation to both the conceptual model and prior empirical studies.

2. Literature Review and Hypotheses Development

2.1. E-banking and Adoption Models

E-Banking

In traditional banking practice, customers accessed banking products and services through daily physical contact with bank tellers. This approach to delivering banking services created a mismatch between customer demands and bank capabilities because customers could only access financial services at specific locations and during a bank’s working hours. With the advent of technological innovations, banks can now deliver their products and services to clients from anywhere and at any time through diverse communication media such as the internet, mobile networks, ATM networks, etc. These innovative methods of delivering bank products and services using electronic communication channels are known as e-banking.

Rather than exchanging actual cash, cheques, or other negotiable instruments [19] , the term e-banking is a broad concept that describes the provision and delivery of banking products, services, and solutions through electronic channels [20] . The Basel committee report defines e-banking as the provision of retail and small value banking products and services through electronic channels as well as large value payments and other wholesale banking services delivered electronically [17] .

E-banking services began in developed countries; they initially encompassed only Automated Teller Machines (ATM) in the early 1980s. In the 1990s, the banking sector began to perform some of their e-banking transactions through the telephone. In 1995 internet banking services were introduced in the United States of America i.e. USA [4] . Banking has, for a long time, relied on information technology (IT) to acquire, process, and deliver its services to all relevant users. It is not only critical in the processing of information, it also provides a way for the banks to differentiate their products and services, as well as provide convenient, reliable, and expedient services [21] . As a result, banks have tended to invest more in technology and information to achieve maximum return by efficiently attracting and serving a large number of clients [22] .

The concept of e-banking and the various forms it takes continue to evolve with technological innovations. In the early stages, e-banking took the form of only ATMs. Forms of e-banking now include ATMs, Point-of-sale Transfer Terminals (POS) using debit and credit cards, online/Internet banking, and mobile banking [21] [23] . E-banking also can be categorized on the basis of the instruments used: telephone connection, personal computers, means of payment [bank cards] and self-service zones [22] . Overall, in terms of the stages of e-banking capabilities development, literature seems to indicate that established banks in developed countries began with ATMs and evolved through Personal Computer-banking, Telephone-banking, Internet-banking, TV-banking, and now Mobile-banking. Having understood the breadth of e-banking and the development stages, it is necessary to consider factors influencing its adoption by bank customers.

E-Banking Adoption Models

Over the past two decades, researchers in ICT have proposed many theories and models to explain and predict technology adoption but the prominent models include the Theory of Reasoned Action (TRA), Theory of Planned Behaviour (TPB) and the Technology Acceptance Model i.e. TAM [14] .

Theory of Reasoned Action (TRA) and Theory of Planned Behaviour (TPB)

The TRA emanates from social psychology and it identifies the determinants of consciously intentional behaviour [24] . It assumes that individuals are rational and are constantly evaluating relevant behavioural beliefs in the processes of forming their attitude toward the behaviour. The theory is based on three constructs namely behavioural intention, attitude and subjective norms. Attitude is the sum of beliefs about a particular behaviour when favourably or unfavourably evaluating that particular behaviour; “is it a good thing for me to do?” [24] . Subjective norms would be the influence of people in one’s social environment on his/her behavioural intentions; “would people important to me approve this behaviour?”. Usually this refers to the beliefs of people, weighted by the importance one attributes to each of their opinions that will influence one’s behaviour.

Reference [24] defines behavioural intention as a function of both attitudes and subjective norms toward that behaviour. It is this intention that has been found to predict actual behaviour. In relation to e-banking, TRA would suggest that intention to adopt or reject e-banking would be determined by subjective norms and personal attitude toward the e-banking. To help improve the prediction of behavioural intention, the TPB was proposed by adding the concept of Perceived Behavioural Control (PBC) to the constructs of attitudes and subjective norms. Reference [25] defines perceived behavioural control as an individual’s perception of the ease or difficulty of performing the behaviour of interest in light of possible barriers; “if I wanted to do it, could I do it?”. Empirically, the TRA and the TPB have been used widely to examine individual’s acceptance and use of different technologies [26] including e-banking in UK [14] , Jordan [27] , Taiwan [28] and Hong Kong [29] . On the Zambian context, no study was found in the literature on e-banking adoption based on the TRA and TPB, this limits generalisability of prior research conclusions.

Technology Acceptance Model (TAM)

The TAM was proposed by Fred Davis [13] . The theory was adapted from the Theory of Reasoned Action (TRA). This model is the most widely used for exploring user acceptance of a technology. According to this model, the use of an information system depends on perceived usefulness and perceived ease of use. Favourable or unfavourable attitudes toward any technology are a function of perceived ease of use and perceived usefulness about the technology. The first belief, perceived usefulness (PU), is the user’s “subjective probability that using a specific application system will increase his or her job performance” [13] (p. 985). Initially defined in the context of one’s job performance, PU was later used for any common task in organisational or non-organisational settings [30] .

The second belief, perceived ease of use (PEU), is “the degree to which the user expects the target system to be free of efforts” [13] (p. 985). PU is also influenced by PEU. As is the case for the TRA and TPB, the strength of such beliefs, attitudes and intention in predicting actual behaviour largely depends on the degree of measurement specificity attained [31] . In order to apply these notions to the technology acceptance context, it is necessary to measure beliefs regarding the use of technology, rather than the technology itself. Empirically, the TAM model has been used widely to examine individuals’ acceptance and use of different technologies [32] including e-banking in UK [14] , Malaysia [33] , Iran [34] and Jordan [17] . However, there are no studies in the Zambian context based on the TAM model, this limits generalisability of prior research conclusions.

2.2. Conceptual Framework and Hypotheses

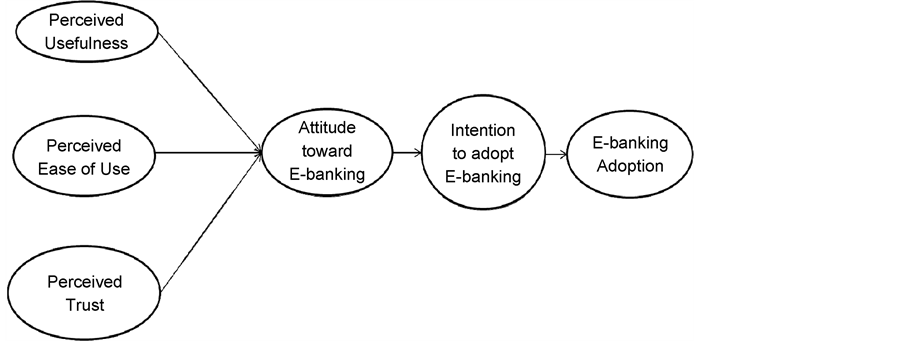

Recent studies [26] [32] have compared the dominant models, namely TRA, TPB and TAM, for examining E-banking adoption. Based on empirical data in UK, Yousafzai and colleagues [14] conclude that the TAM model is superior to the other models in predicting intention and actual adoption. However, based on their findings, they highlight the importance of trust (i.e. perceptions of credibility, security and safety) in adoption. Therefore, they recommend that trust should be included in exploring e-banking end user behaviour. In the TAM model, as earlier indicated, technology adoption primarily originates from perceived usefulness and perceived ease of use by the end user. These in turn determine attitude toward usage. Attitude toward usage positively influences intention to use, a reflection of user loyalty. Empirically, dimensions of the TAM model were found to be reliable and valid for assessing online banking adoption [34] [35] . This research has adapted the TAM model and therefore employs perceived usefulness, perceived ease of use and perceived trust as independent variables to determine attitude (see Figure 1). It is the attitude that engenders intention. In turn intentionality determines actual e-banking adoption.

Perceived Ease of Use and Attitude toward E-banking

Perceived ease of use (PEU) refers to the degree to which a person believes that using the relevant technology would require minimal effort or better still effort free [13] (p. 320). Perceived ease of use does not determine whether one will use a new information system or not, but will rather create an attitude towards using it. If an information system has high user-friendliness it will have a positive impact on the user and create a positive attitude towards using the new technology [13] . Empirically, prior studies [36] [37] indicate that perceived ease of use is a significant antecedent of positive attitude toward e-banking and customer satisfaction. Therefore, the first hypothesis is as follows:

H1: Perceived ease of use positively influences attitude towards e-banking.

Perceived Usefulness and Attitude toward E-banking

According to [13] , perceived usefulness in relation to technology use refers to consumers’ perceptions regarding the outcome of the experience. If the outcome were beneficial or useful then the user would have a positive attitude toward the use of that technology. Similarly, other scholars define perceived usefulness as the extent to which a person deems a particular system to boost his or her job performance [38] . For e-banking technology, perceived usefulness considers whether customers find it cheaper, convenient, flexible and efficient. This also

Figure 1. E-banking adoption conceptual model.

means that if customers find user-friendly self-service technologies give them greater autonomy in performing banking transactions, in obtaining information on financial advices, and in purchasing other financial products, they are more likely to have a positive attitude toward such technologies. Empirically, scholars suggest that customers who find e-banking to be useful are more likely to have a positive attitude toward e-banking use [34] [35] . Based on these perspectives, the study posits as follows:

H2: Perceived usefulness of e-banking positively influences attitude towards e-banking.

Trust and Attitude toward E-banking

Trust is defined as the reliance on and the confidence in the integrity, strength, ability, surety of a person, a system or thing [39] [40] . In relation to e-banking and e-commerce, trust has four elements, namely security, integrity, authentication and authorization [14] . Security refers to the protection of information exchanged during electronic transactions from the threats and risks of transactional integrity, authentication, and authorisation. Transactional integrity is the belief that the information will not be generated, intercepted, changed, or removed illegally. Authentication belief assures customers that only genuine transactions will be accepted. Finally, authorisation belief establishes that the parties to an electronic transaction are who they claim to be. No one wants to be swindled out of his or her money. No wonder scholars suggest that trust is an essential consideration for users in the acceptance or rejection of e-banking or e-commerce technology [39] . This is because it may positively affects the attitudes of customers and their satisfaction with finance related technology [40] . Based on these considerations, the study postulates as follows:

H3: Trust positively influences attitude towards e-banking adoption.

Attitude’s influence on Intention

Attitudes may be positive, negative, or neutral [41] . This is because attitudes are evaluative statements or judgments, either favourable or unfavourable concerning objects, people or events. Attitude has a relationship with e-banking adoption [34] . Attitude toward an innovation is a critical intervening variable in the innovation adoption decision [13] . Intention to use is affected by the user’s attitude towards using the information system. Thus, attitude toward a specific information technology is conceptualised as a potential user’s assessment of the desirability of intending to use that technology [13] . If the attitudes of potential users are favourable (positive) there will be higher intentions to adopt and if the attitudes are unfavourable (negative), intentions to adopt will be lower. Empirically scholars submit that the higher the level of favourable attitude, the higher the intention to adopt e-banking [36] [42] . Therefore, the following hypothesis is suggested:

H4: Attitude towards e-banking positively influences intention to adopt e-banking.

Intention and Actual Behaviour

Reference [13] defines behavioural intention as “the degree to which a person has formulated conscious plans to perform or not to perform some specified future behaviour”. Intention is determined by a person’s favourable or unfavourable attitude toward the use of that technology and his or her perception concerning its usefulness. The higher the level of intention, the higher the likelihood that such a behaviour will be performed [12] . In relation to e-banking, based on empirically data, scholars note that individuals with higher intentions to adopt e-banking are more likely to actually use e-banking services [43] [44] . The following hypothesis is grounded on these observations:

H5: High intention towards using e-banking is positively associated with e-banking adoption.

3. Methods and Measurement

Population, Sample and Data Collection

The purpose of this study was to test the modified TAM model in an under-researched Zambian commercial banking context. Specifically, the study sought to examine the effects of perceived ease of use, usefulness and trust on the attitudes and intention to adopt e-banking among bank customers. As such the study employed a quantitative correlational design [45] [46] . Prior studies exploring determinants of e-banking adoption such those in India [37] , Iran [34] , Nigeria [43] , and the United Kingdom [14] have employed similar approaches. In line with extant literature highlighting the need for banks to use e-banking, inter alia, to widen their customer base, this study focused on retail bank customers in the two largest cities of Zambia.

Over a period of four weeks, based on the five e-banking pioneering banks, self-administered questionnaires were distributed to walk in bank customers who were willing to participate. Before each potential respondent could answer the questionnaire, the purpose of the study was explained and informed consent was signed. 330 questionnaires in all were handed out and only 250 (75.76%) were returned by respondents. However only 222 (67.27%) were properly completed. Table 1 shows the profile of the 222 usable sample. 67.1% of the respondents were male while 32.9% were female. The majority of the respondents were between the ages of 20 - 30 years, consistent with national census figures indicating that 57.14% of the working age population is below the age of 30 years [47] and that 43% of the economically active are in that age range. In relation to level of education, 80.6% of the respondents had either a university/college diploma or degree. No wonder, 87.4% of the sample used e-banking services. Education level is likely to be positively related to e-banking usage because of the aspect of internet usage required for some services like internet and online banking [43] . In Zambia 20.4% of the population has access to internet (3,167,934 out of 16,717,332 population), way below the 28.7% average for Africa and 54.2% average globally [7] . Of the 87.4% of the respondents who indicated that they were using some aspects of E-banking, the majority (49.74%)

Table 1. Sample profile.

cited Automated Teller Machines and Mobile Banking and the least usage was with Point of Sale services and online banking.

Measurement Model Validity

To ensure content validity, the measurement items in the questionnaire were adapted/adopted from the prior related studies in Jordan [27] , Taiwan [28] , Lebanon [15] , India [16] , Hong Kong [29] , Iran [34] and in UK [14] . These included three items for perceived usefulness, three items for perceived ease of use, while trust (representing perceptions of credibility and safety) had six items [29] . The attitude construct had three items [27] [48] ; intention to adopt e-banking had 4 items [29] ; and, finally, actual e-banking adoption (actual behaviour) had only one item [28] . For each item, a 5-point Likert scale was used (1 being strongly disagree and 5 being strongly agree) to enable respondents to indicate the extent to which they agreed with these items. The questionnaire was pilot tested before final distribution to ensure the questions were clear and where necessary rephrased.

The data were analysed using the Statistical Package for Social Sciences (SPSS) version 23. Factor analyses was conducted (since the sample size was > 150) to establish unidimensionality of constructs and validity of the independent variables [49] [50] . Specifically, exploratory factor analysis with principal components extraction and Varimax rotation was conducted. The assumptions for factorability of the data (with correlation coefficients above 0.30) were fulfilled [51] since the Kaiser-Meyer-Olkin Measure of sampling adequacy was 0.901 (minimum value required 0.60), and Bartlett’s Test of Sphericity was significant (Approx. Chi-square = 2672.917, df = 190, sig. = 0.0005). The cumulative percentage of variance explained was 75.882%. To check for consistency and stability of items, Table 2 illustrates the factor loadings resulting in clear five factors with

Table 2. Factor and reliability analyses for constructs.

Eigen values above 1 and all Cronbach’s Alpha values above the minimum threshold of 0.70 [50] . Most parametric multivariate techniques require normally distributed data to reduce the risk of biased and flawed results [52] . In this study, values of skewness and kurtosis were within the acceptable thresholds of + or ?1 for psychometric tests [53] .

4. Results and Discussion

Correlation and Regression Analyses

Correlation Analyses

Pearson correlation analysis was performed to assess the direction and strength of relationships among all variables. Table 3 presents the correlations, mean and standard deviations among the dependent variables (attitudes towards e-banking, intention to adopt e-banking and actual e-banking use), independent variables (perceived usefulness i.e. PU, perceived ease of use, i.e. PEU, and perceived trust, i.e. PT, of e-banking systems) and control variables (age, gender and level of education). The results in Table 3 show relatively low inter-correla- tions among variables (all of them below 0.80). This entails that multicollinearity is not a problem [50] .

Firstly, for control variables, with very small effect sizes, only gender and level of education are significantly associated with e-banking use intention and actual adoption, respectively; age is insignificant. Secondly, Table 3 indicates that attitude toward e-banking services is positively significantly associated (all sig. ≤ 0.01) with each independent variable, namely PU (R = 0.622), PEU (R = 0.509) and PT (R = 0.493). The effect sizes are generally large based on Cohen’s criteria i.e. small = 0.10 to 0.29, medium 0.30 to 0.49 and large = 0.50 to 1.00 [54] . Thirdly, the significant positive correlations indicate that the higher the level of favourable attitude toward e-banking use, the more likely that bank customers will intend to use e-banking services (R = 0.681, p < 0.001, with a large effect size). Similarly, the higher the favourable attitude to e-banking use, the more likely that the bank customers will actually adopt use of e-banking services (R = 0.327, p < 0.001, with a medium size effect). Lastly, the higher the level of intention, the

Table 3. Mean, Standard Deviation (SD) and correlation matrix.

**Correlations significant at the 0.01 level (2-tailed). *Correlation is significant at the 0.05 level (2-tailed).

higher the likelihood of actual adoption of e-banking (R = 0.454, p < 0.01, R2 = 0.206, with a medium effect size).

Multiple Regression Analyses

The study employed regression analysis technique to test the modified Technology Acceptance Model (TAM). The model posits that perceived ease of use, perceived usefulness and perceived trustworthiness of e-banking systems predict customers’ attitude toward e-banking use. Attitude toward e-banking use in turn determines the intention and eventually actual adoption of e-banking [13] [29] [42] . Table 4 and Table 5 show the results of the regression analyses. As can be confirmed from Table 4 and Table 5, the simple and multiple regression analyses present low (< 5) VIF i.e. Variance Inflation Factor for all variables. This indicates that the regression models are not prone to the econometric problem of multicollinearity [50] [55] [56] . The implication is that the multiple regression results presented are unlikely to be biased and the estimates of regression, correlation and determination coefficients are less likely to be inflated.

When considering the results of the regression analyses, Table 4 consists of two models. Model 1 shows the combined effect of the control variables, i.e. age, gender and level of education, to be statistically insignificant with R = 6.1%

Table 4. Multiple regression―antecedents of attitudes to e-banking.

***sig < 0.001 (0.01 percent), **sig < 0.01 (1 percent), *sig < 0.05 (5 percent). VIF = Variance Inflation Factor.

Table 5. Regression-attitude’s influence on intention to adopt e-banking.

***sig < 0.001 (0.01 percent).

(small effect size) and the adjusted R-Squared of less than 1%. None of the control variables makes a significant unique contribution in the multiple regression model. Gender and level of education are only positively significant in the bivariate correlations (Table 3). This result is consistent with prior studies [57] which found a positive influence of the level of education on attitudes towards e-banking. This was in keeping with the notion that e-banking services require use of technology. Therefore, individuals who are educated are likely to find it easy to learn new technologies. Perhaps for this sample in Zambia, the insignificant results in the multiple regression model was because the majority (92.3%) of the respondents had tertiary education. Therefore, the effects of differences in education levels were hardly discernible.

Model 2, besides the three control variables, introduces the three independent variables yielding combined R = 0.693 (large effect size) and R-squared of 46.5%, which are statistically significant. The results indicate a fairly good fit for model 2 and the adjusted R squared is significantly different from zero. The implication is that 46.5% of the variation in the attitude toward e-banking use is explained by the combined effect of perceived usefulness, perceived ease of use and perceived trustworthiness of e-banking systems.

In line with technology adoption and diffusion theories, intended and actual behaviour on e-banking are expected to result from the three attitudinal antecedents of e-banking use. The attitudinal antecedents of e-banking use, namely, perceived usefulness, perceived ease of use and trust, are statistically significant from the presented regression results. These results support Hypotheses H1, H2 and H3. In terms of relative contribution towards predicting attitude to e-banking use, the largest contribution is from perceived usefulness of e-banking services (Beta = 0.463, p < 0.001), followed by trustworthiness of e-banking services (Beta = 0.249, p < 0.001) and lastly perceived ease of use of e-banking systems (Beta = 0.128, p < 0.05).

Lastly, Table 5 displays the regression result of attitude’s influence on intention to adopt E-banking. The adjusted R squared is significantly different from zero and gives a reasonably good fit. Overall, 46.1% of the variation in intention to use e-banking services is explained by the effect of attitude toward E-banking.

Based on correlation and regression results in Table 4 and Table 5, Hypotheses H4 and H5 are also supported. This entails that attitudes toward e-banking use are a significant predictor of intention to adopt e-banking use. Intention in turn is significantly associated with actual e-banking adoption.

Discussion

With the aid of correlation and multiple regression analyses, the findings of the study show that all the three antecedents, namely, perceived ease of use of e-banking services, perceived useful of e-banking services and perceived trust worthiness and safety of e-banking systems, are significantly and positively associated with attitude towards e-banking use. This means that an individuals’ attitude to embrace the use of E-banking services can be improved by increasing his/her perception that e-banking services are useful, ease to use and trustworthy and safe. The results also show that attitudes towards e-banking use significantly help to increase the intention for individuals to adopt e-banking services. Ultimately intention leads to eventual actual adoption of e-banking.

These findings are not only consistent with the hypothesised relationships in the conceptual model, but they also resonate with findings in other countries such as Hong Kong [29] , United Kingdom [14] , India [39] and Malaysia [33] . The results validate the applicability of the modified TAM model in this unique study on the Zambian context. This study adds evidence to the emerging knowledge by providing better understanding to banking entities on the importance of ease of use, perceived usefulness and trust in e-banking adoption decisions by clients.

5. Conclusions and Future Research Direction

The aim of this research was to assess the applicability of the modified Technology Adoption Model (TAM) in the under-researched Zambian context. Thus, the study examined the factors that influence the adoption of e-banking among bank customers. Based on a correlational design and a sample of 222, the research has revealed that perceived usefulness, perceived ease of use and trustworthiness of e-banking systems and services positively correlate with attitude toward e-banking use. In addition, the study found that attitudes to e-banking are positively associated with intention to adopt e-banking. Ultimately intentionality predicts actual adoption of e-banking services.

The theoretical contributions of this study are threefold. Firstly, while there have been many prior studies on the TAM model in relation to factors influencing e-banking adoption, few have actually incorporated the element of trustworthiness of e-banking systems in terms of security, credibility and safety perceptions. This study has established that trust is a significant predictor of e-banking adoption attitudes. Secondly, the study shows that the level of education is positively associated with actual e-banking adoption and gender is also positively related to the intention to adopt e-banking. This means that the more educated and the males are more likely to adopt e-banking.

Thirdly, this is the first study to extend the application of the TAM model to the Zambian context in relation to e-banking. Reproducibility and replicability are at the heart of science and critical to the development of knowledge in any scientific field [58] . The Academy of Management Journal (AMJ), globally the top journal in business and management research, indicates that replication research is important for enhanced confidence in existing knowledge even for seemingly well understood relationships. This is especially so if 1) internal or external validity issues are not yet settled for whatever reasons (e.g. limited contexts of prior research); and 2) there is an empirically established relationship that should serve as a basis for broad theorising in a field or that has company-wide or public policy implications [18] [59] (p. 314). The fact that literature on Zambia was non-existent represented a contextual gap in knowledge which limited generalisability of prior research conclusions [60] . To contribute to filling this gap, this research tested the modified TAM model in the under researched Zambian context. The findings conclude that indeed in the Zambian context also, perceived usefulness, perceived ease of use and trust are significant in predicting e-banking adoption. This research helps to increase the evidence base and generalisability of the model.

For scholars, practitioners and policy makers, the practical implications of these findings are four-fold. Firstly, the modified TAM model is applicable in the Zambian context for assessing, monitoring and increasing the adoption of e-banking services. Secondly, to increase adoption of e-banking services, there is need to increase awareness among current and potential bank customers about the usefulness i.e. benefits of e-banking. Thirdly, to further increase use of e-banking services, it is essential to provide information to customers and potential customers about how to use the e-banking services. This means the easier it is to use e-banking services, the more customers are likely to want to adopt e-banking. Lastly, when current and potential customers trust the e-banking systems and feel that their assets are secure, they will tend to use them more.

Limitations and Directions for Future Research

Like any other study, this research had limitations which form the basis for suggestions on directions for future research. Firstly, the study was conducted in two major provinces of Zambia i.e. the Copperbelt and Lusaka. Though the two have the most population in the country and the highest level of commercial activity, non-inclusion of the other 8 provinces may limit generalisability. Future studies should consider a sample that reaches the whole country. Secondly, the study was cross-sectional and therefore the findings could only proffer a snapshot of the phenomenon. Future studies should attempt longitudinal designs that explore the transition from intention to actual behaviour. With the cross-sectional nature of this study, the results allow for correlational inferences rather than causality. To show causation, longitudinal research, possibly in a quasi-experimental design, may be necessary [14] .

Acknowledgements

The authors wish to thank Virginia Halubobya Moono for data collection support and Chanda Chileshe for data entry support.

Cite this paper

Mwiya, B., Chikumbi, F., Shikaputo, C., Kabala, E., Kaulung’ombe, B. and Siachinji, B. (2017) Examining Factors Influencing E-Banking Adoption: Evidence from Bank Customers in Zambia. American Journal of Industrial and Business Management, 7, 741-759. https://doi.org/10.4236/ajibm.2017.76053

References

- 1. PWC (2016) Price Water House. Total Retail Survey—Online Shoppers Globally Are Fundamentally Disrupting Retail Again.

- 2. Mwiya, B. (2006) Credit Default in the Zambian Banking Sector: Need for Credit Reference Bureaus. Journal of Business, 1, 2-15.

- 3. Akrani, G. (2011) What Is Finance? Mcgraw Hill Higher Education, London.

- 4. Khurshid, A., Rizwan, M. and Tasneem, E. (2014) Factors Contributing towards Adoption of E-banking in Pakistan. International Journal of Accounting and Financial Reporting, 4, 437.

https://doi.org/10.5296/ijafr.v4i2.6584 - 5. Nuwagaba, A. and Brighton, N. (2014) Analysis of E-Banking as a Tool to Improve Banking Services in Zambia. International Journal of Business and Management Invention, 3, 62-67.

- 6. Bank of Zambia FinScope Report (2010) A Survey of the Population’s Access to Financial Access in Zambia.

- 7. MMG (2016) Zambia Internet Stats and Telecommunications Reports (IWS). A Miniwatts Marketing Group Publication.

- 8. BOZ Finscope Report (2016) A Survey of the Population’s Access to Financial Access in Zambia.

- 9. Venkatesh, V., Morris, M., Davis, G. and Davis, F. (2003) User Acceptance of Information Technology: Toward a Unified View. MIS Quarterly, 27, 424-478.

- 10. Kuisma, T., Laukkanen, T. and Hiltunen, M. (2007) Mapping the Reasons for Resistance to Internet Banking: A Means-End Approach. International Journal of Information, 27, 75-85.

- 11. Salhieh, L., Abu-Doleh, J. and Hijazi, N. (2011) The Assessment of E-banking Readiness in Jordan. International Journal of Islamic and Middle Eastern Finance and Management, 4, 325-342.

https://doi.org/10.1108/17538391111186564 - 12. Ajzen, I. (2011) The Theory of Planned Behaviour: Reactions and Reflections. Psychology & Health, 26, 1113-1127.

https://doi.org/10.1080/08870446.2011.613995 - 13. Davis, F. (1989) Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Quarterly, 13, 319-340.

https://doi.org/10.2307/249008 - 14. Yousafzai, S.Y., Foxall, G.R. and Pallister, J.G. (2010) Explaining Internet Banking Behavior: Theory of Reasoned Action, Theory of Planned Behavior, or Technology Acceptance Model? Journal of Applied Social Psychology, 40, 1172-1202.

- 15. Tarhini, A., El-Masri, M., Ali, M. and Serrano, A. (2016) Extending the UTAUT Model to Understand the Customers’ Acceptance and Use of Internet Banking in Lebanon. Information Technology & People, 29, 830-849.

https://doi.org/10.1108/ITP-02-2014-0034 - 16. Kesharwani, A. and Singh, B.S. (2012) The Impact of Trust and Perceived Risk on Internet Banking Adoption in India. International Journal of Bank Marketing, 30, 303-322.

https://doi.org/10.1108/02652321211236923 - 17. Al-Smadi, M.O. (2012) Factors Affecting Adoption of Electronic Banking: An Analysis of the Perspectives of Banks’ Customers. International Journal of Business and Social Science, 3.

- 18. Miller, C.C. and Bamberger, P. (2016) Exploring Emergent and Poorly Understood Phenomena in the Strangest of Places: the Footprint of Discovery in Replications, Meta-Analyses, and Null Findings. Academy of Management Discoveries, 2, 313-319.

https://doi.org/10.5465/amd.2016.0115 - 19. Kamrul, H. (2009) E-Banking in Bangladesh: The Future of Banking. School of Business Studies.

- 20. Muzividzi, D., Mbizi, R. and Mukwazhe, T. (2013) An Analysis of Factors That Influence Internet Banking Adoption among Intellectuals: Case of Chinhoyi University of Technology. Interdisciplinary Journal of Contemporary Research in Business, 4, 350-369.

- 21. Bultum, A. (2014) Factors Affecting Adoption of Electronic Banking System in Ethiopian Banking Industry. Journal of Management Information System and E-Commerce, 1, 1-17.

- 22. Alagheband, P. (2006) Adoption of Electronic Banking Services by Iranian Customers. Master Thesis, Lulea University of Technology, Sweden.

- 23. Sohrabi, M., Yee, J. and Nathan, R. (2013) Critical Success Factors For the Adoption of E-Banking in Malaysia. International Arab Journal of e-Technology, 3.

- 24. Fishbein, M. and Ajzen, I. (1975) Belief, Attitude, Intention and Behaviour: An Introduction to Theory and Research. Addison-Wesley, Boston.

- 25. Ajzen, I. (1991) The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes, 50, 179-211.

https://doi.org/10.1016/0749-5978(91)90020-T - 26. Hanafizadeh, P., Keating, B. and Khedmatgozar, H.R. (2014) A Systematic Review of Internet Banking Adoption. Telematics and Informatics, 31, 492-510.

https://doi.org/10.1016/j.tele.2013.04.003 - 27. AbuShanab, E. and Pearson, J.M. (2007) Internet Banking in Jordan. Journal of Systems and Information Technology, 9, 78-97.

https://doi.org/10.1108/13287260710817700 - 28. Shih, Y. and Fang, K. (2004) The Use of a Decomposed Theory of Planned Behavior to Study Internet Banking in Taiwan. Internet Research, 14, 213-223.

- 29. Cheng, T.C.E., Lam, D.Y.C. and Yeung, A.C.L. (2006) Adoption of Internet Banking: An Empirical Study in Hong Kong. Decision Support Systems, 42, 1558-1572.

https://doi.org/10.1016/j.dss.2006.01.002 - 30. Gefen, D. (2002) Reflections on the Dimensions of Trust and Trustworthiness among Online Consumers. ACM SIGMIS Database, 33, 38-53.

- 31. Ajzen, I. and Fishbein, M. (1980) Understanding Attitudes and Predicting Social Behavior. Prentice-Hall, Upper Saddle River.

- 32. Shaikh, A. and Karjaluoto, H. (2015) Mobile Banking Adoption: A Literature Review. Telematics and Informatics, 32, 129-142.

https://doi.org/10.1016/j.tele.2014.05.003 - 33. Chong, Y., Seow, A. and Lee, E. (2015) The Adoption of E-banking among Rural SME Operators in Malaysia: An Integration of TAM and TPB. The Josai Journal of Business Administration, 11-12, 39-49.

- 34. Mohammadi, H. (2015) A Study of Mobile Banking Usage in Iran. International Journal of Bank Marketing, 33, 733-759.

https://doi.org/10.1108/IJBM-08-2014-0114 - 35. Sundarraj, R. and Manochehri, N. (2013) Application of an Extended TAM Model for Online Banking Adoption: A Study at a Gulf-Region University. In: Khosrow-Pour, M., Ed., Managing Information Resources and Technology: Emerging Applications and Theories, IGI Global, Hershey, PA, 1-13.

https://doi.org/10.4018/978-1-4666-3616-3.ch001 - 36. Lee, K., Lee, H. and Kim, S. (2007) Factors Influencing the Adoption Behavior of Mobile Banking: A South Korean Perspective. Journal of Internet Banking & Commerce, 12, 1-9.

- 37. Sikdar, P., Kumar, A. and Makkad, M. (2015) Online Banking Adoption. International Journal of Bank Marketing, 33, 760-785.

https://doi.org/10.1108/ijbm-11-2014-0161 - 38. Mathwick, C., Malhotra, N. and Rigdon, E. (2001) Experiential Value: Conceptualization, Measurement and Application in the Catalog and Internet Shopping Environment. Journal of Retailing, 77, 39-56.

https://doi.org/10.1016/S0022-4359(00)00045-2 - 39. Gupta, D. and Kamilla, U. (2014) Cyber Banking in India: A Cross-Sectional Analysis Using Structural Equation Model. IUP Journal of Bank Management, 13, 47.

- 40. Zhou, T. (2014) Understanding the Determinants of Mobile Payment Continuance Usage. Industrial Management & Data Systems, 114, 936-948.

https://doi.org/10.1108/IMDS-02-2014-0068 - 41. Al-Shbiel, S. and Ahmad, M. (2016) A Theoretical Discussion of Electronic Banking in Jordan by Integrating Technology Acceptance Model and Theory of Planned Behavior. International Journal of Academic Research in Accounting, Finance and Management Sciences, 6, 272-284.

- 42. Wu, M., Jayawardhena, C. and Hamilton, R. (2014) A Comprehensive Examination of Internet Banking User Behaviour: Evidence from Customers Yet to Adopt, Currently Using and Stopped Using. Journal of Marketing, 30, 1006-1038.

https://doi.org/10.1080/0267257x.2014.935459 - 43. Aderonke, A.A.J. (2010) An Empirical Investigation of the Level of Users’ Acceptance of E-Banking in Nigeria. Journal of Internet Banking and Commerce, 15, 1-13.

- 44. Feizi, K. and Ronaghi, M. (2010) A Model for E-banking Trust in Iran’s Banking Industry. International Journal of Industrial Engineering and Production Research, 20, 23-33.

- 45. Creswell, J. (2012) Educational Research: Planning, Conducting and Evaluating Qualitative and Quantitative Research. 4th Edition, Pearson Education, Thousands oaks, CA.

- 46. Saunders, M.N.K., Lewis, P. and Thornhill, A. (2009) Research Methods for Business Students. 5th Edition, Pearson Education, London.

- 47. CSO (2013) Zambian 2010 Census Data Reports. Central Statistical Office in Zambia.

- 48. Nor, K.M. and Pearson, J.M. (2008) An Exploratory Study into The Adoption of Internet Banking in a Developing Country: Malaysia. Journal of Internet Commerce, 7, 29-73.

https://doi.org/10.1080/15332860802004162 - 49. Hair, J., Black, W., Babin, B. and Anderson, R. (2010) Multivariate Data Analysis. 7th Edition, Pearson Education, NJ.

- 50. Pallant, J. (2016) SPSS Survival Manual: A Step by Step Guide to Data Analysis Using SPSS Program. 6th Edition, McGraw-Hill Education, London, UK.

- 51. Tabachnick, B.G. and Fidell, L.S. (2012) Using Multivariate Statistics. Pearson Education, London.

- 52. Hair, J., Black, W., Babin, B., Anderson, R. and Tatham, R. (2006) Multivariate Data Analysis. 6th Edition, Pearson Education, NJ.

- 53. George, D. and Mallery, P. (2003) Using SPSS for Windows Step by Step: A Simple Guide and Reference. 4th Edition, Pearson Education, London.

- 54. Cohen, J.W. (1988) Statistical Power Analysis for the Behavioral Sciences. 2nd 4th Edition, Lawrence Erlbaum Associates, Hillsdale, NJ.

- 55. Studenmund, A.H. (2011) Using Econometrics: A Practical Guide. Pearson Publishers, New York.

- 56. Wang, Y. and Ahmed, P.K. (2009) The Moderating Effect of the Business Strategic Orientation on E-Commerce Adoption: Evidence From UK Family Run SMEs. The Journal of Strategic Information Systems, 18, 16-30.

https://doi.org/10.1016/j.jsis.2008.11.001 - 57. Oyeleye, O., Sanni, M. and Shittu, T. (2015) An Investigation of the Effects of Customer’s Educational Attainment on Their Adoption of E-Banking in Nigeria. Journal of Internet Banking and Commerce, 20, 1-16.

- 58. Evanschitzky, H., Baumgarth, C., Hubbard, R. and Armstrong, J.S. (2007) Replication Research’s Disturbing Trend. Journal of Business Research, 60, 411-415.

https://doi.org/10.1016/j.jbusres.2006.12.003 - 59. Eden, D. (2002) From the Editors Replication. Academy of Management Journal, 45, 841-846.

https://doi.org/10.5465/AMJ.2002.7718946 - 60. Solesvik, M.Z., Westhead, P., Kolvereid, L. and Matlay, H. (2012) Student Intentions to Become Self-Employed: The Ukrainian Context. Journal of Small Business and Enterprise Development, 19, 441-460.

https://doi.org/10.1108/14626001211250153