Open Journal of Statistics

Vol.4 No.5(2014), Article ID:48571,15 pages

DOI:10.4236/ojs.2014.45033

Distribution of the Sample Correlation Matrix and Applications

Thu Pham-Gia, Vartan Choulakian

Department of Mathematics and Statistics, Université de Moncton, Moncton, Canada

Email: Thu.pham-gia@umoncton.ca, Vartan.choulakian@umoncton.ca

Copyright © 2014 by authors and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 29 May 2014; revised 5 July 2014; accepted 15 July 2014

ABSTRACT

For the case where the multivariate normal population does not have null correlations, we give the exact expression of the distribution of the sample matrix of correlations R, with the sample variances acting as parameters. Also, the distribution of its determinant is established in terms of Meijer G-functions in the null-correlation case. Several numerical examples are given, and applications to the concept of system dependence in Reliability Theory are presented.

Keywords: Correlation, Normal, Determinant, Meijer G-Function, No-Correlation, Dependence, Component, Formatting, Style, Styling, Insert

1. Introduction

The correlation matrix plays an important role in multivariate analysis since by itself it captures the pairwise degrees of relationship between different components of a random vector. Its presence is very visible in Principal Component Analysis and Factor Analysis, where in general, it gives results different from those obtained with the covariance matrix. Also, as a test criterion, it is used to test the independence of variables, or subsets of variables ([1] , p. 407).

In a normal distribution context, when the population correlation matrix , the identity matrix, or equivalently,

the population covariance matrix

, the identity matrix, or equivalently,

the population covariance matrix

is diagonal, i.e.

is diagonal, i.e. , the distribution of the sample correlation

matrix R is relatively easy to compute, and its determinant has a distribution that

can be expressed as a Meijer G-function distribution. But when

, the distribution of the sample correlation

matrix R is relatively easy to compute, and its determinant has a distribution that

can be expressed as a Meijer G-function distribution. But when

no expression for the density of R is presently available in the literature, and

the distribution of its determinant is still unknown, in spite of efforts made by

several researchers. We will provide here the closed form expression of the distribution

of R, with the sample variances as parameters, hence complementing a result presented

by Fisher in [2] .

no expression for the density of R is presently available in the literature, and

the distribution of its determinant is still unknown, in spite of efforts made by

several researchers. We will provide here the closed form expression of the distribution

of R, with the sample variances as parameters, hence complementing a result presented

by Fisher in [2] .

As explained in [3] , for a random matrix, there

are at least three distributions of interest, its “entries distribution” which gives

the joint distribution of its matrix entries, its “determinant distribution” and

its “latent roots distribution”. We will consider the first two only and note that,

quite often, the first distribution is also expressed in terms of the determinant,

and can lead to some confusion. In Section 2 we recall some results related to the

case where , and establish the new exact

expression of the density of R, with the sample variances

, and establish the new exact

expression of the density of R, with the sample variances

as parameters, denoted

as parameters, denoted . In Section 3, some simulation

results are given. The distribution of

. In Section 3, some simulation

results are given. The distribution of , the determinant

of R, is given in Section 4 for

, the determinant

of R, is given in Section 4 for . Applications of the above

results to the concept of dependence within a multi-component system are given in

Section 5. Numerical examples are given throughout the latter part of the paper

to illustrate the results.

. Applications of the above

results to the concept of dependence within a multi-component system are given in

Section 5. Numerical examples are given throughout the latter part of the paper

to illustrate the results.

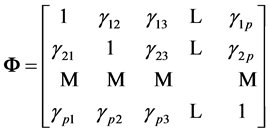

2. Case of the Population Correlation Matrix Not Being Identity

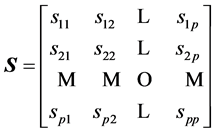

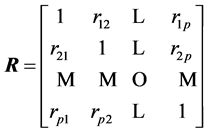

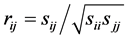

2.1. Covariance and Correlation Matrices

Let us consider a random vector X with mean

and covariance matrix

and covariance matrix , of the form of

a (p × p) symmetric positive definite random matrix

, of the form of

a (p × p) symmetric positive definite random matrix

of pairwise covariances between components in the matrix.

We obtain the population correlation matrix

by diving each

by diving each

by

by . Then

. Then

, where

, where , is symmetrical, with diagonals

, is symmetrical, with diagonals ,

,

, i.e.

, i.e.

.

.

For a sample of size n of observations from , the sample mean

, the sample mean

and the “adjusted sample covariance” matrix

and the “adjusted sample covariance” matrix

, (1)

, (1)

(or matrix of sums of squares and products, ) are independent,

with the latter having a Wishart distribution

) are independent,

with the latter having a Wishart distribution . Similarly, the correlation

matrix

. Similarly, the correlation

matrix

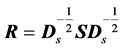

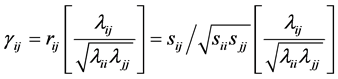

is obtained from S by using the relations:

is obtained from S by using the relations: , or

, or , where

, where . We also have the relation

between determinants:

. We also have the relation

between determinants: , and, similarly,

, and, similarly, .

.

It is noted that by considering the usual sample covariance matrix , which is

, which is

, we have the relation

, we have the relation , between the

two diagonal elements, but the sample correlation matrix is the same.

, between the

two diagonal elements, but the sample correlation matrix is the same.

The

coefficients

coefficients

are (marginally) distributed independently of both the sample and population means

[2] . It is to be noticed that while R can always be defined

from S, the reverse is not true since S has

are (marginally) distributed independently of both the sample and population means

[2] . It is to be noticed that while R can always be defined

from S, the reverse is not true since S has

independent parameters. This fact explains the differences between results when

either R or S is used.

independent parameters. This fact explains the differences between results when

either R or S is used.

In the bivariate case, Hotelling’s expression [4]

clearly shows that the density of r depends only on the population correlation coefficient

and the sample size n (see Section 4.3) and we will see that, similarly, the density

of the sample correlation matrix, with the sample variances as parameters, is dependent

on the population variances and the sample size. However,

and the sample size n (see Section 4.3) and we will see that, similarly, the density

of the sample correlation matrix, with the sample variances as parameters, is dependent

on the population variances and the sample size. However,

are biased estimators of

are biased estimators of , and Olkin and

Pratt [5] have suggested using the modified estimator

, and Olkin and

Pratt [5] have suggested using the modified estimator , with a table of corrective multipliers for

, with a table of corrective multipliers for

for convenience.

for convenience.

2.2. Some Related Work

Several efforts have been carried out in the past to obtain the exact form of the

density of R for the general case, where ,

,

and

and . For example,

Joarder and Ali [6] derived the distribution of

R for a class of elliptical models. Ali, Fraser and Lee

[7] , starting from the identity correlation matrix case, derived the

density for the general case when

. For example,

Joarder and Ali [6] derived the distribution of

R for a class of elliptical models. Ali, Fraser and Lee

[7] , starting from the identity correlation matrix case, derived the

density for the general case when , again by modulating the likelihood

ratio to obtain a density of R containing the function

, again by modulating the likelihood

ratio to obtain a density of R containing the function , already used by Fraser ([8]

, p. 196) in the bivariate case. But here,

, already used by Fraser ([8]

, p. 196) in the bivariate case. But here,

, expressed as an infinite series, has a much

more complicated expression. Schott ([9] , p. 408),

using

, expressed as an infinite series, has a much

more complicated expression. Schott ([9] , p. 408),

using , gives for a first-order approximation for

R and the expression of

, gives for a first-order approximation for

R and the expression of , and Kollo and Ruul

[10] , also using

, and Kollo and Ruul

[10] , also using , presented a general

method for approximating the density of R through another multivariate density,

possibly one of higher dimension. Finally, Farrell ([11]

, p. 177) has approached the problem using exterior differential forms. However,

no explicit expression for the density of R is given in any of these works, and

the question rightly raised is whether that such an expression really exists.

, presented a general

method for approximating the density of R through another multivariate density,

possibly one of higher dimension. Finally, Farrell ([11]

, p. 177) has approached the problem using exterior differential forms. However,

no explicit expression for the density of R is given in any of these works, and

the question rightly raised is whether that such an expression really exists.

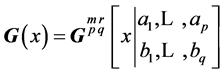

2.3. Some New Results

We begin with the case of . Then it can be easily established that

the density of R is ([12] , p. 107):

. Then it can be easily established that

the density of R is ([12] , p. 107):

(2)

(2)

By showing that the joint density of the diagonal elements

with R, denoted

with R, denoted , can be factorized into the

product of two densities,

, can be factorized into the

product of two densities,

and

and , which has expression

(2) above.

, which has expression

(2) above.

and R are hence independent.

and R are hence independent.

We can also show that (2) is a density, i.e. it integrates to 1 within its definition domain, by using the approach given in Mathai and Haubold ([13] , p. 421), based on matrix decomposition.

In what follows, following Kshirsagar’s approach [14]

, which itself is a variation of Fisher’s

[2] original

method, we establish first the expression of a similar joint distribution, when

is not diagonal.

is not diagonal.

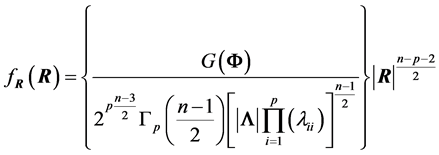

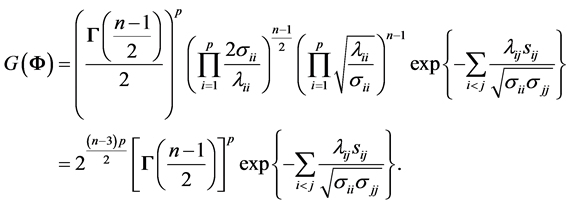

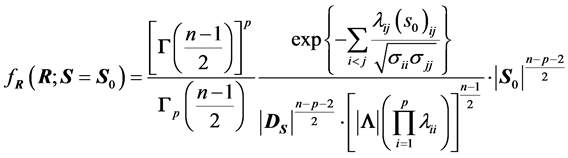

THEOREM 1:

Let

, where we suppose that the population correlation

, where we suppose that the population correlation

and its inverse

and its inverse

has

has

as its diagonal elements. Then the correlation matrix R of a random sample of n

observations has its distribution given by:

as its diagonal elements. Then the correlation matrix R of a random sample of n

observations has its distribution given by:

, (3)

, (3)

where , with the sample covariance

, with the sample covariance ,

,

, serving as parameters.

, serving as parameters.

PROOF: Let us consider the “adjusted sample covariance matrix” S, given by (1).

We know that

, with density:

, with density:

with C being an appropriate constant.

with C being an appropriate constant.

Our objective is to find the joint density of R with a set of variables

so that the density of R can be obtained by integrating out the variables

so that the density of R can be obtained by integrating out the variables .

.

Let

be the inverse of

be the inverse of , the (population)

matrix of correlations, with diagonals

, the (population)

matrix of correlations, with diagonals ,

,

and non-diagonals

and non-diagonals ,

,

,

, . We first transform

the

. We first transform

the

variables

variables ,

,

, into

, into . Since the diagonal

. Since the diagonal

remain unchanged, the Jacobian of the transformation from S to

remain unchanged, the Jacobian of the transformation from S to

is then

is then

and the new joint density is:

and the new joint density is:

where

and

and .

.

We set

(4)

(4)

with , and form the symmetric matrix

, and form the symmetric matrix

, (5)

, (5)

where , which depends on S.

, which depends on S.

The joint density of

and R is now:

and R is now:

.

.

R and

are independent only if the above expression can be expressed as the product

are independent only if the above expression can be expressed as the product

, which is not the case since

, which is not the case since

contains

contains .

.

To integrate out the vector , we set

, we set

,

,

(This integral is denoted

by Fisher

[2] , and by

by Fisher

[2] , and by

by Kshirsagar [14] who used the notation

by Kshirsagar [14] who used the notation

and, in both instances, was left non-computed).

and, in both instances, was left non-computed).

Hence, if

is constant, as in the case when

is constant, as in the case when , R would have density

, R would have density

, (6)

, (6)

with , being the p-gamma function. However, in

the general case this is not true.

, being the p-gamma function. However, in

the general case this is not true.

Consider the quadratic form:

and

and

.

.

Changing to , we have

, we have

Since each integral is a gamma density in , with value

, with value , we obtain

, we obtain

contains all non-diagonal entries of the sample

covariance matrix, and depends on S. We now obtain from (6) expression (3) of Theorem

1. Here, the off-diagonal sample covariance,

contains all non-diagonal entries of the sample

covariance matrix, and depends on S. We now obtain from (6) expression (3) of Theorem

1. Here, the off-diagonal sample covariance,

, serve as parameters of this density.

, serve as parameters of this density.

QED.

Alternately, using the corresponding correlation coefficients, we have:

, (7)

, (7)

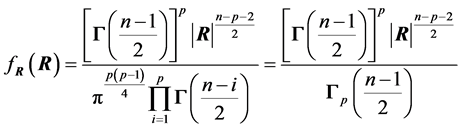

REMARKS:

1) For

our results given above should reduce to known results, and they do. Indeed, since

we now have

our results given above should reduce to known results, and they do. Indeed, since

we now have

.

.

Hence,

as in (2) since we now have .

.

Here, only the value of p needs to be known and this explains why expression (2) depends only on n and p. Also, as pointed out by Muirhead ([15] , p. 148), if we do not suppose normality, the same results can be obtained under some hypothesis.

2) Expression (3) can be interpreted as the density of R when

are known, and

are known, and , is a set of constant sample

covariances. But when this set is considered as a random vector, with a certain

distribution,

, is a set of constant sample

covariances. But when this set is considered as a random vector, with a certain

distribution,

is called mixture distribution, defined in

two steps:

is called mixture distribution, defined in

two steps:

a)

has an (known or unknown) distribution

has an (known or unknown) distribution , i.e.

, i.e. .

.

b) (R; ) has the density given by (3), denoted

) has the density given by (3), denoted .

.

The distribution of R is then , where * denotes the mixture

operation.

, where * denotes the mixture

operation.

However, a closed form for this mixture is often difficult to obtain.

Alternately,

could be

could be , with

, with

being the density of the diagonal sample variances

being the density of the diagonal sample variances

and off-diagonal sample correlations,

while

while

is given by (7).

is given by (7).

3) We have, using (3), and the relation

the following equivalent expression, where

the following equivalent expression, where

:

:

. (8)

. (8)

Expression (8) gives the positive numerical value of

upon knowledge of the value of S. It will serve to set up simulation computations

in Section 3. However, it also shows that

upon knowledge of the value of S. It will serve to set up simulation computations

in Section 3. However, it also shows that

can be defined with S, and when S has a certain distribution the values of

can be defined with S, and when S has a certain distribution the values of

are completely determined with that distribution. This highlights again the fact

that, in statistics, using R or S can lead to different results, as mentioned previously.

are completely determined with that distribution. This highlights again the fact

that, in statistics, using R or S can lead to different results, as mentioned previously.

2.4. Other Known Results

1) The distribution of the sample coefficient of correlation in the bivariate normal

case can be determined fairly directly when integrating out

and

and , and this fact is mentioned explicitly by

Fisher ([2]

, p. 4), who stated: “This, however, is not a feasible path for more than two variables.”

In the bivariate case,

, and this fact is mentioned explicitly by

Fisher ([2]

, p. 4), who stated: “This, however, is not a feasible path for more than two variables.”

In the bivariate case,

, and has been well-studied by several researchers,

using different approaches and, as early as 1915, Fisher

[16] gave its density as:

, and has been well-studied by several researchers,

using different approaches and, as early as 1915, Fisher

[16] gave its density as:

(9)

(9)

Using geometric arguments, with

being the population coefficient of correlation. We refer to ([17]

, p. 524-534) for more details on the derivation of the above expression. Other

equivalent expressions, reportedly as numerous as 52, were obtained by other researchers,

such as Hotelling [4] , Sawkins [18] , Ali et al. [7]

.

being the population coefficient of correlation. We refer to ([17]

, p. 524-534) for more details on the derivation of the above expression. Other

equivalent expressions, reportedly as numerous as 52, were obtained by other researchers,

such as Hotelling [4] , Sawkins [18] , Ali et al. [7]

.

2) Using Equation (3) on the sample correlation matrix , obtained from the

sample covariance matrix

, obtained from the

sample covariance matrix

Together with p = 2, we can also arrive at

one of these forms (see also Section 4.3, where the determinant of R provides a

more direct approach).

Together with p = 2, we can also arrive at

one of these forms (see also Section 4.3, where the determinant of R provides a

more direct approach).

3) Although Fisher [2] did not give the explicit form of the

integral

above, he included several interesting results on

above, he included several interesting results on , as a function of the sample

size n and coefficients

, as a function of the sample

size n and coefficients . For example, in the case all

. For example, in the case all ,

,

, the generalized volume in the p(p −

1)/2-dimension space of the region of integration for rij is found to

be a function of p, having a maximum at p = 6. In the case all

, the generalized volume in the p(p −

1)/2-dimension space of the region of integration for rij is found to

be a function of p, having a maximum at p = 6. In the case all , the expressions

of the partial derivatives of Log

, the expressions

of the partial derivatives of Log w.r.t.

w.r.t.

can be obtained, and so are the mixed derivatives.

can be obtained, and so are the mixed derivatives.

For the case n = 2, and p = 3,

has an interesting geometrical interpretation

as

has an interesting geometrical interpretation

as , where V = generalized volume defined by

, where V = generalized volume defined by

and D is the volume defined by the p unit vectors in a transformation where

and D is the volume defined by the p unit vectors in a transformation where

are the cosines of the angles between pairs of edges.

are the cosines of the angles between pairs of edges.

3. Some Computation and Simulation Results

3.1. Simulations Related to R

A matrix equation such as (3) can be difficult to visualize numerically, especially

when the dimensions are high, i.e. . Ideally, to illustrate (7), a figure

giving

. Ideally, to illustrate (7), a figure

giving

in function of the matrix R itself is most informative, but, naturally, impossible

to obtain. One question we can investigate is how the values of

in function of the matrix R itself is most informative, but, naturally, impossible

to obtain. One question we can investigate is how the values of

distributed, for a normal model

distributed, for a normal model ? Simulation using (8)

can provide some information on this distribution in some specific cases. For example,

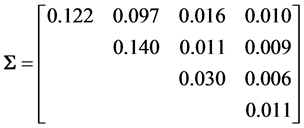

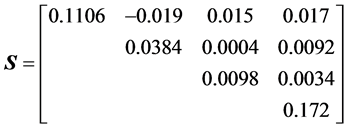

we can start from the (4 × 4) population covariance matrix

? Simulation using (8)

can provide some information on this distribution in some specific cases. For example,

we can start from the (4 × 4) population covariance matrix

taken from our analysis of Fisher’s iris data [19] . It concerns the Setosa iris variety, with x1

= sepal length, x2 = sepal with, x3 = petal length and x4

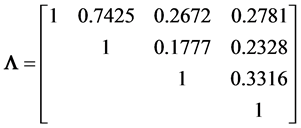

= petal width. It gives the population correlation matrix

taken from our analysis of Fisher’s iris data [19] . It concerns the Setosa iris variety, with x1

= sepal length, x2 = sepal with, x3 = petal length and x4

= petal width. It gives the population correlation matrix

where all

where all . We generate 10,000

samples of 100 observations each from

. We generate 10,000

samples of 100 observations each from , which give 10,000 values

of the covariance matrix S, which, in turn, give matrix values for R, scalar values

for

, which give 10,000 values

of the covariance matrix S, which, in turn, give matrix values for R, scalar values

for

and, finally, positive scalar values for

and, finally, positive scalar values for , as given by (8). Recall

that for X normal S has a Wishart distribution

, as given by (8). Recall

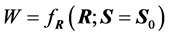

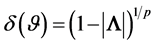

that for X normal S has a Wishart distribution . Figure 1

gives the corresponding histogram, which shows that values of W are distributed

along a unimodal density, denoted by

. Figure 1

gives the corresponding histogram, which shows that values of W are distributed

along a unimodal density, denoted by , with a very small variation

interval, i.e. most of its values are concentrated around the mode.

, with a very small variation

interval, i.e. most of its values are concentrated around the mode.

Note: A special approach to graphing distributions of covariance matrices, using the principle of decomposing a matrix into scale parameters and correlations, is presented in: Tokuda, T., Goodrich, B., Van Mechelen, I., Gelman, A. and Tuerlinckx, F., Visualizing Distributions of Covariance Matrices (Document on the Internet).

It is also mentioned there that for the Inverted Wishart case, with

degrees of freedom, then

degrees of freedom, then

where

where

is the i-th principal sub-matrix of R, obtained by removing row and column i (p.

12).

is the i-th principal sub-matrix of R, obtained by removing row and column i (p.

12).

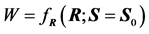

3.2. Simulations Related to

Similarly, the same application above gives the approximate simulated distribution

of

presented in Figure 2. We can see that it is a

unimodal density which depends on the correlation coefficients

presented in Figure 2. We can see that it is a

unimodal density which depends on the correlation coefficients .

.

Using expression (7), which exhibits explicitely rij, and replacing rij

by the corrected value the unbiased estimator

of

the unbiased estimator

of , we obtain

, we obtain . However, since an unbiased estimator

of

. However, since an unbiased estimator

of

is still to be found we cannot use neither

is still to be found we cannot use neither

nor

nor

as point-estimate of

as point-estimate of . Figure 2

gives the simulated distributions of

. Figure 2

gives the simulated distributions of

and of

and of . We can see that the two approximate densities

are different, and the density of

. We can see that the two approximate densities

are different, and the density of

has higher mean and median, resulting in a shift to the right. But, again, the two

variation intervals are very small.

has higher mean and median, resulting in a shift to the right. But, again, the two

variation intervals are very small.

3.3. Expression of

In the proof of Theorem 1, we have established that

Figure 1. Simulated density

of .

.

Figure 2.

Simulated densities of

and

and .

.

Using the above matrix , for a simulated sample,

say

, for a simulated sample,

say

we compute directly the left side by numerical integration,

and the right side by using the algebraic expression. The results are extremely

close to each other, with both around the numerical value 1.238523012 × 105.

we compute directly the left side by numerical integration,

and the right side by using the algebraic expression. The results are extremely

close to each other, with both around the numerical value 1.238523012 × 105.

4. Distribution of , the Determinant of R

, the Determinant of R

First, let det(R) be denoted by . In this case

. In this case , this distribution is very complex

and no related result is known when

, this distribution is very complex

and no related result is known when . Nagar and Castaneda

[20] , for example, established some results in the general case,

for p = 2.

. Nagar and Castaneda

[20] , for example, established some results in the general case,

for p = 2.

Theoretically, we can obtain the density of

from (3) by applying the transformation

from (3) by applying the transformation , with differential

, with differential , but the expression obtained quickly

becomes intractable. Only in the case of

, but the expression obtained quickly

becomes intractable. Only in the case of

that we can derive some analytical results on

that we can derive some analytical results on , as presented in the next section.

Gupta and Nagar [21] established some results

for the case of a mixture of normal models, but again under the hypothesis of

, as presented in the next section.

Gupta and Nagar [21] established some results

for the case of a mixture of normal models, but again under the hypothesis of .

.

4.1. Density of the Determinant

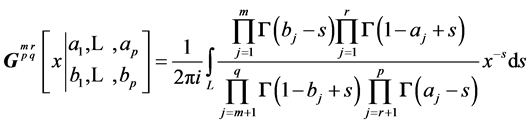

When considering Meijer G-functions and their extensions, Fox’s H-functions [22] , for

the density of

the density of

can be expressed in closed forms, as are those of other related multivariate statistics

[23] . Let us recall that the Meijer

function

can be expressed in closed forms, as are those of other related multivariate statistics

[23] . Let us recall that the Meijer

function , and the Fox function

, and the Fox function , are defined as follows:

, are defined as follows:

is the integral along the complex contour L of a

rational expression of Gamma functions

is the integral along the complex contour L of a

rational expression of Gamma functions

(10)

(10)

It is a special case, when

, of Fox’s H-function, defined as:

, of Fox’s H-function, defined as:

.

.

Under some fairly general conditions on the poles of the gamma functions in the numerator, the above integrals exist.

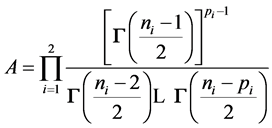

THEOREM 2: When , for a random sample of size n from

, for a random sample of size n from , the density of

, the density of

depends only on n and p:

depends only on n and p:

. (11)

. (11)

PROOF:

From (2) the moments of order t of

are:

are:

, (12)

, (12)

, which is a product of moments of order t of independent beta

variables. Upon identification of (12) with these products, we can see that

, which is a product of moments of order t of independent beta

variables. Upon identification of (12) with these products, we can see that , with

, with , with

, with . Using

[23] the product of k independent betas,

. Using

[23] the product of k independent betas,

, has as density

, has as density

Hence, we have here, the density of

as:

as:

where

where ,

,

,

,

,

,

and

and ,

, .

.

And, hence, we obtain:

(13)

(13)

QED.

The density of

can easily be computed and graphed, and percentiles of

can easily be computed and graphed, and percentiles of

can be determined numerically. For example, for p = 4, n = 8. The 2.5th

and 97.5th percentiles can be found to be 0.04697 and 0.7719 respectively.

can be determined numerically. For example, for p = 4, n = 8. The 2.5th

and 97.5th percentiles can be found to be 0.04697 and 0.7719 respectively.

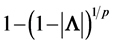

4.2. Product and Ratio

Let

and

and

be two independent correlation matrices, obtained from 2 populations, each with

zero population correlation coefficients. The determinant of their product is also

a G-function distribution, and its density can be obtained. This result is among

those which extend relations obtained in the univariate case by Pham-Gia and Turkkan

[24] , and also has potential applications in

several domains.

be two independent correlation matrices, obtained from 2 populations, each with

zero population correlation coefficients. The determinant of their product is also

a G-function distribution, and its density can be obtained. This result is among

those which extend relations obtained in the univariate case by Pham-Gia and Turkkan

[24] , and also has potential applications in

several domains.

THEOREM 3: Let

and

and

be two independent random samples from

be two independent random samples from

and

and

respectively, both

respectively, both

being diagonal. Then the determinant

being diagonal. Then the determinant

of the product

of the product

of the two correlation matrices

of the two correlation matrices

and

and

has density:

has density:

, (14)

, (14)

where

and

and .

.

PROOF: Immediate by using multiplication of G-densities presented in [23] .

QED.

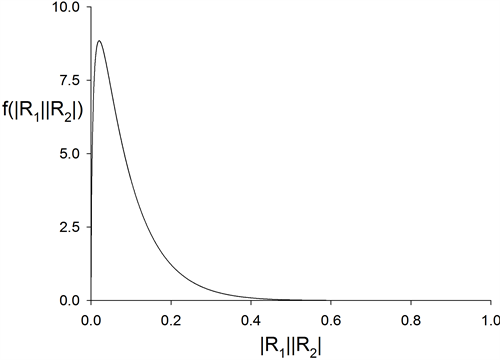

Figure 3 shows the density of , for

, for ,

,

and

and ,

, .

.

Using again results presented in [23]

we can similarly derive the density of the ratio

in terms of G-functions. Its expression is not given here to save space but is available

upon request.

in terms of G-functions. Its expression is not given here to save space but is available

upon request.

4.3. Particular Cases

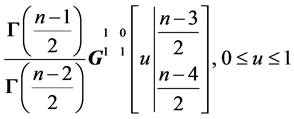

1) Bivariate normal case: a) for the bivariate case we have , and when

, and when

is zero, we have from (11) the density of

is zero, we have from (11) the density of

as

as

which is the G-function form of the beta

which is the G-function form of the beta . Hence, the distribution

of

. Hence, the distribution

of

is:

is: ,

,

, and the density of r is:

, and the density of r is:

Figure 3. Density of product of independent correlation determinants.

, (15)

, (15)

for . Testing

. Testing

is much simpler when using Student’s t-distribution,

is much simpler when using Student’s t-distribution,

, and is covered in most textbooks.

, and is covered in most textbooks.

Pitman [25] has given an interesting distribution-free

test when .

.

2) When

Hotelling ([4] ) gave the density of

Hotelling ([4] ) gave the density of

as:

as:

(16)

(16)

where

is Gauss hypergeometric function with parameters

is Gauss hypergeometric function with parameters

and c.

and c.

3) Mixture of Normal Distributions: With X coming now from the mixture: ,

,

, Gupta and Nagar [21]

consider

, Gupta and Nagar [21]

consider , and give the density

of W in terms of Meijer G-functions, but for the case

, and give the density

of W in terms of Meijer G-functions, but for the case

only. The complicated form of this density contains the hypergeometric function

only. The complicated form of this density contains the hypergeometric function , as expected.

, as expected.

For the bivariate case, Nagar and Castaneda [20]

established the density of r and gave its expression for both cases,

and

and . In the first case

the density of r, when only one population is considered, reduces to the expression

obtained by Hotelling [4] above.

. In the first case

the density of r, when only one population is considered, reduces to the expression

obtained by Hotelling [4] above.

5. Dependence between Components of a Random Vector

5.1. Dependence and

Correlation is useful in multiple regression analysis, where it is strongly related

to collinearity. As an example of how individual correlation coefficients are used

in regression, the variance inflation factor (VIF), well adopted now in several

statistical softwares, measures how much the variance of a coefficient is increased

by collinearity, or in other words, how much of the variation in one independent

variable is explained by the others. For the j-th variable,

is the j-th diagonal element of

is the j-th diagonal element of . We know that it equals

. We know that it equals , with

, with

being the multiple correlation of the j-th variable regressed on the remaining

being the multiple correlation of the j-th variable regressed on the remaining

others.

others.

When all correlation measures are considered together, measuring intercorrelation

by a single number has been approached in different ways by various authors. Either

the value of

or those of its latent roots can be used. Rencher ([26]

, p. 21) mentions six of these measures, among them

or those of its latent roots can be used. Rencher ([26]

, p. 21) mentions six of these measures, among them , where

, where

is an observed value of R, and takes the value 1 if the variables are independent,

and 0 if there is an exact linear dependence. But since the exact distribution of

R is not available this sample measure is rather of descriptive type and no formal

inferential process has really been developed.

is an observed value of R, and takes the value 1 if the variables are independent,

and 0 if there is an exact linear dependence. But since the exact distribution of

R is not available this sample measure is rather of descriptive type and no formal

inferential process has really been developed.

Although the notion of independence between different components of a system is of widespread use in the study of the system structure, reliability and performance, its complement, the notion of dependence has been a difficult one to deal with. There are several dependence concepts, as explained by Jogdev [27] , but using the covariance matrix between different components in a joint distribution remains probably the most direct approach. Other more theoretical approaches, are related to the relations between marginal and joint distributions, and Joe [28] can be consulted on these approaches. Still, other aspects of dependence are explored in Bertail et al. [29] . But two random variables can have zero correlation while being dependent. Hence, no-correlation and independence are two different concepts, as pointed out in Drouet Mari and Kotz [30] . Furthermore, for two independent events, the product of their probabilities gives the probability of the intersection event, which is not necessarily the case for two non-correlated events. Fortunately, these two concepts are equivalent, when the underlying population is supposed normal, a hypothesis that we will suppose in this section.

5.2. Inner Dependence of a System

When considering only two variables, several measures of dependence have also been

suggested in the literature (Lancaster [31] ),

and especially in system reliability (Hoyland and Rausand

[32] ), but a joint measure of the degree of dependence between several

components of a random vector, or within a system , or inner dependence of

, or inner dependence of , denoted by

, denoted by , is still missing. We approach

this dependence concept here by way of the correlation matrix, where a single measure

attached to it would reflect the overall degree of dependence. This concept has

been presented first in Bekker, Roux and Pham-Gia [33]

, to which we refer for more details. It is defined as

, is still missing. We approach

this dependence concept here by way of the correlation matrix, where a single measure

attached to it would reflect the overall degree of dependence. This concept has

been presented first in Bekker, Roux and Pham-Gia [33]

, to which we refer for more details. It is defined as , with

, with . The measure of independence

within the system is then

. The measure of independence

within the system is then

, estimated by

, estimated by , where

, where

is a point estimation of

is a point estimation of

based on R, the correlation matrix associated with a sample of n observations of

the p-component system. In the general case this estimation question is still unresolved,

except for the binormal case,

based on R, the correlation matrix associated with a sample of n observations of

the p-component system. In the general case this estimation question is still unresolved,

except for the binormal case, . We then have

. We then have , and

, and , where

, where

is the coefficient of correlation with its estimation well known, depending on either

is the coefficient of correlation with its estimation well known, depending on either

is supposed to be zero or not. The associated sample measure being

is supposed to be zero or not. The associated sample measure being , it is of interest to

study the distribution of the sample inner dependence

, it is of interest to

study the distribution of the sample inner dependence , based on a sample of n observations

of the system.

, based on a sample of n observations

of the system.

In the language of Reliability Theory, a p-component normal system is fully statistically

independent when the

correlation coefficients

correlation coefficients

of its components are all zero. We have:

of its components are all zero. We have:

THEOREM 4: 1) Let the fully statistically independent system

have p components with a joint normal distribution with

have p components with a joint normal distribution with , where

, where .

.

a) Then the distribution of the sample coefficient of inner dependence

is:

is:

(17)

(17)

b) For the two-component case (p = 2), we have:

(18)

(18)

2) For a non-fully independent two-component binormal system , for

, for :

:

(19)

(19)

where

and

and

is Gauss hypergeometric function.

is Gauss hypergeometric function.

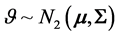

PROOF: a) For , the density of

, the density of , as given by (17), is obtained

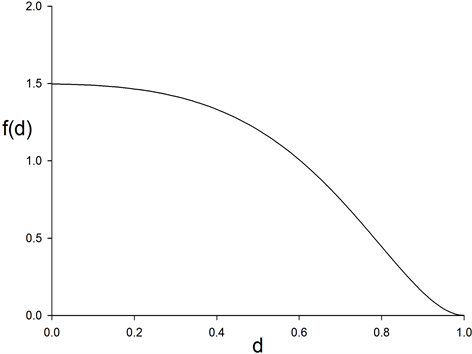

from (11) by a change of variable. Figure 4 gives

the density of the sample coefficient of inner dependence

, as given by (17), is obtained

from (11) by a change of variable. Figure 4 gives

the density of the sample coefficient of inner dependence , for n = 10 and p = 4.

, for n = 10 and p = 4.

Expression (18) is obtained from (15) by the change of variable . Again, the density of

d, as given by (19), can be derived from (16) by considering the same change of

variable. QED.

. Again, the density of

d, as given by (19), can be derived from (16) by considering the same change of

variable. QED.

Numerical computations give . Estimation of

. Estimation of

from

from

now follows the same principles as

now follows the same principles as

from r.

from r.

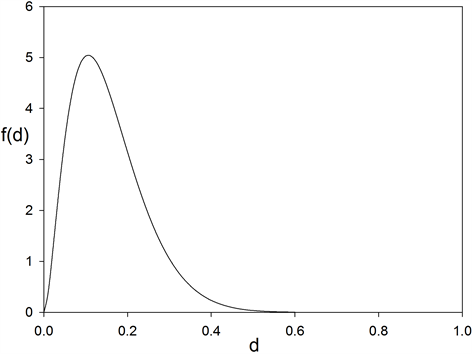

Figure 5 gives the density , as given by (19), for

n = 8, p = 2,

, as given by (19), for

n = 8, p = 2, .

.

6. Conclusion

In this article we have established an original expression for the density of the correlation matrix, with the sample variances as parameters, in the case of the multivariate normal population with non-identity population correlation matrix. We have, furthermore, established the expression of the distribution of the determinant of that random matrix in the case of identity population correlation matrix, and computed its value. Applications are

Figure 4. Density (17)

for sample coefficient of inner dependence

(normal system with four components, n = 10, p = 4).

(normal system with four components, n = 10, p = 4).

Figure 5. Density (19)

of sample measure of a binormal system dependence, .

.

made to the dependence among p components of a system. Also, expressions for the densities of a sample measure of a system inner dependence are established.

References

- Johnson, D. (1998) Applied Multivariate Methods for Data Analysis. Duxbury Press, Pacific Grove.

- Fisher, R.A. (1962) The Simultaneous Distribution of Correlation Coefficients. Sankhya, Series A, 24, 1-8.

- Pham-Gia, T. and Turkkan, N. (2011) Distributions of the Ratio: From Random Variables to Random Matrices. Open Journal of Statistics, 1, 93-104. http://dx.doi.org/10.4236/ojs.2011.12011

- Hotelling, H. (1953) New Light on the Correlation Coefficient and Its Transform. Journal of the Royal Statistical Society: Series B, 15, 193.

- Olkin, I. and Pratt, J.W. (1958) Unbiased Estimation of Certain Correlation Coefficients. Annals of Mathematical Statistics, 29, 201-211. http://dx.doi.org/10.1214/aoms/1177706717

- Joarder, A.H. and Ali, M.M. (1992) Distribution of the Correlation Matrix for a Class of Elliptical Models. Communications in Statistics—Theory and Methods, 21, 1953-1964. http://dx.doi.org/10.1080/03610929208830890

- Ali, M.M., Fraser, D.A.S. and Lee, Y.S. (1970) Distribution of the Correlation Matrix. Journal of Statistical Research, 4, 1-15.

- Fraser, D.A.S. (1968) The Structure of Inference. Wiley, New York.

- Schott, J. (1997) Matrix Analysis for Statisticians. Wiley, New York.

- Kollo, T. and Ruul, K. (2003) Approximations to the Distribution of the Sample Correlation Matrix. Journal of Multivariate Analysis, 85, 318-334. http://dx.doi.org/10.1016/S0047-259X(02)00037-4

- Farrell, R. (1985) Multivariate Calculation. Springer, New York. http://dx.doi.org/10.1007/978-1-4613-8528-8

- Gupta, A.K. and Nagar, D.K. (2000) Matrix Variate Distribution. Hall/CRC, Boca Raton.

- Mathai, A.M. and Haubold, P. (2008) Special Functions for Applied Scientists. Springer, New York. http://dx.doi.org/10.1007/978-0-387-75894-7

- Kshirsagar, A. (1972) Multivariate Analysis. Marcel Dekker, New York.

- Muirhead, R.J. (1982) Aspects of Multivariate Statistical Theory. Wiley, New York. http://dx.doi.org/10.1002/9780470316559

- Fisher, R.A. (1915) The Frequency Distribution of the Correlation Coefficient in Samples from an Indefinitely Large Population. Biometrika, 10, 507-521.

- Stuart, A. and Ord, K. (1987) Kendall’s Advanced Theory of Statistics, Vol. 1. 5th Edition, Oxford University Press, New York.

- Sawkins, D.T. (1944) Simple Regression and Correlation. Journal and Proceedings of the Royal Society of New South Wales, 77, 85-95.

- Pham-Gia, T., Turkkan, N. and Vovan, T. (2008) Statistical Discriminant Analysis Using the Maximum Function. Communications in Statistics-Simulation and Computation, 37, 320-336. http://dx.doi.org/10.1080/03610910701790475

- Nagar, D.K. and Castaneda, M.E. (2002) Distribution of Correlation Coefficient under Mixture Normal Model. Metrika, 55, 183-190. http://dx.doi.org/10.1007/s001840100139

- Gupta, A.K. and Nagar, D.K. (2004) Distribution of the Determinant of the Sample Correlation Matrix from a Mixture Normal Model. Random Operators and Stochastic Equations, 12, 193-199.

- Springer, M. (1984) The Algebra of Random Variables. Wiley, New York.

- Pham-Gia, T. (2008) Exact Distribution of the Generalized Wilks’s Statistic and Applications. Journal of Multivariate Analysis, 99, 1698-1716. http://dx.doi.org/10.1016/j.jmva.2008.01.021

- Pham-Gia, T. and Turkkan, N. (2002) Operations on the Generalized F-Variables, and Applications. Statistics, 36, 195-209. http://dx.doi.org/10.1080/02331880212855

- Pitman, E.J.G. (1937) Significance Tests Which May Be Applied to Samples from Any Population, II, the Correlation Coefficient Test. Supplement to the Journal of the Royal Statistical Society, 4, 225-232. http://dx.doi.org/10.2307/2983647

- Rencher, A.C. (1998) Multivariate Statistical Inference and Applications. Wiley, New York.

- Jogdev, K. (1982) Concepts of Dependence. In: Johnson, N. and Kotz, S., Eds., Encyclopedia of Statistics, Vol. 2, Wiley, New York, 324-334.

- Joe, H. (1997) Multivariate Models and Dependence Concepts. Chapman and Hall, London. http://dx.doi.org/10.1201/b13150

- Bertail, P., Doukhan, P. and Soulier, P. (2006) Dependence in Probability and Statistics. Springer Lecture Notes on Statistics 187, Springer, New York. http://dx.doi.org/10.1007/0-387-36062-X

- Drouet Mari, D. and Kotz, S. (2004) Correlation and Dependence. Imperial College Press, London.

- Lancaster, H.O. (1982) Measures and Indices of Dependence. In: Johnson, N. and Kotz, S., Eds., Encyclopedia of Statistics, Vol. 2, Wiley, New York, 334-339.

- Hoyland, A. and Rausand, M. (1994) System Reliability Theory. Wiley, New York.

- Bekker, A., Roux, J.J.J. and Pham-Gia, T. (2005) Operations on the Matrix Beta Type I and Applications. Unpublished Manuscript, University of Pretoria, Pretoria.